In recent quarters, I’ve remained adamant that the immediate first step of the Federal Reserve in normalizing monetary policy should have been to reduce the size of its balance sheet. The Fed’s failure to prioritize that first step, in the apparent desire to maintain an aggrandized role in the U.S. financial markets, has significantly increased the risk of a collapse from the speculative extremes the Fed has created in recent years. Given the increasing risk-aversion evident in market internals, we doubt that even a reversal of last week’s rate hike would materially reduce that prospect.

To see why, it’s important to understand how the Federal Reserve’s tools - open market purchases, interest on reserves, and reverse repurchases - actually work in affecting the economy and the behavior of speculative investors.

Let’s begin with open market operations. Traditionally, the Fed has used open market purchases of Treasury securities in order to affect short term interest rates. The Fed’s transactions don’t really accomplish this by directly pressuring market prices higher and lower. Instead, the Fed has traditionally determined the level of short-term interest rates by determining the quantity of zero-interest money that must be held across the economy as a whole.

Specifically, when the Fed goes out and buys a Treasury bond from the public, it pays for that bond in the form of currency and bank reserves (known as “base money” or “monetary base”). The bond becomes an asset on the Fed’s balance sheet, and the base money is a liability of the Fed. As a reminder that currency is a liability of the Fed, look at one of the pieces of paper in your wallet that reads “Federal Reserve Note.” The same is true for bank reserves. Bank reserves are deposits that banks have with the Federal Reserve. They are assets to the banks, and liabilities to the Fed.

In short, when the Fed makes open market purchases of government bonds, it takes those bonds on as assets, and creates new liabilities in the form of currency and bank reserves.

Once created, someone in the economy has to hold the existing quantity base money, at every moment in time, until it’s retired by the Federal Reserve. Someone with cash can certainly use it to buy stock, but the same cash then goes into the hands of the seller. So base money is always “cash on the sidelines” in the sense that someone gets stuck with it, like a hot potato changing hands. But it’s impossible for that cash to go “into” or “out of” the stock market. It merely goes through it.

Traditionally, currency and bank reserves have been zero-interest money. Of course, the more zero-interest money there is sloshing about in the economy, the more people that are uncomfortably holding those hot potatoes, and the more yield-seeking you’ll tend to see in securities that offer the hope for higher returns. The first stop, because it’s the closest to safe, liquid cash, is Treasury bills. Increase the amount of zero-interest money in the economy, and you’ll increase the number of investors who are willing to pay up for Treasury bills, so Treasury bill yields will fall. The “reach for yield” stops when the last “marginal” holder to get the hot potato is indifferent between ultra-liquid cash and near-liquid Treasury bills.

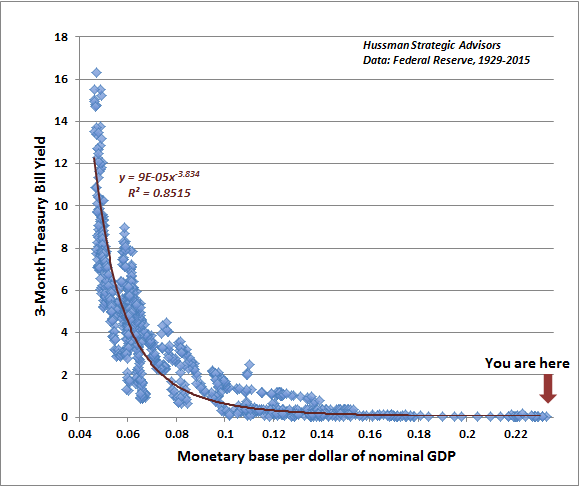

The chart below shows the relationship between the monetary base and Treasury bill yields in monthly data since 1929. The higher the quantity of zero-interest monetary base, as a fraction of GDP, the lower Treasury bill yields have fallen. It’s a rather pretty relationship, and it’s our version of what economists call the “liquidity preference curve.”

