An Open Letter to the FOMC: Recognizing the Valuation Bubble in Equities

John P. Hussman, Ph.D.

All rights reserved and actively enforced.

To the members of the FOMC,

You’ve emphasized the tremendous burden placed on the Fed in recent years, and your dedication to collectively doing right by the country. It’s important to start with that recognition, because as concerned as I’ve been about the impact and economic assumptions behind the Fed’s actions, I don’t question your motives or integrity. What follows is simply information that may be helpful in realistically assessing the outcomes and risks of the present policy course, and perhaps to help prevent a bad situation from becoming worse.

Some brief background

As the head of an investment company, it’s natural to conclude that what follows is simply “talking my book,” but for what it’s worth, the majority of my income is directed to theHussman Foundation. Academically, I earned my doctorate in economics from Stanford, studying with Tom Sargent, John Taylor, Ron McKinnon, Robert Hall, and Joe Stiglitz, and spent several years as a professor at the University of Michigan and Michigan Business School before focusing on finance.

We’ve done well in prior complete market cycles (combining both bull and bear markets), and were among the few who warned of the market collapses and recessions of 2000-2002 and 2007-2009. In contrast, the half-cycle of the past 5 years has been challenging because of the awkward transition it provoked, following a credit crisis that we fully anticipated. Economic policy failures, departures from Section 13(3) of the Federal Reserve Act (which Congress subsequently spelled out like a children’s book), avoidance of needed debt-restructuring (except in the auto industry), and extortionate cries of “global meltdown” from the financial industry all contributed to a collapse in economic confidence beyond anything witnessed in post-war data. That forced us to stress-test every aspect of our approach against Depression-era outcomes. We missed returns from the market’s low in the interim of that stress-testing, and have foregone the more recent speculative advance because identical features have resulted in spectacular market losses throughout history.

In hindsight, the crisis ended - precisely - onMarch 16, 2009, when the Financial Accounting Standards Board abandoned FAS 157 “mark-to-market” accounting, in response to Congressional pressure from the House Committee on Financial Services onMarch 12, 2009. That change immediately removed the threat of widespread insolvency by making insolvency opaque. My impression is that much of the market’s confidence and oversensitivity to quantitative easing stems from misattribution of the initial recovery to QE. This has created a nearly self-fulfilling superstition that links the level of stock prices directly to the size of the Fed's balance sheet, despite the absence of any reliable or historically demonstrable transmission mechanism that relates the two with any precision at all.

The FOMC certainly had a part in creating a low-interest rate environment that provoked a reach-for-yield and a gush of demand for securities backed by mortgage lending of increasingly poor credit quality (I’ll note in passing that new issuance of “covenant lite” debt has now eclipsed the pre-crisis peak largely due to the same yield-seeking). Still, it may ease the burden of power to consider the likelihood that the actions of the Federal Reserve – though clearly supportive of the mortgage market – were not responsible for the recovery. One can thank the FASB for that, provided we’re all comfortable with the reduced transparency that results from mark-to-model and mark-to-unicorn accounting.

Recognizing the equity bubble

How does one establish the value of a long-lived asset? Hopefully, that question stirs the economist in all of you, and you immediately respond that every security is a claim on some long-term stream of cash payments (including any terminal value) that the holder can expect to receive over time. If price is known, the discount rate that equates price to the present value of expected future payments can be interpreted to be the expected long-term return of that security. This is how one calculates the yield-to-maturity on a long-term bond, for example. Conversely, we can make assumptions about the long-term return that investors will require over time and then calculate an implied price. Discounting the expected long-term stream of cash flows using some required long-term return results in a “fair value” that quietly incorporates those underlying assumptions.

Of course, nobody likes to discount an entire stream of expected payments, so investors create shortcuts. The most common shortcut is to compress all of the relevant cash flows and discount rates into a “sufficient statistic.” So for example, if we have a perpetuity with price $P that throws off cash flow $C every year forever, the ratio C/P is a sufficient statistic for the expected long-term rate of return, and everything knowable about valuation can be neatly summarized by that ratio. Nice economic assumptions about constant growth rates, returns on invested capital, payout ratios, and other factors encourage similar approaches in the equity market. So we look at price/earnings ratios based on a single year of earnings and immediately believe we know something about long-term value.

