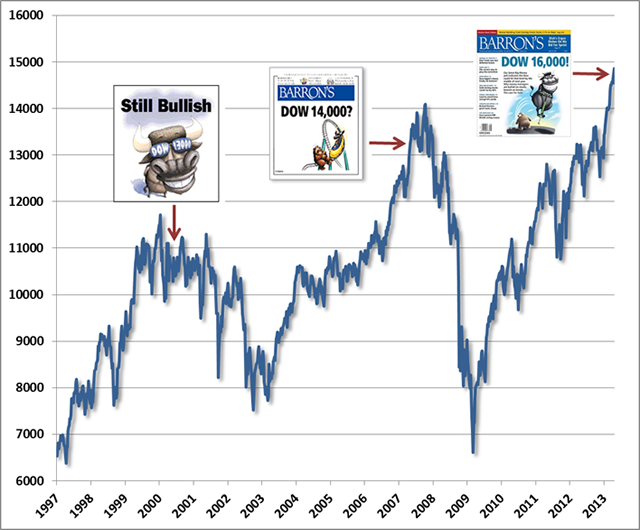

“The stock market isn't the only thing that has set records this spring. Barron's semiannual Big Money poll of professional investors also is setting a record -- for bullishness, that is. In our latest survey, 74% of money managers identify themselves as bullish or very bullish about the prospects for U.S. stocks -- an all-time high for Big Money, going back more than 20 years.”

“Dow 16000!” – Barron’s Magazine Big Money Poll 4/20/2013

A few reminders…

“Still Bullish! (Dow 13000)” – Barron’s Magazine Big Money Poll, May 1, 2000

The May 2000 Big Money Poll was published with the Dow Jones Industrial Average at 10733.91. The Dow had already peaked nearly a thousand points higher in January of 2000, and would go on to lose about 40% of its value in the 2000-2002 bear market, with the S&P 500 and Nasdaq faring far worse.

“Dow 14000?” – Barron’s Magazine Big Money Poll, May 2, 2007

The May 2007 Big Money Poll was published with the Dow at 13264.62. The Dow did advance another 6% to reach 14000 by October 2007. By November (the poll is semi-annual), bulls were outnumbering bears by 2-to-1, and the headline ran “The Party’s Not Over.” In fact, the market had already peaked, and proceeded to lose over half its value in the 2007-2009 bear market.

The Barron’s Big Money Poll is typically bullish, on balance. This is Wall Street, after all. But variations in the tone and extent of that bullishness can be informative, especially when the consensus is extremely optimistic at new highs of mature bull markets, and defensive at new lows of mature bear markets. I can’t really throw stones about 2009, as I had my own concerns at the time (relating to the need to stress-test against Depression era outcomes, despite our favorable views of valuation). But it’s worth noting that the 2009 Big Money Poll questioned the advance from the March lows, noting “good reason not to jump in with both feet yet.” The 2003 Big Money Poll – already well into a new bull market – was bullish on balance, and up from just 43% bulls in an October 2002 poll near the market lows. Still, the 2003 poll noted “the bulls’ views have been tempered by the market’s losses in recent years. Consequently their expectations for the Dow, the Standard & Poor’s 500 stock index, and the Nasdaq Composite have been ratcheted down from past surveys.”

This certainly isn’t a criticism of Barron’s itself. I grew up on Barron’s Magazine, and will remain a devoted reader at least as long as Alan Abelson provides a worthy counterbalance to the more short-sighted views of Wall Street and the Market Lab section remains in print. Still, the Big Money Poll is most useful as a contrary indicator.

Rule o’ Thumb: When the cover of a major financial magazine features a cartoon of a bull leaping through the air on a pogo stick, it’s probably about time to cash in the chips.