You can see the effect of quantitative easing above. At the point that the monetary base reached about 13% of nominal GDP in 2009 (about $2.3 trillion in base money), one would have correctly expected Treasury bill yields to fall to about 0.25%. As the Fed increased the monetary base further, to about 16% of nominal GDP in 2012 (passing $2.7 trillion), Treasury bill yields fell to about 0.10%. Over the past few years, the Fed has increased the size of its balance sheet even further, to $4.1 trillion and 23% of nominal GDP. As expected, Treasury bill yields have been driven to zero, but additional amounts of QE have had progressively smaller effects.

Notice the following: given $4.1 trillion in hot potatoes, the Federal Reserve could have reduced the size of its balance sheet by fully $1.3 trillion without pressuring Treasury bill yields up by even 10 basis points. The Fed could have done that as the first step toward normalizing policy, but perhaps thinking that the size of the Fed’s balance sheet itself somehow stimulates the economy, and perhaps wanting to maintain the Fed’s aggrandized role in the financial markets, the members of the FOMC decided not to do so. Remember this fact as you read on, because their refusal to take steps to systematically wind down the Fed’s bloated balance sheet before raising rates was a crucial mistake, in my view.

Reaching for yield

As the Fed drove the monetary base to the most extreme level in history, the “reach for yield” didn’t stop at Treasury bills. With over $4 trillion in hot potatoes steaming uncomfortably in the hands of investors, they reached for yield in riskier securities (just as similarly uncomfortable investors chased mortgage securities during the housing bubble). This drove up demand for junk debt, leveraged loans, and equities, all of which became the beneficiaries of reckless but ultimately temporary yield-seeking speculation. What makes this nearly beyond belief is that encouraging this yield-seeking speculation was one of Ben Bernanke’s intentional objectives. That’s not economics, it’s sociopathy.

A zero yield on risk-free securities makes investors blind. Reaching for higher yielding securities can seem like a good idea, but only as long as one ignores the prospect of capital losses that might wipe out the extra “pickup” in return. The same dynamic drove the housing bubble - mortgage securities seemed perfectly safe, but the extent of the speculation ultimately had disastrous consequences for the economy.

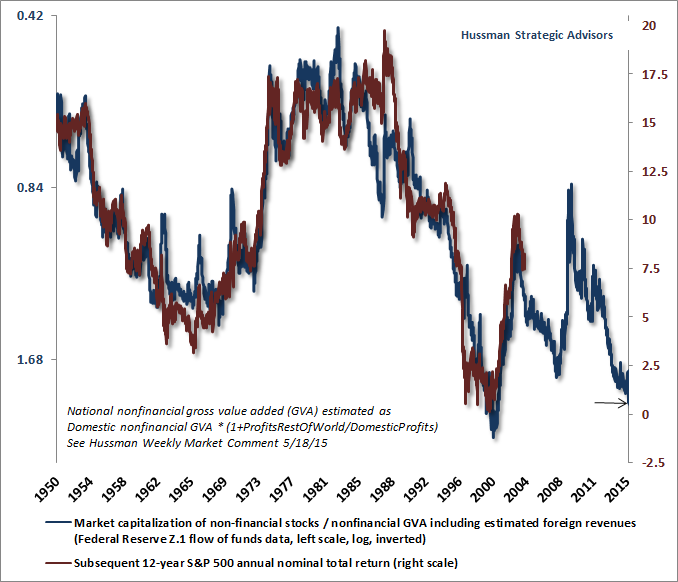

As a reminder of how extreme the latest episode of speculation has become in the U.S. stock market, the chart below shows the ratio of nonfinancial market capitalization to corporate gross value added on an inverted log scale (left, blue), along with the actual subsequent nominal annual total return of the S&P 500 over the following 12-year period (right, red). The correlation is about 93%, and currently indicates the likelihood of nearly zero total returns for the S&P 500 over this horizon (as was true coming off of the 2000 extreme).

The birth of interest on reserves

Prior to 2008, total reserves in the entire U.S. banking system amounted to only about $10 billion. When the reserves of a given bank fell below the required level, it had to go out and borrow excess reserves from another bank. The interest rate charged on those overnight loans is the called the “federal funds” rate. In an economy that’s now bloated with $2.6 trillion in reserves, over $2.4 trillion being excess reserves, this sort of inter-bank lending is hardly necessary, and is therefore practically non-existent, except for activity from government-sponsored enterprises (“GSEs” such as Fannie Mae and Freddie Mac) that are also allowed to trade on the federal funds market.