But valuation shortcuts are only useful if the “fundamental” being used isrepresentative of the entire long-term stream of cash flows that will be delivered into the hands of investors. And it’s precisely here where the FOMC may find a careful review of the evidence to be useful.

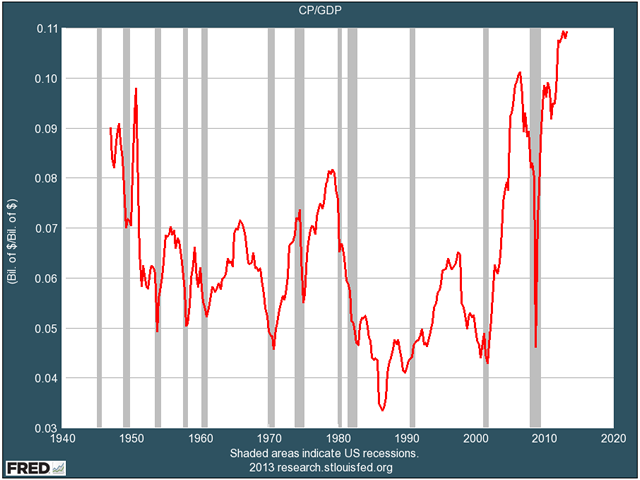

The chart below is from one of the best tools that the Fed offers the public, the Federal Reserve Economic Database (FRED). The chart shows the ratio of corporate profits to GDP, which is presently at a record. The fact that profits as a share of GDP are more than 70% above their historical norm should immediately raise a question as to whether current year earnings or next year’s projected “forward earnings” should be used as a sufficient statistic for long-term cash flows and equity market valuation without any further reflection. Then again, more work is required to demonstrate that such an approach would be misleading. We’re just getting warmed up.

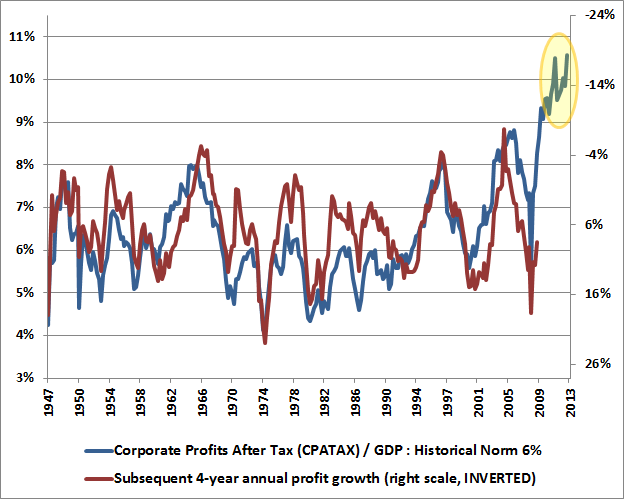

A simple way to see the implications of the present elevation of the profit share is to relate the level of profit margins to subsequent growth in profits over a reasonably “cyclical” horizon of several years. Remember, when one values equities, one is valuing a long-term stream, not just next year’s earnings. Investors taking current-year or forward-year profits as a sufficient statistic should be aware that high margins are reliably associated with weak profit growth over subsequent years.

The next relevant question is to ask why profit margins are presently so high. One might argue that the profitability of companies has achieved a permanently high plateau. Despite historical mean-reversion in profit margins (which tend to collapse over the full course of the business cycle), maybe this time is different. As it happens, we can relate the surfeit of corporate profits in recent years rather precisely to the extraordinary combined deficits of the household and government sectors during the same period.

|

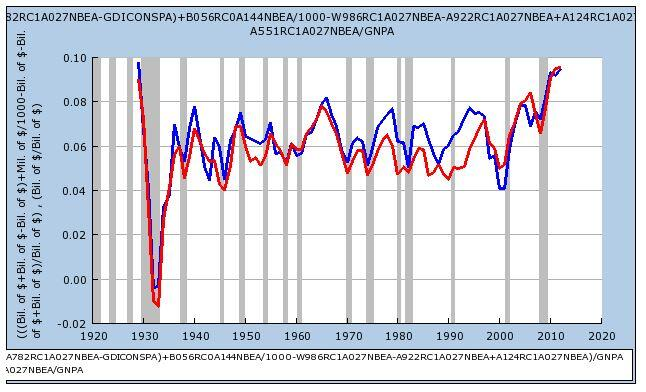

Box: The deficits of one sector emerge as the surplus of another To see what’s going on, we can exploit the savings-investment identity Investment = Savings Investment = Household Savings + Government Savings + Corporate Savings + Foreign Savings (the inverse of the current account) Corporate Profits = (Investment – Foreign Savings) – Household Savings – Government Savings + Dividends This basic decomposition, at least to an approximation allowed by national income accounting and modest statistical discrepancies, is shown below (h/t Jesse Livermore, Michal Kalecki).

