It will come as no surprise that market conditions remain of great concern here. As always, but particularly now, it’s important to stress that our defensiveness is a reflection of prevailing, observable evidence and the alignment of our investment views with the average outcome of such evidence across similar instances over the course of history. The consistency of negative outcomes also worsens the expected return/risk ratio presently. A defensive stance here does not require any particular forecast about recession, profit margins, bubble/crash dynamics, QE, European banking strains, or any of the numerous risks in the economic and financial backdrop. All of these factors are worthy of discussion in their own right. Still, our approach is always to align our investment stance with the average return/risk profile that is associated with a given set of market conditions, placing heavy weight on valuations, market action (e.g. trend-following factors, market internals, measures of overextension, price/volume behavior), as well as monetary factors, sentiment, economic measures and other considerations. SeeAligning Market Exposure with the Expected Return/Risk Profilefor a review of this general approach.

My concerns here are not based on a forecast about any particular event in this specific instance. It is based on an ensemble of observable factors that can be tested and validated across numerous independent samples of market history over time, and the average profile of market return and risk produced by instances that share the same central features. Every instance matching the present one on central features (which in this case include the 1929 peak, the late-1972 euphoria as gold-linked monetary policy was abandoned, the 1987 pre-crash peak, the 2000 peak of the tech bubble, and the 2007 peak of the credit bubble) has also had other features that never before and will never again be observed in exactly the same way. That’s the reason for validating those central features against numerous independent samples of history. In some respects, this time is always different. But on the central features that have regularly been associated with the worst market outcomes – namely the acute syndrome of overvalued, overbought, and overbullish conditions that we presently observe – this time has never been different.

To the extent that we align our investment stance with the average return/risk profile, one might reasonably say that we are relying on the belief that this profile is representative of the most likely range of outcomes in the current instance. But that still does not require a specific forecast. To see the difference, suppose you have a pair of dice and a combined roll of 7 or 11 gets a payoff. Now suppose that the “6” faces on both of the dice are wiped off, and replaced with a “1.” There are still a few ways to win, but the return/risk profile has changed. One does not need to forecast the next specific roll to understand that the prospect of winning further bets has declined significantly.

For investors, the prospect of winning further bets has declined significantly.

Rock, Paper, Scissors

A curious result of our 2009-early 2010 “miss” (which emerged in the interim of stress-testing our approach against Depression-era data), coupled with the lagging performance even of pure trend-following approaches since about April 2010, is the impression that we don’t consider or include trend-following considerations in our work. This is incorrect. The fact, however, is overvalued, overbought, overbullish syndromes have historically disabled the otherwise favorable implications of constructive trend-following measures (again seeAligning Market Exposure with the Expected Return/Risk Profile). It’s also notable that the additional trend-following exclusions that we’ve incorporated in recent years – to narrow our defensive positions to an “essential” set – are not exclusions that apply here.

I’ve certainly discouraged the reliance on simple moving-average crossover strategies, arguing that information is best extracted by using “multiple sensors” to capture a broader picture of market action (seeThe Trend is Your Fickle Friend), but this is not an argument against trend measures altogether.

Put simply, trend-following considerations are important, and there are historically sound reasons for including them in any systematic market analysis. Indeed, I shifted to a constructive outlook despite still-rich valuations early in the 2003 bull market advance largely on that basis. But the sequence of our stress-testing miss in 2009-early 2010, the whipsaw-prone behavior of trend-following measures during the QE period, and the present overvalued, overbought, overbullish “veto” may create the appearance that we ignore such evidence. It’s best to clarify any misbeliefs now than to create confusion later. The best opportunities to establish a constructive investment stance tend to occur when a moderate retreat in valuations is coupled with an early improvement in market action. These opportunities do not require absolute undervaluation, and embracing these opportunities will not require any departure from our discipline.

Markets move in cycles. This one will be no different, and we are now in a mature, euphoric, unfinished half. I fear that investors will destroy their long-term financial security if they imagine they are “forced” to lock in depressed prospective long-term returns, at elevated valuations, out of fear that better opportunities will never arrive.

