Nice article this week from someone who knows our work well - Jonathan Laing, the senior editor at Barron’s Magazine. He emphasizes our concerns about valuation and the need to account for the effect of profit margin variation, which can "make stocks seem beguilingly cheap at market peaks," duly observes our miss in this half-cycle (though stress-testing wasn't discussed), “after deftly side-stepping the dotcom- and housing bubble-crashes," and adds "We expect some vindication of his obduracy may lie ahead.” No argument here.

One of the things that some forget is that we shifted to a constructive stance between those two crashes in early 2003, and initially moved toward a constructive stance after the market collapsed in late-2008 (see Why Warren Buffett is Right and Why Nobody Cares) until a parade of policy errors forced us to entertain Depression-era outcomes. My 2009 stress-testing miss and the awkward transition that resulted certainly injured my reputation during this uncompleted half-cycle. Still, having addressed that “two data sets” problem, I expect no similar stress-testing response in future market cycles. Meanwhile, I have every expectation that the current speculative extremes will end in tears for those inclined to dismiss hard, historically reliable evidence by mumbling “permabear.” On the bright side, the conclusion of the present cycle and the course of those that follow are likely to provide strong, extended opportunities to take aggressive investment exposure. Now would just be a particularly inopportune moment to do so.

Extraordinary market returns and dismal market returns both come from somewhere. Long periods of outstanding market returns have their origins in depressed valuations. Long periods of dismal market returns have their origins in elevated valuations. The best way to understand the returns that investors can expect over the long-term is to have a firm understanding of where reliable measures of valuation stand at each point in time.

A few quick valuation studies may be helpful. As the workhorse for these studies, we'll use the ratio of market capitalization to GDP. Warren Buffett observed in a 2001 Fortune interview that "it is probably the best single measure of where valuations stand at any given moment."

A variety of normalized earnings measures could be used as well, but emphatically, what should not be used is any price/earnings measure that is not adjusted for the variation of profit margins over the economic cycle. That includes the "Fed Model" and any number of "equity risk premium" measures, which actually have a rather weak correlation with actual subsequent market returns. For more evidence on why margin variation is important to consider, see Margins, Multiples, and the Iron Law of Valuation.

Quick Valuation Study: 1950

In 1950, the ratio of market capitalization to GDP was at 0.40, while the dividend yield on the S&P 500 was 6.7%. Over the next decade, nominal GDP would grow by about 6.3% annually, and the ratio of market cap to GDP would increase to its (pre-bubble) historical norm of 0.63. As a result, the S&P 500 would go on to post total returns averaging nearly 18% annually over the following decade.

Stay with me here. It’s critical to understand the basic arithmetic behind those outstanding market returns.

The capital gains portion of that annual return was driven by two pieces: the growth in nominal GDP, and the reversion in the ratio of market capitalization to GDP toward its historical norm. Given the numbers above, that piece comes out to:

(1+nominal GDP growth)*(normal MCAP/GDP ratio / actual MCAP/GDP ratio)^(1/10) – 1.0

(1.063)*(0.63/0.40)^(1/10) – 1.0 = 11.2% annually for capital gains

Now add in the 6.7% dividend yield, and you’ve got – not surprisingly – 17.9% annually.

Quick Valuation Study: 1982

Let’s try that again. In 1982, the ratio of market capitalization to GDP had fallen to 0.35, while the dividend yield on the S&P 500 had again soared to 6.7%. Nominal GDP growth over the following decade would remain close to its historical average peak-to-peak growth rate across economic cycles, roughly 6.3% annually.

Assuming long-term mean-reversion in the ratio of market cap to GDP, what might you have expected the annual total return of the S&P 500 to be, in the decade following the 1982 low? Do the math:

(1.063)*(0.63/0.35)^(1/10) – 1.0 + 0.067 dividend yield = 19.4% annually.