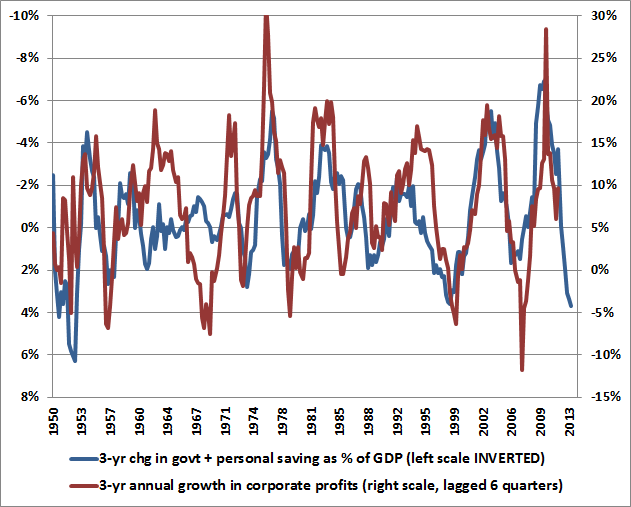

We can go further. The reason (Investment – Foreign Savings) are in parentheses above is because particularly in U.S. data, they have an inverse relationship, as “improvements” in the current account are generally associated with a deterioration in gross domestic investment. So the term in parentheses adds very little variability over the course of the business cycle. Likewise, dividends are fairly smooth, and add very little variability over the course of the business cycle. As a result, the above identity reduces – from the standpoint of overall variability – to a statement that corporate profits as a share of GDP are nearly the mirror image of deficits in the household and government sectors. A simple way to think about this is that dissaving in both sectors helps to support corporate revenues and limit the need for competition, even when wages and salaries are depressed. It follows that most of the variability in corporate profits over time is driven by mirror image variations in the household and government sectors. As it happens, this relationship turns out to be strongest with a lag of roughly 4-6 quarters. Given the general improvement in combined government and household savings that began just over a year ago, it follows that current-year or even higher year-ahead earnings estimates may not be particularly useful “sufficient statistics” for the purpose of valuing equities.

A predictable response among investors is to immediately seek alternate explanations that might allow profit margins to remain permanently elevated. First among these is the argument that somehow the production of U.S. companies abroad is not being taken into account. But the difference between Gross National Product (which does exactly that) and Gross Domestic Product – even if it represented pure profit – is only about 1%. The adjustment might make a difference in Ireland, where the gap between GNP and GDP is far larger, but the effect is purely second-order in the United States. Moreover, any additional dynamic that prompts the claim “this time is different” had better be one that emerged in the past few years, because as the charts above demonstrate, the mirror-image relationship between variations in corporate profits and variations in combined government and household savings has hardly missed a beat in the past century. |

Valuation measures and prospective equity returns

Even if we overlook the foregoing arguments, a historical comparison of competing valuation methods speaks loudly enough. The most important test of any valuation measure is how closely that measure is related to actualsubsequent returns over a period of several years. While valuation measures often have little to do with near-term returns, valuation measures that are also unrelated to subsequent long-term returns are not only useless, but dangerous.

The fact is that valuation measures driven by single-period earnings (whether trailing earnings or forward operating earnings) are poorly correlated with subsequent market returns, mainly because they impose the counterfactual assumption that profit margins can be held constant over time. In contrast, measures that account for the cyclicality of profit margins typically have far greater explanatory power than their raw counterparts.

