With advisory sentiment running at 56% bulls and fewer than 20% bears, with most historically reliablevaluation metrics about twice their pre-bubble norms (and presently associated with negative expected S&P 500 nominal total returns on every horizon of 7 years and less), with capitalization-weighted indices near record highs but smaller stocks and speculative momentum stocks diverging badly, and with a Federal Reserve clearly intent on winding down the policy of quantitative easing that has brought these distortions about, we continue to view the present market environment as among the most dangerous instances in history.

Major market peaks, even those like 2000 and 2007 that were followed by 50% losses, have never felt dangerous at the time. That’s why they were associated with exuberant price extremes. Sure, investors had a sense that prices had advanced a great deal, but endless reasons could be found to justify the advance. Avoiding major losses required an intimate familiarity with market history, and enough discipline and patience to maintain what Galbraith called a “durable sense of doom” about observable conditions. The general rule is that you don’t observe the “catalyst” in advance, only the stack of dynamite.

Over the years, we’ve repeatedly emphasized that the very best investment opportunities are associated with a significant retreat in valuations that is then coupled with early improvement in market internals across a broad range of stocks, industries, and security types. Conversely, the very worst market outcomes are associated with overvalued, overbought, overbullish conditions that are then coupled with divergences in market internals and a loss of uniformity (as we observe today). As I wrote in October 2000, “when the market loses that uniformity, valuations often matter suddenly and with a vengeance. This is a lesson best learned before a crash rather than after one.”

None of the market cycles we’ve observed in recent decades have been exceptions to these general rules. It’s true that investor enthusiasm about the novelty and size of quantitative easing has prolonged speculative extremes beyond most prior instances, but understand that those prior instances are limited to 1929, 1972, 1987, 2000, 2007 and a brief point in 2011 that was followed by a near-20% market retreat (see It is Informed Optimism to Wait for the Rain). To the extent that speculative pressures have pushed further in the broad stock market, the eventual payback is likely to be distressing.

Make no mistake, reliable valuation measures for the median stock are actually more extreme today than in 2000. On a capitalization-weighted basis, valuations are beyond every pre-bubble point in history except for a few months in 1929. In the bubble that ended in 2000, final valuations were higher owing to the extremes in large-capitalization technology stocks at that peak. Many observers seem to believe that valuations are of no concern unless they match that singular extreme. Good luck on that. The novelty, imagination, and extrapolation born of the late-1990’s internet and technology revolution is unlikely to be matched by an economy that can’t post growth beyond the threshold between expansion and recession despite the largest monetary intervention in history. The Fed is already retreating from that intervention, and for good reason, because while the Fed's extraordinary actions are not actually linked to real economic outcomes, they encourage very risky speculative side-effects.

Meanwhile, an average, run-of-the-mill bear market would wipe out the entire advance in the S&P 500 Index since April 2010. Even on a total return basis, I doubt that any of the market’s gains from that point will actually be retained by investors by the completion of the present cycle.