That estimate would have been almost precisely correct. While small variations in GDP growth and dividend yield can change that basic math in a small, fairly linear way, the main factor behind the outstanding total returns in the decade following the 1982 low was the remarkably depressed initial valuation of the market, reflected by the market capitalization to GDP ratio, and the gradual reversion toward less extreme valuations over a period of years.

Quick Valuation Study: 2000

In early 2000, the ratio of market capitalization to GDP reached the highest level in history, at 1.54, while the dividend yield of the S&P 500 was just 1.1%. At that point, a reasonable estimate of subsequent 10-year total returns for the S&P 500 would have been:

(1.063)(0.63/1.54)^(1/10) – 1.0 + .011 = -1.7% annually.

That is just what we were saying in 2000: negative total returns for a decade. Those concerns were predictably shrugged off, as they are today. But in fact, the S&P 500 lost value exactly as expected. Importantly, this outcome was not simply an artifact of the 2008-2009 market decline. By early 2010, when that 10-year period ended, the S&P 500 was already 80% above its March 2009 low (in hindsight thanks to the March 2009 change to accounting rule FAS 157), yet had still posted a negative 10-year total return. The actual total return of the S&P 500 from 2000 to the 2009 low was considerably worse than -1.7% annually.

Quick Valuation Study: 2000 to 2014

Let’s take a slightly longer horizon, from 2000 until today. A 14-year estimate of total returns from the 2000 peak would change only one thing in the equation above, which is the number of years. The estimate from 2000 to the present would have been:

(1.063)(0.63/1.54)^(1/14) – 1.0 + .011 = 0.8% annually.

As it happens, the S&P 500 has achieved a greater return over these past 14 years. In fact, the annual total return has averaged 3.5% annually. Moreover, the market has squeezed out this higher rate of return even though the actual growth rate for nominal GDP since 2000 has averaged just 3.9% instead of the historical peak-to-peak growth rate of 6.3% annually.

Why have market returns been able to average even 3.5% over the past 14 years? Simple. Valuations have been pushed, once again, to some of the highest levels in history. Instead of terminating this 14-year period anywhere near historical norms, the ratio of market capitalization to GDP presently stands at 1.25, which is double its historical norm.

Here’s another way to understand this outcome. Considering both the overshoot of returns and the undershoot of nominal GDP growth, one would have expected the total return of the S&P 500 over the past 14 years to be 5.1% lower than we’ve actually observed (0.8% - 3.5% + 3.9% - 6.3%). Compounding a 5.1% overshoot for 14 years now places valuations at double their historical norm.

Importantly, this level of overvaluation isn't simply true for market capitalization to GDP, but for a variety of other historically reliable measures that have a roughly 90% correlation with actual subsequent market returns (see It is Informed Optimism to Wait for the Rain).

Quick Valuation Study: 2009

Let's do this one. In March 2009, the ratio of market cap / GDP fell to 0.60, while the S&P 500 dividend yield briefly hit 3.6% at the market's low. What might we estimate for 10-year S&P 500 total returns, measured from that market trough?

(1.063)(0.63/0.60)^(1/10) – 1.0 + .036 = 10.4% annually.

So as we noted at the time, stocks were - briefly - quite reasonably valued on a historical basis in 2009. Our other methods placed projected returns at that time in a range between 10-14%. It's no secret that my insistence on stress-testing against Depression-era outcomes resulted in a miss that both our pre-2009 methods or current ones could have captured. But without our current, stress-tested methods in hand, we faced the reality that similar valuations in the Depression were followed by an additional two-thirds loss in the stock market, while many measures of market action that were reliable in post-war data were badly whipsawed during the Depression.

In any event, those prospective returns have already been realized, and investors can now reasonably expect negative total returns on every horizon shorter than about 7 years. With the upward half of this market cycle behind them, and the completion of this market cycle still ahead, investors are chasing a critter that is already in their pocket, tail and all, and is gnawing to get out.

