Expect the S&P 500 to Underperform Risk-Free T-Bills Over the Coming 10-12 Years

Last week, Treasury bill yields rose to 0.75% following the Federal Reserve’s quarter-point hike in the target Federal Funds rate, placing the yield on even risk-free liquidity above our 0.6% estimate for 12-year prospective S&P 500 annual total returns. This isn’t the first time in history that prospective 12-year stock market returns have fallen below the prevailing T-bill yield, but it’s certainly the lowest return that has prevailed at any of those points.

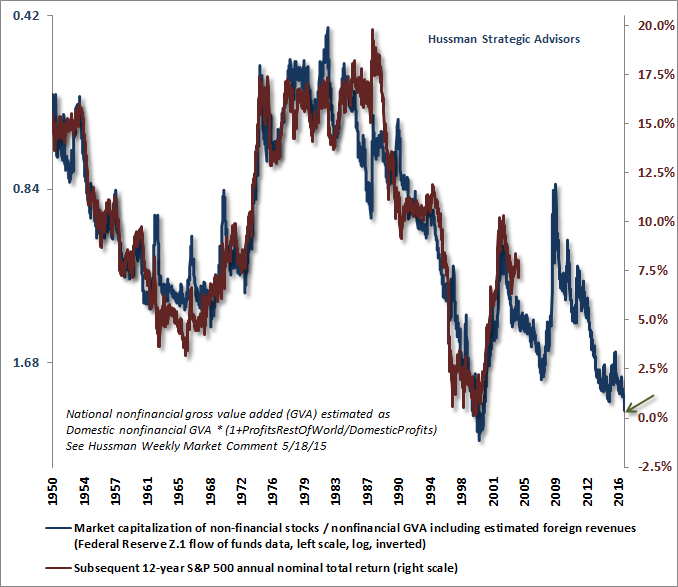

We should distinguish those points, in and of themselves, from market peaks. For example, in early-1969, prospective 12-year S&P 500 total returns (based on MarketCap/GVA - chart below) fell below the prevailing T-bill yield of 6.2%. That point wasn’t quite a market top, but it did usher in a long period of equity market underperformance relative to Treasury bills (as it happened, the S&P 500 Index itself would not durably trade above its early-1969 level until late-1982). On a total return basis, the S&P 500 total return averaged 6% over the following 12-year period, while the yield on risk-free Treasury bills averaged 6.8% over the same horizon.

Similarly, by mid-1997, prospective 12-year S&P 500 annual total returns fell below the prevailing T-bill yield. Again, that wasn’t a market top, but over the next 12 years, the actual S&P 500 annual total return averaged just 1.6%, while Treasury bill returns averaged 3.3%.

By 2000, prospective 12-year annual total returns fell to nearly zero. In real-time, using similar methods, I projected negative S&P 500 total returns over the 10-year period ahead. By 2010, the S&P 500 had indeed posted a negative total return over the intervening decade, and even by 2012, the S&P 500 remained lower than its 2000 peak, with a total return, including dividends, of just 1% annually.

Though we know that the extreme valuations of the 2006-2007 period were followed by the deepest market collapse since the Great Depression, we don't yet know the 12-year outcome for total returns. Given that the market has now ascended to valuations that actually eclipse the 2007 bubble, and roughly match the 2000 extreme, market returns in recent years have exceeded those that we projected back then (as is common at valuation extremes - see A Better Lesson than "This Time is Different" for examples of this overshooting behavior, and how it is typically resolved). As we've seen in prior cycles, I have little doubt that the completion of the cycle will similarly resolve the overshooting of valuations in recent years.

