Failed Transmission - Evidence on the Futility of Activist Fed Policy

“When buying a used car, punch the buttons on the radio. If all the stations are rock and roll, there's a good chance the transmission is shot.” - Larry Lujack, “Superjock,” WLS Radio, Chicago

In 1983, after graduating from Northwestern, I spent much of my time in the old Vogelback computing center, lodged in a semi-underground building reminiscent of a bomb shelter. You’d have to carry stacks of punchcards to a mainframe operator, and then wait patiently until your output was delivered through a mail slot. There, I ran statistical studies on the financial markets, using every data series I could get my hands on, convinced that the best basis for investment decisions was evidence and historically-informed discipline. Since I lived fairly cheaply, for example, servicing my used car with parts pulled from similar cars at the junk yard (Larry Lujack was right), I was able to spend the rest of my time playing music: teaching children’s musical theatre, playing guitar and lead vocals for a great but rather loud pop-rock band called Smith/Smith, and working in the programming department of WLS Radio in Chicago, where we would track record store sales, requests, and other data to choose songs for the playlist. I credit my typing ability to Larry Lujack, who once walked by my desk as I was entering data, shaking his head in mock disappointment as I henpecked the keyboard with my index finger.

Over more than three decades since then, I’ve remained convinced that the data people look at, and the actions they take, need to be meaningfully and reliably linked to the outcomes they seek. Without data, as W. Edwards Deming once said, “you’re just another person with an opinion.” Whether we’re talking about investing, international relations, or economic policy, acting without the benefit of evidence is a shortcut that - despite its occasional near-term rewards - regularly ends in failure, and sometimes in disaster. The effectiveness of any “transmission mechanism” depends on a reliable correlation between behaviors and outcomes. Investors and policy makers have to adapt to new evidence, of course, but even if we are inclined to say “this time is different,” it should never mean discarding the lessons of history. Instead, it’s essential to discover how the new data fit in with what we already know.

With regard to the financial markets, my emphatic view is that Fed policy has not created a new, permanently high plateau as a result of its actions during the half-cycle since 2009. Rather, as I detailed in our 2016 Annual Report,

“From the standpoint of our investment discipline, the half-cycle since 2009 has been different from market cycles across history in only one significant way. By driving interest rates to zero, central banks intentionally encouraged investors to speculate long after historically dangerous ‘overvalued, overbought, overbullish’ extremes emerged. In my view, this has deferred, but has not eliminated, the disruptive unwinding of this speculative episode. By encouraging a historic expansion of public and private debt burdens, along with equity market overvaluation that rivals only the 1929 and 2000 extremes on reliable valuation measures, the brazenly experimental policies of central banks have amplified the sensitivity of the global financial markets to economic disruptions and shifts in investor risk aversion.”

Before addressing the economic impact of Fed policy, it’s useful to further examine its impact on the financial markets. Here, it’s quite obvious that zero interest rate policy has encouraged yield-seeking speculation by investors. Still, investors should be careful how they interpret this. As I’ve previously detailed in data from both the U.S. and Japanese markets, monetary easing in and of itself does not “support” the financial markets. Rather, easy money only reliably stimulates speculation when investors are already inclined to embrace risk (as evidenced by broad uniformity across market internals). As soon as investors become risk-averse (witness 2000-2002 and 2007-2009 for example), even aggressive and persistent Fed easing fails to prevent a market collapse.

Moreover, any economist with even a vague understanding of how securities are priced should understand that elevating the price that investors pay for financial securities doesn’t increase aggregate wealth. A financial security is nothing but a claim to some future set of cash flows. The actual "wealth" is embodied in those future cash flows and the value-added production that generates them. Every security that is issued has to be held by someone until that security is retired. So elevating the current price that investors pay for a given set of future cash flows simply brings forward investment returns that would have otherwise been earned later, leaving little but poorly-compensated risk on the table for the future (see QE and the Iron Laws for an illustration of this process).

In this context, the following statement last week by Federal Reserve Vice-Chairman Stanley Fischer last week (Bloomberg) displayed a strikingly narrow understanding of the investment process:

“Well, clearly there are different responses to negative rates. If you’re a saver, they’re very difficult to deal with and to accept, although typically they go along with quite decent equity prices. But we consider all that and we have to make trade-offs in economics all the time, and the idea is the lower the interest rate, the better it is for investors.”

