Before the current yield-seeking bubble implodes, I expect, in the same manner as every prior speculative episode across history, it’s worth examining the key conceit of the central bankers that produced it. The misconception is straightforward, and is the same notion that ultimately produced the yield-seeking mortgage bubble that imploded into a global financial crisis less than a decade ago. It is the false belief that “wealth” is embodied in the price of an asset, rather than the stream of cash flows it delivers over time. That belief is quietly reflected in every reference by central bankers to “wealth effects.” It is equally reflected in memory-impaired statements suggesting that, in response to recovering home prices, families should begin extracting some of that “wealth” as a way to finance more spending.

I use the word “conceit” for these views because they are more than just ideas. Rather, they reflect a self-congratulatory delusion that by distorting asset markets, central bankers themselves can be credited for having created “wealth” for their nation.

The problem is this. While encouraging yield-seeking speculation may boost the paper price of an asset, the only way to “capture” that gain is to sell the same overvalued asset to someone else. The elevated price does not reflect wealth creation, but merely creates the opportunity to obtain a wealth transfer from some poor soul who will end up holding the bag. Over time, the only true “wealth” embodied in the asset is realized via the long-term stream of payments that the security delivers into the hands of successive holders.

Those cash flows themselves must come from somewhere. Indeed, from the standpoint of the full economic equilibrium, we can go even further in describing what actually constitutes “wealth.” As I detailed in Stock-Flow Accounting and the Coming $10 Trillion Loss in Paper Wealth:

“When one nets out all the assets and liabilities in the economy, the only thing that is left - the true basis of a society’s net worth - is the stock of real investment that it has accumulated as a result of prior saving, and its unused endowment of resources. Everything else cancels out because every security represents an asset of the holder and a liability of the issuer. Conceptualizing ‘saved or unconsumed resources’ as broadly as possible, the wealth of a nation consists of its stock of real private investment (e.g. housing, capital goods, factories), real public investment (e.g. infrastructure), intangible intellectual capital (e.g. education, inventions, organizational knowledge and systems), and its endowment of basic resources such as land, energy, and water. In an open economy, one would include the net claims on foreigners (negative, in the U.S. case). Understand that securities are not net economic wealth. They are a claim of one party in the economy - by virtue of past saving - on the future output produced by others.”

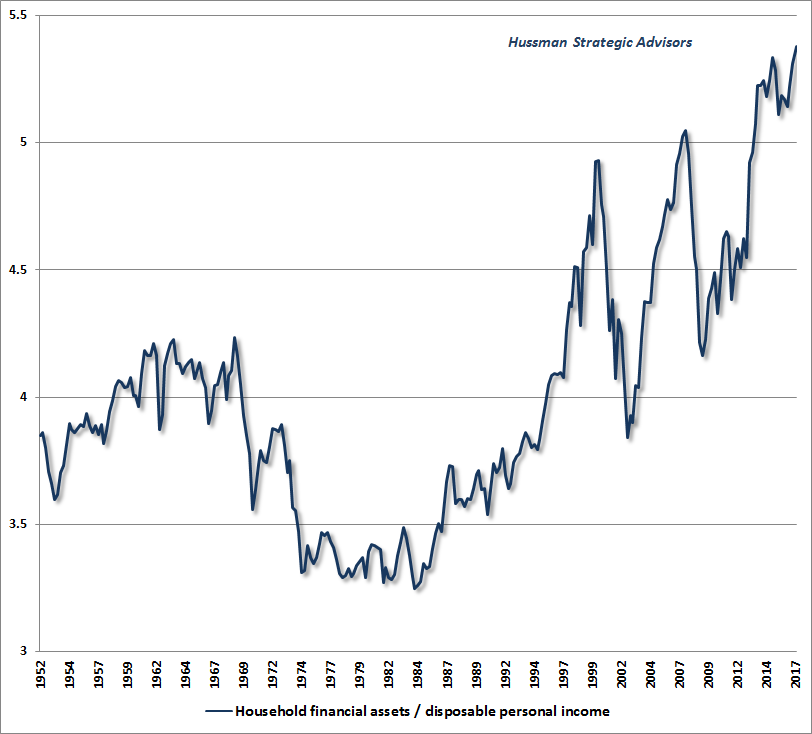

To illustrate the scope of central bankers' conceit in this speculative episode, the chart below shows household financial assets as a ratio of household disposable income. Certainly, the immediate impression is that households have never been as “wealthy” as they are today. So take in this chart for a moment, but hold on for the one that follows next.