Quick Valuation Study: 2014

Let’s assume that despite the weak economic growth at present, nominal GDP picks back up to a nominal growth rate of 6.3% annually from here. This may be overly optimistic, but near market peaks, optimistic assumptions often still result in troubling conclusions (recall our 2007 piece An Optimistic Route to a Poor Market Outlook). Given the present market cap / GDP ratio of 1.25 and an S&P 500 dividend yield of just 2%, what might we estimate for total returns over the coming decade?

(1.063)(0.63/1.25)^(1/10) – 1.0 + .02 = 1.3% annually.

Since we use a whole range of additional measures, including earnings-based methods, to estimate prospective returns, our actual estimates are somewhat higher here, at about 2.4% annually over the coming decade. Tomato. Tom-ah-to. Keep in mind that these estimates assume a significant acceleration in economic growth. One can certainly quibble that the long-term ratio of market capitalization to GDP will have a somewhat higher norm in the future. But the present ratio is still100% above its pre-bubble norm. It’s unlikely that this situation will end well.

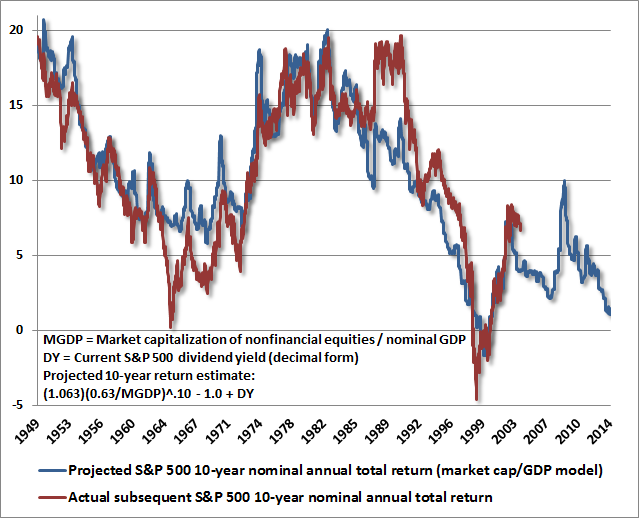

The chart below shows the record of these estimates since 1949, along with the actual 10-year S&P 500 total returns that have followed.

As the Buddha taught, “This is like this, because that is like that.” Extraordinary long-term market returns come from somewhere. They originate in conditions of undervaluation, as in 1950 and 1982. Dismal long-term returns also come from somewhere – they originate in conditions of severe overvaluation. Today, as in 2000, and as in 2007, we are at a point where “this” is like this. So “that” can be expected to be like that.

The Federal Reserve’s Two Legged Stool

“Fundamental to modern thinking on central banking is the idea that monetary policy is more effective when the public better understands and anticipates how the central bank will respond to evolving economic conditions… Recall how this worked during the couple of decades before the crisis. The FOMC's main policy tool, the federal funds rate, was well above zero, leaving ample scope to respond to the modest shocks that buffeted the economy during that period. Many studies confirmed that the appropriate response of policy to those shocks could be described with a fair degree of accuracy by a simple rule linking the federal funds rate to the shortfall or excess of employment and inflation relative to their desired values. The famous Taylor rule provides one such formula.”

- Janet Yellen, FOMC Chair, April 16 2014

In her first public speech on monetary policy, Janet Yellen made it clear that the Fed intends to pursue a more rules-based, less discretionary policy. This is good news. The bad news, however, is that Yellen focused only on employment and inflation. In that same speech, not a single word was said about attending to speculative risks or financial instability (which are inherent in Fed-induced, yield-seeking speculation). Without attending to that third leg, the Fed is resting the fate of the U.S. economy on a two-legged stool.

The problem is this. In viewing the Fed’s mandate as a tradeoff only between inflation and unemployment, Chair Yellen seems to overlook the feature of economic dynamics that has been most punishing for the U.S. economy over the past decade. That feature is repeated malinvestment, yield-seeking speculation, and ultimately financial instability, largely enabled by the Federal Reserve’s own actions.

