In July 2011, just before the market lost nearly 20% (but also the last time it corrected materially), I observed “Like Wile E. Coyote holding an anvil just past the edge of a cliff, here we are, looking down below as if there is much question about what happens next.” In my view, the stock market is hovering in what has a good chance of being seen in hindsight as the complacent lull before a period of steep losses. Meanwhile, we would require a certain amount of deterioration in stock prices, credit spreads, and employment growth to amplify our economic concerns, but even here we can say that there is little evidence of economic acceleration. Broad economic activity continues to hover at levels that have historically delineated the border of expansions and recessions.

With the S&P 500 price/revenue ratio more than twice its historical norm prior to the late 1990’s market bubble, the ratio of market capitalization to GDP also more than twice its historical norm, the most lopsided bullish sentiment in decades, an overbought market trading at a record highs – and two standard deviations above its 20-period moving averages at weekly and monthly resolutions, a “log-periodic” bubble at its most likely finite-time singularity (seeEstimating the Risk of a Market Crash), bond yields well above their 6-month average, an economy where growth in real GDP, real final sales and employment are all near or below the growth rates at which historical recessions have started, and our own estimates of prospective market return/risk quite negative based on a broad ensemble of observable market conditions, we view prospective near-term and multi-year returns as strongly unfavorable, and prospective market risk as unusually elevated.

Emphatically, our investment stance here doesn’t presume or require a market crash (though we wouldn’t rule one out). As usual, we align our view with the prevailing return/risk profile that we estimate on the basis of observable evidence at each point in time. We have no downside target for the market, nor do we rely on any particular scenario. We estimate likely return/risk as conditions change over time. These estimates have been persistently negative in the face of the recent market advance because similarly extreme conditions throughout history have come to dismal ends. Our stance will change as the evidence does.

On valuation, we continue to see extremes in a broad range of measures that are very well correlated with actual subsequent market returns. Of course, there are some measures like the “Fed Model” (forward earnings yields less 10-year Treasury yields) that are fairly benign, and suggest no valuation concerns at all. The problem is that these alternative models don’t perform nearly as well in explaining actual subsequent market returns. Much of the reason is that they take profit margins at face value even when margins are elevated. At present, this is equivalent to assuming that the current extreme in profit margins will be permanent, and then fully reflecting that assumption in stock prices, even when all of history demonstrates that margins are cyclical.

We can calculate the historical errors of various valuation models in forecasting actual subsequent 7-10 year market returns. A good model should have random errors – that is, the errors should not themselves be highly predictable based on data that was readily available at the time. For the “equity risk premium” models that Janet Yellen and Alan Greenspan often reference as evidence that stocks are not overvalued, it turns out that the errors of these models have a correlation of about 85% with profit margins that were observable at each point in time. In other words, these models make large and systematic errors because they fail to account for the cyclical variation of profit margins over time (seeAn Open Letter to the FOMC: Recognizing the Valuation Bubble in Equities, andThe Coming Retreat in Corporate Earnings).

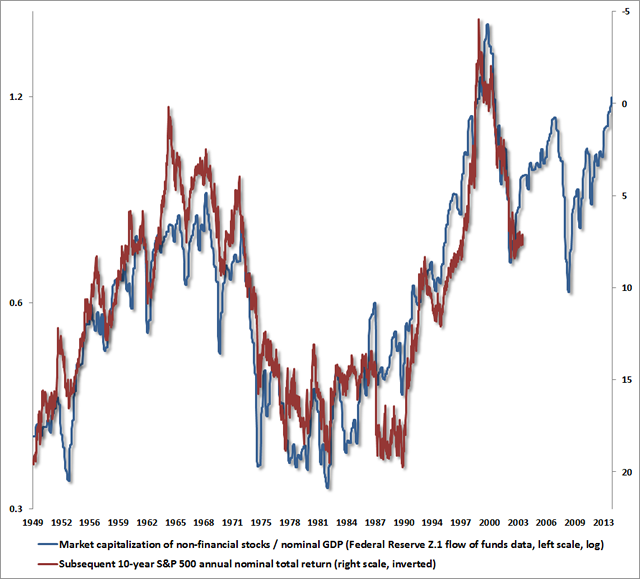

A few quick charts will bring some of our present concerns up to date. The chart below shows the ratio of nonfinancial equity market capitalization to GDP. Again, this measure is about twice its pre-bubble norm, and is presently associated with an expectation of negative total returns for the S&P 500 over the coming decade. Measures based on properly normalized earnings are a little bit more favorable, with the overall outcome that we broadly expect nominal total returns for the S&P 500 of about 2.3% annually over the coming decade, with negative total returns on horizons of less than about 7 years.

Keep in mind that the 2000-2002 decline wiped out the entire total return of the S&P 500, in excess of Treasury bills, all the way back to May 1996. The 2007-2009 decline wiped out the entire total return of the S&P 500, in excess of Treasury bills, all the way back to June 1995. Our present expectations are rather conservative by comparison.

On the economic front, we really don’t take a great deal of “signal” from the December payroll report, which fell short of expectations. The fact is that the seasonal adjustment for January alone was 876,000 jobs (and the change in the seasonal adjustment was 320,000 jobs). It’s quite difficult to get a good read from monthly employment changes just before and after the holidays.