Meanwhile, it’s also worth noting that monetary indicators, however defined over history, are not nearly as effective as trend-following considerations (and we’ve tested scores of metrics based on policy rates, market rates, monetary aggregates, and other candidates). The disturbing fact is that many of the worst bear market losses have occurred in an environment of aggressive monetary easing. This was certainly the case throughout the 2001-2002 plunge, as well as 2008 when the Fed was easing with increasing urgency throughout the year. But it is also invariably true that the Fed is still easing at the time that a new bull market emerges. Pair that stimulus and reward with the belief that monetary policy acts with some undefined “long and variable lag,” and the result is a classical conditioning response worthy of Pavlov’s dogs, who were conditioned to salivate at the ringing of a bell, even when there was no longer any meat.

This is certainly not to imply that monetary factors are not useful. But there’s a sort of rock-paper-scissors relationship to financial indicators. Trend-following considerations typically trump valuations alone, while overvalued, overbought, overbullish syndromes trump trend-following and monetary considerations. Monetary factors tend to be most effective as confirmation of other measures, particularly of trend-following factors, but only in the absence of overvalued, overbought, overbullish syndromes.

Certain important central features happen so rarely that they haven’t occurred with others. For example, in the most extreme handful of overvalued, overbought, overbullish peaks in history, monetary policy was not yet easing. How does one deal with those instances? The straightforward answer is to relax the criteria to capture a larger group of instances that reflect the same central features, and examine the outcomes. Even on weaker criteria, overvalued, overbought, overbullish features still dominate monetary easing, on average. This time may be different in the short-term, but the hangover is likely to be that much worse.

Whatever investors believe most strongly here, they would do well to test those beliefs over decades of historical evidence than to invest blindly on aphorisms about what not to fight.

Four questions

Fed Chairman Ben Bernanke appeared before the Joint Economic Committee last week, mostly reaffirming the strategy of pursuing quantitative easing until employment conditions improve further. However, the Federal Open Market Committee is already increasingly split on continued quantitative easing, and the Chair of the JEC correctly voiced concerns that quantitative easing was “played out,” questioning the effectiveness of the policy in affecting economic activity other than financial markets.

Keep in mind that with a $3 trillion balance sheet, an estimated duration of about 8 years, and an average yield of only about 2.5% on Fed holdings, it only takes an interest rate increase of about 30 basis points to wipe out all of the annual interest that the government pays on this debt (which the Fed refers to as “profits”) and to create a capital loss (which the Fed refers to as a “deferred asset” since it reduces the future “outflow” that the Fed will make back to the Treasury). Last week, Bernanke casually noted that increasing the amount of interest that the Fed pays to banks would be a key part of its eventual exit strategy. So the Fed will not only be withholding interest payments from the Treasury, it also plans to dissipate those interest payments to banks in order to prevent inflationary pressures that might result from banks actually lending the money it has created.

Many observers believe that the major risk in the next employment report is that it will come in too strong, and lead the Fed to taper its program of QE more quickly. My impression is that a very weak report would be a greater risk for the markets, because it would properly bring the economic ineffectiveness of QE into stronger focus. In the absence of demonstrable benefits, the attempt to balance the benefits versus costs of QE may abruptly shift all remaining weight to the “cost” side.

Four Questions for the Federal Reserve Open Market Committee (an open letter)

