Hussman Funds

Mountain, Cliff, or Ocean

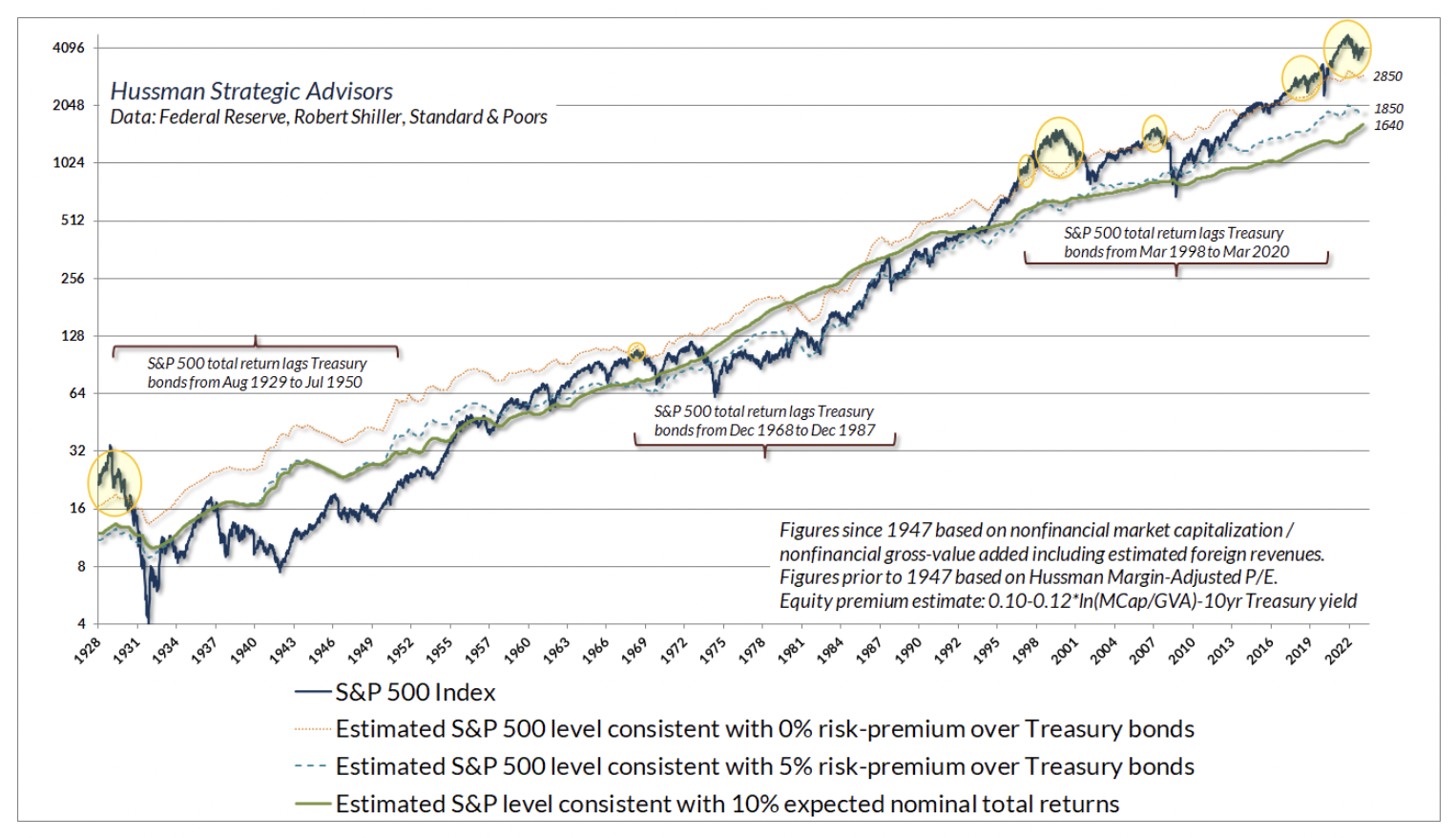

The current level of stock market valuations remains – easily – the most speculative extreme in U.S. financial history, beyond both the 1929 and 2000 extremes. Our baseline estimate is that the S&P 500 has a material risk of losing something on the order of 75% over the completion of this cycle.

Record Extremes, Alternative Investments, and the Hippo

The essential feature of a useful alternative asset isn’t that it’s unusual or exotic, but that its returns aren’t tightly linked to the risks that already dominate the portfolio. The value of an alternative asset comes from the way it interacts with the other assets in the portfolio.

(More) Roses Amid Garbage and Trap Doors

What to do? Does one capitulate and chase the bubble at the highest valuations in history? Does one wring their hands at the prospect of a bubble that might only go higher and higher forever without end? My hope is that this month’s comment will offer both perspective and confidence that it is not necessary to chase current extremes, nor to be anxious even about the possibility of steeper ones.

Causes and Conditions

The defining feature of a Ponzi scheme is that it persuades investors to pay for future cash flows that, at least in part, don’t actually exist, while creating the impression that those cash flows imply an attractive return on the price investors pay. If we look carefully at the record valuation extremes in the equity market, and the wildly elevated profit margins that investors appear to view as permanent, we can already see the potential for difficult, even tragic outcomes for investors.

