The financial markets are at a transition that reflects tension between two realities. The first is that the Federal Reserve’s policy of quantitative easing has driven the stock market to valuations associated with the most extreme speculative peaks on record, coupled with a fresh boom in initial public offerings – with companies having zero or negative earnings accounting for three-quarters of new issuance – and record issuance of “covenant lite” leveraged loans (loans to already highly indebted borrowers, lacking normal protections that mitigate losses in the event of default). The other reality is that unconventional monetary policy has done little to push real economic activity or employment past the border that has historically distinguished expansions from recessions (about 1.8% year-over-year growth in both real final sales and non-farm payroll employment).

There is no question that quantitative easing has supported the mortgage market, and was almost wholly responsible for that role in late-2008 and 2009. But QE is not what ended the financial crisis (the March 2009 change in accounting rule FAS 157 is what removed the risk of widespread bank failures). Any economist familiar with the work of Nobel laureates like Milton Friedman or Franco Modigliani, or simply with decades of economic data, could have predicted even in 2010 that Bernanke’s efforts at creating a “wealth effect” would have weak effects on consumption, job creation and economic activity. In order to get any meaningful overall effect, it was clear that the Fed would have to create enormous but ultimately temporary distortions, inviting risk of longer-term financial instability. The Fed has now done exactly that.

The good news is that despite the long-term cost of diverting hundreds of billions to speculative pursuits instead of productive investment, a substantial retreat in the stock market and accompanying losses in illusory “wealth” is likely to compound this damage only weakly and temporarily – provided that the Fed is diligent in its oversight responsibilities and actively looks to minimize any systemic fallout from the portion of margin debt and leveraged loans that will inevitably go bad.

The best course for the Fed is to continue a gradual move toward a less discretionary, more rules-based policy. To the extent it feels the need to intervene, the FOMC should engage those policy tools where it actually has clear and measurable historical evidence of a cause-effect link between policy changes and intended outcomes. Unfortunately, it’s difficult to find such tools.

As Former Fed Chairman Paul Volcker observed last year, “I know that it is fashionable to talk about a ‘dual mandate’ – that policy should be directed toward the two objectives of price stability and full employment. Fashionable or not, I find that mandate both operationally confusing and ultimately illusory: operationally confusing in breeding incessant debate in the Fed and the markets about which way should policy lean month-to-month or quarter-to-quarter with minute inspection of every passing statistic; illusory in the sense it implies a trade-off between economic growth and price stability, a concept that I thought had long ago been refuted not just by Nobel prize winners but by experience.”

Though a substantial normalization in equity valuations and interest rates would certainly have short-run economic impacts, that sort of normalization would be the best way to ensure that scarce savings are allocated toward productive ends rather than repeated bouts of speculation. We don't believe that monetary policy should be used to deflate bubbles, but it should not be used to create or encourage them either, and that damage is already done. Moreover, the Fed also has a regulatory role in the financial markets, and in that role, it has a very real responsibility to provide oversight to reduce the likelihood and assess the potential consequences of reckless misallocation of capital, speculation, and practices that create systemic risk. This is a role that was clearly abdicated in the years prior to 2008, and is essential in the face of record margin debt and low grade leveraged loan issuance today.

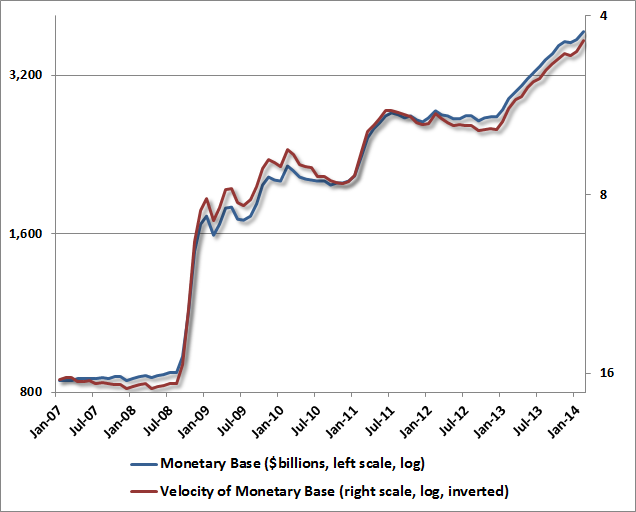

Meanwhile, like any policy that creates risk and distortions without reliable effects, more QE isn’t the answer to anything – not even if economic growth were to weaken, not even if inflation was to slow further, and not even if the equity markets were to decline substantially. Among the many problems with quantitative easing, an important feature is that monetary velocity falls in almost exact inverse proportion as the monetary base expands. In other words, regardless of the quantity, the new monetary base simply sits idle. Regardless of effects on financial speculation, there is almost precisely zero effect on economic activity – not on prices, not on real GDP, not on nominal GDP.