To be fair, there’s a kernel of truth in Fischer’s view that lower interest rates are “better” for investors. In recent years, low interest rates have certainly encouraged speculation, stretching reliable measures of equity market valuation to the third most offensive level in U.S. history next to 1929 and 2000. But Fischer’s statement is also incomplete. A clear understanding of how financial securities are priced suddenly turns Fed policy from something that seems quite generous to investors into something that’s actually terrifically hostile. See, the lower the interest rate, the better it is for investors, but only provided that investors wholly ignore the future.

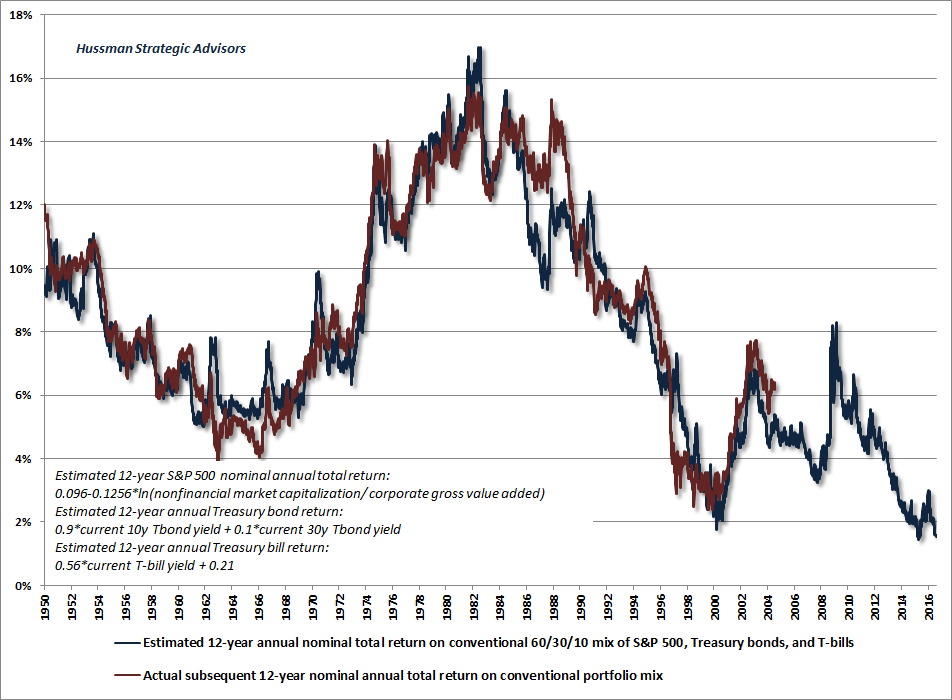

In reality, depressed interest rates ultimately benefit only those investors actually cash out at the speculative pre-crash extremes that the Fed seems so fond of producing. From here, for example, we estimate that the prospective 12-year nominal total return on a conventional portfolio mix (60% stocks, 30% bonds, 10% cash equivalents) is likely to average just 1.5% annually. As for the S&P 500 Index itself, we presently estimate annual total returns of just 1.4% annually over that horizon, with a strong likelihood of cyclical losses on the order of 40-55% in the interim (which would be a rather run-of-the-mill outcome from present extremes). Real prospective long-term returns are already likely to be negative on both fronts after inflation. The blue line on the following chart brings the future of conventional investing up-to-date.

The foregoing chart estimates 12-year prospective S&P 500 total returns using the log ratio of nonfinancial market capitalization to corporate gross value-added. The two have a -93% correlation on that horizon in post-war data (negative, because higher valuations imply lower subsequent returns). In judging any valuation measure, one should always ask how that measure is related to actual subsequent market outcomes. For a review of the reliability of other popular valuation measures see Choose Your Weapon.

Meanwhile, as I detailed in Morton’s Fork, it’s fine to assert that the S&P 500 is “fairly valued relative to interest rates” here, provided that “fair” is defined as an expected nominal total return now averaging just 1.4% annually on the S&P 500 over the coming 12-year period. Understand that when anyone says that stock market valuations are “justified” by the low level of interest rates, that’s exactly what they mean, whether they realize it or not.

Failed transmission: evidence on the futility of activist Fed policy

As a former academic economist, I was fortunate enough to have Thomas Sargent, Joseph Stiglitz, Ronald McKinnon, Robert Hall, and John Taylor as advisors during my doctoral study at Stanford. I remember sitting across from Tom as I eagerly started to write out an economic model to address a particular issue. He looked at me with a wry smile, and just said, Yoda-like, “investment precedes consumption.”