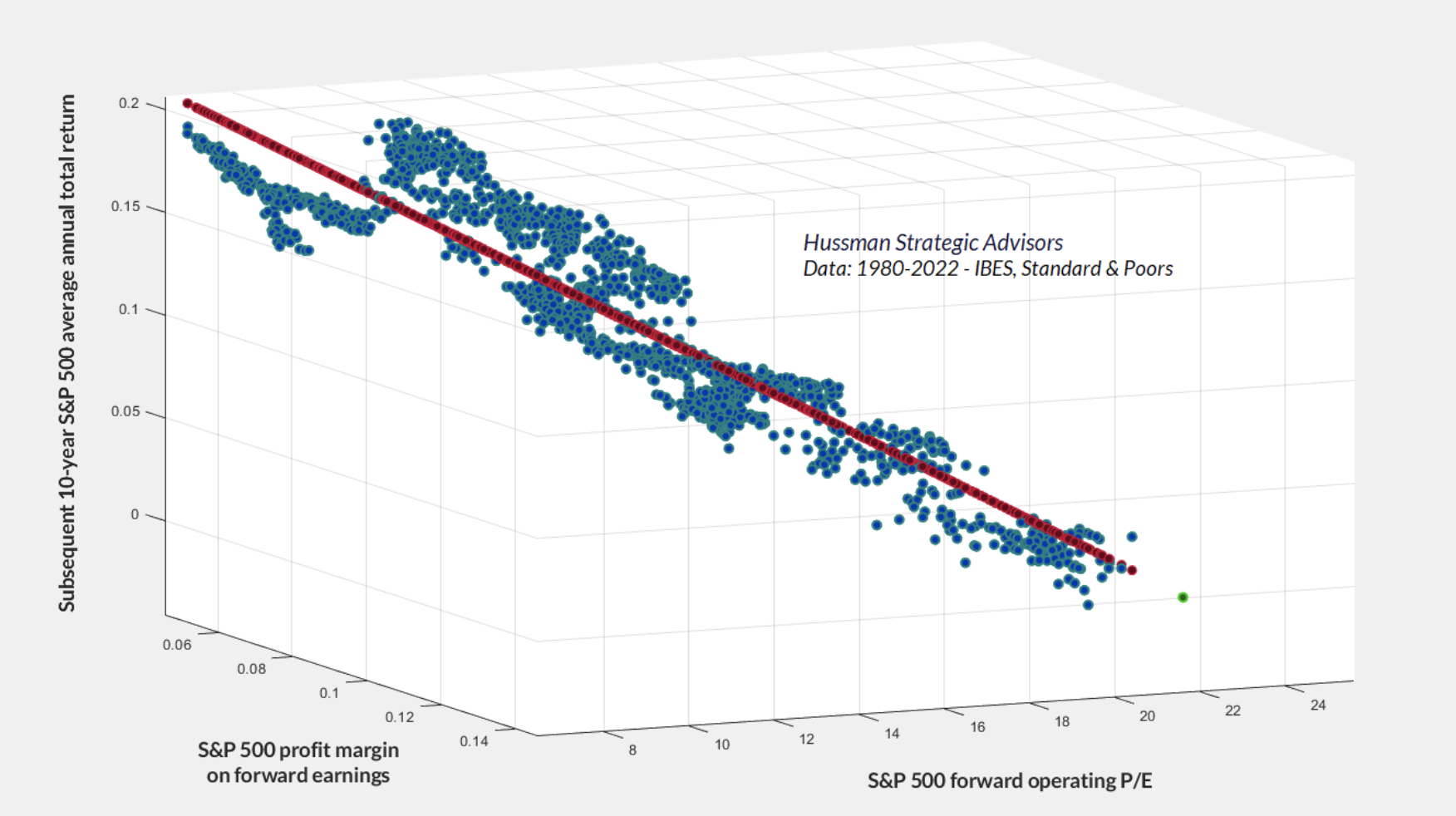

Extreme Earnings Forecasts Mask Stock Market Risk

In elevated financial markets, risk is rarely eliminated. It is usually only relocated. During the run-up to the 2008 financial crisis, mortgage risk did not disappear. It was transformed, repackaged, and spread across the system in ways that made it appear safer than it was.

Equilibrium and the Dentist in Poughkeepsie

The word 'equilibrium' is an invitation to recognize that nothing exists by itself, alone. Subject and object are two sides of the same coin – their interaction is a single phenomenon. That perspective can offer a great deal of insight about economics, financial markets, speculative bubbles, passive investing, and nearly everything in existence.

How I Learned To Love the Bubble (Even Before it Bursts)

To love a bubble but hate a crash is to misunderstand the market. A bubble is a crash on its way to becoming. A crash is a bull market on its way to becoming. All we can do is to accept, and as difficult as it may be – embrace – whatever form we have in the present moment, so we can do our best with each of them.

Record Stock Valuations, Fed Independence, and Macro Volatility

As political pressure on the Federal Reserve intensifies and markets ponder the nomination of a new Chair, understanding this chain of risk is increasingly important for investors. Equity valuations are heavily affected by expectations for long-term cash flows, along with the interest rates and risk-premiums that drive how much investors are willing to pay for those future dollars.

How the Bubble Manipulates Time

The defining feature of every bubble is the same: a growing inconsistency between the long-term returns that investors expect in their heads - based on extrapolation of the past, and the long-term returns that properly relate prices to likely future cash flows - based on valuations. Every bubble smuggles the same tragic past into the same tragic future by packaging it with new wrinkles that convince investors that this time is different. Ultimately, they still end the same way.

A Payroll Playbook to Gauge Recession Risk

With the federal government open after its longest shutdown on record, we will soon get a clear indication of how payrolls fared in September and October.

An Unsustainable Equilibrium

As I detailed in August, our most reliable valuation measures – based on their relationship with actual subsequent S&P 500 total returns across a century of market history – suggest that the expectations of investors for long-term market returns are wildly misaligned with the returns implied by discounted cash flows.

Singularity and the Buzzard

Division by zero is known as a “singularity.” It’s the point where equations break down, values become “indeterminate,” things stop working normally, and variables shoot toward infinity and suddenly collapse on the other side.

The Bubble Term

The word “bubble” gets tossed around quite a bit. Usually, it comes in the form of verbal arguments about whether prices have advanced to a point that’s “too high” in some sense. We can do much better than that. A bubble is a mathematical object.

The Impression of Invincibility

With our most reliable stock market valuation measures at the highest extremes in U.S. history, it’s useful for investors to remember that a market crash is nothing but risk-aversion meeting a market that is not priced to tolerate risk.

The Bubble – Contains the Collapse – Contains the Resurgence

When investors approach the financial markets, there’s a tendency to imagine that conditions can be judged as favorable or unfavorable based on one single measure or another. The fact is that market conditions at any moment in time are a composite of interdependent forces.

An Abrupt and Cascading Dislocation

While we remain open to changes in market conditions, as well as periodic “fast, furious, prone-to-failure” advances that can relieve the oversold “compression” produced by market losses, we are presently on high alert for a possibly abrupt and cascading market and economic dislocation in the weeks ahead.

Humpty Dumpty Was Pushed

The stock market faces severe downside risk ahead, and the U.S. is constrained in the unsystematic monetary and fiscal expansion that both amplified that bubble and fueled record but wholly impermanent corporate profit margins. Meanwhile, the U.S. economy now faces an imminent recession, and if we fail to be vigilant, we, once united Americans, risk losing what is far greater and more valuable than money.

How To Survive Falling Markets

One of the biggest challenges investors face today is navigating the most concentrated U.S. stock market in history, where the largest stocks represent a record share of total market value.