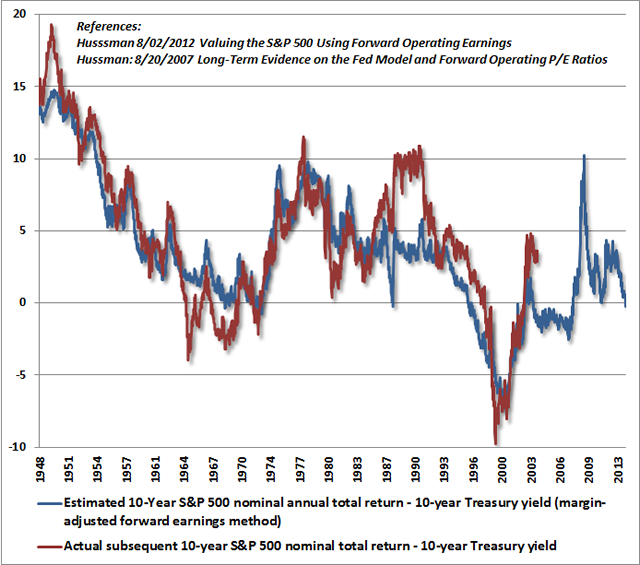

A few examples will demonstrate these regularities. The first chart presents estimated and actual subsequent 10-year S&P 500 total returns (in excess of the 10-year Treasury bond yield) based on the S&P 500 forward operating earnings, but adjusting for the predictable cyclicality of profit margins (seeValuing the S&P 500 Using Forward Operating Earnings). Presently, this estimate implies that the S&P 500 is likely to underperform even the depressed yield on 10-year Treasury bonds over the coming decade. The same was true at the 1972 peak (before stocks lost half their value), the 1987 peak, not to mention the more severe valuation peaks of 2000 and 2007. Present valuations notably contrast with the quite favorable estimated premium that briefly emerged in 2009.

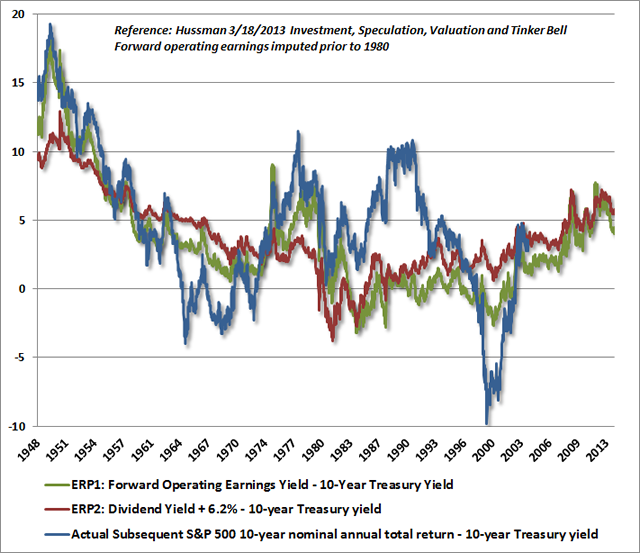

The raw counterparts to the above graph are what Janet Yellen appeared to reference in her testimony to the Senate two weeks ago. Below are two alternate versions of the “equity risk premium.” The first shows the raw “forward operating earnings yield” of the S&P 500 less the 10-year Treasury yield. The second shows the dividend yield on the S&P 500 plus 6.2% (reflecting long-run nominal economic growth) less the 10-year Treasury yield. Neither measure has a very good empirical record of explaining subsequent S&P 500 total returns in excess of Treasury yields.

As a side-note, the presumed one-to-one relationship between forward equity yields and bond yields is actually an artifact of the 16-year period from 1982 to 1998 when bond yields enjoyed a disinflationary decline while stocks gradually moved from a secular valuation low to the dangerous elevations of the late-1990’s. Though Fed officials including Alan Greenspan and Janet Yellen seem attracted to the seemingly elegant simplicity of these “equity risk premium” models, they seem somehow oblivious to the fact that they don’t actually work.

Why is the historical record of these simple “equity risk premium” estimates such a cacophony of noise? The answer should be immediately apparent. It turns out that theerror between these estimates and actual subsequent 10-year S&P 500 total returns (in excess of 10-year Treasury yields) has a correlation of 0.86 with – you guessed it –profit margins.With profit margins at the highest level in history, the record suggests that these models are grossly overestimating prospective equity returns at today's all-time stock market highs. Unfortunately, this evidence also suggests that the faith expressed in these “equity risk premium” estimates by Janet Yellen and others is likely to coincide with their most epic failure in history.

