“Even the intelligent investor is likely to need considerable will power to keep from following the crowd.”

- Benjamin Graham

“Human beings desperately want to belong, but, they also desperately want to understand the environment around them. Often, the desire to belong and the desire to know the truth conflict. The idea of the majority view or the ‘mainstream,’ gives people the sense that they are a part of a group, and at the same time, gives them the illusion of being informed.”

- Brandon Smith

The bears are gone, extinct, vanished. Among the ones remaining, many are people whom even I would consider to be either permabears or nut-cases. And yet, the historical evidence for major defensiveness has rarely been stronger.

The newest iteration of the bullish case is the idea of a “great rotation” from bonds and cash to stocks, as if the outstanding quantity of each is not held by someone at every point in time. The head of a “too big to fail” investment firm argued last week that stocks are “underowned” – as if every share of stock presently in existence is not actually owned by someone. To assert that stocks can be “underowned” seems to reflect either a misunderstanding of how markets work, or a desire to distribute overvalued institutional holdings onto the unwashed muppets. Likewise, the idea of a “rotation” out of bonds and into stocks begs the question of who will buy the bonds and sell the stocks, as someone must be on the other side of that trade. Similarly, to “move cash into the market” requires a seller of stock who becomes the new holder of said cash.

Quite simply, the reason that pension funds and other investors hold more bonds relative to stocks than they have historically is that there are more bonds outstanding, relative to stocks, than there have been historically. What is viewed as “underinvestment” in stocks is actually a symptom of a rise in the gross indebtedness of the global economy, enabled and encouraged by quantitative easing of central banks, which have been successful in suppressing all apparent costs of that releveraging.

The "rotation" fallacy has emerged even in the work of analysts that we admire. Ray Dalio of Bridgewater talked on CNBC last week of a move “out of” cash and “into” stocks, seemingly reversing comments he made only weeks ago at theDealbookconference (h/t PragCap) where he suggested that risk premiums are likely to expand, that the effects of QE are diminishing as we do more rounds, that we’re facing austerity, that growth is flagging, that the economy is facing unprecedented risk, and that we face a slowdown with very little room to maneuver. Meanwhile, Albert Edwards of SocGen suggested that there has been an excessive “move away from equities” in recent years – instead of noting, for example, that the volume of U.S. government debt foisted upon the public (even excluding what has been purchased by the Fed) has doubled since 2007, not to mention other sources of global debt issuance, while the market capitalization of stocks has merely recovered to its previously overvalued highs.

It’s fine to argue that perhaps investors are momentum chasers, and with profit margins now about 70% above historical norms (making stocks seem both "safe" and misleadingly cheap), with stock prices up, and with low returns on cash, investors not holding stocks will be the greater fools that allow investors who do hold stocks to get out. Indeed, that is an argument that I fully embrace as logical – the only issue being the extent to which one wants to assume the perpetual existence of a greater fool, as the supply of greater fools seems increasingly exhausted. But the problem with the “great rotation” argument is that somebody has to hold the debt. Somebody has to hold the cash. It cannot go anywhere, and it is impossible – in aggregate – for the markets to “rotate” out of it.

On the economic front, the recent decline in new unemployment claims seems to have added a great deal of steam to the bullish case. But as I noted last week, much of that effect is actually tied to the very heavy downward seasonal adjustment that accompanies initial claims data in January. Beginning this week, and continuing through about mid-March, the seasonal adjustment factors will “think” that they have already corrected for that post-holiday bulge in new claims. Given that we did not see that bulge (particularly the second week of January) and that the jobs typically end up coming off anyway when the bulge doesn’t emerge on schedule, the figures from now until mid-March are actually the ones to watch. We’ll see. Meanwhile, it’s notable that recent weeks have included significant downward revisions to the two survey components that ordinarily leap higher at the beginning of new economic recoveries - Philadelphia Fed, and the new orders component of the Chicago ISM (Institute for Supply Management) survey. Markit has begun publishing its own purchasing managers survey, which was modestly encouraging last week, but we have no historical baseline to evaluate its reliability, and find it difficult to abandon cautionary indices that have a strong record in favor of more optimistic ones with no record at all as yet.

