“It’s quite possible that even a small taper will be too much for investors, but the alternative to tapering is to make an already precarious situation more precarious, while damaging the Fed’s credibility in the process.”

Hussman Weekly Market Comment,Baby Steps, September 16, 2013

Last week, the Federal Open Market Committee (FOMC) decided to go the alternative route. The Fed’s decision does not seem intended to be a “reset” of perpetual quantitative easing. Instead, it appears to reflect the committee’s belief that QE has real economic effects, but that these economic benefits have not gained sufficient momentum. Notably, one member of the FOMC who voted in favorobservedon Friday that the decision not to reduce the pace of quantitative easing was a “borderline decision.” Another voicedconcernsthat the Fed now faces “challenges that come with issues of credibility” and that the inaction “discounts the potential costs of the policy tool with which we have limited experience.”

In my view, the problem with quantitative easing is that its entire effect relies on provoking risk-taking by those who would otherwise choose not to do so; that the FOMC has extended and amplified financial market distortions without regard to the rich valuations and dismal prospective returns that financial assets are most likely priced to achieve; and that this distortion of financial asset prices has precious little to do with the presumptive goal of Fed policy, which is greater job creation and economic activity.

Unfortunately, even though the equity market has been rising on what we view as nothing but noxious psychological ether, the FOMC has – perhaps unintentionally – released another tank of the stuff. Quantitative easing only “works” however, to the extent that investors have no immediate desire to hold short-term, risk-free assets. In any environment where investors become eager to hold currency and other low-risk, default-free assets despite their low yield, I expect that both investors and the Fed will discover that quantitative easing is wholly ineffective in supporting the prices of risky assets. This is an experiment that has not yet run its course, and we have no intention of being the guinea pigs in that study.

The challenge at present is that last week’s Fed’s decision does make an already precarious situation more precarious. So the question is how to respond. From the experience of the past few years, the risk is that enthusiasm that the Fed is “all-in” could prompt a surge of further speculation, and even greater financial distortions. At the same time, examining market cycles over a century of market history, present conditions cluster among the most negative 2-3% of data points in terms of average return and downside risk.

It’s sometimes assumed that the views I express in these weekly comments are simply based on my personal inclinations toward the financial markets, but I exert far less discretion than one might imagine. The notable exception was the period between 2009 and early 2010, when I insisted on making our approach robust to Depression-era data as a fiduciary matter: though our existing estimation methods had proved successful, they were also based solely on post-war data, and events at the time were inconsistent with outcomes observed during that period. With that exception, our investment approach is generally driven by a full-cycle discipline of aligning our outlook with the expected market return/risk profile that we estimate at each point in time, based on well-defined methods and historical evidence (seeAligning Market Exposure with the Expected Return/Risk Profile). We pursue this approach because we are convinced of its long-term effectiveness, and have a century of evidence to support that view, despite challenges that we’ve experienced in the unfinished half of the present extraordinary cycle. Some investors might trade by intuition, or faith in the Fed that goes beyond anything that can be quantified historically. I have no idea how one could possibly test that approach over time.

Given the objective and unusually negative market return/risk estimates we observe at present, it follows that I continue to believe that present conditions warrant a generally defensive outlook. Still, the Fed’s decision last week creates the possibility of a dangerous contingency over the next 6-8 weeks that a tapering decision might have avoided: the possibility of a short-lived but spectacular speculative blowoff (which would in turn add to the conditions for a fairly steep market collapse). My impression is that a slight amount of insurance against a speculative blowoff could be helpful in easing concerns on that front. Inexpensive, out-of-the-money call options can be useful instruments for that purpose.

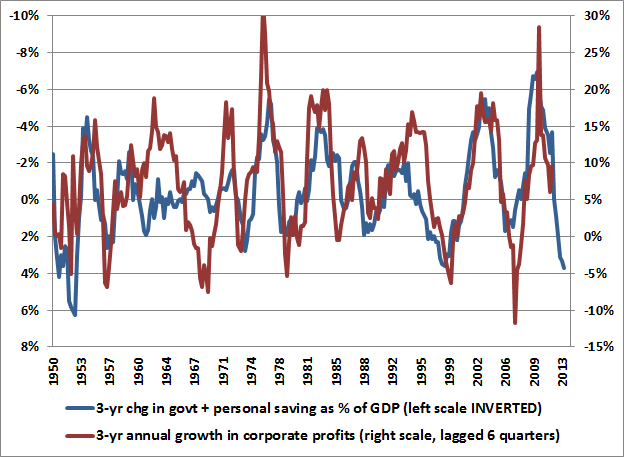

From the standpoint of long term stock market returns, the most important feature of valuations to note at present is the extreme level of profit margins, which are more than 70% higher than historical norms. This is well-explained by the fact that the deficits of one sector must, in equilibrium, emerge as the surplus of another sector. As has been consistently evident U.S. economic data across history, large deficits in the combined government and household sectors are invariably reflected in mirror-image surpluses in corporate profits, as a share of GDP. This is not only true in terms of levels but in terms of changes. That is, the change in combined government and household savings over periods of say, 3-4 years is also closely mirrored by changes in corporate profits in the opposite direction. This isn’t even a theory – it’s largely driven by accounting identities and economic equilibrium.