My strong disagreement should not be confused with disrespect, and none is intended, but wasn't it Janet Yellen who in October 2005, at the height of the housing bubble, delivered aspeecheffectively proposing that monetary policy could mitigate any negative economic consequences of a housing collapse, and arguing that the Fed had no role in preventing further housing distortions? Given the lack of concern with the present elevation of the equity markets, these remarks from 2005 have a rather ominous ring in hindsight:

“First, if the bubble were to deflate on its own, would the effect on the economy be exceedingly large? Second, is it unlikely that the Fed could mitigate the consequences? Third, is monetary policy the best tool to use to deflate a house-price bubble? My answers to these questions in the shortest possible form are, ‘no,’ ‘no,’ and ‘no.’”

The reason that the Fed does not see an “obvious” stock market bubble (to use a word regularly used by Governor Bullard, as if to imply that misvaluations cannot exist unless they smack their observers with a two-by-four) is because while price/earnings multiples appear only moderately elevated, those multiples themselves reflect earnings that embed record profit margins that stand about 70% above their historical norms.

We can demonstrate in a century of evidence that a) profit margins are mean-reverting and inversely related to subsequent earnings growth, b) margin fluctuations are largely driven by cyclical variations in the combined savings of households and government, and importantly, c) valuation measures that normalize or otherwise dampen cyclical variation in profit margins aredramatically better correlated with actual subsequent outcomes in the equity markets.

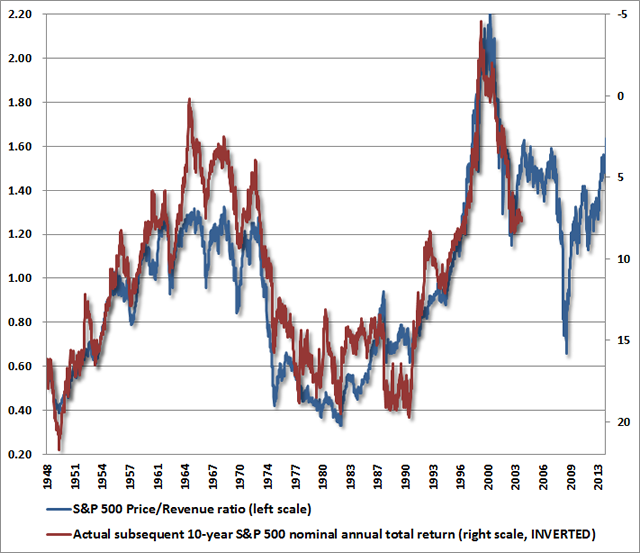

A few additional charts will drive this point home. The chart below shows the S&P 500 price/revenue ratio (left scale) versus the actual subsequent 10-year nominal total return of the S&P 500 over the following decade (right scale, inverted). Market valuations on this measure are well above any point prior to the late-1990’s market bubble. Indeed, if one examines the stocks in the S&P 500 individually, the median price/revenue multiple is actually higher today than it was in 2000 (smaller stocks were more reasonably valued in 2000, compared with the present). This is a dangerous situation. In this context, the dismissive view of FOMC officials regarding equity overvaluation appears misplaced, and seems likely to be followed by disruptive financial adjustments.

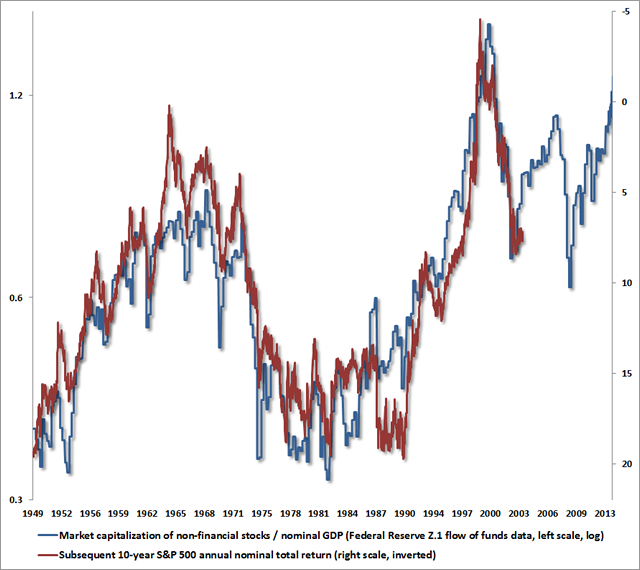

One obtains a similar view, with equal historical reliability, from the ratio of nonfinancial equity capitalization to nominal GDP, using Federal Reserve Z.1 Flow of Funds data. On this measure, equities are already beyond their 2007 peak valuations, and are approaching the 2000 extreme. The associated 10-year expected nominal total return for the S&P 500 is negative.