While the attention of investors is focused on the short-run market outlook in what is already a mature bull market advance, it’s crucial to understand the endgame to this overvalued, overbought, overbullish, overleveraged episode of market history. That endgame will be forced liquidation, as declining prices force leveraged investors to sell – voluntarily or otherwise. I noted back in January that margin debt had surged above 2% of GDP for the fourth time in history (the other three being 2000, 2007, and February 2011 - less severe, but still followed by an 18% market correction). In February, NYSE margin debt (the amount that investors have borrowed to purchase NYSE-traded stocks on margin) reached $366 billion, and there’s a fair chance that given the continuation of that advance in the subsequent weeks, more recent margin debt will have accumulated to a total that eclipses the July 2007 record of $381 billion.

Clearly, the dollar value of margin debt has experienced a secular increase over time, so the levels aren’t as important as the cyclical variations. In particular, note that rapid and nearly parabolic increases in leverage tend to appear as the market approaches major peaks and bullishness feeds on itself. There are a number of series that can be used to normalize the long-term uptrend and to put the amount of margin debt in context. Notice that one would not want to normalize using the market value of stocks themselves. The reason is that margin debt surges near market peaks and collapses at market troughs, so to divide by the level of prices at those points would actually destroy much of the information content of margin debt (though you still typically observe debt rising much faster than prices as the market peaks).

Below, margin debt is presented as a percentage of GDP. Presently, margin debt is more than 2.3% of GDP, the highest level in history with the exception of the approaches to the 2000 and 2007 market peaks. Clearly, there have been changes in market structure over time, such as the emergence of hedge funds, long-short strategies and the like. So the long-term increase in margin debt certainly has some “structural” features to it. Again, however, the important feature to observe is not so much the absolute level, but the cyclical tendency for spikes in margin debt to accompany overvalued, overbought, overbullish market peaks. The subsequent market collapses are typically worsened by the inability of investors to simultaneously exit overleveraged positions that were all based on the same investment thesis.

There is no question that objective, careful, historically-informed analysis has had enormous challenges in the context of monetary interventions and fiscal deficits that have suppressed yields, temporarily boosted profit margins, and encouraged speculative leverage. Unfortunately, however effective these interventions have been in achieving speculative outcomes and kicking cans beyond their normal resting places, the endgame is still the same. Again, the endgame of overvalued, overbought, overbullish, overleveraged markets is forced liquidation.

Margin debt is soaring, valuations are now elevated even on the assumption that profit margins 70% above their historical norms will be sustained indefinitely, yields are compressed on nearly every asset class, and there is increasing evidence that Fed “stimulus” is incapable of exerting meaningful effects on the real economy and is exerting only speculative effects on an already overspeculative market. With a record 74% of Wall Street strategists now bullish, who is left to embrace further speculation, and how deep will the required losses be to induce the conservative 26% to absorb the overleveraged exposure of the exuberant 74% when forced liquidation becomes necessary?

On the temptation to disregard proven indicators

As a side-note, it’s important for investors to be wary of “structural” arguments intended to discard indicators that have very reliable cyclical records. For example, hardly a day goes by that we don’t see an attempt to harness some long-term structural factor, such as increasing globalization of trade, to explain away the spike in profit margins over the past few years – in the hope of proving that these margins will be permanent this time. Some of these arguments are discussed in recent weekly comments. But these factors don’t explain the cyclical fluctuations in profit margins at all, and can’t be used to discard the accounting relationships and decades of evidence that corporate profits have a strong secular and tight cyclical mirror-image relationship with the combined total of government and household savings.

Investors get themselves in trouble when they embrace “new economy” theories not because those new theories can be demonstrated in the data; not because existing approaches fail to fully explain the subsequent historical outcomes; but solely because time-tested approaches suggest uncomfortable outcomes in the present instance.

The same sort of structural second-guessing is evident in the gold market here – a good example of what forced liquidation looks like, as my impression is that leveraged longs have been forced into a fire-sale in recent weeks, creating good values for longer-term investors, but with continued near-term risks. If we look at the ratio of gold prices to the Philadelphia gold index (XAU), we do believe there are structural factors that affect that ratio (primarily the increasing cost of extracting gold over time). But these don’t explain away or eliminate the strong cyclical relationship between the gold/XAU ratio and subsequent returns on the XAU over the following 3-4 year periods. So while we don’t believe that the record high gold/XAU ratio can be taken entirely at face value, there’s no question that it is elevated even on a cyclical basis (that is, even allowing for a gradual structural increase over time), and there’s no question in the data that cyclically elevated gold/XAU ratios have been associated with strong subsequent gains in the XAU index over a 3-4 year period on average, though certainly not without risk or volatility.