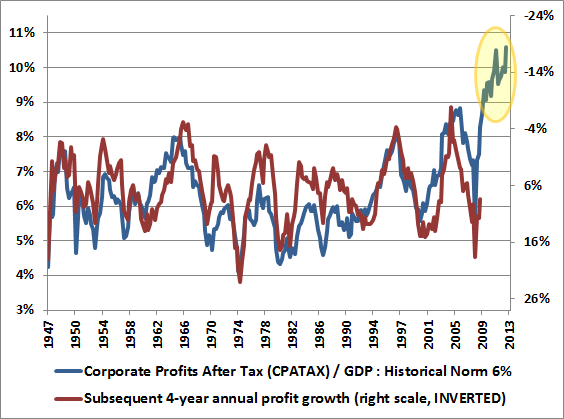

Again, the difficulty with valuing stocks on the basis of raw price/earnings ratios is that corporate profits as a share of GDP are presently over 70% above their long-term historical norm. Though the actual course of corporate profits will be affected by numerous factors, including the extent to which extraordinary fiscal deficits normalize, we would expect corporate profits over the coming 3-4 year period to contract at a rate of somewhere between 5-15% annually. The practice of valuing stocks on the basis of current earnings or Wall Street’s projections of “forward operating earnings” (which embed assumptions of even more extreme profit margins) has never in history been more reckless and misleading.

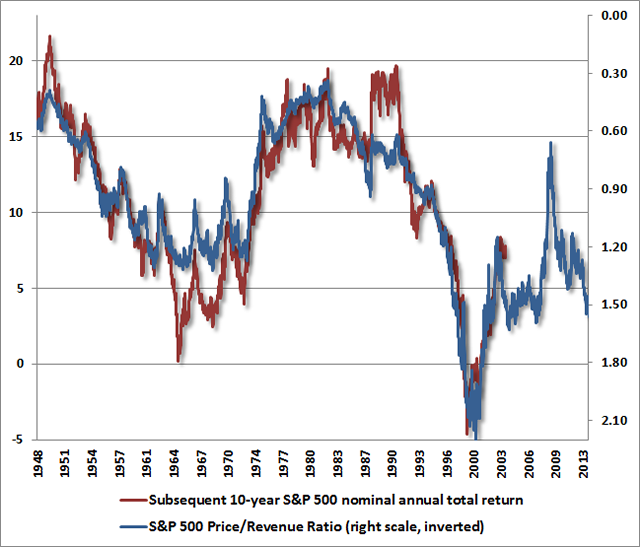

One hardly needs to accept any of these concerns to recognize that current equity valuations are consistent with the likelihood of dismal long-term returns. The historical record of reliable valuation measures should be sufficient. The chart below illustrates the relationship between the S&P 500 price/revenue ratio and subsequent 10-year nominal annual total returns for the S&P 500.

Last week, much was made of a remark by Warren Buffett that he was having difficulty finding any bargains in the current market. In our view, he did not go far enough, because even his more recent comments about valuation seem inconsistent with his own very accurate observations in the past. For example, Buffett noted in 1999 that “In my opinion, you have to be wildly optimistic to believe that corporate profits as a percent of GDP can, for any sustained period, hold much above 6%.” That assertion was clearly demonstrated by the clearly cyclical behavior of margins in the years that followed. It’s an assertion that deserves particular attention today.

