The Shiller P/E (S&P 500 divided by the 10-year average of inflation-adjusted earnings) is now 27, versus a long-term historical norm of 15 prior to the late-1990’s bubble. Importantly, the profit margin embedded into the Shiller P/E is currently 6.7% versus a historical norm of just 5.4%. The implied margin is simply the denominator of the Shiller P/E divided by current S&P 500 revenues (the ratio of trailing 12-month earnings to revenues is even higher at 8.9%). As I showed in Margins, Multiples and the Iron Law of Valuation, taking this embedded margin into account significantly improves the usefulness and correlation of the Shiller P/E in explaining actual subsequent market returns. With this adjustment, the margin-adjusted Shiller P/E is now nearly 34, easily more than double its historical norm.

This fact is important, because the Shiller P/E averaged 40 during the first 9 months of 2000 as the tech bubble was peaking. But that Shiller P/E was associated with an embedded profit margin of only 5.0%. Adjusting for that embedded margin brings the margin-adjusted Shiller P/E at the 2000 peak to 37.

Quite simply, stocks are a claim not on one or two years of earnings, but on a very long-term stream of cash flows that will actually be delivered into the hands of investors over time. For the S&P 500, that stream has an effective duration of about 50 years. At normal valuations, stocks have a duration of about half that because a larger proportion of the cash flows is delivered up-front.

The point is that our concerns about valuation aren’t based on what profit margins might do over the next several years. To take earnings-based valuation measures at face-value here is essentially a statement that current record-high profit margins, despite being highly cyclical across history, will remain at a permanently high plateau for the next 5 decades. That’s the only way that one can use current earnings as representative of the long-term stream of cash flows that stocks will deliver over time. In order to use a simple P/E multiple to value stocks, this representativeness assumption is an absolute requirement.

On other measures that have an even stronger historical correlation with actual subsequent market returns than either the Shiller P/E or the S&P 500 price/operating earnings ratio, the ratio of stock market capitalization to GDP is now about 1.33, compared to a pre-bubble norm of 0.55. The S&P 500 price/revenue multiple is now about 1.80, versus a historical norm of 0.80. On the measures we find most reliably associated with actual subsequent 10-year market returns (with a correlation of about 90%), the S&P 500 is not just double, but about 120-140% above historical norms. On a broader set of reliable but more varied measures, the elevation averages about 116%.

Current equity valuations provide no margin of safety for long-term investors. One might as well be investing on a dare. It may seem preposterous to suggest that equities are literally more than double the level that would provide a historically adequate long-term return, but the same was true in 2000, which is why the S&P 500 experienced negative total returns over the following decade, even by 2010 after it had rebounded nearly 80% from the 2009 lows. Compared with 2000 when we estimated negative 10-year total returns for the S&P 500 even on the most optimistic assumptions, we presently estimate S&P 500 10-year nominal total returns averaging about 1.3% annually over the coming decade. Low interest rates don’t change this expectation – they just make the outlook for a standard investment mix even more dismal – and the case for alternative investments stronger than at any point since 2000. I’ll repeat that if one associates historically “normal” equity returns with Treasury bill yields of about 4%, the promise to hold short-term interest rates at zero for 3-4 years only “justifies” equity valuations 12-16% above historical norms. Again, at more than double those historical norms, current equity valuations provide no margin of safety for long-term investors.

To put some full-cycle perspective around present valuations, understand that 1929 and 2000 are the only historical references to similar extremes. Moreover, aside from the 2000-2002 bear market (which ended at fairly elevated valuations but still allowed us to shift to a constructive outlook in early 2003), no bear market in history – including 2009 – ended with prospective 10-year returns less than 8% (See Ockham’s Razor and the Market Cycle to review the arithmetic of these estimates). This was true even in historical periods when short and long-term interest rates were similar to current levels. Currently, such an improvement in prospective equity returns would require a move to about 1200 on the S&P 500, which we would view as a fairly pedestrian completion of the current market cycle – certainly not an outlier from the standpoint of historical experience.

Major secular valuation lows like 1949, 1974 and 1982 pushed stocks to valuations consistent with prospective 10-year returns over 18% annually, and dragged the S&P 500 price/revenue ratio to about 0.40, and the ratio of market capitalization/GDP to about 0.33. At present, a secular valuation low would require "S&P 500" to be not only an index but a price target - though one that would also make a rather satisfying megaphone pattern out of the past 15 years of market action. Such an outcome only seems preposterous if one ignores the cyclicality of profit margins and assumes they have established a permanently high plateau. In any event, with the current price/revenue ratio at 1.80, and market cap/GDP at 1.33, the notion that stocks are in the early phase of a secular bull market (as some Wall Street analysts have suggested) can only reflect a complete ignorance of the historical record.

