As of last week, our assessment of the overall market return/risk profile remains dominated by three factors, the first being wickedly extreme valuations (which we associate with near-zero expected S&P 500 nominal total returns over the coming 12-year period, with the likelihood of interim losses on the order of 50-60%), the second being the most extreme syndromes of overvalued, overbought, overbullish conditions we define, and the third - and the most important in terms of near-term market risk - being divergent and deteriorating market internals on the measures we use to assess investor risk-preferences.

It’s important to emphasize that this full set of conditions has been present during only a fraction of the advancing half-cycle since 2009, and that on balance, the S&P 500 has lost value during these periods. Moreover, this is the same set of conditions that allowed us to anticipate the 2000-2002 and 2007-2009 collapses.

Investors would do well to understand the distinction between an overvalued market that retains uniformly favorable market internals, and an overvalued market that has lost that feature. I’ve openly detailed our challenges in this half cycle and how we adapted, primarily in 2014 (see Being Wrong In An Interesting Way for a detailed narrative). The central lesson of this half-cycle is not that quantitative easing or zero interest rates can be relied on to permanently support stocks, but rather, that the novel and deranged monetary policy of the Federal Reserve was able to encourage continued yield-seeking speculation long after the emergence of “overvalued, overbought, overbullish” extremes that had reliably heralded steep downside risk in prior market cycles across history. In the face of zero interest rates, one had to wait for market internals to deteriorate explicitly (indicating a shift in investor preferences from speculation to risk-aversion), before adopting a hard-negative market outlook.

Even here, an improvement in market internals would defer our immediate concerns about severe downside risk. Presently, however, investors who believe our current defensiveness is simply “more of the same” haven’t absorbed the central lessons of our challenges in the advancing portion of this market cycle, nor the distinctions that could potentially save them from extraordinary market losses over the completion of this cycle.

How to wind down a $4 trillion balance sheet

Last week, the Federal Reserve issued a set of Policy Normalization Principles and Plans, by which the size of its portfolio of government securities would “decline in a gradual and predictable manner until the Committee judges that the Federal Reserve is holding no more securities than necessary to implement monetary policy efficiently and effectively.” Essentially, as existing securities held by the Fed mature, the Fed would reinvest the proceeds into new government securities only to the extent that those proceeds exceed “caps” which begin at $10 billion monthly, expand by an additional $10 billion every 3 months, and top out at $50 billion monthly.

Recall how the Federal Reserve’s open market transactions operate. When the Fed buys Treasury securities or U.S. government agency securities from the public (it can’t buy them directly from the Treasury, because, see, that would make us look like a banana republic), it pays for those securities by creating bank reserves, which are deposited in the seller’s bank account. The bonds become assets on the Fed’s balance sheet, and the reserves are liabilities of the Fed (as is the currency in your pocket, which you can verify by looking at the top line just above the picture of a President). The sum of currency and bank reserves comprises the “monetary base,” which is the only version of the money supply that the Fed can directly control. In short, when the Fed buys bonds, the Fed creates base money. When the Fed sells bonds (or Fed holdings mature without the Fed reinvesting the proceeds in new bonds), the Fed retires base money.

How does this relate to short-term interest rates? Well, historically, neither currency nor bank reserves have earned interest (I'll discuss a new wrinkle shortly). As the Fed creates more zero-interest base money, some investors decide that they would prefer to hold a closely competing asset that does earn interest; the most similar option being Treasury bills. Those transactions don't change the amount of outstanding base money or Treasury bills; it just changes who owns them, and at what price. Increasing the size of the zero-interest monetary base encourages some investors to bid up Treasury bills (which drives down the interest rate on Treasury bills), and the process stops at the point where the yield on Treasury bills is just low enough to make investors indifferent between holding zero-interest base money and those now-lower yielding Treasury bills. Put another way, the new level of short-term interest rates ensures that investors, in aggregate, are willing to hold the outstanding quantity of both base money and Treasury bills. Conversely, contracting the size of the monetary base tends to raise short-term interest rates.