We’re quite aware of the quote of John Maynard Keynes that “the market can stay illogical longer than the investor can remain solvent” – which as an historical aside, was in reference to his experience trading foreign currencies on margin. But it’s one thing to establish a position that risks a major wipeout of capital, and another to pursue an investment disipline that maintains a lower tolerance for risk than ordinary buy-and-hold investors require over the course of a typical market cycle. Our defensiveness is certainly uncomfortable here, but in my view, the primary risk of investors is the intolerance of missed gains in a mature bull market, impatience with a defensive position, and capitulating against both discipline and evidence.

And capitulation is everywhere. CNBC ran a story last week “Bears on the Brink: I Can’t Fight It Anymore.” Even the normally staid Alan Abelson of Barron’s finally threw in the towel last week, abandoning his own caution that stocks have run too fast, too far, and suggesting that investors let their profits run “until they start to go the other way. After all, markets rarely fall out of a bed in one fell swoop as they did in 1987 and, more recently, the turn of the century, so there’s usually plenty of time to cut and run … we hope.” I suspect that Alan is actually gagged in a closet somewhere, and that someone is submitting rogue articles in his absence. Alan, I hope very much for your timely return.

It’s interesting that Alan mentioned historical points where stocks “fall out of a bed in one fell swoop, as they did in 1987 and, more recently, the turn of the century.” Because it just so happens that we can now restrict market extremes matching the present instance to seven instances in history: 1929 (at least on the basis of imputed sentiment data), 1972, 1987, 2000, 2007, 2011, and today.

The blue lines on the chart below identify each point in history where the following overvalued, overbought, overbullish, rising yields syndrome would have been observed: S&P 500 overvalued with the Shiller P/E (the ratio of the S&P 500 to the 10-year average of inflation-adjusted earnings) greater than 18; overbought within 3% of its upper Bollinger band (2 standard deviations above the 20-period average) at daily, weekly, and monthly resolutions, more than 7% above its 52-week smoothing, and more than 50% above its 4-year low; overbullish with the 2-week average of advisory bullishness (Investors Intelligence) greater than 52% and bearishness below 28%; and yields rising with the 10-year Treasury bond yield higher than 6-months earlier. August 1929 can also be included, given that we can impute bullish/bearish sentiment with reasonable accuracy based on the size and volatility of prior market movements.

The market lost 85% between 1929-1932, lost over 50% between 1972-1974, crashed abruptly in 1987, lost over 50% in 2000-2002 and again between 2007-2009, and even lost nearly 20% in the less-memorable 2011 instance. Nobody cares. They should. They don’t. Past performance is not indicative of future returns. This time may be different. I doubt it. Enough said.

Even without suggesting that money will move “out of cash and into stocks,” one might argue that relative valuations are too wide, and that stocks should be priced to achieve lower long-term returns, given the poor returns available on bonds. On that point, it’s worth noting that we currently estimate a prospective 10-year nominal total return for the S&P 500 of just 3.9% annually. The strong one-to-one relationship between these estimates and actual subsequent market returns is presented in numerous prior weekly comments (see for exampleToo Little to Lock In).

There are certainly some periods when actual 10-year returns have deviated from the estimates implied by fundamentals (normalized earnings, forward earnings, revenues, book values, dividends). It turns out that these deviations themselves have been strikingly informative about market returns over the subsequent decade – the greater the deviation, the more the market corrects in the opposite direction. The largest negative deviation was in October 1974, when the actual annual 10-year return for the S&P 500 was about 5% lower than the projections that our valuation methodology indicated a decade earlier. That undershoot created a point of enormous undervaluation for the market (resulting in projected and actual total returns for the S&P 500 above 15% annually over the following decade). In contrast, the largest positive deviations (where the actual S&P 500 total return over the preceding 10-year period exceeded projections) were in August 1987, January 1999, February 2007, and today. The figures for the current instance are: actual total returns of about 7.6% annually for the S&P 500 over the past decade (capturing a move from a bear market low to a bull market high) versus projections of about 4.2% in 2003, based on our standard valuation methodology. In prior instances, those overshoots represented points of significant overvaluation for the market. I suspect the same is true today.

Quantitative easing and stock market returns

No discussion of present market conditions would be complete, of course, without discussing the elephant in the room, which is the continued policy of quantitative easing by the Federal Reserve.