One of the features of the foregoing chart that might create a reason for pause is the collapse in the ratio of household financial assets to disposable income during 2000-2002 and 2007-2009. Somehow, the asset valuations don’t seem to be as durable as one might wish, and indeed, we can show that this is the case. High valuations are simply followed by correspondingly weak subsequent returns.

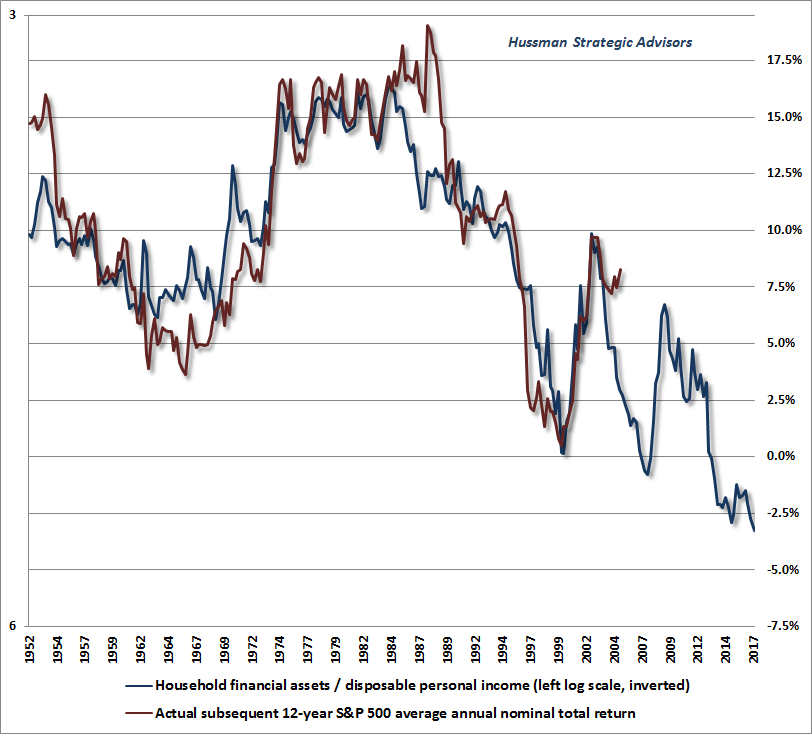

Below, the blue line shows the ratio of household financial assets to disposable personal income on an inverted log scale; that is, lower levels on the blue line represent more extreme levels of asset valuation. The red line shows the actual subsequent average annual total return of the S&P 500 Index over the following 12-year period. The true consequence of elevating asset prices is simply to reduce the subsequent returns that investors actually achieve as the underlying cash flows are delivered. Central banks haven’t made investors wealthier (again, except for investors who sell at these obscene valuations and thereby obtain a wealth transfer from the ones who buy). No. Central banks have simply helped to pull future returns into current prices, leaving investors in aggregate with the prospect of zero or negative investment returns out to about 2029 (an expectation that is also supported by a range of other reliable measures).