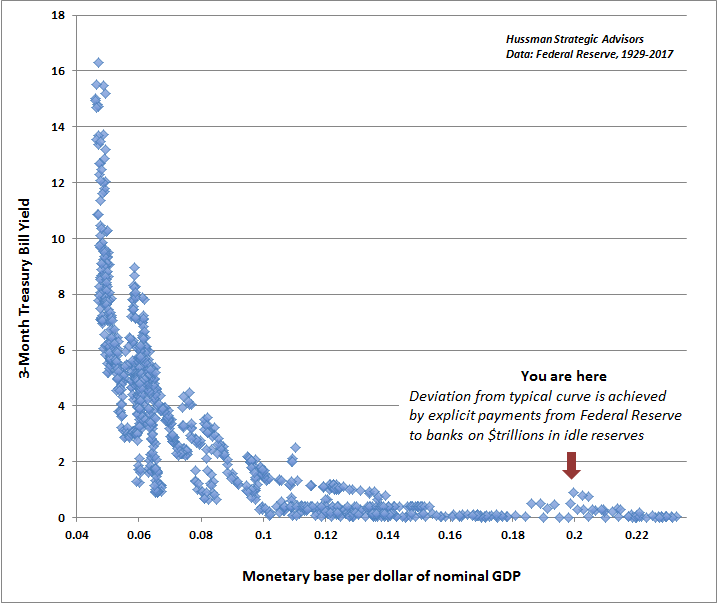

Economists know this relationship between base money and interest rates as the “liquidity preference curve.” As a practical matter, though, one has to normalize the monetary base by the size of the economy itself, so we find that the actual relationship is between Treasury bill yields and the ratio of monetary base/nominal GDP. The chart below shows this link; our version of the liquidity preference curve, in U.S. data since 1929. It’s one of the most robust relationships you’ll find in economics. The Fed does not have to make guesses about exactly what is required to normalize its balance sheet, except to the extent that it ignores a century of evidence.

Notice the little scatter of points in recent quarters that are slightly above the level one would expect given the current size of the monetary base. These points can exist because the Fed has added a new wrinkle in recent quarters. Because quantitative easing was pushed to deranged (literally de-ranged) extremes, the only way to raise interest rates above zero without immediately cutting the monetary base in half was to explicitly pay banks for holding idle reserves. This new practice of paying interest on reserves is how the Fed has raised rates in recent quarters, without the need to massively contract its balance sheet.

One of the risks the Fed is courting here is that if it buys, say, a 7-year Treasury bond, and its average policy rate over the next 7 years exceeds the yield-to-maturity when the Fed bought the bond, it will effectively be engaging in fiscal policy because it will have to pay more interest to banks than the interest it actually receives on the bond, and it would not recover that difference at maturity. This would effectively be unconstitutional, since only Congress can authorize such expenditures through an explicit budget process. It will be interesting to see how this plays out.

Currently, there are about 20 cents of monetary base outstanding for every $1 of U.S. nominal GDP. On the subject of "holding no more securities than necessary," the Fed’s balance sheet remains more than $1 trillion larger than is actually necessary to produce zero interest rates, and is nearly $2 trillion larger than the level that could achieve the current 1% Federal Funds target, without any need to pay banks interest on their idle reserves.

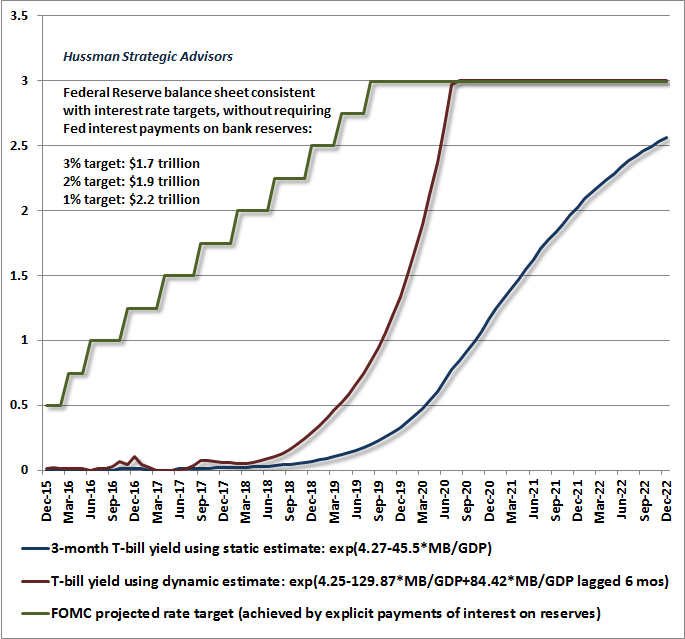

Given the extraordinarily well-behaved relationship between short-term interest rates and the ratio of the monetary base to nominal GDP, we can easily estimate the level of interest rates consistent with any particular size of the Fed’s balance sheet. A “static” or steady-state estimate does reasonably well, and requires only the current level of MB/GDP (though the best function is non-linear). One obtains a better fit across history by including the 6-month lagged value of MB/GDP as well, since there is a clear tendency for rates to decline faster than the static estimate when the monetary base is expanding, and to rise faster than the static estimate when the monetary base is contracting.