The line between rational speculation and market collapse

However – and this is really where the experience of the past few years and our research-based adaptations come into play – there are some conditions that historically appear capable of supporting what might be called “rational speculation” even in a severely overvalued market. Depending on the level of overvaluation, a safety net might be required in any event, and that would certainly be the case if those conditions were to re-emerge here. But following my 2009 insistence on stress-testing our methods against Depression-era data, and the terribly awkward transition that we experienced until we nailed down these distinctions in our present methods, the central lesson is worth repeating:

Neither our stress-testing against Depression-era data, nor the adaptations we’ve made in response extreme yield-seeking speculation, do anything to diminish our conviction that historically reliable valuation measures are of immense importance to investors. Rather, the lessons to be drawn have to do with the criteria that distinguish periods where valuations have little near-term impact from periods where they suddenly matter with a vengeance.

I detailed these lessons in my June 16, 2014 comment – Formula for Market Extremes (see the section entitled Lessons from the Recent Half Cycle). That’s really the point at which we were finally able to put a box around this awkward transition and view it as fully addressed. See also Air Pockets, Free Falls, and Crashes, A Most Important Distinction, and Hard-Won Lessons and the Bird in the Hand.

Historically, the emergence of extremely overvalued, overbought, overbullish conditions has typically been followed by an “unpleasant skew” – a succession of small but persistent marginal new highs, followed by a vertical collapse in which weeks or months of gains are wiped out in a handful of sessions. In prior market cycles, more often than not, periods of extremely overextended conditions were also already accompanied by a subtle deterioration in market internals or widening credit spreads.

In recent years, the persistent yield-seeking speculation encouraged by quantitative easing has weakened the overlap between these two conditions. That is, we’ve had repeated periods of severely overvalued, overbought, overbullish conditions, but they often have not been accompanied by internal deterioration or widening credit spreads. In those periods, stocks were generally resilient to significant losses. In contrast – even since 2009 – periods that have joined 1) overvalued, overbought, overbullish conditions with 2) deteriorating internals or widening credit spreads have been responsible for nearly stair-step market losses.

During the tech bubble, we introduced considerations related to market internals (what I often called "trend uniformity") as an overlay to our value-driven models. So our pre-2009 method of classifying market return/risk profiles had this distinction hard-wired into it. The ensemble methods that came out of our 2009-2010 stress-testing efforts were more effective in market cycles across history - including Depression-era data - but while they included trend-sensitive measures, they didn't impose them as an overlay. The basic narrative of the transition from those pre-2009 methods to our present ones boils down to 1) our self-inflicted stress testing miss, and 2) the need to re-introduce those overlays (albeit in a somewhat different form) to make our methods more tolerant of speculative bubbles. We certainly learned all of this the hard way, and my hope is that others will draw some benefit from that experience. Unfortunately, my sense is that many have learned entirely the wrong lesson, and are just as vulnerable to the next crash as they were to the other two collapses in recent memory.

You can see the effect of imposing those overlays in the narrowing of conditions under which we view a hard-negative outlook as appropriate. See last week’s comment, Iceberg at the Starboard Bow, for a chart of the cumulative performance of the S&P 500 across history in periods restricted to the conditions we presently observe.

Now, if we do observe an improvement in market internals and credit spreads, it would not make valuations any less obscene, but it would significantly ease our immediate concerns about market losses. A safety net would be required in any event, but there is a range of possible outlooks between hard-negative and constructive with a safety net. I suspect that the range of variation in our investment outlook is likely to be very confusing in the coming years to those who have swallowed the hook that I’m a permabear, because our present methods would have encouraged an unhedged, leveraged investment stance through about 62% of history (including over 20% of recent cycle – though at no time in the past 3 years). Again, we completed the transition from our pre-2009 method to our present method of classifying market return/risk profiles in June. The resulting adaptations are robust to market cycles across history, including the Depression, including recent bubbles and crashes, and including the current cycle. With these adaptations in place, nothing in recent years leaves us concerned that we would be unable to navigate a long continuation of the recent bull market (unlikely as we might view that outcome). We don’t need to hope for a market collapse, nor dread the possibility of a further advance. Our primary goal is simply to maintain a historically-informed discipline and align our outlook consistently as market conditions change.