The Government Deficits Land in the Deepest Pockets

With our most reliable valuation measures more extreme than both the 1929 and 2000 market peaks, we continue to believe that the stock market is tracing out the extended peak of the third great speculative bubble in U.S. history.

Slimming Down a Top-Heavy Market

The strong performance of large-cap stocks over the past decade has left the market exceptionally top-heavy. By some measures, stock market capitalization has never been more concentrated among a handful of large stocks as today.

Pressing for Yet More

On December 6, the S&P 500 set the most extreme level of valuations on record, exceeding both the 1929 and 2000 market peaks on measures that we find best-correlated with actual, subsequent 10-12 year S&P 500 total returns across a century of market cycles.

Ring Out, Wild Bells

On Friday December 6th, the U.S. stock market pushed to the most extreme level of valuation in U.S. history

The Turtle and the Pendulum

Change is the sum of fundamental trends, the gradual elimination of accumulated extremes, and the random arrival of new shocks.

Subsets and Sensibility

One of most dangerous habits of a speculative crowd is the tendency to use unconditional averages and unconditional probabilities regardless of how extreme market conditions have become. This is like stepping into a house with two rooms, one with the temperature at 0 degrees and one at 140 degrees, and expecting a temperature of 70 either way.

Asking a Better Question

On September 18, the Federal Reserve cut the Federal funds rate, as expected, announcing at the same time that the Fed will continue to reduce its balance sheet. In my view, both of these decisions were appropriate. The Fed reduced short-term rates by 50 basis points, which was consistent with economic conditions that remain near the threshold of recession.

Fed Pivots and Baby Aspirin

When you see that behavior at extreme valuations, it tends to be a sign of underlying skittishness and risk aversion. When valuations are setting record extremes because the news can’t get any better, even a slightly less optimistic outlook becomes a risk.

Going All In – The Bubble in Profit Expectations

During each speculative run-up in asset prices – whether the dot-com bubble, the housing bubble, or more recently the rapid rise (and fall) of the stocks of electric vehicle companies – there’s typically a moment when Wall Street strategists, analysts, and investors go all-in on that theme.

You’re Soaking in It

The stock market is not a balloon that gets bigger when money “flows into” it. It doesn’t get smaller because money “flows out” of it. Holding the number of shares constant, the stock market gets bigger if investors pay a higher price for those shares. Period.

You Can Ring My Bell

I may as well just say it. Based on the present combination of extreme valuations, unfavorable and deteriorating market internals, and a rare preponderance of warning syndromes in weekly and now daily data, my impression is that the speculative market advance since 2009 ended last week.

This Is Where You Start Bear Markets From

As of last week, the total return of the S&P 500 was even with 3-month Treasury bill returns since the valuation peak of January 2022, more than two years ago. In our view, investors continue to “grasp at the suds of yesterday’s bubble,” ignoring extreme valuations, lopsided bullish sentiment, emerging pressure on profit margins, economic conditions at the border of recession...

Universal Capitulation and No Margin of Safety

Based on the valuation measures we find best-correlated with actual subsequent S&P 500 total returns across a century of market cycles, the stock market presently stands at valuation extremes matched only twice in U.S. financial history.

Speculative Euphoria and the Fear of Missing Out

If you’re losing your mind and plagued by fear of missing out, it might be that you’re best served with some passive investment exposure in your portfolio. Not because it will do well, at least not in our estimation, but so you don’t lose your mind.

Cluster of Woe

As I observed last month, the strongest stock market returns in the coming decade, perhaps longer, are likely to emerge during advances in the S&P 500 that attempt to catch up with the cumulative return of risk-free Treasury bills.

The Return of Buy-Low Sell-High

The strongest stock market returns in the coming decade, perhaps longer, are likely to emerge during advances in the S&P 500 that attempt to catch up with the cumulative return of risk-free Treasury bills.

The Secret Life of Fed Pivots

It’s worth noting that despite the recent market advance, our own investment discipline, and even Treasury bills, have outpaced the S&P 500 and Nasdaq 100 during this period, with less volatility.

Soft Selling a Hard Landing

For the better part of two years, investors have been primed with hope of a “Fed pivot” that will presumably restore easy monetary policy and supportive conditions for the financial markets.

Seven Reminders While on Recession Watch

A recent survey asking economists about the probability of recession next quarter shows a retreat in expectations from a high of 47 percent at the end of 2022 to just 34 percent, according to the Philadelphia Federal Reserve.

When the Bough Breaks

Value-conscious, historically-informed, full-cycle investors place a great deal of emphasis on the relationship between the price an investor pays today and the cash flows they can expect to receive in the future. The reason is simple.

Central Bankers Wandering in the Woods

On the interest rate front, the Federal funds rate is now close to systematic benchmarks that have historically been consistent with prevailing core inflation, nominal GDP growth, and unemployment.

Air Pockets, Free Falls, and More Cowbell

There is a particular “setup” that we’ve historically found to be associated with abrupt “air pockets” and “free falls” in the S&P 500. It combines hostile conditions in all three features most central to our investment discipline: rich valuations, unfavorable market internals, and extreme overextension.

Grasping at the Suds of Yesterday’s Bubble

Bull markets and bear markets can’t be identified in real-time – only in hindsight. More importantly, the return/risk profile of a “bull market” or a “bear market” can change dramatically depending on whether valuations are consistent with the beginning of a market cycle or the end of one.

Money, Banking, and Markets – Connecting the Dots

Most of us spent moments of our childhood, crayon in hand, connecting numbered dots that gradually revealed a picture that we couldn’t deduce simply by looking at the separate dots. With experience, we got better at looking at those isolated dots and mentally connecting them into a coherent “gestalt.”

Fabricated Fairy Tales and Section 2A

Amid the overabundance of economic opinion, unexamined clichés, and unverified assertions, and nutrient-free word salad dispensed by talking heads on television, market observers, and even Federal Reserve officials, I often wonder how many of them have ever taken the time to carefully examine historical data.

Pushing Your Luck

The problem with speculation is that there’s usually a gap between the underlying risk and the inevitable outcome.

Pushing Your Luck

The problem with speculation is that there’s usually a gap between the underlying risk and the inevitable outcome.

They’ve Ruled Out Tail Risk

As of Friday, December 16, the S&P 500 Index is down -19.7% from the most speculative level of valuations in U.S. history – exceeding even the 1929 and 2000 extremes, based on the valuation measures we find best-correlated with actual subsequent market returns in cycles across history.

