From a long-term perspective, we believe that investors have a strong opportunity here to reduce equity risk near the peak of a market cycle that has reached the second greatest overvaluation extreme in U.S. history (second only to the 2000 peak). Among the valuation measures we’ve found most strongly correlated with actual subsequent S&P 500 10-12 year total returns, market valuations have pushed to a level that is more than double their reliable historical norms. From these levels, we fully expect 10-12 year S&P 500 nominal total returns near zero, with negative real returns after inflation.

Notably, the completion of every market cycle in history has taken the most reliable equity valuation measures toward or below their historical norms - levels associated with subsequent total returns approaching 10% annually. That includes two cycle completions since 2000, as well as cycles prior to 1960 when interest rates regularly hovered near present levels. After an unusually extended speculative half-cycle, we doubt that the completion of the present cycle will be any different. It has taken the third speculative bubble in 16 years to bring the nominal total return of the S&P 500 since March 2000 to just 3.6% annually. It is not an act of pessimism to reject the notion that investors are doomed, from here, to suffer permanently elevated valuations and permanently dismal long-term returns. No. It is an act of historically-informed optimism.

From a shorter-term perspective, market conditions are more ambiguous. Our measures of market internals remain broadly unfavorable, but enthusiasm over yet another round of monetary intervention in Europe pushed the S&P 500 above its 200-day average last week, and credit spreads, though still wide, narrowed somewhat. At the same time, participation remains tepid, with fewer than 40% of individual stocks above their own respective 200-day averages, sponsorship is questionable, as evidenced by waning trading volume, and short-term conditions are clearly overbought. While a market break of even a few percent would be sufficient to clarify the technical picture and restore a steeply negative market outlook, there’s just enough ambiguity to keep our near-term views a bit more neutral at present.

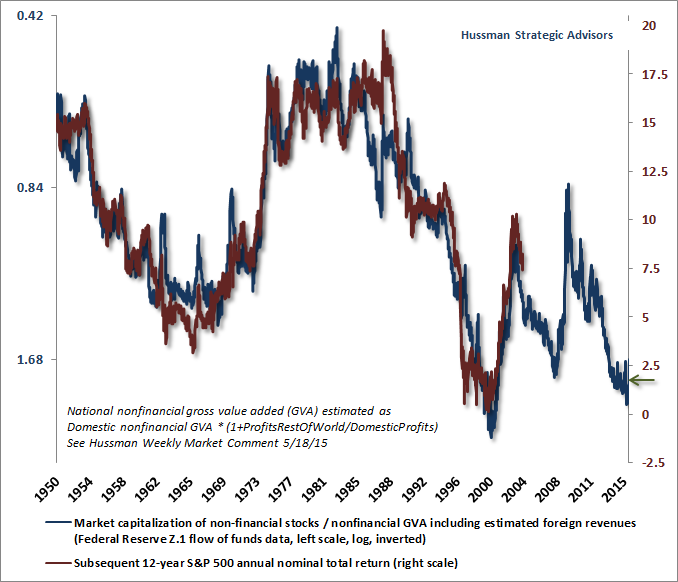

The chart below shows the ratio of market capitalization to corporate gross value added on an inverted log scale (blue line, left scale), and the actual S&P 500 nominal annual total return over the following 12-year period (red line, right scale). For a mathematical decomposition, see Rarefied Air: Valuations and Subsequent Market Returns, which details why subsequent total returns are so strongly correlated with the log valuation ratio, and why the effects of changing interest rates and fundamental growth systematically offset each other over a 10-12 year holding period.

Value investor Seth Klarman once wrote that “value investing is at its core the marriage between a contrarian streak and a calculator.” Benjamin Graham wrote "Buy not on optimism, but on arithmetic." Unfortunately, at every speculative peak, a different message emerges, suggesting that the calculator is broken, that “this time is different,” and that “the old valuation measures no longer apply.”

As John Kenneth Galbraith wrote decades ago about the advance to the 1929 peak, “as in all periods of speculation, men sought not to be persuaded by the reality of things but to find excuses for escaping into the new world of fantasy." Be skeptical of measures that show stocks reasonably valued today, but that are not strongly correlated with actual subsequent market returns in prior cycles across history. Be even more skeptical when most of the data is drawn from the past 16 years, because as noted above, the nominal total return of the S&P 500 over the past 16 years has been just 3.6% annually. Be particularly wary of arguments that propose that valuation doesn’t matter at all.

There are certainly points in history where low valuations were followed a decade later by another plunge to low valuations, resulting in 10-year returns that were not nearly as strong as one would have expected. There are certainly points where reasonable valuations were followed by an extreme valuation peak (or trough) a decade later, resulting in a 10-year total return much higher (or lower) than one would have expected. Over shorter horizons, the most spectacular outcomes have been where a valuation extreme in one direction was followed by a valuation extreme in the other. The 1929-1932 period stands out, when the Dow Jones Industrial Average plunged by 89.2%.