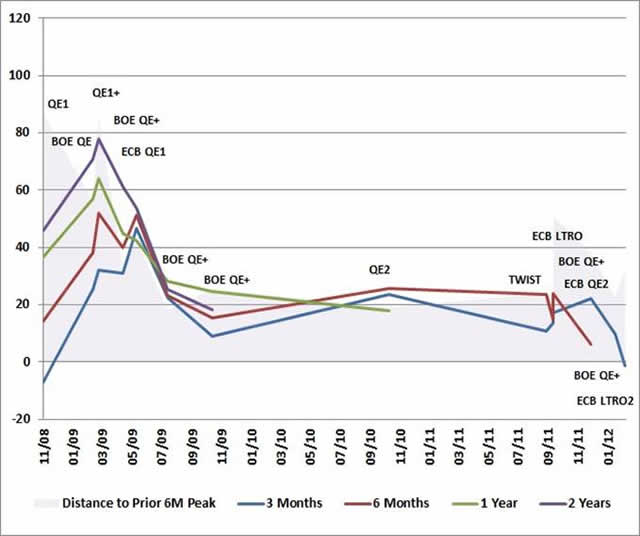

As I’ve observed before, quantitative easing both in the U.S. and internationally has had a very consistent impact on stocks. Specifically, the primary effect of QE has been to help the stock market to recover the loss that it experienced over the preceding 6-month period. The chart below shows quantitative easings by the Federal Reserve, the Bank of England, and the European Central Bank (where QE is referred to as a long-term repurchase operation or LTRO). The shaded area shows the amount of market gain that would be required to recover the peak-to-trough drawdown experienced by the corresponding stock index (S&P for Fed interventions, EuroStoxx for ECB interventions, FTSE for BOE interventions) in the 6-month period preceding the quantitative easing operation.

The lines plot the 3-month, 6-month, 1-year and 2-year market gain following each intervention, adding any gain from the low of the preceding 2 months, to account for any "announcement effects." Technically, the lines should not be connected, since they represent the gains following distinct actions of different central banks, but connecting the points shows the trend toward less and less effective interventions.

While technically not an LTRO, the ECB’s pledge last year to do “whatever it takes” (not shown) has allowed the EuroStoxx index to recover its prior 6-month loss, taking the index a few percent above its early-2012 high.

Notice that central banks have typically initiated QE interventions only when the market had somewhere in the area of 18% or more of ground to make up. Not this time, however. The most recent round of QE was associated with a market decline of just 8% from the September 2012 high in the S&P 500, and the S&P 500 has already recovered that ground to a marginal new high. The continued advance that investors expect in response to monetary easing here requires what is in some sense a “free” gain that comes without the cost of any preceding loss. There really isn’t anything in either historical data, nor in the most recent cycle, to support this expectation.

Another way to see the link between QE and stock market returns is to examine the relationship from a lead/lag perspective. The chart below presents slope estimates, showing the 6-month change in the S&P 500 as a function of the 6-month change in the monetary base, at various leads and lags. The zero lag shows the “coincident” relationship between these two in data since 2006: a strong negative relationship, with a slope coefficient of nearly -0.6 (aggressive monetary easing has largely been a response to strong market losses over the overlapping period). The earlier points show the relationship of the monetary base and preceding stock market returns, which have a consistently negative slope estimate. This is another way of saying that monetary easing today generally goes hand-in-hand with market losses that occurred at a prior date. Finally, the points where the X-axis is positive show the relationship between monetary easing and subsequent market returns. Notice that the positive relationship between monetary growth andsubsequent market returns (a coefficient about +0.4) is weaker than the negative relationship (-0.6) that initiated the monetary easing in the first place.Monetary easing induces recovery of prior market losses, not novel gains.

The key point is this: while monetary easing has been positively associated with stock market gains over the following 10 months or so, the essential driver of those gains has been the recovery of preceding losses in the months leading up to each round of QE, rather than de novo returns.

It’s also important to note that monetary growth explains only a fraction of the total variation we’ve observed in stocks. Prior to the crisis, variation in the monetary base had a very weak correlation with stock returns even on a coincident basis. Since 2006, the strongest relationship between monetary base growth and stock market returns has has been at the point where weakness in stocks leads growth in the monetary base by about 8 weeks. In contrast, the relationship between monetary growth and subsequent stock market returns has been only half that strong, explaining just over one-fifth of the total variation in stock market returns. So the effect of monetary easing should be viewed as a component of total market variation, and a response to prior market variation, not the sole driver of future returns.