The unfortunate situation is that while the required financial adjustment may or may not be as brutal for investors as in 2007-2009, or 2000-2002, or 1972-1974, when the stock market lost half of its value from similar or lesser extremes, the consequences of extremely rich valuation cannot be undone by wise monetary policy. The Fed has done enough, and perhaps dangerously more than enough. The prospect of dismal investment returns in equities is an outcome that is largely baked-in-the-cake. The only question is how much worse the outcomes will be as a result of Fed policy that has few economic mechanisms other than to encourage speculative behavior.

Textbook speculative features

A discussion of bubble risk would be incomplete without defining the term itself. From an economist’s point of view, a bubble is defined in terms of differential equations and a violation of “transversality.” In simpler language, a bubble is a speculative advance where prices rise on the expectation of future advances and become largely detached from properly discounted fundamentals. A bubble reflects a widening gap between the increasingly extrapolative expectations of market participants and the prospective returns that can be estimated through present-value relationships linking prices and likely cash flows.

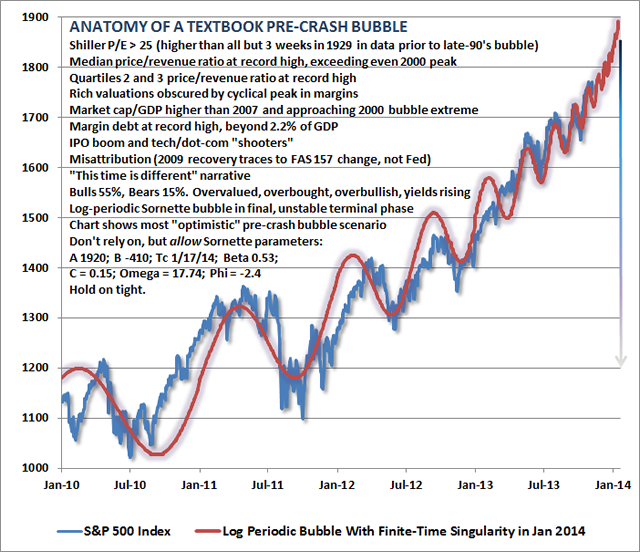

As economist Didier Sornette observed inWhy Markets Crash, numerous bubbles in securities and other asset markets can be shown to follow a “log periodic” pattern where the general advance becomes increasingly steep, while corrections become both increasingly frequent and gradually shallower. I’ve described this dynamic in terms of investor behavior that reflectsincreasingly immediate impulses to buy the dip.

Along with this pattern, which has emerged with striking fidelity since 2010, we observe a variety of other features typically associated with dangerous extremes: unusually rich valuations on a wide variety of metrics that actually have a reliable correlation with subsequent market returns; margin debt at the highest level in history and beyond 2.2% of GDP (a level that was matched only briefly at the 2000 and 2007 market extremes); a blistering pace of initial public offerings - back to volumes last seen at the 2000 peak and featuring “shooters” that double on the first day of issue; confidence in the narrative that “this time is different” (in this case, the presumption of a fail-safe speculative backstop or “put option” from the Federal Reserve); lopsided bullish sentiment as the number of bearish advisors has plunged to just 15% and bulls have crowded one side of the boat; record issuance of covenant-lite debt in the leveraged loan market (which is now spreading to Europe); and a well-defined syndrome of “overvalued, overbought, overbullish, rising-yield” conditions that has appeared exclusively at speculative market peaks – including (exhaustively) 1929, 1972, 1987, 2000, 2007, 2011 (before a market loss of nearly 20% that was truncated by investor faith in a new round of monetary easing), and at three points in 2013: February, May, and today (seeA Textbook Pre-Crash Bubble). Many of us in the financial world know these to be classic features of speculative peaks, but there is career risk in responding to them, so even those who view the situation with revulsion can't seem to tear themselves away.