At the moment, Tom wasn't talking about economics. Yes, the fundamental driver of economic growth, productivity, and living standards is productive investment. Indeed, the central failure of policymakers since 2000 has been their constant efort to encourage debt-financed consumption, rather than creating incentives to channel savings toward real, productive investment at every level of the economy (productive infrastructure, workforce training, early-stage capital investment, R&D, education). Since the late-1990's, the growth of real U.S. gross domestic investment has collapsed to one-fifth of the rate it enjoyed in preceding post-war decades. Growth in real gross domestic investment has been zero over the past decade. Not surprisingly, U.S. productivity growth has followed. See, speculative malinvestment, debt-financed consumption, and market overvaluation doesn't produce wealth. Financial securities actually net out to zero in the calculation of a nation’s wealth because every security is an asset to the holder and a liability to the issuer. Instead, the true wealth of a nation is embodied in its capacity to produce, as measured by the stock of real investment (productive capital, stored resources, infrastructure, knowledge) it has accumulated as a result of prior saving. Policy makers would benefit from that understanding. But that's not what Tom was talking about in the moment.

No, when Tom said "investment precedes consumption," he was talking about restraint. It would be helpful if policy makers carried that idea in their heads. “Consumption” in this sense, is the desire to act, to form policy, to make whatever assumptions that will quickly allow us to get going and do something. “Investment” is the care and effort we take to clearly understand the problem, and especially when our actions involve risk, to establish evidence that our actions will be meaningfully related to the outcomes we seek.

Once I left that group of mentors, it became clear how few of my other colleagues in the field actually studied the economy. Rather, they studied “economies” in a very abstract sense, often with virtually no mapping between the models they studied and the real world. “Assume an economy with two islands, a turnpike, and 5 guys named Jack, one of whom is the government and nobody knows it.” Or “assume that a representative consumer has a fixed endowment and chooses how to spend it over time, based on the interest rate set by a monetary authority.” Assume, assume, assume, and if you test against real data at all, you can claim validity as long as you get a significant F-test, even if the practical magnitude of that effect is economically meaningless. The problem, for me, is that the models were then used to suggest real-world policies.

So here’s a question: “Is there clear evidence, across history, showing that large, activist changes in monetary policy instruments are reliably correlated to positive outcomes, of a meaningful size, in the real economy?”

The dogmatic insistence on pursuing policies based on assumptions rather than economic evidence; the failure to invest in the careful analysis of cause-and-effect relationships before consuming in the form of activist policy, is where I’ve lost all respect for monetary economists. They’ve jumped straight to consumption - pursuing recklessly experimental policies, without first establishing evidence that their tools have a reliable correlation with actual subsequent economic outcomes.

As I’ve noted before, the “counterfactual” of how the economy would have done without these interventions is readily available. Macroeconomists know that this involves comparing the projections from constrained and unconstrained vector autoregressions (VARs). Regardless of whether one uses observable data, as we do, or “shadow” monetary measures, as Wu and Xia do, the result is the same: all of this reckless intervention has boosted U.S. output by less than 1%, and lowered the unemployment rate by just over one-tenth of 1% beyond what would have been expected from conventional monetary policy (as defined by the Taylor Rule). Though Wu-Xia dutifully report this negligible impact as evidence that extraordinary monetary policy “succeeded,” the magnitude of this success is economically meaningless, and pales in comparison with the speculative extremes that have been created in the process.

The essential truth is this. Most of the variation in output, employment growth, and inflation across history can be reasonably predicted using lagged values of non-monetary variables alone. Adding information from monetary variables like the Federal Funds rate, the monetary base, and even Treasury yields, provides very little additional information. Moreover, only the “systematic” component of monetary policy - the part that can be explained by lagged non-monetary variables, has any meaningful correlation at all with subsequent economic outcomes. The remaining “activist” component does very little except to cause distortions, particularly in the financial markets. Those distortions ultimately cause economic damage when they collapse, but over a much longer horizon than the Fed seems to consider.