The latest statement from the Federal Reserve suggests a projected course for short-term interest rates reaching 3% by 2019, which would effectively require a 0.25% rate hike roughly every 5 months. Regardless of whether one agrees with that projection or not, it is relatively straightforward to project the size of the monetary base that would be consistent with that interest rate trajectory, without requiring the Fed to pay interest on excess bank reserves (IOER). Below, I’ve included both our dynamic and our static estimates of interest rates that would be consistent, in the absence of IOER, with the normalization plan announced by the Fed. It assumes that the Fed begins its normalization plan in December of this year, and pursues it until the Fed balance sheet is sufficient to achieve a 3% target. I estimate that a 3% target would be reached (using dynamic estimates) in 2020, after which the monetary base would have to continue to decline for a while longer, though at a reduced pace, in order to maintain that target over time.

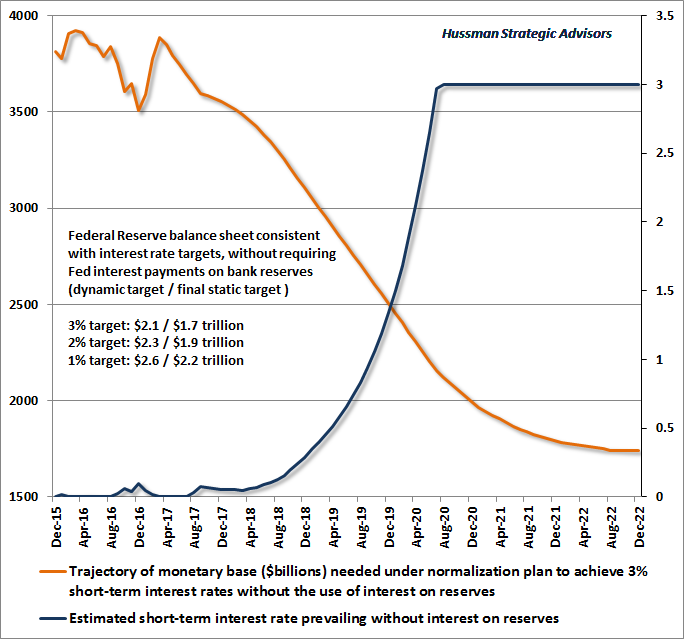

The chart below shows the associated trajectory of the monetary base under a bona-fide normalization plan. Depending on whether one uses static or dynamic estimates, the monetary base would have to decline from its current level of $3.8 trillion to a range between $2.2 and $2.6 trillion in order to establish a 1% target rate (without IOER); between $1.9 and $2.3 trillion to establish a 2% target rate; and between $1.7 and $2.1 trillion to establish a 3% target rate. If the Federal Reserve maintains a larger balance sheet, achieving those targets would require continued explicit payments of interest to banks on idle reserves, and the Fed would continue to exceed the historical parameters required to implement sound monetary policy. The chart below assumes a 5% growth rate for nominal GDP. Slower growth would require somewhat greater balance sheet contraction to achieve various interest rate targets (without IOER) over the coming years.

Frankly, we’re not hopeful that the coming years will unfold gently, not because the Fed will or will not normalize its balance sheet, but because a great deal of damage is already baked-in-the-cake as the result of years of yield-seeking speculation and low-grade credit issuance. If there was clear evidence that activist monetary policy has reliable economic benefits (above and beyond those that can be expected from simple mean-reverting behavior of non-monetary variables like output and employment, which is the entire story of the recovery since 2009), there might be some justification for what the Fed has done. But as I detailed in Failed Transmission: Evidence on the Futility of Activist Fed Policy, despite vapid theoretical diagrams and baseless verbal prose to the contrary, the hard economic data fail to support that view.

