“Remember how these things unwound after 1929 (even before the add-on policy mistakes that created the Depression), 1972, 1987, 2000 and 2007 – all market peaks that uniquely shared the same extreme overvalued, overbought, overbullish syndromes that have been sustained even longer in the present half-cycle. These speculative episodes don’t unwind slowly once risk perceptions change. The shift in risk perceptions is often accompanied by deteriorating market internals and widening credit spreads slightly before the major indices are in full retreat, but not always.”

Yes, This is an Equity Bubble, Hussman Weekly Market Comment, July 2014

“Normally, market internals deteriorate in a way that provides more time to establish a defensive position – market breadth lags, divergences develop across various industries and security types, price/volume action shows signs of distribution and so forth. The overvalued, overbought, overbullish syndrome may present none of those warnings, particularly when there is even modest upward movement in Treasury yields.

“So while I recognize that my insistence on defensiveness may appear to be interminably stubborn and at odds with ‘obvious’ trends, it is precisely the apparent obviousness of those trends that contributes to my uneasiness. At the late 1972 – early 1973 peak market listed above, Barron's annual investment ‘roundtable’ was accompanied by the title ‘Not a Bear Among Them.’ It's notable that the latest roundtable just published by Barron's reflects an identical uniformity of optimism.”

Hazardous Ovoboby! Hussman Weekly Market Comment, January 2007

“Abrupt market weakness is generally the result of low risk premiums being pressed higher. There need not be any collapse in earnings for a deep market decline to occur. The stock market dropped by half in 1973-74 even while S&P 500 earnings grew by over 50%. The 1987 crash was associated with no loss in earnings. Fundamentals don't have to change overnight. There is in fact zero correlation between year-over-year changes in earnings and year-over-year changes in the S&P 500. Rather, low and expanding risk premiums are at the root of nearly every abrupt market loss. One of the best indications of the speculative willingness of investors is the ‘uniformity’ of positive market action across a broad range of internals. Probably the most important aspect of last week's decline was the decisive negative shift in these measures.”

Market Internals Go Negative, Hussman Weekly Market Comment, July 2007

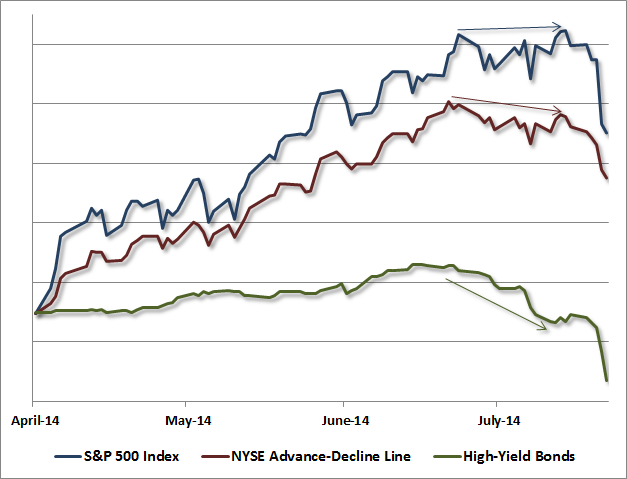

Historically-informed investors are being given a hint of advance warning here, in the form of a strenuously overvalued market that now demonstrates a clear breakdown in internals. We observe these breakdowns in the form of surging credit spreads (junk bond yields versus Treasury yields of similar maturity), weakness in small capitalization stocks, and other measures. These divergences have actually been building for months, but rather quietly. Note, for example, that as the S&P 500 pushed to new highs in recent weeks, cumulative advances less declines among NYSE stocks failed to confirm those highs, while junk bond prices were already deteriorating. We don’t take any single divergence as serious in itself, but the accumulation of divergences in recent weeks should not be ignored. Notably, the majority of NYSE stocks are now below their respective 200-day moving averages (which again, isn’t serious in itself, but feeds into a larger syndrome of internal breakdowns in a market that remains strenuously overvalued).

In the late-1990’s and during the 2000-2002 market plunge, we generally referred to the presence or lack of internal divergences with the phrase “trend uniformity.” In that cycle, those measures actually shifted negative just as the S&P 500 itself was peaking (see my September 4, 2000 market comment). As I observed in 2001, “It is crucial to understand that trend uniformity is not based on the extent or duration of a market advance. Rather, trend uniformity measures the quality of an advance. Without disclosing anything proprietary, trend uniformity considers the market action of a wide range of market internals, industry groups, and security types. Most legitimate and sustained bull moves very quickly generate trend uniformity, which I interpret as a signal that investors have developed a robust preference for taking risk. Some advances never generate this, as we saw between March and May this year. Those rallies are suspect, because there is a skittishness underlying them. When you have unfavorable trend uniformity in an overvalued market, the situation is very vulnerable because there is no natural floor to support prices.”

The worst market return/risk profiles we estimate are associated with an early deterioration in market internals following severely overvalued, overbought, overbullish conditions. This is what we observe at present. In contrast, the strongest market return/risk profiles we estimate are associated with a material retreat in valuations coupled with early improvement in market internals. I have every expectation that we will observe this combination over the completion of the present market cycle. So I expect that, perhaps to the surprise of many who don’t understand this approach, we will be quite bullish and aggressively invested as market conditions shift over the completion of the present market cycle. But now is emphatically not that time.

A reminder - much of our stress-testing following the expected collapse of the market in 2008 was related to those measures of “early improvement” in market action. Both Depression-era data and the credit crisis required broader and more robust measures than were typically required in post-war data (it’s instructive to review how we walked into that challenge in late-2008 after the market plunged and we made an initial constructive shift – see Why Warren Buffett is Right and Why Nobody Cares). There’s no question that my stress-testing decision in 2009 set off a very challenging experience in recent years, both because of our 2009-early 2010 miss in the interim of that stress testing, and also because extreme overvalued, overbought, overbullish syndromes have persisted much longer, without resolution, in the present cycle than they have historically. We’ve addressed those challenges, but without a time-machine we can only demonstrate that going forward. Meanwhile, our valuation measures have been consistently reliable for a century with respect to 10-year and full-cycle market returns, and they have not missed a beat even in recent cycles. Don’t make the mistake of believing that our valuation concerns today can be dismissed on the basis of that stress-testing miss.

The key point is this: after an extended and extreme compression of risk premiums, we’re now observing increasing divergences across a variety of market internals and security types (e.g. breadth, leadership, momentum stocks, small caps, junk bonds). We’ve come to avoid pointed warnings in this market, because speculative conditions have extended much longer than in other cycles. Indeed, we’ve had a few deteriorations in recent years that reversed fairly quickly as investors shifted back to risk-seeking, particularly after fresh initiatives or assurances about monetary easing (though further initiatives may not be forthcoming in this instance). So we're open to a favorable shift on these measures, and if that was to occur following a somewhat greater retreat in valuations, it could even open up some amount of constructive opportunity. Meanwhile, despite our view of stocks as severely overvalued, our response is to remain defensive without taking a stance that greatly relies on immediate market weakness.

An awareness of divergence and uniformity is the bread-and-butter of signal extraction – inferring true information signals from the sea of random noise. We take the present breakdown of market internals seriously. Whatever the crowd wishes to do about it, historically-minded investors should think carefully about whether a strenuously overvalued market with deteriorating market internals is a desirable environment for risk taking. For our part, the answer is a resounding “No.”