To overlook yield-seeking speculation as a central element connected to the Federal Reserve’s mandate is to invite a repeat of dismal economic consequences over and over again. The Fed’s mandate need not explicitly refer to financial stability – it is enough to recognize that the failure to take speculation, malinvestment, and financial stability seriously has been one of the primary causes of economic and financial crises that prevent the Fed from achieving that mandate. Indeed, the Fed has again baked such consequences into the cake as a result of its policy of quantitative easing, and an associated lack of appreciation for how equity valuations work (particularly the need to consider valuation multiples and profit margins jointly, whenever one uses earnings-based measures).

Nearly every argument that stocks are not in a “bubble” begin with an appeal to 2000, arguing that present conditions are not nearly as extreme as then, so the word “bubble” cannot be accurately applied. Technically, the word “bubble” also implies certain mathematical features, such as violations of “transversality.” Maybe it’s better to use the phrase “speculative extreme.”

While 2000 was certainly the most extreme period of equity speculation in U.S. financial history (taking valuations well beyond even what was observed at the 1929 peak), it is certainly not the only one that deserves that distinction. For example, in 1901, valuations reached a peak that would be followed by a 20-year period of negative real total returns. Stock prices were below the 1901 peak even two decades later. Undoubtedly 1929 would fall into the definition of a speculative extreme, as it was also followed by a 20-year period of negative real total returns. And while valuations in the mid-1960’s did not reach similar extremes, they too were followed by nearly two decades of negative real total returns, with the level of the S&P 500 little changed even 18 years later.

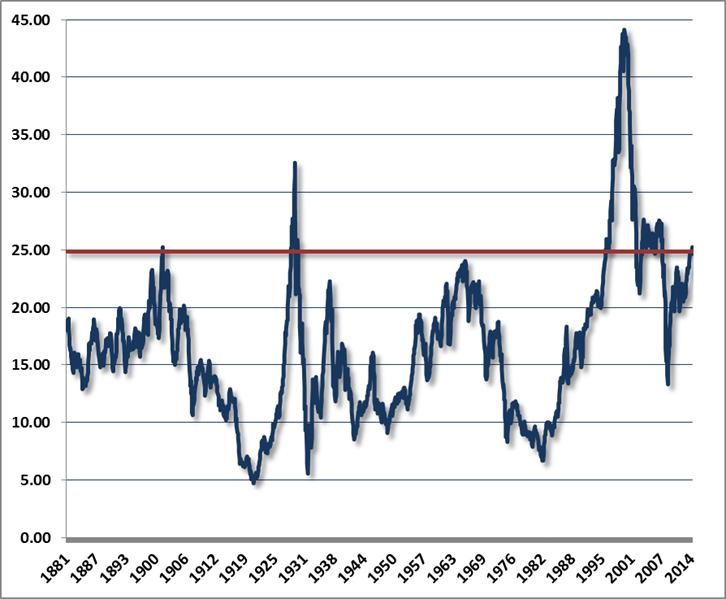

The chart below shows the position of valuations on the basis of Robert Shiller’s cyclically-adjusted P/E. As I’ve noted elsewhere, the reliability of the Shiller metric is greatly improved by adjusting for the implied level of profit margins (Shilller “earnings” divided by S&P 500 revenues) embedded into that P/E. At normal profit margins, the Shiller P/E would presently be above 30.

Remember also that the 2000-2002 decline wiped out every bit of S&P 500 total return, in excess of Treasury bill returns, all the way back to May 1996, and that the 2007-2009 decline wiped out every bit of the market’s excess return all the way back to June 1995. Valuations were stretched to further extremes for a few months in 1929, as well as in 2000 and 2007, but those gains were the first to be surrendered. The possibility that valuations may become stretched further in the short-term doesnothing to remove concern about dismal long-term returns even if we take the Shiller P/E at face value.