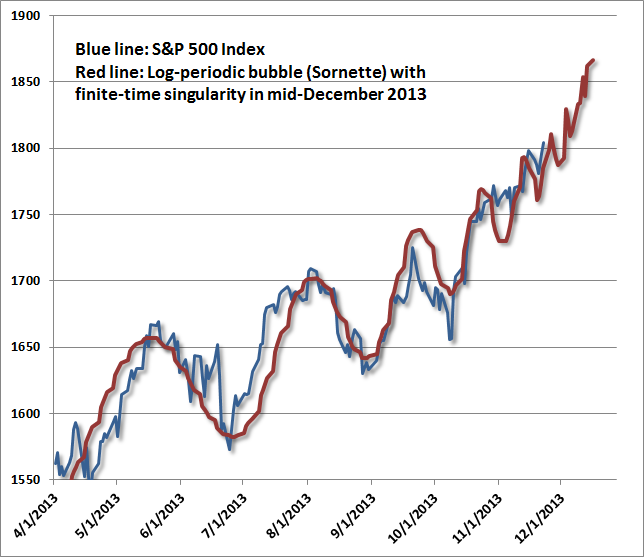

While I have no belief that markets follow any mathematical trajectory, the log-periodic pattern is interesting because it coincides with a kind of “signature” of increasing speculative urgency, seen in other market bubbles across history. The chart above spans the period from 2010 to the present. What’s equally unsettling is that this speculative behavior is beginning to appear “fractal” – that is, self-similar at diminishing time-scales. The chart below spans from April 2013 to the present. On this shorter time-scale, Sornette’s “finite time singularity” pulls a bit closer – to December 2013 rather than January 2014, but the fidelity to this pattern is almost creepy. The point of this exercise is emphatically not to lay out an explicit time path for prices, but rather to demonstrate the pattern of increasingly urgent speculation – the willingness to aggressively buy every dip in prices – that the Federal Reserve has provoked.

The way forward

In my view, good public policy acts to both impose and relieve constraints – focusing on relieving obstructive constraints when they actually become binding; imposing constraints where their absence creates excessive risk or the potential for undue harm to others; and avoiding policies where the risk of unintended consequences overwhelms the expected benefit from any demonstrated cause-effect relationship.

From this perspective, the policy of quantitative easing has run its course. It undermines planning, as every economic decision must be made in the context of what the Federal Reserve may or may not do next. It starves risk-averse savers, the elderly, and the disabled from interest income. It lowers the bar for speculative, unproductive, low-covenant lending (as it did during the housing bubble). It relaxes a constraint that is not binding – as there are already trillions of dollars in idle reserves at U.S. banks, on which the Federal Reserve pays interest both to keep them idle and to avoid disruptions in short-term money markets. It undermines price signals and misallocates scarce savings to speculative pursuits. It further skews the distribution of wealth, and while the extent of this skew has a scarce chance of persisting, the benefits of any spending from transiently elevated stock market wealth will accrue to primarily to higher-income individuals who are not as constrained as the millions of lower-income, low-asset families hoping for some “trickle-down” effect. We have seen numerous variants of this movie before, and we should have learned the ending by now.

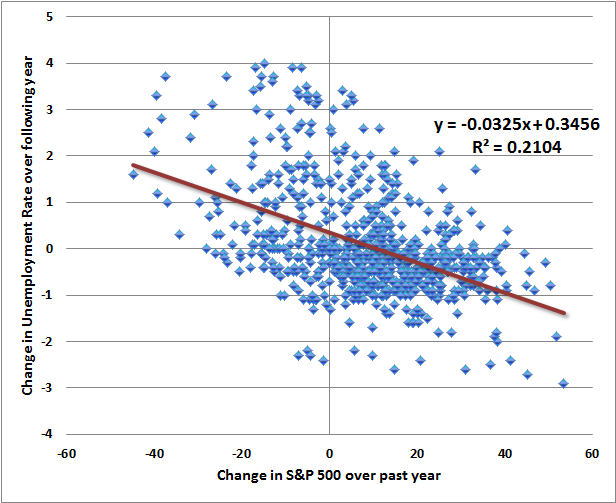

Importantly, the magnitude of the “wealth effect” on employment is dismally small. Even if the entire relationship between stock market fluctuations and employment fluctuations was causal and one-directional, it would still take a roughly 40% advance in the stock market to draw the unemployment rate down by 1%. Unfortunately, price advances do not create the underlying cash flows to support them, so the strategy of manipulating stock prices higher also involves a piper that must be paid.