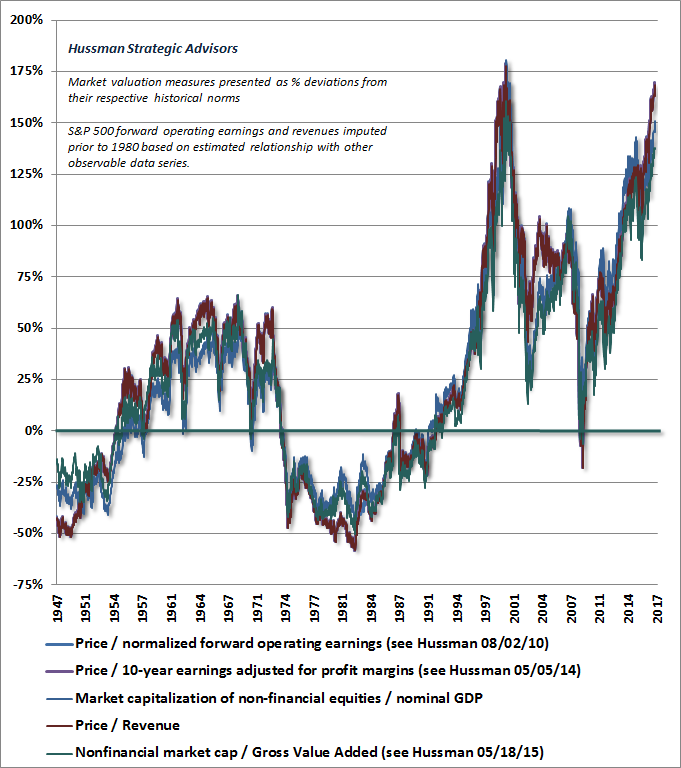

While the chart above adequately makes its point, I should note that the ratio of household financial assets to disposable income is an indirect measure of equity market valuation at best. The valuation metrics in the chart below are those we find best correlated with actual subsequent market returns across history. Each is presented as a percentage deviation from its own historic norm. Every market cycle in history has ended by drawing these measures toward or below those norms. At the recent market high, the consensus of these measures was consistent with estimated S&P 500 total returns of zero over the coming 12-year period, with an interim market loss on the order of -60% over the completion of the present market cycle. It’s also worth remembering that when interest rates are low because growth is also low, no valuation premium is “justified” at all. For more on this point, see Imaginary Growth Assumptions and the Steep Adjustment Ahead.

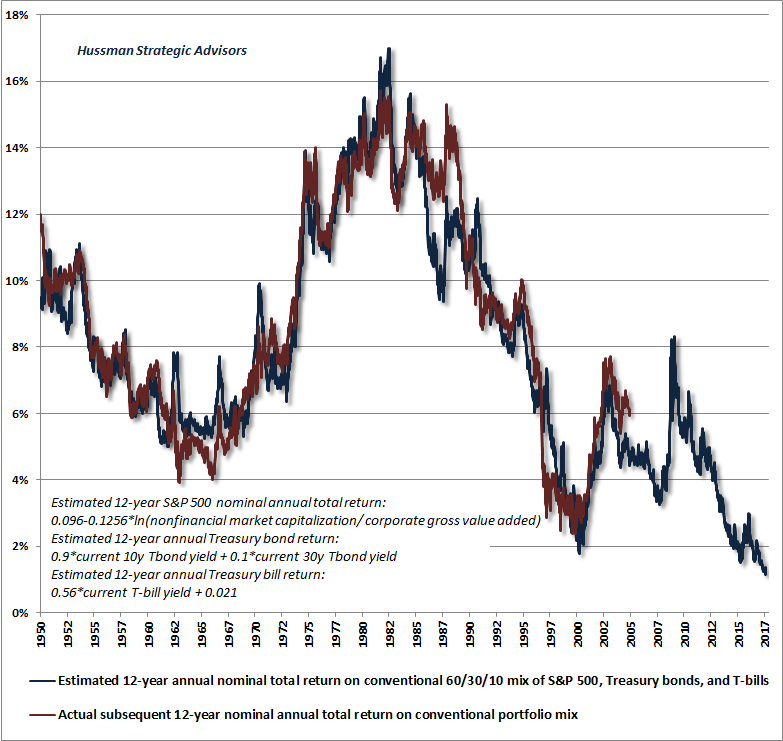

As for household financial assets as a whole, the following chart presents our estimates of 12-year total returns for a conventional portfolio invested 60% in the S&P 500, 30% in Treasury bonds, and 10% in Treasury bills. While the speculative distortion of the financial markets has encouraged a rush into passive investment strategies, it's worth remembering here that past returns appear most glorious at exactly the point that prospective future returns are most dismal. The coming years are likely to be a painful reeducation in that principle.

Valuations and full-cycle losses

I’ve regularly observed that while valuations often have little near-term impact on market outcomes over limited segments of the market cycle, they are extremely informative about investment returns over a 10-12 year horizon, and about the potential market losses that investors face over the completion of any given cycle. Let’s take a look at those prospective full-cycle losses.