December 2022 Portfolio Notes

We continue to believe that a value-conscious, risk-managed, full-cycle discipline, focused on the combination of valuations and market internals, will be essential in navigating market volatility in the years ahead.

Weighing Machine, Voting Machine

Two aspects of the financial markets operate simultaneously. Emphatically, they do not operate alternately, but simultaneously. One aspect is driven entirely by arithmetic. Every security is a claim to some long-term stream of cash flows that will be delivered to the holder, or series of holders, over time.

Estimating Downside Market Risk

At the beginning of 2022, our most reliable stock market valuation measures stood at record levels, beyond even their 1929 and 2000 extremes. The 10-year Treasury yield was at 1.5%, the 30-year Treasury bond yield was at 1.9%, and Treasury bill yields were just 0.06%. By our estimates, that combination produced the most negative expected return for a conventional passive investment portfolio in U.S. history.

Now Comes the Hard Part

Surveying the current condition of the financial markets, we presently observe a combination of still historically-extreme valuations, rising yet still only normalizing interest rates, measurably inadequate risk-premiums in both equities and bonds, and ragged, unfavorable market internals, suggesting continued risk-aversion among investors.

The Structural Drivers of Investment Returns

After more than 40 years of work in the financial markets, studying all the data I could get my hands on, I’ve found it to be universally true that those who argue “history doesn’t matter” have never actually studied history.

The Structural Drivers of Investment Returns

After more than 40 years of work in the financial markets, studying all the data I could get my hands on, I’ve found it to be universally true that those who argue “history doesn’t matter” have never actually studied history.

Are We There Yet?

Lao Tzu wrote, “A journey of a thousand miles begins with a single step.”

Making Friends with Bears Through Math

A fascinating aspect of the financial markets is that long-term returns are driven almost entirely by math, while short-term returns are driven almost entirely by psychology.

Repricing a Market Priced for Zero

The most challenging financial event for investors in the coming decade will be the repricing of securities to valuations that imply adequate long-term returns, following more than a decade of reckless and intentional Fed-induced yield-seeking speculation.

Return-Free Risk

In an economy where the Fed has lost every systematic tether to common sense, empirical evidence, and concern for financial stability, it’s worth beginning this first market comment of 2022 by recalling the ways we’ve adapted in order to navigate that environment.

Collision Course: Monetary Tightening Meets an Easy Money Bubble

Whether investors are ready or not, global monetary tightening cycles are fast approaching.

Motherlode

There are certain features of valuation, investor psychology, and price behavior that emerge, to one degree or another, when the fear of missing out becomes particularly extreme and the focus of speculation becomes particularly narrow. We’ve suddenly hit a motherlode of those conditions. Emphatically, this is not a forecast. It's a statement about current, observable conditions.

When Bubble Meets Trouble

Speculative psychology is the only thing standing between an hypervalued market that continues to advance and a hypervalued market that drops like a rock. Our best gauge of that psychology - the uniformity of market internals - remains divergent enough to keep market conditions in a trap-door situation.

The Wealth Is In The Denominator

Among the illusions encouraged by every speculative bubble is the idea that wealth is embodied in the prices of securities – that higher prices inherently represent greater “wealth.” The fact is that every security is, at base, a claim to some future stream of cash flows that will be delivered into the hands of investors over time.

Maladaptive Beliefs

Among the most persistent questions I hear is why we don’t just adapt to the reality that the Federal Reserve will never again “allow” the market to experience a serious decline. The problem with this view is that it rests on the premise that Federal Reserve policy supports the market in a clear-cut and mechanical way, when its effectiveness actually relies on the speculative psychology of investors.

The Folly of Ruling Out a Collapse

A remarkable feature of extended bull markets is that investors come to believe – even in the face of extreme valuations – that the world has changed in ways that make steep market losses and extended periods of poor returns impossible.

What Triggered the Crash?

The title of this comment may seem odd, given that – as I write this on July 14, 2021 – the S&P 500 is at a record high.

Alice’s Adventures in Equilibrium

Coherent thinking is interested in how things are related; where they come from, where they go, and the mechanisms by which they affect each other.

Counting the Chickens Twice

There’s an old bit of advice that one shouldn’t count one’s chickens before they’re hatched.

Always a Reckoning

From 1949 through 1964, the S&P 500 enjoyed an average annual total return of 16.4%. In the 8 years that followed, through 1972, the total return of the index averaged a substantially lower 7.6% annually; strikingly close to the 7.5% projection that Graham had suggested based on prevailing valuations, yet still providing what Graham had suggested would likely “carry a fair degree of protection” against inflation, which averaged 3.9% over that period.

How to Spot a Bubble

The word “bubble” is tossed around quite a bit in the financial markets, but it’s rarely used correctly.

Detached Parabolas and Open Trap Doors

Nothing so animates a speculative herd as a parabolic price advance in an asset detached from any standard of value. I am convinced that future generations will use the present moment to define the concept of a reckless speculative extreme, in the same way our generation uses “1929” and “2000.”

The Speculative “V”

The speculative “V” is one of the most interesting and challenging features of the market cycle. For passive investors, it can be a period of exhilaration followed by panic.

A Good Response to a Bad Situation

I should start by saying that I’ve got great admiration for Robert Shiller. Even three decades ago when I was completing my doctorate at Stanford, I avidly embraced his work, including his studies on excess volatility. He has originated an impressive range of useful tools, including the Case-Shiller housing price indices. As the tech bubble was peaking in 2000, I doubt that any 30-something in finance was more pleased to see Shiller become a widely-quoted figure in the financial markets. All of that is important to say, before I tear into this particular metric.

Hypervaluation and the Option Value of Cash

One of the most insidious ideas foisted on investors by Wall Street, in tacit cooperation with activist policy makers at the Federal Reserve, is the fiction that zero interest rates offer investors “no alternative” but to speculate in risky securities.

Pushing Extremes

In calling the current market the third “Real McCoy” bubble of recent decades, Jeremy Grantham described, in his own words, what I call the Iron Law of Valuation: a security is nothing more than a claim on some set of future cash flows that investors expect to be delivered into their hands over time. The higher the price an investor pays today for some amount of cash in the future, the lower the long-term return the investor can expect on that investment.

Herd Mentality

Here in the U.S., I estimate that the actual number of people infected by SARS-CoV-2 to-date is currently just over four times the number of reported cases. Actual cases are undercounted partly because, based on very large-scale, unbiased testing, roughly 45% of people who acquire SARS-CoV-2 infection are asymptomatic.