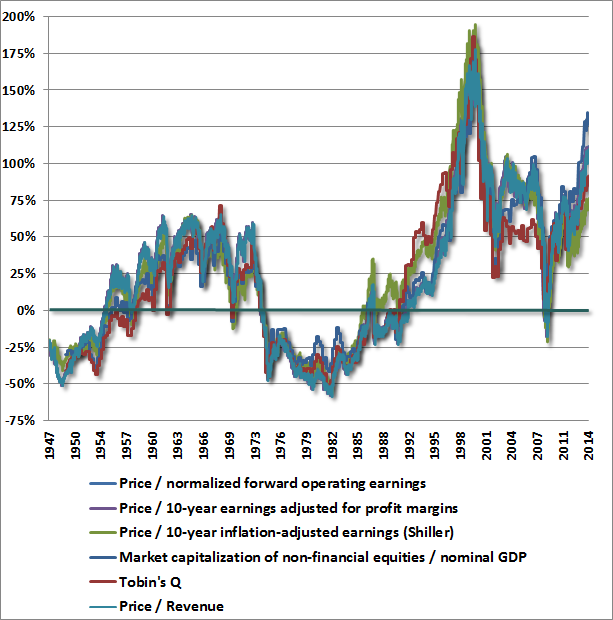

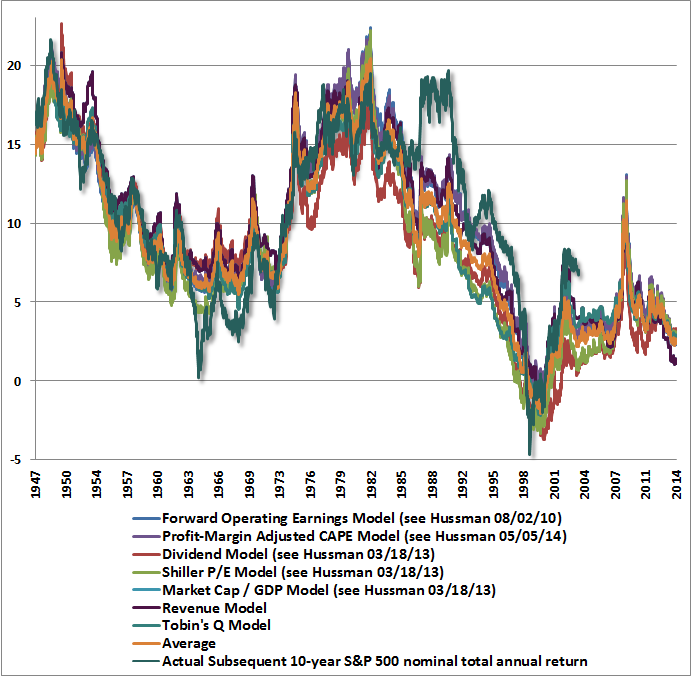

We currently estimate S&P 500 nominal total returns averaging about 2.4% annually over the coming decade. The two charts below bring the situation up to date. The first presents numerous historically reliable measures of market valuation, presently averaging just over double their pre-bubble norms. The second converts these measures to projected S&P 500 total returns over the coming decade (see the referenced weekly comments for the algebraic calculations involved here), and compares these projections with actual subsequent 10-year S&P 500 total returns.

Needless to say, the valuation picture is not encouraging for long-term investors, but that emphatically does not imply that we need valuations to normalize fully in order to justify a constructive position. Even a fairly moderate retreat in valuations, followed by early improvement in market action, could provide a constructive opportunity. However, a shallow retreat in valuations invites a smaller response, so we would be likely to encourage at least a line of put option protection as a safety net in that event. Investors relying on the Fed to provide a safety net against major losses should recall that aggressive monetary easing throughout 2000-2002 and 2007-2009 did not prevent the market from falling in half in either instance. Much of what investors believe about the “effectiveness” of QE is purely psychological. Except for short-term Treasury bills, there is no reliable or mechanistic relationship that links the size of the monetary base to the price of financial assets or the real activity of the economy.

Setting the record straight

It may be helpful to set our longer-term record straight, as it may explain why we are so confident in pursuing our full-cycle discipline here. With one primary exception, that record is a chronicle of becoming constructive or aggressive when improved valuations are coupled with early improvement in market action, and becoming defensive when overvalued, overbought, overbullish conditions emerge – particularly once market internals lose uniformity and become divergent.

Following the 1990 bear market, these considerations allowed me for years to be a leveraged, “lonely raging bull” (in the words of the Los Angeles Times). As the decade continued and valuations became progressively extreme, market conditions gradually moved us to a highly defensive stance in the late-1990’s. We were certainly early, but the market collapse that followed wiped out the entire total return of the S&P 500, in excess of the return on Treasury bills, all the way back to May 1996. Whatever returns we missed from not joining the speculation were ripped from the portfolios of others by the end of the 2000-2002 bear market anyway, and our approach navigated that market decline quite nicely, thank you.

Following the 2000-2002 bear market, we shifted to a constructive stance, observing “we have no evidence to hold anything but a constructive position.” Though valuations weren’t particularly attractive, the shift was based – not surprisingly – on a significant retreat in valuations coupled with early improvement in market internals. As valuations became progressively extreme, we moved back to a highly defensive position. The market collapse that followed would wipe out the entire total return of the S&P 500, in excess of the return on Treasury bills, all the way back to June 1995. Remember – risk management is generous. As I noted approaching the 2007 peak (see Rip Van Winkle), whatever returns that disciplined, value-conscious investors “miss” in overvalued markets are rarely retained by other investors anyway.

In late-2008, with the market down more than 40%, we made an initial shift to a constructive position, though still advising a line of index put option defense, which helped enormously in what followed (see Why Warren Buffett is Right and Why Nobody Cares – and read that piece carefully if you incorrectly believe I am a “permabear”). That shift was based – not surprisingly – on a significant retreat in valuations coupled with an early improvement in market internals. The problem was that measures of “early improvement in market internals” which proved quite reliable throughout the post-war period proved to be inadequate during the credit crisis of late-2008. As we discovered when we took our methods to Depression-era data, they performed fine overall, but they were repeatedly whipsawed in that data and allowed intolerably deep - if temporary - drawdowns along the way (as did popular trend-following methods).