Normally, we can get useful economic signals from a broad range of leading measures such as various components of Fed surveys and purchasing managers indices, but in the face of repeated bouts of quantitative easing, the correlation between the most historically reliable leading measures and subsequent economic outcomes has been utterly destroyed in recent years (though probably only temporarily). Indeed, the correlation has actually turned negative (seeWhen Economic Data is Worse than Useless).

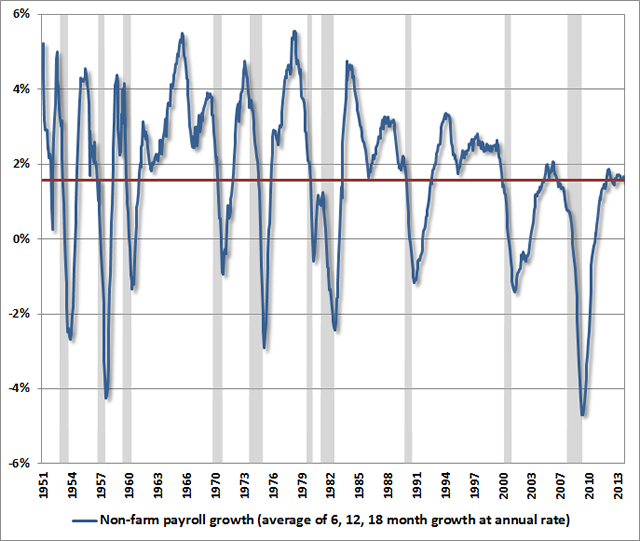

Given that leading measures have been of no use at all in gauging economic activity, a reasonable (though somewhat lagging) gauge of the economy is to examine growth rates in output and employment (though on much more than a month-to-month basis). On that front, we continue to observe an economy that hovers at the border that has historically delineated expansions from recessions. I think it’s quite optimistic to believe that this situation has improved considerably in recent months – we see little basis for that inference. At the same time, we’ve seen a far longer period of “hovering” at this edge than in prior economic cycles – about three years in fact, with very little variation. This hovering and negative correlation between leading economic measures and actual economic outcomes has made it very difficult to form economic expectations in this cycle. In any event, we don’t observe any meaningful acceleration.

It’s worth emphasizing that our market concerns are rather independent of our economic views here. Given elevated valuations, thin risk premiums, and heavy issuance of low-quality debt in recent years, economic deterioration would contribute a great deal to weakness in the financial markets. However, our concerns about financial weakness aren’t predicated on expectations of economic weakness. The likelihood of poor market returns is largely baked into the present set of overvalued, overbought, overbullish, rising-yield conditions. I’ll note in passing that market peaks tend to be associated with strong consumer confidence and low new claims for unemployment, so neither of those provide any comfort about stocks. Of course, the deepest market declines in history have also eventually been complicated by recession, but it’s not advisable to wait for that. The market has typically experienced deep losses well before even a hint of recession has become evident to the consensus of economists.

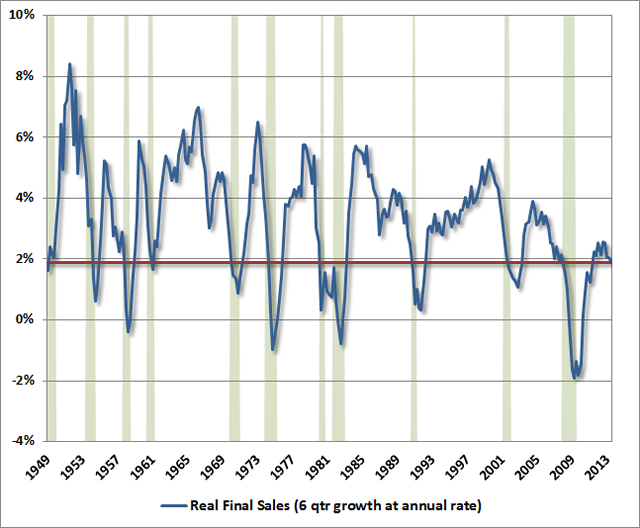

The chart below shows the growth of real final sales (GDP less inventory accumulation) over the past 6-quarters. The chart of real GDP itself is quite similar, but real final sales give a complementary picture of final demand. Presently, activity is at levels about where previous recessions have started.

That’s not an assertion that a recession must begin in this instance. Our own recession concerns would spike if the S&P 500 was to decline below its level of 6-months prior, employment growth was to slow another few tenths of a percent (to about 1.4% on a year-over-year basis or 0.5% on a 6-month trailing basis), and credit spreads (the difference between corporate bond yields and Treasury bond yields) were to perk up a bit more. For now, the main point is that there is little evidence of a material shift in economic prospects. The economy continues to hover at the borderline that has historically delineated expansion from recession.

Past performance does not ensure future results, and there is no assurance that the Hussman Funds will achieve their investment objectives. An investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted above. More current performance data through the most recent month-end is available at www.hussmanfunds.com. Investors should consider the investment objectives, risks, and charges and expenses of the Funds carefully before investing. For this and other information, please obtain a Prospectus and read it carefully.

© Hussman Funds