Yikes

You know it’s a bubble when you have to edit the Y axis on all of your charts because valuations have broken above every historical peak, and estimated future market returns have fallen beyond the lowest points in history, including 1929.

Avoiding a Second Wave

About two-thirds of this month’s comment is about COVID-19 and the risk of a second wave. This is not only for the sake of public health, which would be enough, and not only to contribute to a better understanding of the epidemic.

Fundamentally Unsound

Saying that extreme stock market valuations are “justified” by low interest rates is like saying that poking yourself in the eye is “justified” by smashing your thumb with a hammer.

Incubation Phase: Gradually and then Suddenly

Severe economic recessions often feature what might be called an “incubation phase,” where an exuberant rebound from initial stock market losses becomes detached from the quiet underlying deterioration of economic fundamentals and corporate balance sheets.

Amygdalotomy: Surviving the Intentional Demolition of Warning Signs

A compassionate society has both economic reason and ethical responsibility to provide a social safety net to its most vulnerable members. It is an act of both economic insanity and ethical corruption to provide a financial safety net to its most reckless speculators.

Containing the Crisis

Amid the current crisis, a forceful economic policy response is essential. The central principle here is that the closer we can get economic support to the point where current spending enters the “circular flow” – basic incomes, net rent and lease obligations, utilities, contractual payments, even net interest payments, the better we can support the entire economy.

Navigating Turbulence

I expect that the most valuable aspect of our investment discipline over the completion of this cycle will be our ability and willingness to flexibly respond to changes in observable market conditions as they emerge.

Clearing Rallies and Crashes (Buckle Up)

From a full-cycle perspective, the decline in the U.S. stock market from its recent high remains something of a non-event, compared with the probable market loss over the completion of this cycle.

Make Good Choices!

There are two key drivers of investment returns. One is valuations, which provide a great deal of information about long-term investment prospects, and about the income component of total returns. The other is the uniformity or divergence of prices across thousands of individual securities, which helps to distinguish whether shorter-term investor psychology is inclined toward speculation or risk-aversion.

Whatever They’re Doing, It’s Not “Investment”

Understand this. The more glorious this bubble becomes in hindsight, the more dismal future investment returns become in foresight. The higher the price investors pay for a set of future cash flows, the lower the return they will enjoy over time. Whatever they’re doing, it’s not “investment.”

One Tier and Rubble Down Below

One of the striking things about bull markets is that they often end in confident exuberance, while simultaneously deteriorating from the inside. We’ve certainly observed this sort of selectivity during the past year. The market advance in 2019 fully recovered the market losses of late-2018, fueled by a wholesale reversal of Fed policy, hopes for a “phase one” trade deal, and as noted below, a bit of confusion about what actually constitutes “quantitative easing.”

The Meaning of Valuation

The recent half-cycle has been admittedly difficult. My bearish response to historically-reliable “overvalued, overbought, overbullish” syndromes proved detrimental in the face of zero-interest rate policies that amplified speculation, and we’ve adapted our discipline to give priority to our measures of market internals – which we use to gauge that speculation.

Marks of a Phase Transition

By the time a bull market reaches its peak, investors have experienced numerous instances where the market has declined by several percent, followed by an advance to fresh highs.

A Striking Collection of Duck-Like Features

One of the pitfalls of identifying market conditions using labels like “bull market” and “bear market” is that the accuracy of those labels can only be verified in hindsight.

Propositions for a Recessionary Bear Market

As the financial markets enter what I expect to be a rather disruptive completion to the recent speculative half-cycle, it will be helpful for investors to consider certain propositions that are readily available from history, rather than insisting on re-learning them the hard way.

Going Nowhere in an Interesting Way

Not surprisingly, the higher the valuation at the bull market peak, the longer the subsequent period of disappointing returns, in several instances extending more than a decade, though not without intermittent failure-prone bull market rallies to add excitement. This is what I often call ‘going nowhere in an interesting way.’

How to Needlessly Produce Inflation

What distinguishes an overvalued market that continues to advance from an overvalued market that often drops like a rock? In my view, it’s the psychological disposition of investors toward speculation or risk-aversion.

They’re Running Toward the Fire

While investors appear exuberant about the prospect for Fed easing, they seem largely unaware that initial Fed easings have almost invariably been associated with U.S. recessions. They’re running toward the fire.

Warning: Federal Reserve Easing Ahead

Of all the distinctions that investors might make in the coming few years, one that I expect will serve investors particularly well is the distinction between how the market responds to monetary policy when investors are inclined toward speculation, versus how the market responds when investors are inclined toward risk-aversion.

Vulnerable Windows and Swinging Trap Doors

Why do economies collapse into recession in ways that seem so difficult to predict? Why do financial markets collapse into free-fall with timing that’s so loosely related to market valuations? Much of the reason is that complex systems usually aren’t linear.

Why a 60-65% Market Loss Would Be Run-Of-The-Mill

One might view the very comparison of present stock market conditions to 1929 market peak as exaggerated and preposterous, but then, one would be wrong. The fact is that on the valuation measures we find most strongly correlated with actual subsequent long-term and full-cycle market returns across history (and even in recent decades), current market valuations match or exceed those observed at the 1929 peak.

You Are Here

Probably the most useful exercise we can do at present is to examine where the markets and the U.S. economy are in their respective cycles - with 19 charts and detailed analysis. There’s little question that the market is long into what Rhea described as the final phase of a bull market; “the period when speculation is rampant – a period when stocks are advanced on hopes and expectations.”

Ground Rules of Existence

Over the years, I’ve often quoted Galbraith’s remark about the “extreme brevity of the financial memory.” During every speculative episode, investors come to believe that past experience is “the primitive refuge of those who do not have the insight to appreciate the incredible wonders of the present,”...

Turtles All the Way Down

Last week, the Federal Reserve issued policy statements intended to telegraph a shift toward easier, or at least more patient monetary policy. Though Wall Street interpreted this shift as a major about-face in the Fed’s policy stance, the most significant shift in Fed Chair Jerome Powell’s statements actually occurred on November 28.

Questions We Hear a Lot

In recent days, we’ve heard a number of analysts gushing that the S&P 500 is vastly cheaper than it was only a few months ago. It’s worth noting that they’re actually referring to an index that is now less than 10% below the steepest speculative extreme in history.