As Bernanke launched QE1 and the quantity of bank reserves skyrocketed in 2008, legislation was passed to allow the Federal Reserve to pay banks interest on their reserve balances. The idea was that by paying interest on reserves directly, the Fed could control the federal funds rate even if banks were awash in excess reserves. For example, no bank would have the incentive to lend money on the federal funds market at an interest rate below the interest rate that the Fed was paying on reserves (IOR) or on excess reserves (IOER). So in recent years, the Fed has been paying banks interest of 0.25% on trillions of idle reserves.

The Fed argues that since the Treasury securities it holds generate a higher average yield than 0.25%, this isn’t really a give-away to the banks. But wait - if the Fed has been paying 0.25% to banks all this time, why has the Fed Funds rate been nearly zero in recent years? The answer is that GSEs like Fannie Mae and Freddie Mac aren’t eligible for interest on reserves, but they can still trade in the federal funds market. Interest rates are determined by the marginal lender. Since the GSEs didn’t automatically earn interest on their excess cash, they were willing to accept an interest rate of only a few basis points on their overnight lending. So it didn’t matter that the banks were getting 0.25%. The Fed Funds rate still hovered near zero anyway.

This begs the question: Since the marginal lenders were getting zero, wouldn’t we have obtained the identical result even if we hadn’t paid the banks 0.25% on trillions of dollars of reserves? Wouldn’t over $6 billion annually have been returned to the Treasury for the benefit of U.S. citizens, rather than paying banks 0.25% on reserves for no reason? The answer is yes, but hey, who doesn’t want to subsidize banks? Total profits of the U.S. banking system have soared to a record $160 billion annually, so $6 billion is a drop in the bucket. Just look away.

Clinging to $4 trillion by explicitly paying every Joe in sight

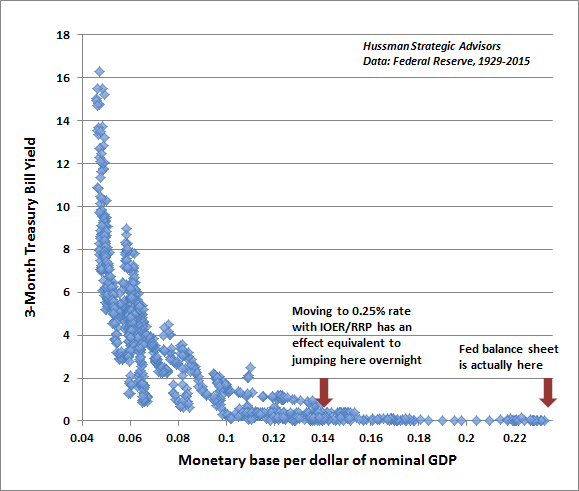

Last week, the Fed finally moved from the zero bound, pushing short-term interest rates, including the federal funds rate and the 3-month Treasury bill rate, to 0.25%. Now, traditionally, the way to accomplish this would be to shift the monetary base back to about 13-14% of nominal GDP. To get to short-term rates of 0.25% through market supply and demand, the Fed needed to roll about $1.7 trillion in Treasury securities off of its balance sheet as the bonds matured. We know from nearly a century of history that market interest rates would hardly have budged until the balance sheet was about $1.4 trillion smaller, so doing so would not have been disruptive to the credit markets. Instead, the Fed has insisted on continually reinvesting the proceeds of maturing holdings into new Treasury debt, holding its balance sheet near its peak, above $4 trillion.

So how will the Fed move the Federal Funds rate up to 0.25% with $4 trillion dollars of monetary base still outstanding? First, it announced that it would increase the amount of interest it pays to banks on $2.6 trillion of reserves, raising the rate to 0.50%. I know - the 0.50% doesn’t seem to make sense if the target fed funds rate is 0.25%, but all will be clear shortly. See, the second thing the Fed did was to vastly expand something called a “reverse repurchase” or RRP facility that will pay 0.25% to other institutions that also hold cash, but aren’t eligible to receive interest on reserves. These include the GSEs, foreign banks, and money market funds - what the Fed calls an expanded list of “counterparties.”