In order to increase monetary velocity without proportionally reducing the monetary base, we would have to observe exogenous upward pressure on interest rates. That’s likely to emerge in the back-half of this decade, though probably after an intervening economic slowdown. At that point, fairly early into the next expansion, the Fed is likely to stop hoping for higher inflation and discover it instead to be the last thing it wants. Until then, the Fed would provide the greatest benefit to long-run economic prosperity simply by ceasing its insistence on harming it by promoting speculation in efforts to offset short-run cyclical fluctuations.

The tortured narrative of these efforts should be obvious. As Fred Hickey of the High Tech Strategist observed last week, “After the tech bubble broke, the Fed jumped in to save the markets and economy with a period of extraordinarily low interest rates, which then led to the gross malinvestment in the housing sector (another bubble) and the misallocation of capital in the credit markets. The housing bubble imploded first, and the credit markets followed, leading to one of the worst financial crises in US history in 2008. Once again, the Fed stepped in to save the markets and the economy, this time with really free money (0% short-term interest rates for almost six years and counting) as well as trillions of dollars in outright money printing. Every time the Fed steps in… money gets misallocated and trouble follows.”

Some of the misallocations noted by Hickey include the Fed-enabled runup in the national debt to $17.57 trillion, the surge in global debt issuance to $100 trillion, up from $70 trillion at the mid-2007 peak, the suspension of any need to address unfunded entitlement liabilities, a doubling of the student loan burden, record highs in subprime auto lending, soaring corporate borrowing – partly to buy back stock at inflated valuations (notes Hickey, “as they always tend to do at market tops”) and partly to prop up sagging per-share earnings, a record $465.7 billion in margin debt, more initial public offerings in Q1 than at any point since the 2000 bubble peak, and a litany of other speculative outcomes.

Having witnessed the glorious advancing portion of the uncompleted market cycle since 2009, investors might, perhaps, want to consider how this cycle might end. After long diagonal advances to overvalued speculative peaks, the other side of the mountain is typically not a permanently high plateau. I captured a screenshot on Friday morning, in order to put a timestamp on what may prove – in hindsight – to be a point in history worth remembering.

That said, I should also reiterate that market peaks are not a moment but a process. The bars on the chart above are monthly. If you look carefully, it should be clear that the 2000 and 2007 peaks involved an extended period of volatility that included sharp selloffs, thrilling recoveries, marginal new highs, fresh breakdowns, and sideways movement. All of that day-to-day and week-to-week emotion and uncertainty is absent from a long-term chart where investors know, in hindsight, how utterly insignificant all of it was in the context of what followed.

In 2000 and 2007, we regularly encountered two arguments, which boil down to a) there’s no catalyst, and b) this time is different. In 2000, it was a New Economy. In 2007 and 2008, Ben Bernanke assured investors that the risks were “contained” and Janet Yellen confidently dismissed concerns about speculative risk with the words “No, No, and No.” History suggests a straightforward response: following speculative peaks, market losses are typically in full swing well before any catalyst is widely recognized, and b) the specifics of every cycle may be different, but broadly speaking, speculative episodes end the same way.

Adieu Quantitative Easing

Notably, these now inexorable risks are clearly evident to several members of the FOMC itself. In particular, Dallas Fed President and FOMC voting member Richard Fisher gave an informed, thoughtful speech in Hong Kong on Friday that is essential reading. While I have a very strong bias toward rules-based, historically informed economic policy having reliable cause-effect relationships, my sense is that if the Fed is going to be flexible, Fisher’s comments about forward guidance are probably the most straightforward guide to understanding the direction of Fed policy that investors are likely to get. A few excerpts:

“Adieu Quantitative Easing… Thus far, much of the money we have pushed out into the economy has been stored away rather than expended to the desired degree. For example, we have seen a huge buildup in the reserves of the depository institutions of the United States. Less than a fifth of commercial credit in the highly developed U.S. capital markets is extended through depository institutions. Yet depository institutions alone have accumulated a total of $2.57 trillion in excess reserves—money that is sitting on the sidelines rather than being loaned out into the economy. That’s up from a norm of around $2 billion before the crisis.