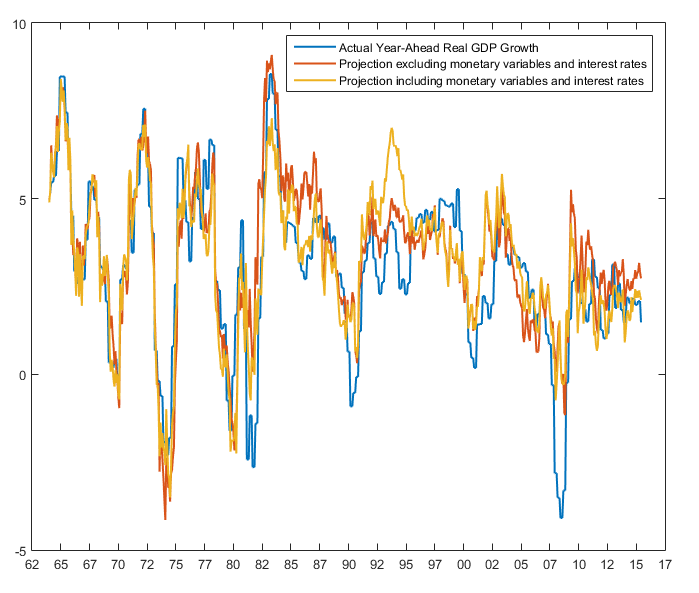

I've previously made this argument using methods like vector autoregression and Kalman filtering. Below, in an effort to demonstrate the case as simply as possible, in a way that readers can replicate if they like, the charts were produced by estimating rolling regressions, which ensure that the simple projections shown would have been available to a policy maker at each point in time. The first chart shows the year-ahead growth rate of real GDP, along with projected values based a) solely on non-monetary variables and b) including monetary variables and interest rates.

Non-monetary variables include current and lagged values of real GDP growth, payroll employment growth, CPI inflation, the output gap between real and potential GDP, and the ISM Purchasing Managers Index. The monetary variables include the Federal Funds rate, the ratio of the U.S. monetary base to nominal GDP, and the 10-year Treasury bond yield.

You’ll notice that, with few exceptions, there’s precious little difference between the red and yellow lines. Adding monetary variables to the information set simply does not materially improve forecasts about subsequent real GDP growth over and above the information that’s already contained in purely non-monetary variables.

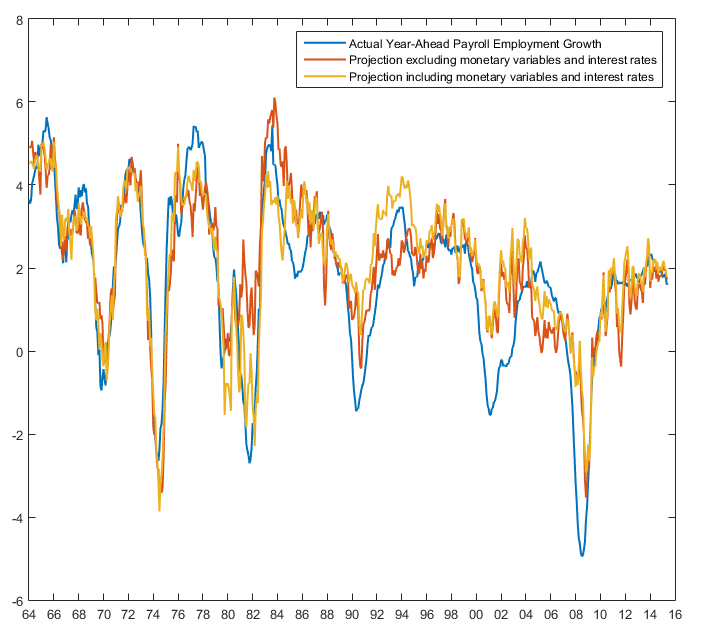

The next chart shows the same outcome for subsequent growth in total nonfarm payrolls.