At present, the fact that we are highly concerned about market risk is a reflection of a market environment that joins extremely overvalued, overbought, overbullish conditions with still-troubling dispersion in market internals and a widening of credit spreads. That will change. In short, our concerns about market risk remain extreme at present, and will shift considerably as the evidence changes.

Unpleasant skew

From a near-term perspective, my impression is that recent market action is very much in line with the “unpleasant skew” that one would expect from present conditions. On that basis, we should fully expect a tendency toward small but persistent marginal new highs – including points where the market retreats somewhat and then spikes back up to a marginally higher level. Absent a material improvement in market internals and credit spreads, however, that tendency is also likely to be accompanied by an abrupt vertical drop that wipes out weeks or months of market gains within a handful of sessions. It would be nice to be able to narrow down the window for that event, but that research question has always been difficult to answer. The best we can say is that going into every session here, the probability of an advance is greater than 50%, but the expected return is significantly negative. Numerous small gains, more than offset by a handful of wicked losses. That’s what I mean by unpleasant skew.

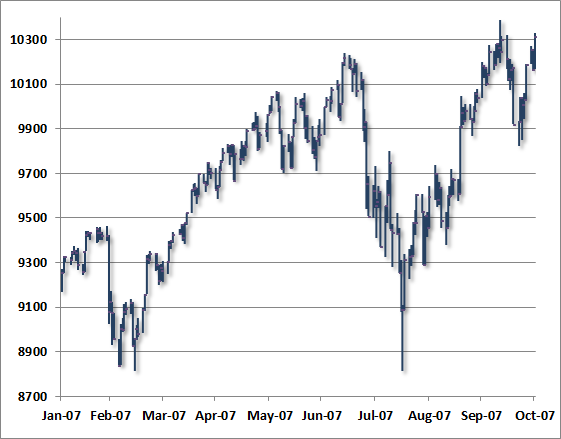

Valuations remain obscene from a historical perspective, bullish sentiment is lopsided (52.5% bulls to 15.8% bears according to Investors Intelligence), and we observe severely overbought conditions at record highs. Moreover, credit spreads have normalized only slightly, and internals have not improved enough to signal a shift from the risk-aversion that emerged a few months ago. Indeed, the day-to-day action of the broad market here looks quite a bit like the topping process that the market experienced in 2007. The chart below shows the peaking process of the New York Stock Exchange Composite Index during 2007. Note the initial selloff as market internals broke down in July of that year. See Market Internals Go Negative for my comments at the time. That initial selloff was followed by a full recovery and a persistent series of marginal new highs, a smaller selloff, and then another push higher before the market eventually rolled into a major collapse.

In hindsight, we remember the endless second-guessing that accompanied that peaking process in the face of overvalued, overbought, overbullish conditions, widening credit spreads, and deteriorating market internals that had yet to fully assert themselves. Our concerns about cyclically-elevated profit margins understating valuations were dismissed, as they are today. The common theme at the time focused on the market’s “resilence,” and the confidence that credit problems were “contained” – particularly as the FOMC had already shifted to aggressively cutting the fed funds rate.

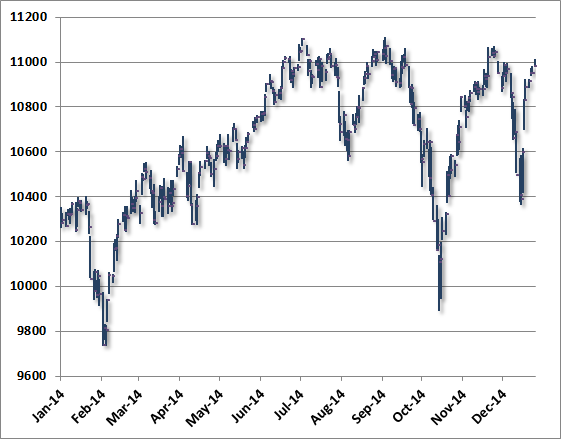

The recent chart below shows a similar dynamic in the broad market as measured by the NYSE Composite, which has largely stagnated over the past two quarters, but with a similar profile of churning and unpleasant skew that we saw in 2007 after internals had deteriorated. Of course, any resemblance to prior outcomes doesn’t ensure a similar outcome in the future. Still, it is challenging to find much but air-pockets, free-falls and crashes in the historical record once extremely overvalued, overbought, overbullish conditions are joined by deteriorating market internals or widening credit spreads.