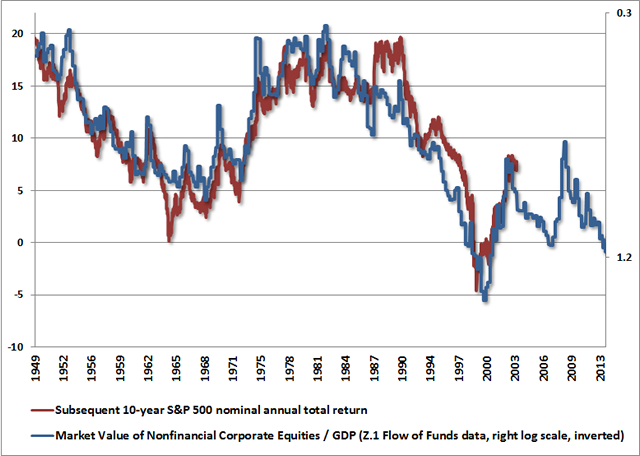

Likewise, Buffett observed in 2001 that the ratio of equity market value to national output is “probably the best single measure of where valuations stand at any given moment.” On that front, the chart below shows the value of nonfinancial corporate equities to GDP (imputed from March to the present based on changes in the S&P 500). On this measure, the likely prospective 10-year nominal total return of the S&P 500 lines up at somewhere less than zero. Suffice it to say that our estimates using both earnings and non-earnings based measures suggest a likely total return for the S&P 500 over the coming decade of less than 2.9% annually, essentially driven by dividend income, and implying an S&P 500 that is roughly unchanged a decade from now – though undoubtedly comprising a volatile set of market cycles on that course to nowhere.

On the possibility (not expectation) of a speculative blowoff

With our longer-term valuation concerns on the table, let’s move to the more immediate risks of the Fed’s decision last week – the potential to extend an already strenuously overvalued market by triggering a speculative blowoff. This would only make the subsequent completion of the present market cycle that much worse. I should note that this near-term possibility does not significantly affect our broader investment outlook, and nothing discussed below represents a material basis of our general market analysis.

Keep in mind that our discipline is based on aligning our investment outlook with the return/risk profiles that we estimate on the basis of a century of evidence. In contrast, my view about the potential for a short-lived speculative blowoff is more tentative; best viewed as a hypothetical possibility instead of a data-driven estimate. This isn’t a forecast – it’s simply a near-term possibility that we’re forced to consider because the Fed has suddenly created conditions that could support it.

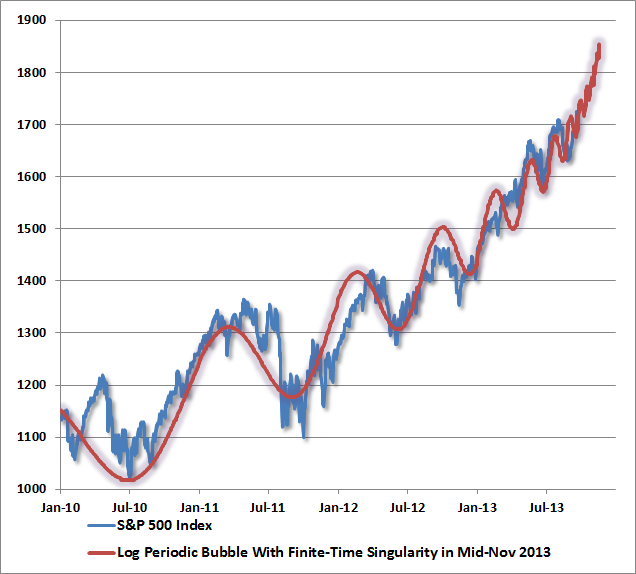

My impression is this. Based on numerous past speculative episodes in the financial markets, we know that financial bubbles have often proceeded in an oscillating pattern featuring increasingly frequent cycles of advance, punctuated by gradually shallower declines reflecting an accelerating eagerness to buy dips. This can produce what Didier Sornette has called “log-periodic” oscillations (seeIncreasingly Immediate Impulses to Buy the Dip). Given the negative return/risk estimates we observed in April and early-May, I believed that this series of oscillations was ending several months ago. In order to preserve a log-periodic pattern, further oscillations needed to exhibit an even faster alternation between steeply-sloped advances and shallow declines. Yet despite the strongly negative return/risk estimates we already had in April and May, this is unfortunately what has unfolded. With the Fed’s decision last week, we can’t rule out one particularly extreme version of a log-periodic bubble that is consistent with price fluctuations to date. That version is pictured below, and would comprise an advance above 1800 in the S&P 500 over a period of about 6 weeks. Again, this is emphatically not a forecast, but the conditions for a final wave of speculation may have been created by the Fed’s decision last week, and it leaves us unable to rule out this admittedly hypothetical possibility – particularly in the context of what has been a classic Sornette-type bubble to-date.

Whether or not this sort of outcome unfolds, the completion of the present market cycle appears likely to wipe out more than half of the market’s gains from the 2009 lows, as even run-of-the-mill bear market declines have regularly done in market cycles throughout history.

Past performance does not ensure future results, and there is no assurance that the Hussman Funds will achieve their investment objectives. An investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted above. More current performance data through the most recent month-end is available at www.hussmanfunds.com. Investors should consider the investment objectives, risks, and charges and expenses of the Funds carefully before investing. For this and other information, please obtain a Prospectus and read it carefully.

© Hussman Funds