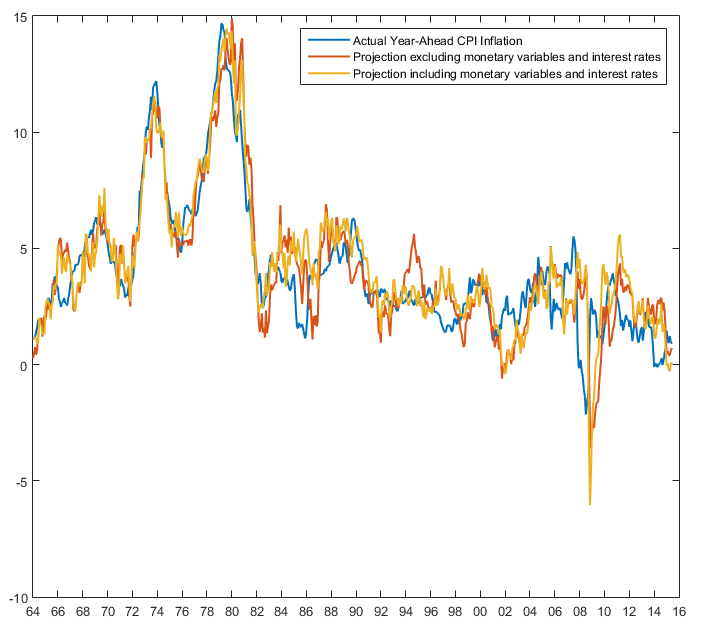

Strikingly, the same is also true for CPI inflation. Adding information about monetary variables and interest rates does virtually nothing to improve on forecasts based on purely non-monetary variables.

Does this mean that monetary policy is completely useless in affecting subsequent economic outcomes? Not so fast. We have to make a distinction between the “systematic” component of monetary policy that’s correlated with non-monetary variables (output, employment, inflation), and the remaining “activist” component. See, it’s possible that the systematic or rules-based component of policy is actually useful and necessary in producing economic outcomes. Since that systematic component overlaps or “spans the same space” as the non-monetary variables, we can’t rule out the possibility that it has legitimate effects. All we can say with confidence is that the activist component isn’t doing much, except to produce speculative episodes that negatively impact the economy when they collapse. But those effects emerge over a much more extended horizon.

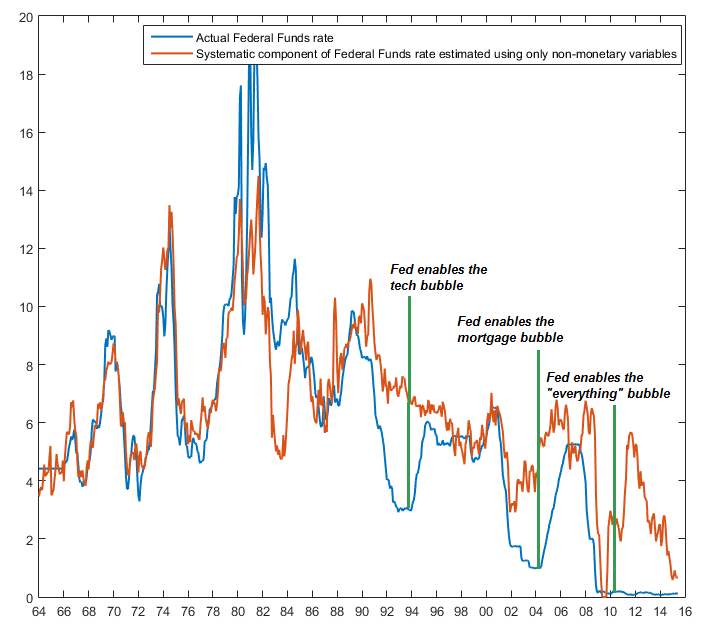

In the chart below, the blue line shows the actual Federal Funds rate over time, while the red line shows the systematic component. The difference between these two lines is what I’m calling the “activist” component of monetary policy.

You’ll notice a few things immediately. First, in the effort to break the back of inflation, Paul Volcker probably tightened monetary policy in 1981 a few percent beyond what might have been necessary, but it was also quite a brief deviation. Likewise, it’s possible that monetary policy could have been briefly loosened following the 1981-1982 recession somewhat more than it was in practice, but it’s clear that this was also a brief deviation. In the context of the disruptive inflation of the 1970’s, I have nothing but praise for the remarkable fidelity of monetary policy during Volcker’s tenure to a systematic and rules-based discipline. Since we observe nearly zero correlation between the “activist” component of monetary policy and subsequent economic outcomes, the most likely effect of Volcker’s additional tightness in 1982 was to help in driving the financial markets to their deepest level of undervaluation, and highest level of prospective future investment returns, in the post-war era.