So our partial shift to a constructive position was followed by an awkward stress-testing transition to ensure that we could navigate Depression-like outcomes (we called this our "two data sets problem" at the time). The immediate effect was a significant “miss” in the interim that both our pre-2009 methods and our present methods – had they been available at the time – could have captured. That transition was further complicated by quantitative easing, which required us to essentially reintroduce certain bubble-tolerant features of our pre-2009 methods. That said, nothing in the historical record indicates that we should be tolerant of present extremes.

The reason we repeatedly discuss our stress-testing challenge earlier in this cycle is not to excuse the missed returns that resulted. Rather, the point is to underscore that investors should not infer, based on that miss, that present market risks can be safely ignored. I’ve got very thick skin for criticism of what I viewed as a fiduciary duty to stress-test our methods earlier in this cycle. Go at it, but understand that none of those criticisms alter objective historical market evidence, or make the present situation any less likely to result in deep stock market losses.

In short, market cycles across a century of market history encourage us to maintain a risk-sensitive, value-conscious discipline that becomes constructive or aggressive when improved valuations are coupled with early improvement in market action, and becomes defensive when overvalued, overbought, overbullish conditions emerge – particularly once market internals lose uniformity and become divergent.

It is a misguided non-sequitur to observe our stress-testing miss earlier in this cycle and use that observation to conclude that present speculative conditions will end differently than they did following similar pre-collapse conditions in 1929, 1972, 1987, 2000, and 2007 (as well as a brief instance in 2011 just before the S&P 500 lost nearly 20%).

If you believe history has nothing to teach because of our experience since 2009, you’re allowing our stress-testing miss to obscure a much larger picture. To paraphrase the same warning I offered in 2000 and 2007: If you think the market is not going to lose a large fraction of its value over the next few years, a century of history thinks you’re wrong.

“Monetary Policy Going Forward: De-Spiking the Punch Bowl 10 Ounces at a Time”

The header above is from a speech on Friday by FOMC voting member Richard Fisher. Take a moment to understand what he is saying (emphasis added):

“The Federal Open Market Committee (FOMC) is in the process of winding down its massive purchases of Treasuries and mortgage-backed securities. At our last meeting, in recognition that the economy is improving and acknowledging that we have generated massive amounts of excess reserves among depository institutions operating in the U.S., we voted to reduce our purchases to a combined $45 billion per month, on the path to eliminating them at the earliest practicable date. Speaking only for myself as a voting member, barring some destabilizing development in the real economy that comes out of left field, I will continue to vote for the pace of reduction we have undertaken, reducing by $10 billion per meeting our purchases and eliminating them entirely at the October meeting with a final reduction of $15 billion.

“I was not for this program, popularly known as QE3, to begin with. I doubted its efficacy and was convinced that the financial system already had sufficient liquidity to finance recovery without providing tinder for future inflation. But I lost that argument in the fall of 2012, and I am just happy that we will be rid of the program soon enough.

“I am often asked why I do not support a more rapid deceleration of our purchases, given my agnosticism about their effectiveness and my concern that they might well be leading to froth in certain segments of the financial markets. The answer is an admission of reality: We juiced the trading and risk markets so extensively that they became somewhat addicted to our accommodation of their needs… you can’t go from Wild Turkey to cold turkey overnight. So despite having argued against spiking the punchbowl to the degree we did, I have accepted that the prudent course of action and the best way to prevent the onset of market seizures and delirium tremens is to gradually reduce and eventually eliminate the flow of excess liquidity we have been supplying… one would be hard pressed to say that ending our asset purchases, which the depository institutions from which we buy them deposit back with us as excess reserves, would deny the economy needed liquidity. The focus of our discussions now is when and how to ‘normalize’ monetary policy.”

That sucking sound you hear is the Federal Reserve exiting from the most reckless policy experiment in its history. Unfortunately, that policy experiment has been the primary driver of speculation in recent years. One can’t rule out some stall in the tapering timeline, but even QEternity appears to have an expiration date. Despite present complacency, this transition is likely to be painful for the market, as one does not normalize valuations that are 100% above historical norms without pain – typically concentrated in a handful of steep but short-lived free-falls. That said, there was no evidence years ago that boosting the market to speculative highs would do much good for the economy (consumers spend from their view of “permanent income,” not from temporary fluctuations in volatile assets), and there is no evidence that a retreat from speculative highs will do much harm to the real economy – aside from a normal, shallow, cyclical and transitory softening –provided that the Fed is diligent about systemic risks on the regulatory side, particularly where leveraged loans and leveraged equity are concerned.

Past performance does not ensure future results, and there is no assurance that the Hussman Funds will achieve their investment objectives. An investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted above. More current performance data through the most recent month-end is available at www.hussmanfunds.com. Investors should consider the investment objectives, risks, and charges and expenses of the Funds carefully before investing. For this and other information, please obtain a Prospectus and read it carefully.

(c) Hussman Funds