On the basis of other measures that are even better correlated with actual subsequent market returns, valuations now meet or exceed the levels observed at prior market extremes in history that were followed by 18-20 year periods of negative real returns. We call these extremes not just “cyclical” but “secular” market peaks. Present market extremes can only be excluded from this class of speculative instances if we restrict the definition of "extreme" to the 2000 peak alone. Even then, the price/revenue ratio of the median stock is now higher than in 2000 (as smaller capitalization stocks were much more reasonably priced at the 2000 peak than today).

Make no mistake. The Federal Reserve’s policy of quantitative easing has starved investors of all sources of safe return, provoking them to reach for yield in more speculative assets, including equities, leveraged loans, covenant-lite debt, and other securities. Having stomped on the pedal for years, all of these asset classes are valued at levels that are strenuously elevated from a historical perspective, and as a result, offer strikingly poor prospective returns for long-term investors.

To quote a decades-old passage by economist Ludwig von Mises, and as a reminder of what weshould have learned after Fed-induced yield-seeking led to a reckless expansion of mortgage debt, a bubble in housing, and the worst economic collapse in modern times: “The recurrence of periods of boom which are followed by periods of depression is the unavoidable outcome of the attempts, repeated again and again, to lower the gross market rate of interest by means of credit expansion. True, governments can reduce the rate of interest in the short run. They can issue additional paper money. They can thus create an artificial boom and the appearance of prosperity. But such a boom is bound to collapse soon or late and to bring about a depression.”

Friedrich Hayek concurred “To combat depression by a forced credit expansion is to attempt to cure the evil by the very means which brought it about; because we are suffering from a misdirection or production, we want to create further misdirection - a procedure which can only lead to a much more severe crisis as soon as the credit expansion comes to an end.”

Frankly, I don’t have any strong impression that economic outcomes in the completion of the present cycle must be severe. Further policy mistakes would be required beyond a QE-induced speculative run. On the other hand, I have no doubt at all that having driven equity valuations to present levels, investors will be starved of total return – from current prices – for at least a decade (assuming valuations never move below historical norms), and possibly much longer (in the event that valuations do indeed move below historical norms 15 or 20 years from today).

Keep in mind, however, that a significant retreat in valuations even over the next couple of years could dramatically reverse this situation, creating the prospect for very good long-term investment returns from those lower price levels. I remain very optimistic that strong opportunities will emerge even over the completion of the present cycle. Given supportive conditions and the absence of extremely overvalued, overbought, overbullish syndromes, reasonable opportunities would not even require a retreat to historically “normal” valuations. It’s just that from current price levels, the prospect of adequate long-term returns is thin. In short, the same amount that investors are likely to obtain by selling equities years from now is already sitting on the table for the taking today. For investors without multi-decade horizons, it may be wise to use that opportunity.