Contrast that with the large and persistent activist deviations that Alan Greenspan, Ben Bernanke and Janet Yellen have pursued under their leadership at the Fed. In each case, we observe aggressive departures from the Fed Funds rate that one would have projected based on current and lagged data on output, employment, and inflation. In turn, those three large deviations helped to produce a series of three speculative bubbles in the financial markets; the first that ended with the technology collapse, the second that ended with the global financial crisis, and the third that has now brought reliable measures of valuation to one of the most offensive extremes in U.S. history. The problem is that these speculative consequences only emerge over a period of years. Indeed, the "activist" component of the Federal Funds rate has a correlation of -0.53 with the ratio of market capitalization/nominal GDP three years later. The two prior postwar valuation extremes in 2000 and 2007 were both followed by a loss of half the market value of the S&P 500 (with even deeper losses in technology and financial sectors, respectively). The disruptive consequences of this third episode are still ahead, and are now effectively baked-in-the-cake.

Let’s examine the “systematic” and “activist” components of monetary policy and their relationship to actual subsequent economic outcomes a bit further. The table below shows the correlation of each component with changes in real GDP growth, employment growth, and CPI inflation over the following year. Only the systematic component of the Federal Funds rate is meaningfully related to subsequent economic outcomes (though even that relationship isn't very strong). Those correlations are negative because when the systematic component of the Fed Funds rate is lower, subsequent economic activity is typically stornger. But notice that the relationship between the activist component and subsequent economic outcomes is essentially zero. For inflation, the correlation actually goes slightly in the wrong direction. The same general result holds for versions of the Taylor Rule, though to varying degrees. For the monetary base (not shown), whether one uses the growth rate or the ratio to nominal GDP, there’s little correlation with subsequent economic outcomes at all, regardless of which component one examines.

Correlations between systematic and activist components of the Federal Funds rate and subsequent economic activity

|

Systematic |

Activist |

|

|

Subsequent change in real GDP growth |

-0.30 |

+0.02 |

|

Subsequent change in employment growth |

-0.42 |

-0.04 |

|

Subsequent change in CPI inflation |

-0.32 |

+0.05 |

Remember, the systematic component is driven wholly by current and lagged values of non-monetary variables (output, employment, and inflation). Additional monetary policy deviations are useless. Now, one might object that monetary data can’t possibly have such a weak relationship with subsequent economic activity. After all, we know that the yield spread (e.g. between 10-year Treasury bonds and 3-month Treasury bills) is a reasonably useful indicator of subsequent economic fluctuations. In fact, that’s true, but we can also break the yield spread into two components: 1) a systematic component representing the “fitted” value based on non-monetary variables alone (output, employment, inflation), and 2) a smaller residual, which is independent of non-monetary data. Here’s the kicker. It turns out that the systematic component has a higher correlation with subsequent changes in employment growth and real GDP growth (0.55 and 0.40, respectively), than the yield spread itself (0.50 and 0.32, respectively). In contrast, the residual has no meaningful correlation at all with subsequent economic changes on either front (0.06 and -0.05, respectively).

So yes, the yield spread is a useful economic indicator, but entirely because of the systematic component driven by non-monetary data, which acts as kind of a summary statistic for economic conditions. Again, the part that’s uncorrelated (“orthogonal”) to non-monetary data is totally useless.

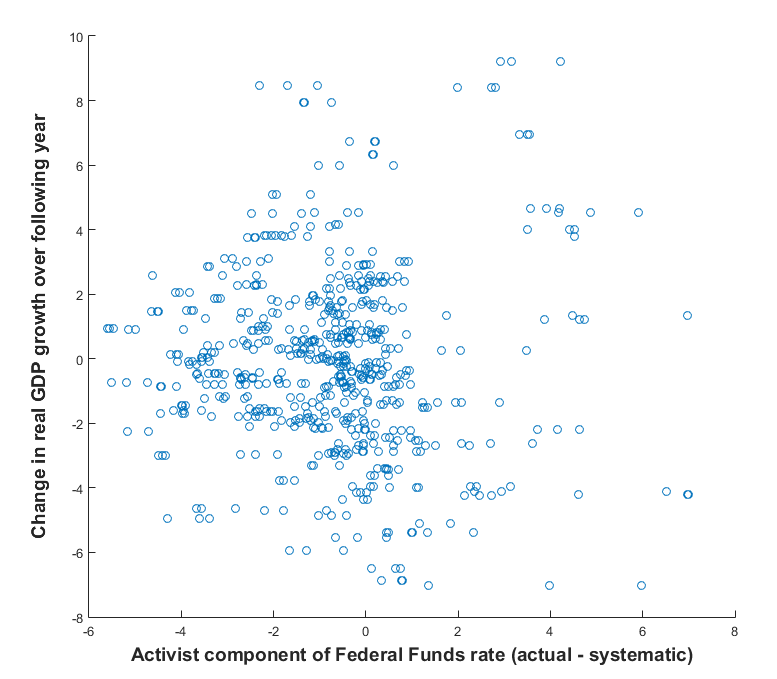

The chart below shows exactly how weak the relationship is between the activist component of monetary policy and subsequent changes in economic growth. The charts for employment and CPI inflation look virtually identical. The relationship is a broad and random scatter of points.