The Fast and the Furious

Given the steep market decline in recent days, short-term market conditions clearly qualify as “oversold” and highly compressed, in my view.

Bubbles and Hot Potatoes

Of all the delusions that have infected the minds of economists, central bankers, and the investing public in recent years, perhaps none is as short-sighted and pernicious as the idea that aggressively low interest rates are “good” for the economy and the financial markets.

The Heart of the Matter

Let’s be clear. October’s market decline was a rather mild warning shot. At its lowest close, the S&P 500 lost -9.9% from its September peak, before rebounding in recent sessions. As I noted during the 2000-2002 and 2007-2009 collapses, intermittent “fast, furious, prone-to-failure” rebounds are among the factors that encourage investors to hold on through the entirety of major declines.

The Music Fades Out

The music is fading out, and a trap-door has opened up in the floor, but they're still dancing. In recent days, the combination of extreme valuations and unfavorable market internals has been joined by acute dispersion in daily trading data that often occurs within a few days of pre-collapse peaks in the market.

Eternal Sunshine of the Spotless Mind

Current stock market capitalization is largely an artifact of speculative psychology, not reasonably discounted cash flows. Unless investors rely on eternal sunshine of the spotless mind – the assumption that current levels of extreme cyclical optimism will be permanent – they should not expect the associated valuation extremes to be permanent either.

Extrapolating Growth

Market returns and economic growth have underlying drivers. At their core, extended periods of extraordinary growth and disappointing collapse reflect large moves in those drivers from one extreme to another. Extrapolation becomes a very bad idea once those extremes are reached.

Mind the Trap Door

Even when extreme “overvalued, overbought, overbullish” warning signs are present, we now require explicit deterioration in market internals before adopting a negative market outlook. That, however, is far different than saying that extreme conditions can be ignored altogether. With market internals negative here, underlying market risks may be expressed abruptly, and with unexpected severity.

Hallmark of an Economic Ponzi Scheme

The hallmark of an economic Ponzi scheme is that the operation of the economy relies on the constant creation of low-grade debt in order to finance consumption and income shortfalls among some members of the economy, using the massive surpluses earned by other members of the economy. The factors most responsible for today’s lopsided prosperity are exactly the seeds from which the next crisis will spring.

Comfort is Not Your Friend

The overall profile of market conditions continues to feature: 1) hypervaluation on the measures we find best-correlated with actual subsequent S&P 500 total returns, coupled with 2) continued deterioration in our measures of market internals, which are the most reliable tools we’ve found to gauge the psychological inclination of investors toward speculation or risk-aversion.

Risk-Aversion Meets a Hypervalued Market

Investment is about valuation. Speculation is about psychology. Both factors are unfavorable here. We’re observing the very early effects of risk-aversion in a hypervalued market. Based on the deterioration we’ve observed in our most reliable measures of market internals, investor preferences have subtly shifted toward risk-aversion, which opens up something of a trap-door.

The Arithmetic of Risk

In my view, the idea that higher risk means higher expected return is one of the most dangerous and misunderstood propositions in the financial markets. The reason it’s dangerous is that it ignores the central condition: “provided that one is choosing between portfolios that all maximize expected return per unit of risk.” Presently, the S&P 500 is both a high risk and a low expected return asset.

Measuring the Bubble

I expect the S&P 500 to lose approximately two-thirds of its value over the completion of this cycle. My impression is that future generations will look back on this moment and say "... and this is where they completely lost their minds." As I’ve regularly noted in recent months, our immediate outlook is essentially flat neutral for practical purposes, though we’re partial to a layer of tail-risk hedges.

When Speculation Has No Limits

Here we are, nearly three times the level at which I expect the S&P 500 to complete this cycle. Yet our immediate outlook remains neutral (though tail-risk hedges remain appropriate). It’s essential to distinguish between valuations, which have long-term implications, and market internals, which have implications for shorter segments of the market cycle.

Survival Tactics for a Hypervalued Market

The essential survival tactic for a hypervalued market, and its resolution ahead, is to recognize that market valuations can experience breathtaking departures from historical norms for extended segments of the market cycle, so long as shorter-term conditions contribute to speculative psychology rather than risk-averse psychology. Yet those departures matter enormously for long-term returns.

Three Delusions: Paper Wealth, a Booming Economy, and Bitcoin

Delusions are often viewed as reflecting some deficiency in reasoning ability. The risk of thinking about delusions in this way is that it encourages the belief that logical, intelligent people are incapable of delusion. An examination of the history of financial markets suggests a different view.

Navigating the Speculative Id of Wall Street

Valuations are understood best not by trying to “justify” or dismiss current extremes, but by recognizing that across history, the speculative inclinations of investors have periodically allowed valuations to depart dramatically from appropriate norms, at least for limited segments of the complete market cycle.

Brief Observations: Distinctions Matter

Last week, the uniformity of market internals shifted to an unfavorable condition. During the advancing half-cycle since 2009, zero interest rates encouraged speculation (and maintained favorable market internals) long after extreme overvalued, overbought, overbullish conditions emerged. But distinctions matter. Once the uniformity of market internals - the most reliable measure of speculation itself - is knocked away, those extremes are still likely to matter with a vengeance.

This Time Is Different, But Not How Investors Imagine It Is Different

Encouraged by the novelty of zero-interest rates, not even the most extreme “overvalued, overbought, overbullish” conditions have been enough to derail the speculative inclinations of investors. Yet in every other way, this speculative episode is simply a more extreme variant of others that have come before it.

Why Market Valuations are Not Justified by Low Interest Rates

Current market valuations are consistent with negative expected returns for the S&P 500 over the coming 10-12 years, with a likely market loss of more than -60% in the interim.

Why Market Valuations are Not Justified by Low Interest Rates

Current market valuations are consistent with negative expected returns for the S&P 500 over the coming 10-12 years, with a likely market loss of more than -60% in the interim. The proposition that “lower interest rates justify higher valuations” has become a rather dangerous slogan, and is a distressingly incomplete statement that ignores the other half of the sentence: “provided that the stream of expected cash flows is held constant.”

Blissful Delusion

The present moment of blissful delusion is remarkable to witness. Take it in. A few words and updated charts will do.

Bubble Mindset

So the mindset, I think, goes something like this. Yes, market valuations are elevated, but, you know, low interest rates justify higher valuations. Besides, there’s really no alternative to stocks because you’ll get what, 1% annually in cash? Look at how the market has done in recent years. There’s no comparison.