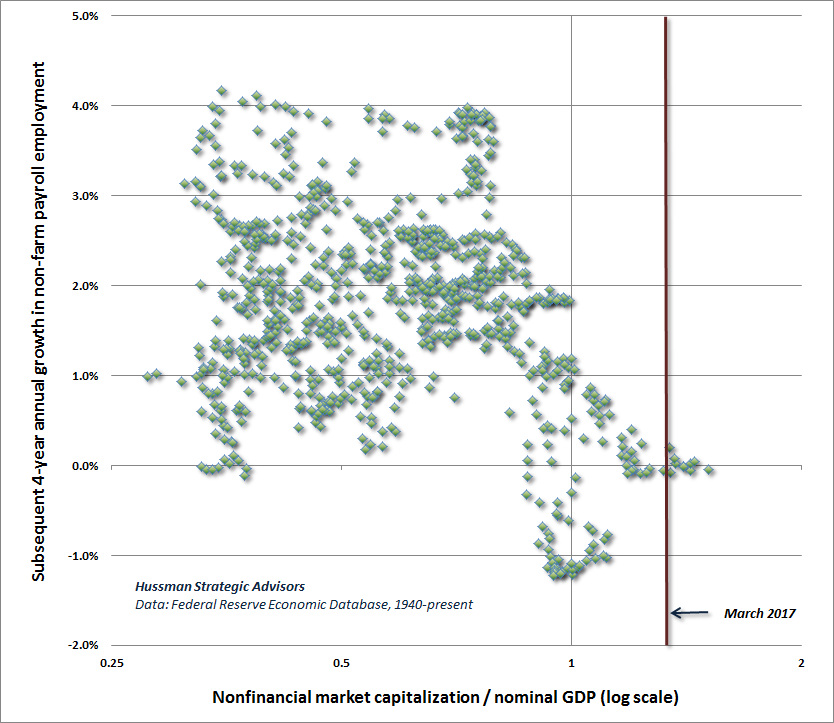

Presently, based on the most historically-reliable valuation measures we identify, we expect annual total returns for the S&P 500 averaging just 0.6% over the coming 12-year period; a prospective return that we expect will not only underperform bonds over this horizon, but even the lowly yields available on risk-free T-bills. Like the unwindings that followed the 2000 peak and the 2007 peak, there will be points in the interim where the prospective total return on stocks will likely be elevated (as a result of steep market losses and improved valuations), providing patient, flexible investors substantial opportunities for long-term total returns.

Before knowing what to do about this situation, you have to know who you are. If you are an investor who cannot tolerate the idea of the market advancing without your participation, it may be best to bind yourself to a passive investment stance, and stick to it, provided that you can also tolerate whatever losses the market endures without abandoning your position. Many people can easily endure losses, provided those losses are experienced in the company of others, yet can’t bear to miss out, or endure losses, when the crowd is making money. If that describes you, then honestly, don’t read my stuff, because it’s not appropriate for your temperament. Frankly, I don’t believe that what passive investors are doing here actually represents “investment” in any valid sense of the word (i.e. purchasing a stream of future expected cash flows at a price that implies a satisfactory risk-adjusted return), but it does address the psychological desire to experience the same fluctuations that others do.

Our own approach is decidedly full-cycle, which requires a tolerance for being out-of-step at extreme valuations. That typically makes us lonely at tops, but contrary to the “permabear” moniker, it has also typically made us lonely at bottoms. The fact is that I’ve encouraged a constructive or leveraged investment stance after every bear market decline in over 30 years as a professional investor, though my late-2008 constructive shift, after the market had lost more than 40% of its value, was truncated by my insistence on stress-testing our methods against Depression-era data (see the discussions in Portfolio Strategy and The Iron Laws and the “Box” in The Next Big Short for that narrative). Sometimes being out-of-step is a benefit, as it has typically been during market collapses, and sometimes it feels excruciating, as it did in 2000, 2007, and has for quite some time during the present bubble.