From the foregoing data, we can conclude the following:

- Much of the variation in U.S. output growth, employment, and inflation follows a systematic and largely mean-reverting process, and is reasonably well-predicted by previous lagged values of those same variables.

- Adding information about monetary policy variables and interest rates does very little to improve on projections based on non-monetary data alone.

- While we can’t rule out a contribution of monetary policy to subsequent economic outcomes, only the “systematic” or “rules-based” component of monetary policy - the portion that can be explained by prior non-monetary variables (output, employment, inflation) - is actually correlated with those outcomes.

- There is no economically meaningful or reliable correlation between “activist” monetary policy departures and subsequent economic outcomes, except to produce speculative bubbles and collapses that impact the economy over a longer horizon than the Fed seems to consider.

- The trajectory of the U.S. economy since the global financial crisis can be largely explained by non-monetary variables alone. Numerous methods (VAR, Kalman filtering, rolling regression) demonstrate that the extreme and activist monetary experimentation of the Federal Reserve has not materially altered that course.

These conclusions aren’t simply a critique but an indictment of Federal Reserve policies. The Fed has insisted on slamming its foot on the gas pedal, refusing to recognize that the transmission is shot. So instead, the fuel is instead just spilling around us all, waiting for the inevitable match to strike. We can clearly establish that activist monetary policy - deviations from measured and statistically-defined responses to output, employment and inflation - have had no economically meaningful effect, other than producing a repeated spectacle of Fed-induced, speculative yield-seeking bubbles. The American public has repeatedly paid the consequences of the Federal Reserve’s insular dogma when those bubbles have inevitably collapsed, but those consequences are typically spread over a longer horizon than the Fed appears to consider.

From dogma to coercion: Jackson Hole becomes the Manhattan Project

If there was one key theme of last week’s economic symposium at Jackson Hole, Wyoming, it certainly wasn’t to examine the weak links between monetary policy tools and economic outcomes. It also wasn’t to examine the extent to which existing policy has distorted financial markets, bringing reliable equity valuation measures to historically obscene levels, and encouraging the highest ratio of corporate debt to corporate gross value-added in history (much of it of the “covenant lite” variety providing little recourse in the event of bankruptcy).

No, the focus was on pushing harder on the string; on the technical details of how policy makers might provide, in the exact words of Carnegie Mellon’s Marvin Goodfriend, “the case for unencumbering interest rate policy so that negative nominal interest rates can be made freely available and fully effective as a realistic policy option in a future crisis.”

Fed Chair Janet Yellen, while not encouraging further easing in the near term, offered speculators the carrot that “future policymakers may wish to explore the possibility of purchasing a broader range of assets.” What she didn’t mention is that those future policymakers would have to include Congress, as Sections 13 and 14 of the Federal Reserve Act explicitly prohibit such purchases, except in the emergency context of discounting bills of less than 30-day maturity. Of course, Ben Bernanke stretched the concept of “discounting” to include shuttling distressed mortgage securities into a series of off-balance-sheet shell companies called Maiden Lane, but Congress has since revised those sections of the Act to read like a children’s book.

The academics at Jackson Hole also discussed the possibility of raising the inflation “target” of the Federal Reserve from 2% to 4%, an idea which is much like saying “we can’t hit the broad side of a barn from 50 feet, so let’s try from 100.” This ties in with the concept of “helicopter money,” which is really just a fiscal stimulus package financed by creating currency. Christopher Sims, as one of a minority of economists who recognizes that monetary policy is never fully independent of fiscal policy, discussed this idea, correctly but chillingly, by noting that helicopter money essentially operates by destroying fiscal credibility:

“Fiscal expansion can replace ineffective monetary policy at the zero bound, but fiscal expansion is not the same thing as deficit finance. It requires deficits aimed at, and conditioned on, generating inflation. The deficits must be seen as financed by future inflation, not future taxes or spending cuts.”

Understand that nothing in these discussions was focused on the question of whether policy instruments were actually reliably and materially correlated with sizeable economic outcomes. No, the transmission mechanisms were taken care of by making assumptions.