At some point, perhaps during the next financial collapse, the public may become willing to demand that policymakers support their behavior with systematic evidence of reliable correlations and substantial effect sizes linking policy actions to real economic activity. Instead, we know only one thing for certain, which is that, across history, extended periods of easy money, and the resulting frenzies of low-quality credit issuance and yield-seeking speculation that follow, have regularly unraveled into crisis and collapse. If one repeatedly learns that feeding a beast can briefly appease it, but predictably makes it more enormous, savage, and unstable, it is best to remember the lesson. Instead, central bankers have doomed the world to learn that lesson again.

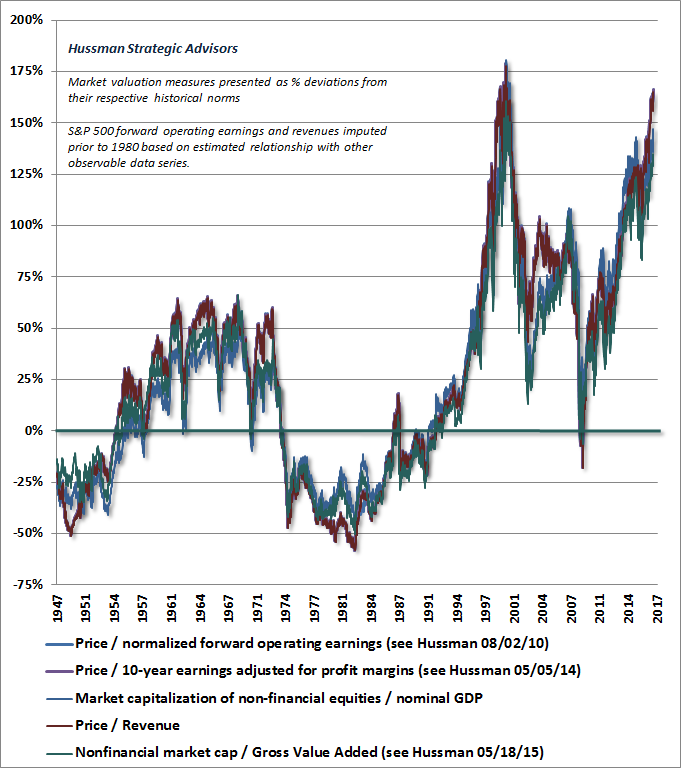

Presently, the most reliable market valuation measures we identify (those best correlated with actual subsequent S&P 500 10-12 year annual total returns) range between 140% and 165% above their historical norms. No market cycle in history, even those featuring quite low interest rates, has failed to draw them within 25% of those norms, or below, implying the likelihood of a 50-60% market decline over the completion of the current cycle.

Suspending the misplaced faith in easy money

Meanwhile, remember that Fed policy matters little once investors become averse to risk. The combination of market valuations and market internals is the most important feature to consider. It’s clear that, in the recent market cycle, zero interest rate policy was able to sustain yield-seeking speculation and uniformly favorable market internals long after extreme “overvalued, overbought, overbullish” syndromes emerged. That’s a lesson we will not forget. But that lesson is far different from assuming that easy money or low interest rates will support extreme valuations even in the face of divergent and deteriorating market internals.

Investors should recognize that in data since 1940 and prior to 2008, U.S. interest rates were at or below present levels about 15% of the time. During those periods, the average level of the Shiller cyclically-adjusted P/E was about -50% below present levels, and the average ratios of MarketCap/GVA, MarketCap/GDP and Tobin’s Q (market capitalization to replacement cost of corporate assets) were all about -60% below present levels. That's roughly the same distance that current market valuations are from post-war pre-bubble norms, even regardless of the level of interest rates. Put simply, investors have vastly overstated the argument that low interest rates "justify" extreme market valuations. Indeed, the correlation between the two is weak, nonexistent, or goes entirely the wrong way in most periods of U.S. history outside of the inflation-disinflation cycle from 1970 to 1998.