I’ve regularly discussed the Achilles Heel that I inadvertently bared in the half-cycle since 2009 as a result of that stress-testing decision, and that we addressed in 2014. It’s incorrect to dismiss our present market concerns, in the face of extreme valuations and divergent market internals, as if they are simply a continuation of that challenging transition. Indeed, our current views are driven by the same considerations that drove our concerns at the 2000 and 2007 peaks. The validity of these concerns may not become obvious until we observe a material completion to the current market cycle. By then, I expect it will be too late for investors to realize that the same historically-informed, full-cycle discipline, and the same valuation concerns, have been repeatedly validated in previous market cycles, both in real time and in a century of historical data.

Meanwhile, we should be clear about what patient discipline actually means. It doesn’t mean that the market has to lose value immediately. Rather, investors should remember that the 2000-2002 market collapse wiped out the entire total return of the S&P 500, in excess of risk-free Treasury bill returns, all the way back to May 1996. Likewise, the 2007-2009 market collapse wiped out the entire total return of the S&P 500, in excess of risk-free Treasury bill returns, all the way to June 1995. By the time that a market cycle is completed, a value-conscious, full-cycle investment discipline tends to be enormously forgiving of early exit, particularly when one exits at historically rich valuations.

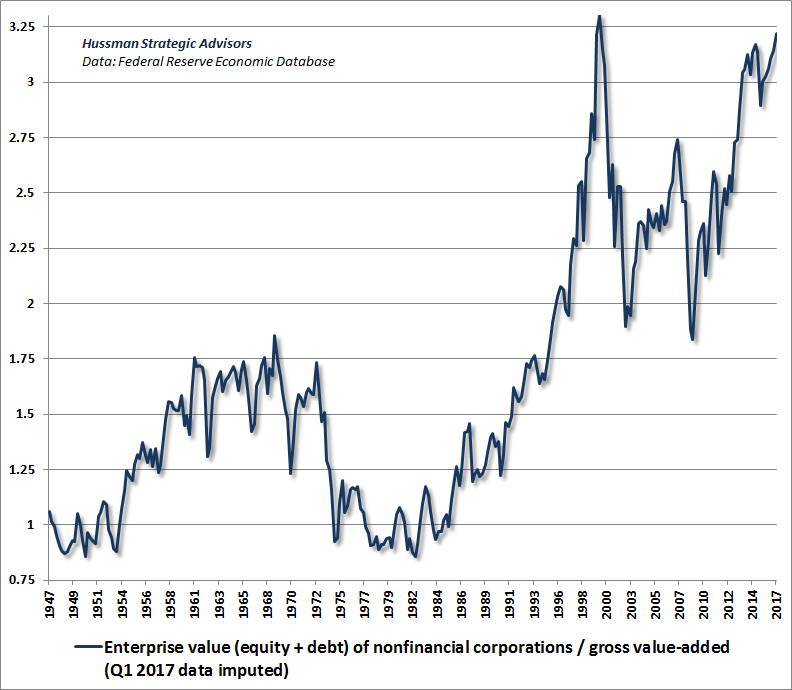

At present, the debt burdens of non-financial companies have never been higher relative to their gross value-added. Meanwhile, the market value of non-financial stocks is also near the 2000 extreme relative to their gross value-added. The sum of equity and debt is known as “enterprise value.” The chart below presents enterprise value as a fraction of corporate gross value-added (h/t @JesseFelder), which illustrates the extreme value of financial claims on corporations, relative to the revenues needed to serve them. Present levels are within a breath of the 2000 extreme.

Keep your eyes open, and look forward

Remember that the valuation measures we’re discussing here have a correlation of more than 90% with actual subsequent S&P 500 total returns (something that cannot be said for price/forward operating earnings, the Shiller CAPE, or the Fed Model). There are lots of analysts on Wall Street who refer to investments as “product” who will eagerly produce alternative measures to show that valuations are just fine. Be sure to get your hands on decades of historical data and test their relationship with actual subsequent full-cycle and 10-12 year market returns. I would love to have a reliable basis for advocating a significant exposure to market risk here, but having studied and tested hundreds (and perhaps thousands) of investment strategies across more than 30 years in the financial markets, all I can say is hold on tight.