In my view, we've gone through an extended period of yield-seeking speculation that has encouraged the issuance of a mountain of low-quality securities to finance reckless malinvestment. In the present cycle, junk debt and covenant lite leveraged loans are the primary vehicles for garbage, but debt-financed stock repurchases (and don't believe they aren't debt-financed) are a close third. We've seen other sorry versions of this story before. We know better how to navigate the bubble portion with adequate safety nets if it continues (which we doubt it will for long), but we also know that the cycle will ultimately end in tears for the average investor. Forget the lesson three times (1929, 2000, 2007), learn it four times.

A few final remarks as we look ahead to 2015. One of the things that should be clear from our experience of recent years is that I discuss and address challenges very openly, and I'm my own harshest critic. So I'll say again that I believe we completed our difficult transition in June. What we've seen then in market action is a deterioration in market internals consistent with a peaking process, but that in any case has made the market more vulnerable to air pockets recently.

It may be imperceptible that we are doing anything differently, or that we have addressed anything at all. It may take even more time for that to become clear. But again, I am convinced that the distinctions and hard-won lessons I've repeatedly articulated in recent months matter, because we can demonstrate their effect across a century of market cycles. Equally important, we don't rely on a collapse or dread a continued bubble. I believe what we need most is patient discipline.

Again, a firming in broad market internals and a return to narrow credit spreads would convey a signal that investors had at least temporarily shifted back to risk-seeking behavior. That wouldn’t ease our concerns about the level of valuations or remove the need for a safety net, but it would defer our concerns about immediate consequences. We’re going to take our evidence as it comes. My hope is that it is clear exactly how and when we addressed the challenges that made the recent half-cycle such a difficult transition. There are useful lessons here that I expect will help investors to avoid outcomes like the market experienced in 2000-2002 and 2007-2009, while still leaning to a constructive investment stance in the majority of market periods when extreme valuations, widening credit spreads, and breakdowns in market internals have typically not been joined as dangerously as they are today.

To look at the past 14 years and draw the lesson that rich valuations can be ignored (even when market internals and credit spreads are deteriorating), that hedging is a fool’s game, and that Fed easing can be relied on to drive stock prices higher, is to forget the principal lessons from the most severe market losses that the equity market has endured throughout history. What repeatedly distinguishes bubbles from the crashes is the pairing of severely overvalued, overbought, overbullish conditions with a subtle but measurable deterioration in market internals or credit spreads that conveys a shift from risk-seeking to risk-aversion.

As for monetary policy, remember that the Fed did not tighten in 1929, but instead began cutting interest rates on February 11, 1930 – nearly two and a half years before the market bottomed. The Fed cut rates on January 3, 2001 just as a two-year bear market collapse was starting, and kept cutting all the way down. The Fed cut the federal funds rate on September 18, 2007 – several weeks before the top of the market, and kept cutting all the way down. Many of the distinctions that investors believe are important are actually useless in avoiding steep market losses, and many of the distinctions that investors are ignoring at present are absolutely critical.

So for those who value and rely on our work, know that I do see the challenging transition of recent years as fully addressed, as the adaptations we’ve made are robust to data from every market cycle we’ve observed across a century of history. We’ve got much to show for our efforts in recent years. I expect that it will be great fun, once again, to demonstrate it all in practice, as we did in the years prior to 2009 (and with any luck, even more clearly).

As always, thank you for your trust. Wishing you a peaceful, joyful new year.

The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds.

---

Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website.

Estimates of prospective return and risk for equities, bonds, and other financial markets are forward-looking statements based the analysis and reasonable beliefs of Hussman Strategic Advisors. They are not a guarantee of future performance, and are not indicative of the prospective returns of any of the Hussman Funds. Actual returns may differ substantially from the estimates provided. Estimates of prospective long-term returns for the S&P 500 reflect our standard valuation methodology, focusing on the relationship between current market prices and earnings, dividends and other fundamentals, adjusted for variability over the economic cycle (see for example Investment, Speculation, Valuation, and Tinker Bell, The Likely Range of Market Returns in the Coming Decade and Valuing the S&P 500 Using Forward Operating Earnings ).

© Hussman Funds