Eyes Wide Shut

At the October 2002 market low, the S&P 500 stood -49.2% below its March 2000 peak (-48.0% including dividend income), with the Nasdaq 100 having lost more than -82.8% from its high, on the basis of both price and total return. The loss wiped out the entire total return of the S&P 500, in excess of Treasury bills, all the way back to May 1996.

Behind the Potemkin Village

The main contributors to the illusion of permanent prosperity have been decidedly cyclical factors. Investors presently appear to be taking past investment returns and economic growth at face value, without considering their underlying drivers at all. My impression is that while the U.S. may very well encounter credit strains or other economic dislocations in the coming years...

Valuations, Sufficient Statistics, and Breathtaking Risks

Current extremes present what I view as one of the three most important opportunities in history to defend capital. My sense is that many investors will squander this opportunity until yet another bubble implodes.

The Conceit of Central Bankers and the Brief Illusion of Wealth

The belief that Fed-induced speculation creates “wealth” is a conceit that rests on the delusion that “wealth” is embodied in the price of an asset, rather than the stream of cash flows it delivers over time.

Imaginary Growth Assumptions and the Steep Adjustment Ahead

Within a small number of years, investors are likely to discover that they have allowed their assumptions about growth in U.S. GDP, corporate revenues, earnings, and their own investment returns to become radically misaligned with reality, and that Wall Street’s justifications for the present, offensive level of equity market valuations are illusory. Based on outcomes that have systematically followed prior valuation extremes, the accompanying adjustment in expectations is likely to be associated with one of the most violent market declines in U.S. history, even if interest rates remain persistently depressed.

Broadening Internal Dispersion

We extract signals about the preferences of investors toward speculation or risk-aversion based on the joint and sometimes subtle behavior of numerous markets and securities, so our inferences don't map to any short list of indicators. Still, internal dispersion is becoming apparent in measures that are increasingly obvious.

Estimating Market Losses at a Speculative Extreme

In my view (supported by a century of market cycles), investors are vastly underestimating the prospects for market losses over the completion of this cycle, are overestimating the availability of “safe” stocks or sectors that might avoid the damage, and are overestimating both the likelihood and the need for some recognizable “catalyst” to emerge before severe market losses unfold.

Hot Potatoes and Dutch Tulips

At the height of the technology bubble, the median of the most reliable market valuation measures we follow (those most strongly correlated with actual subsequent S&P 500 total returns) briefly reached an apex 178% above historical norms that had been regularly approached or breached over the completion of every market cycle in history.

Wrecking Ball

What’s often missed in the “low interest rates justify higher valuations” argument is that this proposition assumes that future cash flows and growth rates are held constant.

Stall Speed

Fully 1.4% of the 2.0% average annual real GDP growth observed since the beginning of 2010 has been driven by growth in civilian employment. As slack labor capacity has slowly been reduced, the unemployment rate has dropped from 10% to just 4.4%. That jig is up.

Mesas, Valleys, Plateaus, and Cliffs

We are at the far edge of a monumental mesa here, but speculators are ignoring the cliff, assuming that they are on a permanently high plateau. The unfortunate aspect of these mesas and valleys is that they encourage backward-looking investors to believe that projected returns based on “old valuation measures” are no longer relevant, precisely when valuations are most informative about future returns.

Two Supports, Already Kicked Away

Put simply, with market internals unfavorable and interest rates off the zero bound, the two main supports that made the half-cycle since 2009 “different” have already been kicked away.

How to Wind Down a $4 Trillion Balance Sheet

The Fed does not have to make guesses about exactly what is required to normalize its balance sheet, except to the extent that it ignores a century of evidence.

Fair Value and Bubbles: 2017 Edition

The characteristic feature of a bubble is that the long-term return implied by discounted cash flows becomes detached from the higher, temporarily self-reinforcing return that is imagined by investors. As a result, the bubble component accounts for an increasingly large proportion of the total price, and becomes progressively vulnerable to collapse. It is in this precise sense that the current speculative episode can be characterized as a bubble, just as I (and Modigliani) characterized the bubble that ended in 2000.

Three Factors

Overall, my impression remains that the market is in the process of tracing out the blowoff finale of the third speculative financial bubble since 2000. Still, as is true for the market cycle as a whole, the broad outline of this top formation is likely to be shaped by three factors: 1) valuations, which primarily affect total market returns over a 10-12 year horizon, as well as the magnitude of potential losses over the completion of the market cycle; 2) the uniformity or divergence of market internals across a broad range of stocks and security-types, which remains the most reliable measure we’ve identified of the psychological preference of investors toward speculation or risk-aversion (when investors are inclined to speculate, they tend to be indiscriminate about it); and 3) overextended market action highlighting extremes of speculation or fear - in the advancing portion of the market cycle, these are best identified by syndromes of overvalued, overbought, overbullish conditions.

When Valuations Don't Seem to "Work"

It’s precisely the failure of valuations to matter over shorter segments of the market cycle that regularly convinces investors that valuations don’t matter at all

Being Wrong in an Interesting Way

My friend Mark Hulbert once had a philosophy professor at Oxford, who distinguished two ways of being wrong: “You can be just plain wrong, or you can be wrong in an interesting way.” In the latter case, Mark explained, correcting the wrong reveals a lot about the underlying truth.

Paying Twice

When investors pay high P/E multiples on earnings that already reflect cyclically-elevated profit margins, they pay twice for their investment.

This Time is Not Different, Because This Time is Always Different

Every episode in history has its own wrinkles. But investors should not use some “new era” argument to dismiss the central principles of investing, as a substitute for carefully quantifying the impact of those wrinkles. Unfortunately, because investors get caught up in concepts, they come to a point in every speculative episode where they ignore the central principles of investing altogether.

Exhaustion Gaps and the Fear of Missing Out

Despite extreme valuations, investors’ fear of missing out is looking increasingly desperate. In market cycles across history, that has been an unfortunate impulse.

Valuation Breakevens

One way to use information on stock valuations and interest rates in a systematic way is to estimate the break-even level of valuation that would have to exist at given points in the future, in order for stocks to outperform or underperform bonds over various horizons. Investors presently face a dismal menu of expected returns regardless of their choice. Indeed, in order for expected S&P 500 total returns to outperform even the lowly return on Treasury bonds in the years ahead, investors now require market valuations to remain above historical norms for the next 22 years.The good news is that this menu is likely to improve substantially over the completion of the current market cycle. The problem is that current valuation extremes present a hostile combination of weak prospective return and steep risk.