To be clear – I am certainly not arguing that monetary easing has had a weak effect on stocks during the recent market cycle. To the contrary, the effect of monetary easing has undeniably been very powerful in recent years. The point, however, is that this powerful effect is almost entirely isolated to a three-step pattern: 1) stocks decline significantly over a 6-month period; 2) monetary easing is initiated, and; 3) stocks recover the loss that they experienced over the preceding 6-month period.

The present round of QE has dispensed with Step 1, which casts some doubt over the amount of follow-through we should expect from Step 3.

If the Federal Reserve follows through with QEternity through 2013, the 6-month growth of the monetary base will peak at nearly 25% (note that as the size of the monetary base grows, larger and larger dollar amounts are required to have a given impact on stocks). In the context of what the Fed has typically done over the most recent market cycle, an easing of that size would have been initiated following a market decline of about 15%, and would be associated with an expected market recovery on the order of 12%. What we actually observed prior to QEternity was a market decline of just 8%, and a subsequent recovery that has now run about 11%. Investors have already enjoyed most of the likely benefit of QEternity. It’s possible that continued quantitative easing will help to mute the potential for sustained market weakness until investors have a sense that the Fed will discontinue its purchases, but in my view, the likelihood of further material gain is limited. With no prior 6-month losses to recover, it seems likely that other factors will exert a stronger effect on market returns going forward than if the Fed’s easing had been initiated in response to a major low.

The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Only comments in the Fund Notes section relate specifically to the Hussman Funds and the investment positions of the Funds.

Fund Notes

As of last week, market conditions joined 1929, 1972, 2000, 2007 and 2011 (less memorable, but still associated with a near-20% market decline) as one of the worst periods on record to accept market risk, based on the syndrome of overvalued, overbought, overbullish, rising-yield conditions presently in place. These conditions comprise the following: S&P 500 overvalued with the Shiller P/E (the ratio of the S&P 500 to the 10-year average of inflation-adjusted earnings) greater than 18; overbought with the S&P 500 within 3% of its upper Bollinger band (2 standard deviations above the 20-period average) at daily, weekly, and monthly resolutions, more than 7% above its 52-week smoothing, and more than 50% above its 4-year low; overbullish with the 2-week average of advisory bullishness (Investors Intelligence) greater than 52% and bearishness below 28%; and yields rising with the 10-year Treasury bond yield higher than 6-months earlier. The present instance may turn out differently than past ones. The enthusiasm of investors here certainly encourages that belief. Then again, virtually by definition of the foregoing syndrome, investors were equally enthusiastic at those prior market peaks.

Strategic Growth Fund remains fully hedged, with a staggered-strike position that raises the strike price of its index put option hedges somewhat closer to market levels, representing about 1% of assets in additional option time premium looking out to springtime. We have rotated some of our holdings in Strategic Growth to reduce the potential impact of “risk on/risk off” swings in investor sentiment, but the Fund continues to have a significantly smaller weight in financials and cyclical stocks than the S&P 500, so such swings will still tend to affect the Fund on a day-to-day basis, as will large changes in significant individual portfolio holdings, which exerted both modestly positive and modestly negative impacts on day-to-day Fund returns last week. Strategic International also remains fully hedged. Strategic Dividend Value is hedged at about 50% of the value of its stock holdings – its most defensive position. Strategic Total Return continues to carry a duration of about 3.5 years in Treasury securities (meaning that a 100 basis point move in interest rates would be expected to impact the Fund by about 3.5% on the basis of bond price fluctuations), and holds about 10% of assets in precious metals shares, and about 5% of assets in utility shares.

---

Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website.

Estimates of prospective return and risk for equities, bonds, and other financial markets are forward-looking statements based the analysis and reasonable beliefs of Hussman Strategic Advisors. They are not a guarantee of future performance, and are not indicative of the prospective returns of any of the Hussman Funds. Actual returns may differ substantially from the estimates provided. Estimates of prospective long-term returns for the S&P 500 reflect our standard valuation methodology, focusing on the relationship between current market prices and earnings, dividends and other fundamentals, adjusted for variability over the economic cycle (see for exampleThe Likely Range of Market Returns in the Coming DecadeandValuing the S&P 500 Using Forward Operating Earnings).

© Hussman Funds