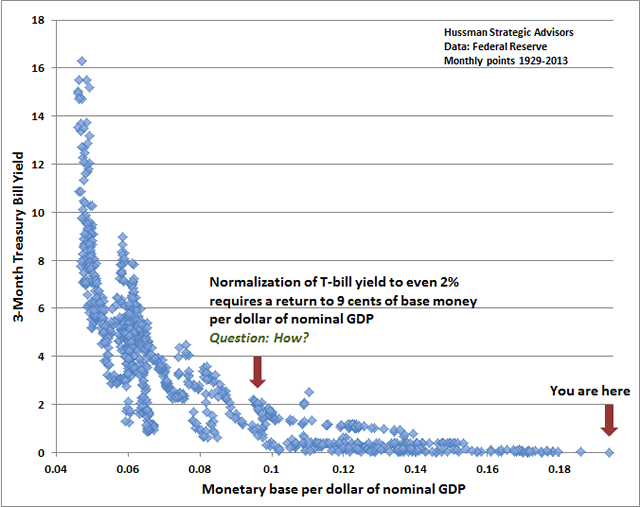

1) Are you all quite aware of how extreme a position you have now placed the U.S. economy? The monetary base now stands near 20 cents for every dollar of nominal GDP. The well-established liquidity preference relationship in U.S. data since 1929 indicates that even 2% T-bill yields would tolerate no more than 9 cents of monetary base per dollar of nominal GDP. The issue is not whether present policy is resulting in near-term inflation. The issue is the long-term imbalance that has already been created.

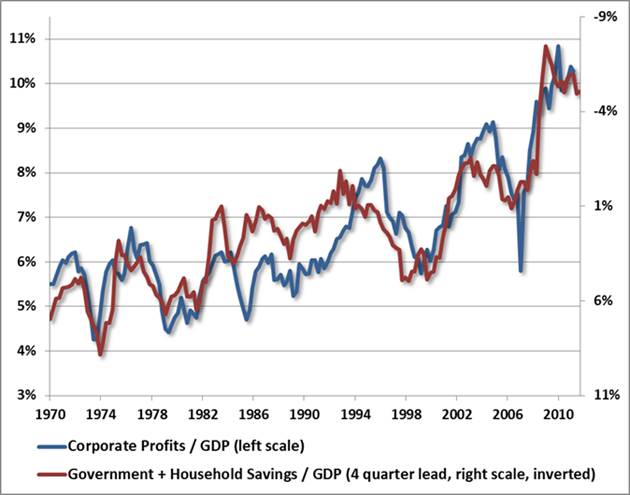

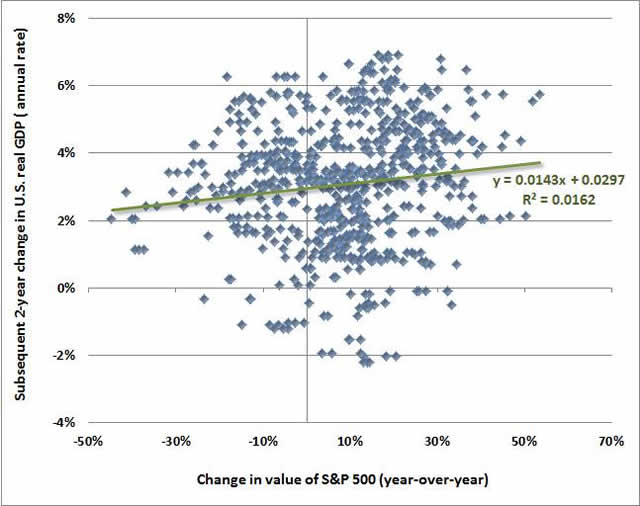

2) Are you all quite aware that an equity bubble is not “obvious” only because profit margins are 70% above their historical norms, being essentially the mirror image of deficits in the fiscal and household sectors (as the deficits of one sector must emerge as the surplus of another)? Equities are not a claim on a single year of earnings – as popular estimates of the “equity premium” implicitly assume. They are a claim on a very long-term stream of future cash flows, and present earnings are an enormously distorted figure to use as a sufficient statistic.

3) Are you all quite aware that there is no material or reliable wealth effect from changes in the value of volatile assets in a world where – in both theory and evidence – consumers spend from “permanent income” (which is why estimated wealth effects have always been weak from equities, and since 2008 have become weak even from housing wealth)?