Good Logic and Bad Facts

One of the benefits of historically-informed investing is that it allows various investment perspectives to be evaluated from the standpoint of evidence rather than verbal argument. That’s particularly important during periods like today, when much of financial commentary on Wall Street can be filed into a folder labeled “it’s hard to argue with your logic, if only your facts were actually true.”

Echo Chamber

Put simply, investors are in an echo chamber here, where their optimism about economic outcomes is largely driven by optimism about the stock market, and optimism about the stock market is driven by optimism about economic outcomes. Given the deterioration in correlations between “soft” survey-based economic measures and subsequent economic and financial outcomes, investors should be placing a premium on measures that are reliably informative. On that front, hard economic data, labor force constraints, factors influencing productivity (particularly gross domestic investment and the position of the current account balance in the economic cycle), reliable valuation measures, and market internals should be high on that list.

Stalling Engines: The Outlook for U.S. Economic Growth

Imagine driving a car moving down the road at 20 miles an hour. You hold a rope out the window. At the other end of that rope is a skateboard. If the skateboard is behind the car, yanking the rope pulls the skateboard forward, so the skateboard might temporarily speed ahead until it gets way ahead of the car and the rope tightens again.

Dissolving Musical Chairs

Over the completion of the current market cycle, we estimate that roughly half of U.S. equity market capitalization - $17 trillion in paper wealth - will simply vanish. Nobody will “get” that wealth. It will simply disappear, like a game of musical chairs where players think they've won by finding chairs as the music stops, and suddenly feel them dissolving as if they had never existed in the first place.

Expect the S&P 500 to Underperform Risk-Free T-Bills Over the Coming 10-12 Years

Presently, based on the most historically reliable valuation measures we identify, we expect annual total returns for the S&P 500 averaging just 0.6% over the coming 12-year period; a prospective return that we expect will not only underperform bonds over this horizon, but even the lowly yields available on risk-free T-bills.

Blue Skies

During the later part of the roaring 20’s, Irving Berlin wrote “Blue Skies,” which captured some of the optimism of the era that preceded the Great Depression. Unfortunately, untethered optimism is not the friend of investors, particularly when they have already committed their assets to that optimism, and have driven valuations to speculative extremes.

The Most Broadly Overvalued Moment in Market History

"The issue is no longer whether the current market resembles those preceding the 1929, 1969-70, 1973-74, and 1987 crashes. The issue is only - are conditions like October of 1929, or more like April? Like October of 1987, or more like July?

When Speculators Prosper Through Ignorance

As Benjamin Graham observed decades ago, "Speculators often prosper through ignorance; it is a cliche that in a roaring bull market, knowledge is superfluous and experience is a handicap. But the typical experience of the speculator is one of temporary profit and ultimate loss."

Time-Stamp of Speculative Euphoria

If there’s any point in U.S. stock market history, next to the market peaks of 1929 and 2000, that has deserved a time-stamp of speculative euphoria that will be bewildering in hindsight, now is that moment.

Portfolio Strategy and the Iron Laws

Investors and even financial professionals rarely recognize asset bubbles while they are in progress. As the price of a financial asset rises, investors have an increasing tendency to use the past returns and the past trajectory of the asset as the basis for their future return expectations.

On Governance

There are moments when one has the responsibility to speak if one has a voice.

Rare Signatures

The key to drawing useful information out of noisy data is to rely on multiple “sensors.” Alone, each sensor may capture only a small portion of the true signal, and may not be greatly useful in and of itself. The power comes when the sensors are used together in order to distinguish the common signal of interest from the surrounding noise.

Cassandra's Song

One of the attempted barbs tossed my way at various points in the past 20 years is “Cassandra.” Frankly, I kind of like it.

The Economic Risk of Ignoring Arithmetic

Outcomes are not independent of initial conditions. While there are certainly policy shifts that could encourage greater productive investment and raise the long-run trajectory of economic growth, no shift in economic policies is likely to produce rapid, sustained economic growth in the next few years because the underlying factors that drive rapid, sustained growth aren’t presently in a position to support it.

Red Flags Waving

When investors are euphoric, they are incapable of recognizing euphoria itself.

More Blowoff than Breakout

The stock market has reestablished an extreme overvalued, overbought, overbullish syndrome of conditions that - unlike much of half-cycle advance from 2009 to mid-2014 - lacks internal uniformity, particularly among interest-sensitive and globally-sensitive sectors.

Action and Reaction

My sense is that investors are exuberant to have a new theme, any theme, other than watching the Federal Reserve.

Judging Economic Policy

If you net out all the assets and liabilities in an economy, you’ll find that the nation’s accumulated stock of real investment is the only thing that remains.

High Risk and Low Conviction

Short-term oversold conditions offer a sense of potential knee-jerk dip-buying behavior, but the conviction of that behavior is often fairly weak and short-lived.

Far Beyond Double

My continued impression is that the global equity markets broadly peaked in the second-quarter of 2015, and that the more recent marginal U.S. highs in August were a “throwover” in response to the post-Brexit plunge in global interest rates.

The Illusion that "Old Measures No Longer Apply"

Put simply, it’s not valuation norms that have increased, but instead the willingness of investors to repeatedly chase stocks to valuation levels that remain associated with predictably dismal subsequent outcomes.

Calm Before the Storm

Several weeks ago, we shifted from a rather neutral near-term stock market view, to a hard-negative outlook, based on fresh deterioration in various trend-sensitive components within our broad measures of market action.

Overvaluation, Deteriorating Market Action, and Coordinated Exit

Historically, the best opportunities to boost market exposure emerge when a material retreat in valuations is joined by an early improvement in market action. At present, exactly the opposite is true. Extreme valuations and compressed risk-premiums have been joined by deterioration in market internals. This deterioration is an indication of growing risk-aversion among investors. Much of the recent bubble has been driven by yield-seeking, trend-sensitive speculators, with value-conscious investors progressively stepping back. As a result, any coordinated attempt by trend-sensitive market participants to exit by selling stock is unlikely to be met by demand from value-conscious investors at prices anywhere near present levels. This, in turn, leaves the market vulnerable to potentially abrupt losses.

Sizing Up the Bubble

Every financial bubble rests on the presumption that there is still some greater fool available to purchase overvalued assets, no matter how overvalued they might become. In the recent half cycle, central banks have intentionally extended this speculation by promising that they, themselves, could be relied upon to be those greater fools.