One session addressed “pass through” from Fed policy to market interest rates; essentially, how buttery the Fed’s low-interest hot potatoes are in affecting other markets as monetary policy tightens the screws. Presently, the Fed pays 0.50% to banks via “interest on excess reserves” (IOER) on their surplus cash, but it pays just 0.25% to money market funds and the like via “reverse repurchases” (RRPs) of their surplus cash. Of course, interest rates are determined at the margin, and there’s no incentive for banks to offer interest rates above the 0.25% rate that non-bank cash holders are stuck with. So market interest rates have tracked the lower RRP rate. Indeed, given that the Fed would have reduce its balance sheet by about $1.5 trillion to generate 0.25% market interest rates the old-fashioned way, without paying that interest itself (see Blowing Bubbles: QE and the Iron Laws), the RRP rate is currently the only thing that pulls market interest rates away from zero. The extra interest the Fed pays on idle bank reserves is essentially a multi-billion dollar giveaway of public funds to the banking system. Predictably, banks tend to quickly lower deposit rates after a Fed cut, and raise them much more slowly after a hike.

At Jackson Hole, these responses of market rates aren't attributed to bank behavior at all. Instead, we're asked to assume something called “depositor attention deficit” where some depositors are just, well, “slow.” In that world, the RRP rate is actually seen as a threat that pulls “fast” depositors into money market funds, and leaves banks with the remaining “slow depositors,” reducing the responsiveness of bank deposit rates after a Fed hike. Proof (this from a paper by Duffie and Krishnamurthy), looked like this:

Another paper argued for keeping the Federal Reserve’s balance sheet permanently high, even after interest rates are well above zero (a feat that would involve paying banks billions of dollars of interest on reserves, potentially at rates well above the interest rates that the Fed is presently bargaining for as it replaces bonds as they mature). The idea, as Harvard’s Greenwood, Hansen, and Stein proposed, is to totally dominate the market for short-term assets so that the Fed can “crowd out” the ability of the private sector to borrow money at short-term rates. This, in their view, would improve financial stability.

This is nothing but an argument for more Fed intervention in order to solve a problem that was created by Fed intervention. As I warned as the bubble was emerging, and before its collapse, the global financial crisis was a predictable response of Fed-induced yield-seeking speculation, brought about by inappropriately low interest rates, and enabled by banks and Wall Street financial institutions who had an incentive to create more “product,” regardless of credit quality, in order to satisfy the yield-seeking demand of speculators. Sound familiar? The Fed has done precisely the same thing in recent years, but writ much larger, to extend to all classes of assets.

I’ll emphasize once again that the global financial crisis did not end because the Fed expanded its balance sheet. The crisis ended precisely when, in the second week of March 2009, the Financial Accounting Standards Board (FASB) responded to Congressional pressure, and changed rule FAS157 to remove the requirement for banks and other financial institutions to mark their assets to market value. With the stroke of a pen, that change eliminated the specter of widespread defaults, by making balance sheets opaque. Of course, if we should have learned anything from Charles Ponzi, Bernie Madoff, Enron, and a thousand other examples, it’s that opaque balance sheets may be great fun in the short-term, but ultimately become weapons of mass destruction.

Think carefully about what the economists at Jackson Hole were really saying: “If you’ve worked hard, and saved, and want to provide for your future without joining in on the late-stage of a speculative bubble, then our job is to figure out how to punish you into abandoning those plans and consuming or speculating now. We’re really smart and well-intentioned people, and can’t imagine that repeated episodes of yield-seeking speculation and collapse could possibly be our doing, so the only solutions to be found must be those that expand the size, scope, and aggressiveness of our interventions. If zero interest rates aren’t enough, perhaps we can eliminate the lower bound entirely. If negative interest rates aren’t enough, then we need to wipe out your purchasing power by raising the inflation targets we already can’t hit. Sorry, it’s a trade-off. We can’t prove the benefits of that trade-off in actual data unless we’re super-careless about what we call evidence and only take credit for improvements, but let’s assume a tradeoff. QED.”

This delight in the technical details of pulling off something new, without evidence of human good, is how intelligent people lose their soul. It seems to me that monetary economists have fallen into that abyss. As the physicist J. Robert Oppenheimer wrote:

“When you see something that is technically sweet, you go ahead and do it and you argue about what to do about it only after you have had your technical success. That is the way it was with the atomic bomb.”

© Hussman Funds