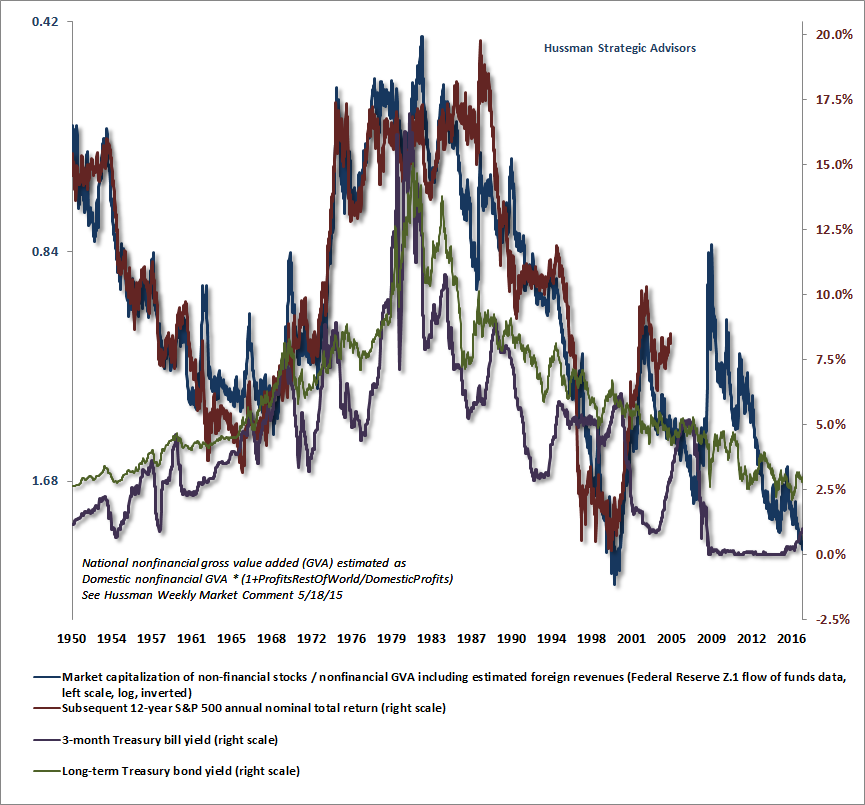

The chart below is instructive. The blue line (left scale, log, inverted) shows the ratio of nonfinancial market capitalization to nonfinancial corporate gross value-added, including estimated foreign revenues. The red line (right scale) shows the actual subsequent S&P 500 nominal average annual total return over the following 12-year period. The purple line shows 3-month Treasury bill yields. The green line shows long-term Treasury bond yields. The fact that this graph is a chaotic tangle of lines is a reminder that the link between interest rates and market valuations is far more tenuous than investors seem to assume.

As I detailed in The Most Broadly Overvalued Moment in Market History, to the extent that investors view interest rates as important, the proper way to factor them in is to first use existing prices and valuations to estimate prospective market returns (an exercise of arithmetic that does not require the use of interest rates), and then to compare those prospective returns with interest rates to judge whether prospective equity market returns are adequate. At present, we estimate that despite their rather depressed yields, Treasury bonds, as well as a sequence of investments in Treasury bills, are likely to outperform the total return of the S&P 500 well beyond a 12-year horizon. That’s a far cry from how stocks were priced between late-2008 and 2012 (see the chart above).

If our measures of market internals improve, we would defer our immediate concerns about downside risk, regardless of current valuation extremes. That’s particularly true if market internals were to improve along with a shift back to zero interest rates (which is essentially the lesson of the pre-2014 period). Indeed, an improvement in market action following a material retreat in valuations would likely shift us to a constructive or aggressive position, even if the retreat in valuations comes far short of a reversion to historically normal valuations. Note that all of these possibilities prioritize the behavior of market internals (and the investor risk-preferences they capture) above Fed policy in and of itself. The same prioritization holds versus economic factors, earnings growth, and a host of other variables.

I’ll say this once again. Our Achilles Heel in the advancing portion of this cycle was straightforward: in prior market cycles across history, the emergence of extreme overvalued, overbought, overbullish syndromes had an urgency that preceded even the behavior of market internals. Quantitative easing disrupted that regularity. But even since 2009, the S&P 500 has lost value, on average, in periods that joined rich valuation, “overvalued, overbought, overbullish” syndromes, and deterioration in the uniformity of market internals. That’s the combination we currently observe, and our market outlook will shift as the evidence does.

Recall that the Fed eased persistently and aggressively throughout the 2000-2002 and 2007-2009 downturns. Once uniformly favorable market internals are lost and investor preferences shift toward risk aversion, monetary policy is not supportive of equities, because safe, liquid money market assets are seen as desirable assets rather than inferior ones. When market internals deteriorate following an extended period of wickedly overvalued, overbought, overbullish conditions, market collapses have typically followed, regardless of the response of the Federal Reserve. Investors should understand that lesson now. My impression is that they are going to need it.

© Hussman Funds

© Hussman Funds

Read more commentaries by Hussman Funds