Critics of historically-informed investing use these outliers as evidence that valuations are meaningless. Yet all of these instances rely on the terminal valuation being an outlier. Investors are certainly free to accept market risk on the expectation that future valuations will be comprised of nothing but outliers for all time. But understand that expecting the S&P 500 to retreat by 45-55% over the completion of the current market cycle is not to expect an outlier. No, a decline of that magnitude would be a historically run-of-the-mill outcome from present valuations. The 2000 peak was the most extreme point of overvaluation in history, and the current market cycle has reached the second most extreme point of overvaluation in history. We expect the completion of this cycle to wipe out the entire total return of the S&P 500 since the 2000 peak, and then some.

One might argue that historical valuation norms are irrelevant in a world of low interest rates. Contrary to a century of evidence, investors have been led to believe that 10-year Treasury yields and prospective 10-year stock market returns should move tightly in sync. On that front, it's important to recognize that over the past century, the correlation between 10-year Treasury yields and subsequent 10-year equity returns has been only 0.23. Indeed, if one excludes the disinflationary 1982-1997 period, the correlation between the two has been zero. Outside of the inflation-disinflation cycle from 1970-1997, the correlation has actually been negative, at -0.42. The same pattern holds even if the data is restricted to the post-war period. Investors vastly overestimate the relationship between 10-year Treasury yields and prospective equity returns, largely because they have overgeneralized a very specific segment of history - see Recognizing The Risks to Financial Stability for a detailed discussion, and how this relates to the "Fed Model."

In short, our measures of valuations and market internals remain jointly unfavorable. Still, given a somewhat mixed technical picture, we have no strong near-term views. A market retreat of even a few percent, say, below 1975 on the S&P 500, would shift our outlook like a light switch to a steeply negative view as the most critical measures would again be wholly one-sided. Until that point, we’ll ease our table-pounding about crash risk. For contrarians, this at least briefly softens one of the loudest voices on the subject, which might be exactly the thing to get a crash going.

QE’s endgame

Global central bankers are locked in a contest to find out who can create the most psychotic variant of quantitative easing, Ben Bernanke’s grotesque brainchild, before irretrievably destabilizing the global financial system once again. Attached to an incorrect understanding of the Phillips Curve (which is actually a relationship between unemployment and wage inflation, and real wage inflation at that), central bankers seem to overlook that quantitative easing provokes neither inflation, nor employment, nor industrial production, nor real investment, nor consumption. The entire operation involves buying up income-producing bonds and replacing them with zero-interest money. Since every dollar of monetary base has to be held by someone until it is retired, the goal of QE is to provoke discomfort with the form in which investors are forced to hold their savings. That doesn’t encourage people to save less. They just look for alternative forms of saving.

As I’ve detailed in other comments, provided that investors are favorably inclined toward risk-seeking (which we measure from the uniformity of market internals across a broad range of financial assets), zero-interest money can encourage each holder to treat it like a hot potato, trading it to someone else in return for a riskier but higher yielding security. The cycle then continues until every speculative asset is overvalued enough to offer a zero prospective return as well. This behavior has produced what all of us will view, in hindsight, as the QE Bubble.

So provided that investors are inclined to speculate, the main effect of QE is to amplify speculative tendencies, enable borrowers to issue massive amounts of low-grade debt, and encourage malinvestment in unproductive projects that would never get funded at a higher hurdle rate. The current episode is really no different than the housing bubble, except that this one has been focused on speculation in equities and covenant-lite debt. Also, of course, we know how the housing bubble ended, and unfortunately, investors seem perennially incapable of recognizing a bubble until after collapses.

Understand, however, that QE fails to “work” when investors are risk-averse. In that situation, the higher potential yield on a riskier security typically isn’t enough to offset the perceived risk of a price decline. That’s why persistent monetary easing was wholly ineffective during the 2000-2002 and 2007-2009 collapses. While monetary easing may encourage investors to shift from risk-aversion to risk-seeking, that outcome is actually the exception, not the rule. Historically, the more accurate statement goes in the opposite direction: monetary easing only reliably supports financial speculation once investors are already inclined to speculate.

As for the effect of QE on the real economy, economists have known since the 1950’s that people base their consumption on what they view as their “permanent” income, not on the fluctuating value of volatile assets. Indeed, Bernanke himself wrote an empirical paper on the subject in 1981, and concluded “The response of expenditure to transitory income changes is as predicted by the permanent income model.” Put simply, there’s no theoretical or factual basis to expect a “wealth effect” to benefit economic activity as a result of Fed bubble-blowing in the financial markets.