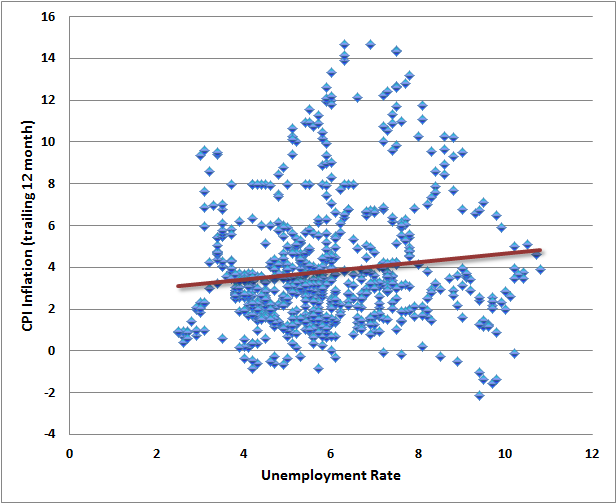

As for inflation-unemployment “tradeoffs,” we should all be clear about what the data look like in practice, particularly how weak and unreliable the relationships are between the two. There are numerous ways to plot the data. For example, lagging unemployment strengthens the positive relationship between inflation and unemployment, while lagging inflation flattens the nearly non-existent relationship from unemployment to inflation. One can augment this with expectations, or vary assumptions about NAIRU all one likes. The scatter is simply not amenable to a practical degree of “optimal control.”

This isn’t to say that A.W. Phillips was incorrect. Rather, his “Phillips Curve” was actually a relationship between the unemployment rate and wage inflation, in a century of British data when Britain was on the gold standard and general prices were stable. What Phillips said, in effect, is that unemployment is inversely related to real wage inflation. That proposition holds true in U.S. data as it does internationally. But it is hardly the basis for any strong belief that we can buy a few more jobs by targeting a higher inflation rate in the general price level.

It’s notable that the “dual mandate” of the Fed repeatedly includes the phrase “long run.” The Federal Reserve has not been asked to be “data-dependent” in response to every monthly fluctuation in output, employment and financial markets. Instead, the Fed is asked to consider the long-run effects of its actions. Minimizing the consideration of longer-term risks in the pursuit of outcomes that are largely beyond the reliable effects of the Federal Reserve’s tools cannot be justified by referencing the Federal Reserve’s mandate.

The intent of this letter is not to criticize, but hopefully to increase the mindfulness of the FOMC as to historical evidence, the strength of various financial and economic relationships, and the potentially grave consequences of further relaxing constraints that are not binding in the first place.

To some extent, certain consequences are baked-in-the-cake, as are various adjustments that the Federal Reserve will have to make in order to normalize its policy stance in the years ahead. Gradually rolling assets off the balance sheet as they mature is certainly an option, though the time profile of maturities is not smooth, the strategy may not be robust to material economic acceleration even several years from now, and such a strategy will continue to punish risk-averse savers for years. You already know my views on what a time-consistent path for normalizing the balance sheet would look like.

The immediate objective, I think, is to continue to emphasize that a gradual reduction in the pace of Fed purchases is distinct from a “tightening” – our own estimates are that a contraction of more than $1 trillion in the Fed’s balance sheet would be required simply to bring Treasury yields to 0.25% without raising the interest rate the Fed pays on excess reserves. Having missed the opportunity for a broadly anticipated “taper” in September, and having provoked even greater speculation as a result, the potential disruption of even a small move in this direction is a legitimate concern. At whatever time this occurs, my own view is that even $10 billion may be too large for a speculative market to swallow, while $5 billion is so small that it could make the Fed appear timid. One might suggest $8.5% billion, or 10%, which is so small a taper that the markets would hopefully view an overreaction as ridiculous – which is not to say that the markets would not overreact even then. From the standpoint of a financial market participant, I can’t emphasize enough how broadly the Fed is viewed as the only game in town.

There is certainly more progress that needs to be made on employment and economic activity. The legitimate question is whether continued relaxation of non-binding constraints is likely to produce this outcome without the increasing risk of severe and unintended consequences. This is a question that begs not for verbal arguments, but empirical evidence, realistic estimates of effect sizes, and clear transmission mechanisms. The Federal Reserve has a critical role in easing constraints - particularly shortages of liquidity in the banking system - when they become binding, and in applying constraints and oversight - or at least refraining from further harm - when risks become untethered. The second aspect of that role is far more imperative today than might be obvious.

I hope that some part of this is useful.

Sincerely,

John P. Hussman, Ph.D.

Hussman Strategic Advisors

© Hussman Funds