In practice, the most reliable valuation measure we’ve studied, or in this case, introduced, is the ratio of nonfinancial market capitalization to corporate gross-value added (including estimated foreign revenues). Notably, however, the inclusion of estimated foreign revenues has much less impact than investors generally imagine, because their contribution has emerged over decades, not just over the past year or two. For a full discussion, see The New Era is an Old Story.

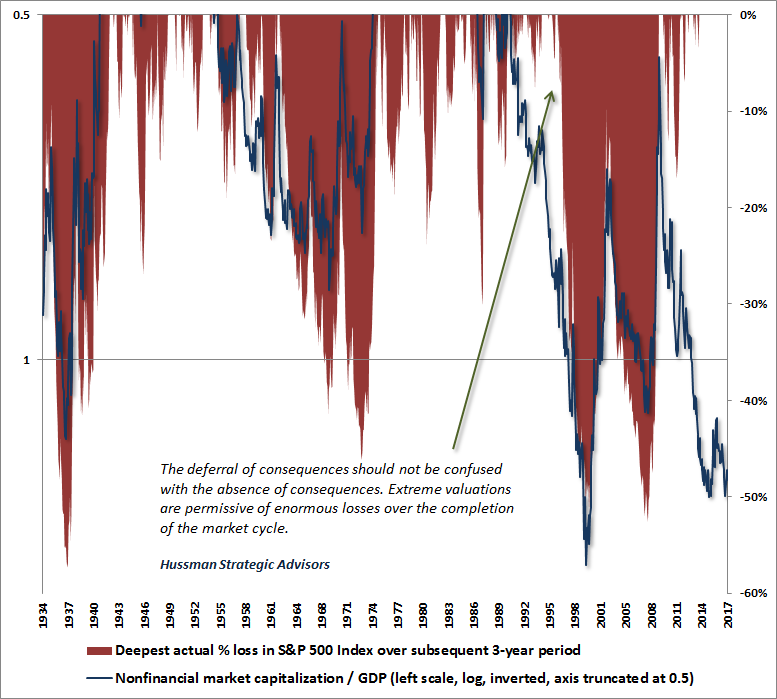

That said, the next most reliable measure (based on correlation with actual subsequent 10-12 year S&P 500 total returns across history) is the ratio of nonfinancial market capitalization to GDP, which has the benefit that it can be more easily estimated in pre-1947 data. To illustrate the relationship between valuations and downside risks over the completion of market cycles across history, MarketCap/GDP gives us a somewhat longer perspective. The following chart shows that measure in blue, on an inverted log left scale. But I’ve also truncated the horizontal axis at 0.5 (which is moderately below the historical norm). The red shaded area shows the deepest loss in the S&P 500 Index over the following 3-year period.

What this chart screams out to investors is that the level of overvaluation sets the likely expectation for market losses over the completion of a given cycle, but emphatically, investors should not confuse the deferral of consequences (e.g. the limited market losses in the period preceding the 2000 market peak) with the absence of consequences. Notice that many market cycles across history were completed with declines that were much worse than the blue outline below would imply, so a -50% market loss is a conservative estimate. As I’ve detailed in prior commentaries, our broader analysis puts our expectation for S&P 500 losses closer to -60%. Negative consequences were certainly deferred both during the tech bubble of the late-1990’s and again in recent years, but material losses, commensurate with peak market valuations, were never avoided in prior cycles. My impression is that future versions of this chart will require a great deal of red ink. Notice how swiftly that ink tends to run.

In short, the belief that Fed-induced speculation creates “wealth” is a conceit that rests on the delusion that “wealth” is embodied in the price of an asset, rather than the stream of cash flows it delivers over time. It is a dogmatic misconception of self-congratulatory central bankers that even the deepest economic downturn since the Great Depression was incapable of shaking. This lesson will be reiterated again, and again, until investors learn it, and until Congress properly restrains the Fed's wildly activist abandonment of systematic policy rules (remember also that the global financial crisis was the result, not the origin, of the Fed's activism). At present, we observe the combination of offensive overvaluation, the most extreme “overvalued, overbought, overbullish” syndromes we identify, and importantly, continued deterioration in market internals. In my estimation, and from any extensive evaluation of financial history, the delay of negative consequences has not eliminated them, but has instead made the likely eventual outcomes worse.

© Hussman Funds

© Hussman Funds

Read more commentaries by Hussman Funds