The “counterfactual” of how the economy would have done without this intervention is readily available. Good macroeconomists know that this involves comparing the projections from a constrained and unconstrained vector autoregression (VAR). Regardless of whether one uses observable or “shadow” monetary measures (as Wu-Xia do), the result is the same: all of this reckless intervention has hardly moved the level of employment, industrial production, or real GDP even 1% from what one would have predicted based on the values of purely non-monetary variables alone.

It’s endlessly fascinating to hear central bankers talk about the effect of monetary policy on inflation and the economy, because they confidently speak as if the models in their heads are true - even reliable. Yet virtually nothing they say can actually be demonstrated in historical data, and the estimated effects often go entirely in the opposite direction. This is particularly true when it comes to inflation and unemployment - precisely the variables that are the targets of central bank policy.

For example, study a century of data and you’ll discover that few economic series, not changes in money growth, not even unemployment, are strongly correlated with inflation - with the exception of prior inflation itself, and only by extension, the level of interest rates. The GDP output gap can also be useful, but the relationship with inflation isn’t quite linear - the main value is to discriminate between “tight capacity getting tighter” and “slack capacity getting slacker.”

Since inflation is correlated from year-to-year, an above-average level of inflation in one period is typically followed by an above-average level of inflation the next. But inflation also tends to mean revert, so a high level of inflation in one period is typically followed by a slower rate of inflation the next period.

As for cyclical behavior, the strongest plunges in the rate of inflation follow points where a) real GDP is below estimated potential GDP and b) that output gap has worsened in the past year. The retreat in inflation tends to be particularly large if the rate of inflation has increased over the prior year despite those conditions. Conversely, inflation accelerates most reliably when a) real GDP is above estimated potential GDP and b) that output gap has improved in the past year, regardless of the level of unemployment. Notably, once information on the output gap and inflation itself is included, additional information about monetary policy doesn’t materially improve projections of inflation. That’s another way of saying that only the systematic component of monetary policy (e.g. what could be captured by a simple Taylor Rule) is relevant to the economy. Activist deviations from systematic policy don’t do anything but distort financial markets.

Beyond those general rules of thumb, what drives inflation? While many economists seem satisfied with having memorized a line from Milton Friedman about inflation being “always and everywhere a monetary phenomenon,” economic models of inflation turn out to be nearly useless for any practical purpose. It’s not difficult to explain inflation, using inflation itself as the main explanatory variable, and information on the output gap is also useful even if unemployment is not. But it’s very difficult to explain most episodes of inflation using monetary variables.

Yes, hyperinflation is always associated with monetary expansion, but monetary expansion isn’t actually enough. Examine major hyperinflations, and you’ll always find a government that has racked up huge external obligations to other countries, and has lost fiscal control by running massive deficits - effectively printing money to fund them. Hyperinflation involves a loss of both fiscal and monetary control, often coupled with a supply shock of some sort, and revulsion toward holding money itself because the willingness of the next person to accept it comes into question.

The long-term value of paper money relies on the confidence that someone else in the future will accept it in exchange for value, and ultimately, that’s a matter of varying confidence in the ability of the government to meet its long-term obligations. Early U.S. money such as confederate currency went to zero because that confidence was absent. Greenbacks held their value because of the expectation (validated in 1879) that convertibility with gold would ultimately be honored. Gold convertibility isn’t necessary, nor are balanced budgets required in the short-run, but confidence in long-run fiscal discipline is essential. If that confidence weakens - which may occur later in this decade, after the next recession - rapid inflation may emerge out of nowhere, and nobody will celebrate it.

Now, expansionary fiscal policies are fine when they result in the accumulation of productive capital by society (which can include infrastructure, workforce training, and even support for productive investment by fiscal means such as tax credits). Put simply, productive investment is the best avenue to expand potential GDP, increase employment, and reduce the likelihood of inflation. But when the primary use of fiscal policy is to wipe up the catastrophe of weak productivity, lost income, unemployment, and malinvestment created in the repeated aftermath of collapsed financial bubbles, the endgame is going to be stagnant living standards and a debased currency.

Ultimately, QE may finally create inflation by provoking a loss of fiscal control. My concern is that central banks have risked just that by encouraging yet another speculative bubble, heavy issuance of low-grade debt, and the diversion of savings toward unproductive investment. The inevitable fiscal consequences are likely to include bailouts, as well as urgency to expand income-replacement and transfer payment programs as the third bubble since 2000 collapses (which QE will helpless to prevent so long as investors remain risk-averse). Europe is approaching that endgame, and last week’s action by the ECB is evidence of increasing panic. Other economies are not far behind. The greatest risk is that Mario Draghi and other central bankers may ultimately get their wish for higher inflation, but not at all as they intend.

© The Hussman Funds