As a final example, some analysts (such as the Dow 36,000 authors) have argued that the proper risk premium on stocks, relative to Treasury securities, should be zero. This line of argument was used in 2000 to suggest that stocks were still cheap despite high apparent valuations. But this “secular” argument for high valuations ultimately did not weaken the long-term evidence and tight cyclical relationship between valuations and subsequent market returns. Despite all the new economy arguments about productivity growth, the internet, globalization, the great moderation, and the outdated relevance of risk premiums, stocks still went on to lose half their value over the next two years, and to produce negative returns over the decade that followed.

The bottom line is that it becomes very tempting – both in speculative markets and fearful ones – to discard well-proven indicators as meaningless by arguing that some “structural” change in the market or the economy makes things different this time. True, those arguments can sometimes be used to explain very long-term changes in the level of an indicator. But even then, new economy arguments are typically ineffective at explaining away the informative cyclical variations in good indicators. Be particularly hesitant about ignoring indicators whose cyclical variations have been effective even in recent data, as is true of the ability of time-tested valuation approaches to explain subsequent 10-year market returns even during the period since the late-1990’s, and the ability of government and household savings to tightly explain cyclical swings in profit margins and subsequent profit growth, even in the most recent economic cycle.

Notes from the Wine Country Conference

A year ago, my friend Mike Shedlock (Mish) lost his wife Joanne to ALS (Lou Gehrig’s disease). Mike called with the idea of hosting a conference in Sonoma, California to benefit theLes Turner ALS Foundation. I thought that this would be something special, and it certainly proved to be just that. I finally met an old friend, John Mauldin, who I’ve corresponded with for years, and who was every bit as engaging, enthusiastic and insightful I expected. Chris Martenson was enormously likeable, not to mention brilliant – giving a powerful presentation on resource use and its present and likely future impact. Jim Chanos and Michael Pettis gave clear-sighted presentations focusing on the growth “miracle” in China and the on-the-ground realities there. Mish finished the day of presentations with historical insights on inflation and fiat currencies. Participants came from around the country and internationally, and joined us for dinner and a tour of Sonoma wineries. Jim added a generous donation in addition to his presentation. Michael Pettis flew in from China to present at the conference, and immediately back, which was a remarkable act of support for the charitable goal. Mish and his partners atSitka Pacific, JJ Abodeely and Brian McAuley were wonderful hosts. In all, their efforts raised nearly $500,000 for ALS.

The presentations and panel discussions were videotaped, and are being posted to theWine Country Conferencewebsite, along with slide decks (see the left menu of the site). If you find them interesting or useful, please consider even a small gift to theLes Turner ALS Foundation. Even modest gifts, across thousands of visitors, will make a real impact. Thanks.

A quick side note – a question relating to corporate profits demanded more time in the Q&A than I was able to properly devote to it – a more complete response is in the footnote of last week’s market comment (seeIncreasingly Immediate Impulses to Buy the Dip). Again, the reason that the (Investment – Foreign Savings) term adds little variation to profits over the business cycle is that variations in gross domestic investment as a share of GDP are tightly and inversely correlated with variations in the current account deficit (a chart is presented inTaking Distortion at Face Value). Nor do dividends add material variation to the profits relationship over the economic cycle. The upshot is that there is an extremely strong inverse relationship, both in terms of levels – and more importantly, in terms of variations – between corporate profits and the combined total of government and household savings. There are a million ways to deny this relationship, and many seem perfectly convincing until one works out the arithmetic and examines the data. The significant retreat in corporate profits over the next several years will take investors by surprise – it should not.

The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Only comments in the Fund Notes section relate specifically to the Hussman Funds and the investment positions of the Funds.

© Hussman Funds