Margins and Multiples in 3D

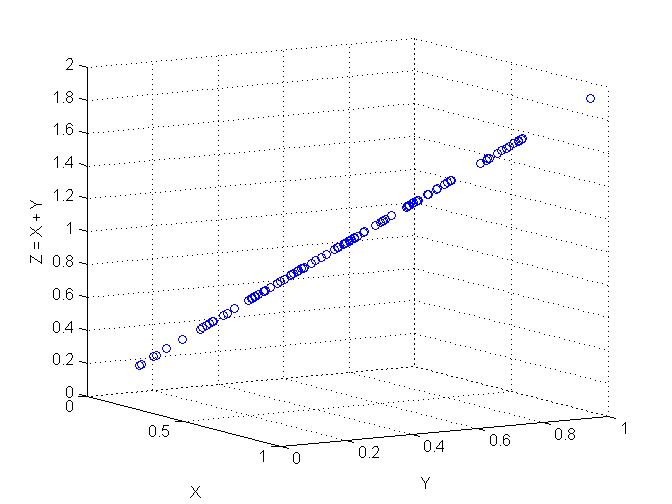

As I noted last week, valuation multiples based on earnings cannot be taken at face value without correcting for the level of profit margins embedded in those earnings (see Margins, Multiples, and the Iron Law of Valuation). A good way to see the effect of factors that cooperate is to examine their effect in 3D. For example, in the chart below, I’ve simulated 100 random values for X and 100 random values for Y. The level on the Z axis is X+Y. If we look at X versus Z head on, or Y versus Z head on, we observe some relationship, but it’s very imperfect. But if we examine X, Y and Z on a 3D plot, from the perspective of the maximum X and the minimum Y (or vice versa), the combined relationship suddenly becomes obvious. Clearly, the highest level of Z is associated with points where both X and Y are simultaneously elevated.

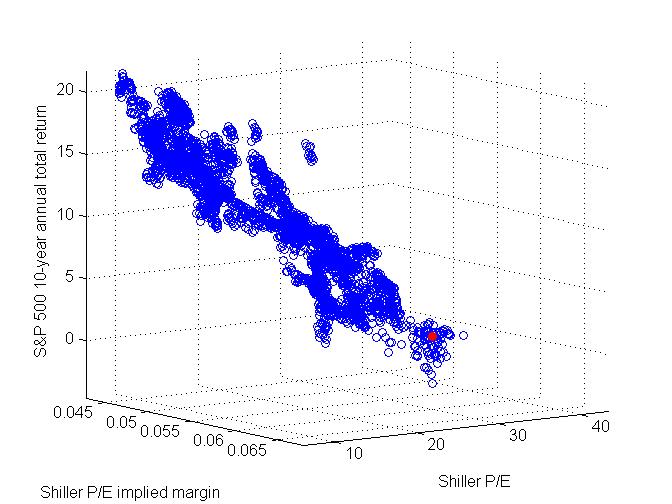

Likewise, the following chart offers a good perspective of why the Shiller P/E is more useful when the impact of profit margins is considered explicitly. It shows the Shiller P/E and the embedded margin from a 3D perspective (technically, the P/E and margin should be plotted on log scale, but the overall plot is little changed by using standard values). The worst market returns, hands down, follow rich P/E ratios, where the earnings themselves reflect elevated profit margins (as we observe presently). For comparative purposes, the current data point is presented in red, with an associated 10-year total return projection hardly above zero.

Of course, the same analysis can be replicated with a variety of earnings-based methods. The implication is very consistent – price/revenue and market capitalization/GDP are generally more reliable metrics of long-term valuation than earnings-based valuation measures that quietly embed the assumption that profit margins will remain permanently depressed or elevated. That’s certainly not to say that earnings are unimportant, but rather that stocks are a claim on a very, very long-term stream of future cash flows, and year-to-year earnings (and even 10-year smoothed earnings) are often poor indications of that long-term stream.

So yes, the equity market is in extremely speculative territory. For the median stock, the overvaluation is more extreme than in 2000. For the broad capitalization-weighted market, the Fed has elevated valuations to the level that promises poor investment returns, and negative real returns – from present levels – for at least a decade. If the Fed truly wishes to achieve its mandate of long run price stability and maximum employment, another leg of the stool is needed in Fed policy, and that is the avoidance of actions that promote yield-seeking speculation and malinvestment.

It is too late to avoid that outcome in this cycle, as it has already occurred. Now we must manage the consequences. One hopes that those consequences will be contained to the financial markets and not the broad economy. Oversight – particularly in leveraged equity, leveraged loans, and covenant lite lending – should be far higher on the agenda than promoting further overvaluation and speculation, in the hope that some small benefit will trickle down to the masses.

Past performance does not ensure future results, and there is no assurance that the Hussman Funds will achieve their investment objectives. An investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted above. More current performance data through the most recent month-end is available at www.hussmanfunds.com. Investors should consider the investment objectives, risks, and charges and expenses of the Funds carefully before investing. For this and other information, please obtain a Prospectus and read it carefully.

(c) Hussman Funds