The present combination of overvalued, overbought, overbullish conditions, coupled with rising interest rates and broad dispersion among market internals, is one that most closely resembles only three other points in the post-war period; the first in early-October 1987 (though at less extreme valuations), the second in January 2000, and the most recent in July 2015 (the S&P 500 lost -12% over the next 6 weeks). Relaxing the set to include the nearly 10% of post-war periods that share the more general market return/risk classification we presently identify, the overall expected return distribution is associated with severely negative market outcomes, on average, capturing a cumulative loss in the S&P 500 exceeding -90%. We currently view a hard-defensive stock market outlook as appropriate.

Even in bonds and precious metals, present market conditions are consistent with only modest return expectations. While a near-term rebound in these markets would be consistent with short-term oversold conditions, our main inclination in response to the recent spike in yields is not so much to embrace Treasury debt but to avoid corporate debt, where credit spreads are compressed to the point where rapid adjustments (and steep price losses) appear likely. I have very weak expectations about direction of long-term interest rates here, but much stronger views about the likelihood of widening credit spreads.

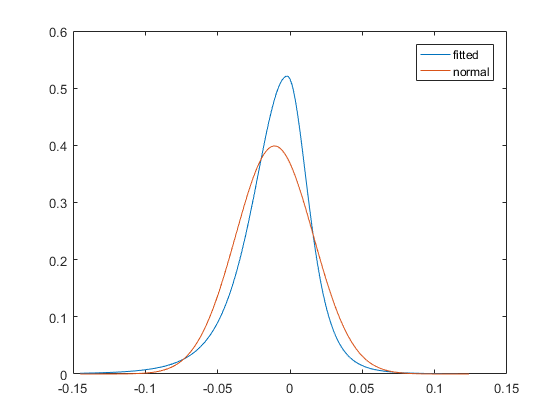

Notably, the implied bell curve of expected stock market returns features what I’ve often called “unpleasant skew.” The chart below shows the fitted probability distribution of weekly market returns under the market return/risk classification we presently identify (blue), compared to a symmetrical distribution centered at the same mean return (red). Notice that in any given week, the single most likely market outcome is actually a small gain, even though the average outcome is negative (near -40% at an annual rate). Notice also that the right tail of the blue curve is narrow, implying a much smaller-than-average probability of a significant market gain, while the left tail is fat, implying a larger-than-average probability of a vertical market loss.

Simply put, don’t be lulled into complacency by thinking that severely hostile market conditions have to resolve into immediate market losses. That’s not the way these environments work, and they never have. Rather, the “unpleasant skew” of present conditions actually means that investors should expect a greater tendency toward small market gains than market conditions might otherwise lead them to expect, punctuated - with no warning at all - by wicked vertical losses that wipe out weeks or months of market gains in handful of sessions. Every market crash in history has been associated with essentially the same skewed distribution. It’s the positive “mode” that creates complacency, it’s the negative average return that drives cumulative losses, and it’s the fat left tail that strikes out of nowhere.

Meanwhile, it’s best not to focus one’s investment horizon on days or weeks, but rather, on the complete market cycle and the longer horizon in the range of 10-12 years. While we’ve adopted a defensive market outlook here, and we expect a 40-55% market loss over the completion of the current market cycle, with 10-12 year S&P 500 total returns barely above zero, we’re also open to the potential for shorter-term shifts in investor risk-seeking that could modify our near-term outlook. I expect that a strong safety-net will be required until we observe a material retreat in valuations, but we’re open to changes in the evidence from week-to-week and will align ourselves accordingly.