“Through financial engineering, we have helped bolster a roaring bull market for equities… Alongside these signs of rebound have been some developments that give rise to caution. I have spoken of these in recent speeches, echoing concerns I have raised in FOMC discussions: The [cyclically adjusted] price-to-earnings (PE) ratio of stocks is among the highest decile of reported values since 1881. .. the market capitalization of the U.S. stock market as a percentage of the country’s economic output has more than doubled to 145 percent—the highest reading since the record was set in March 2000… Margin debt has been setting historic highs for several months running and, according to data released by the New York Stock Exchange on Monday, now stands at $466 billion… Junk-bond yields have declined below 5.5 percent, nearing record lows… Covenant-lite lending is becoming more widespread. In my Federal Reserve District, 96 percent of which is the booming economy of Texas, bankers are reporting that money center banks are lending on terms that are increasingly imprudent. The former funds manager in me sees these as yellow lights. The central banker in me is reminded of the mandate to safeguard financial stability.

“At the current reduction in the run rate of accumulation, the exercise known as QE3 will terminate in October (when I project we will hold more than 40 percent of the MBS market and almost a fourth of outstanding Treasuries). We will then be back to managing monetary policy through the more traditional tool of the overnight lending rate that anchors the yield curve.

“Enter Forward Guidance: My own view is that commitments aren’t always credible, especially if they purport to extend far into the future. It’s hard to bind future policymakers, and it’s difficult to anticipate all the various economic circumstances that might arise down the road. As a general rule, then, the further into the future a commitment extends, the vaguer it tends to be. Along these lines, the FOMC periodically reiterates its commitment to do what it is legally mandated to do: pursue full employment, price stability and a stable financial system.

“We’ll see. That about sums it up. The FOMC is seeking to make sure that we have a sustained recovery without giving rise to inflation or market instability. We will conduct monetary policy accordingly. Regardless of the way we may finally agree at the FOMC to write it out or have Chair Yellen explain it at a press conference, we really cannot say more than that. As Deng Xiaoping would have phrased it: “We will cross the river by feeling the stones.”

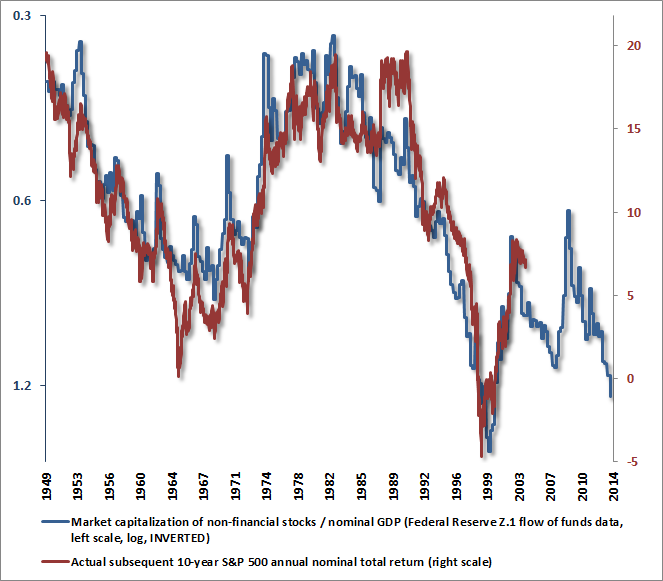

As a bonus, the chart below may help to demonstrate why Fisher is rightly concerned about the extreme ratio of market capitalization to GDP. This measure actually has a stronger correlation (about 90%) with subsequent 10-year returns in the S&P 500 than the Shiller P/E and a wide variety of other measures. Notice that the chart shows market capitalization / GDP on an inverted log scale. Actual subsequent S&P 500 annual total returns over the following decade are plotted on the right scale. Investors learned the hard way how the 2000 and 2007 extremes in this measure turned out. Though we don’t have a 10-year figure for actual returns since 2009, investors should also notice that the improved valuations evident in 2009 will indeed have been followed by a decade of 10% S&P 500 total returns even if the total returns for the market over the coming 5 years are somewhat negative (which we view as likely).

Presently, on the basis of market capitalization to GDP, investors can expect negative total returns (nominal and including dividends) on the S&P 500, not only for the next 5 years, but for the coming decade. Using a broader range of historically reliable valuation measures, we actually estimate a somewhat higher annual total return for the S&P 500 of about 2.3% annually, though still with negative returns on horizons shorter than about 7 years. In any event, history suggests that it is a rather large speculative leap to believe that present extremes will not be amply corrected over the completion of this market cycle.

Past performance does not ensure future results, and there is no assurance that the Hussman Funds will achieve their investment objectives. An investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted above. More current performance data through the most recent month-end is available at www.hussmanfunds.com. Investors should consider the investment objectives, risks, and charges and expenses of the Funds carefully before investing. For this and other information, please obtain a Prospectus and read it carefully.