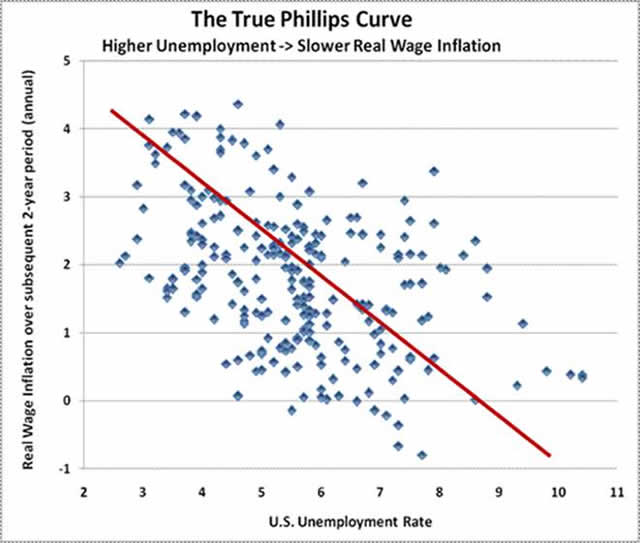

4) Are you all quite aware that A.W. Phillips’ 1958 Economica paper actually dealt with the relationship between unemployment and WAGE inflation in a century of British data (through 1950) when Britain was on the gold standard and GENERAL price inflation was nonexistent? The “Phillips Curve” is actually a relationship between unemployment and real wage inflation, which can also be demonstrated in U.S. data (where other interpretations of the Phillips Curve cannot) and asserts nothing except that labor scarcity results in an increase in the real price of labor. This is not a relationship that can be manipulated to create more jobs. There is certainly room for monetary policy to improve economic conditions when it operates on a binding constraint, but at present, neither interest rates nor the quantity of base money are binding constraints on economic activity.

All of us would like to observe lower unemployment, but the belief that quantitative easing will materially contribute to this outcome is unsupported in both theory and evidence. The present course of Fed policy is destabilizing the global economy by contributing to a financial environment that encourages the allocation of scarce savings toward speculative activity, not productive investment. When “QE” and the “Bernanke put” are the sole focus of the financial markets – not productivity, not innovation, not sound policy options, not careful intermediation of capital, and certainly not the plight of the elderly that have been starved of interest income – it should be obvious that things have gone too far.

This experiment has played out long enough. Establishing the largest fiscal and monetary imbalance in U.S. history has certainly created a pleasant environment for speculators, but it does not create employment, and it sows the seeds of the next collapse. The Fed is stepping on a gas pedal in the hope of making the wheels go faster, and instead the gasoline is spurting out of the tank and feeding speculative flames, because a reliable transmission mechanism does not exist.

---

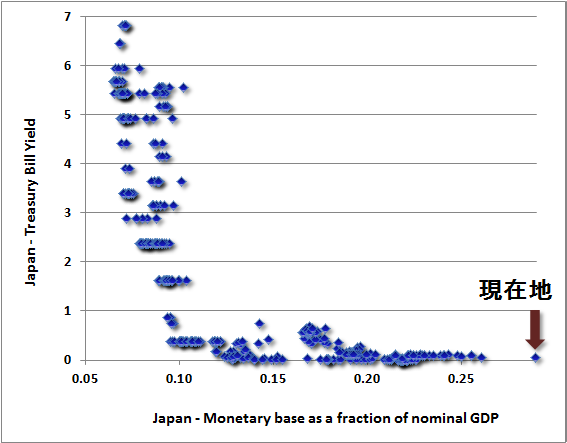

A final note on quantitative easing. This policy experiment is going no better in Japan, where the amount of monetary base as a fraction of GDP is higher than it is here, and the Bank of Japan has become frantic in its attempts to push on the string.

More than a decade of aggressive effort – following Ben Bernanke’sadvice– to elevate monetary stimulation over thoughtful policy has resulted in nothing but persistent economic erosion. Japan has been locked into an extended period of zero GDP growth. Why does anyone believe that QE is exerting any greater economic benefit here?

The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Only comments in the Fund Notes section relate specifically to the Hussman Funds and the investment positions of the Funds.

Past performance does not ensure future results, and there is no assurance that the Hussman Funds will achieve their investment objectives. An investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted above. More current performance data through the most recent month-end is available at www.hussmanfunds.com. Investors should consider the investment objectives, risks, and charges and expenses of the Funds carefully before investing. For this and other information, please obtain a Prospectus and read it carefully.

© Hussman Funds