“Reverse repurchase”? OK, here’s what’s going on. The Federal Reserve Act allows the Fed to buy and sell Treasury securities on the open market. It doesn’t, however, authorize the Fed to go out and pay interest directly to money market funds and foreign banks. But since the Fed refuses to shrink its balance sheet, the only way to hit the 0.25% Fed Funds target is for the Fed to pay interest outright to every Joe who might otherwise lend U.S. dollars at a lower rate. Since the Fed can’t just pay interest to financial institutions that aren’t U.S. banks, it has to make the payment look like it’s a transaction involving a Treasury security.

To pull this off, the Fed has announced that it will open “reverse repurchases” to a whole new list of counterparties, limited only by the amount of Treasury securities it owns. A reverse repurchase goes like this: the Fed agrees to “sell” a Treasury bond to some money market fund today, and to buy it back tomorrow at exactly the same price, plus one day of interest at 0.25%. So the money market fund essentially gets “paid” 0.25% interest on its overnight “investment.”

The effect of it all is this. Rather than reducing the size of its balance sheet, the Federal Reserve has raised its target federal funds rate to 0.25%, to be accomplished with two tools. First, the Fed has raised the interest rate it pays banks on their idle reserves to 0.50%. Second, in order to keep GSEs, foreign banks, and money market funds from lending at a rate lower than 0.25%, the Fed has essentially removed the cap on its “reverse repo facility,” and will pay 0.25% on those RRPs.

Once again, this begs the question: Since the marginal lenders will now be getting 0.25% through the RRP facility, wouldn’t we obtain a 0.25% federal funds rate even if the Fed only paid the banks 0.25% on their excess reserves as well? Wouldn’t over $6 billion annually be returned to the Treasury for the benefit of U.S. citizens, rather than paying banks that additional 0.25% on reserves for no purpose? Once again, the answer is yes, but as the Grinch urged Cindy Lou Who - just take your cup of cold water and go back to bed dear... You didn’t see anything.

Remember that the total monetary base (currency plus bank reserves) amounts to over $4 trillion. About $2.6 trillion of these funds are reserves at U.S. banks that are now eligible for 0.5% interest. The other $1.4 trillion represents currency. So how much money is likely to earn 0.25% through the RRP facility? It depends, because the composition of the monetary base can shift from one category to another. Suppose that a money market fund has $20 million in assets that are currently held on deposit at a U.S. bank. That fund could enter an RRP and transfer the cash directly to the Fed, earning 0.25% on that money, while also reducing U.S. bank reserves by the same $20 million as that transfer of funds clears. As another example, a foreign bank might accumulate $10 million of U.S. currency as vault cash, and choose to earn interest on it through the RRP facility. Still, given how much of the monetary base is held as idle reserves in the U.S. banking system, my impression is that the actual amount going through the RRP facility is unlikely to exceed more than a few hundred billion unless there’s either a major shift from bank deposits to money market funds, or a major shift of currency into non-U.S. banks. We'll certainly see some assets shift from banks that choose not to raise their deposit rates, given that money market funds are eligible for RRPs.

So aside from currency that’s literally in circulation, the Fed will now be paying interest on 1) reserves held directly with the Fed by U.S. banks, and 2) U.S. dollars “lent” to the Fed through the RRP facility by counterparties such as foreign banks and money market funds eligible for 0.25% interest. Again, while the relative amounts of each may change over time, the total amount of money eligible for interest payments should never exceed the total amount of monetary base (and would only equal that amount if all currency in circulation was held by eligible institutions). If the total amount did exceed the monetary base, it would be a sign that non-cleared funds were being improperly pledged through the RRP facility.

Reversing the speculative effect of QE overnight

In 2009, as the Federal Reserve raised the monetary base to about $2.3 trillion (13% of nominal GDP), short-term interest rates predictably fell to 0.25%, as one would have expected based on nearly a century of evidence tightly linking the level of short-term interest rates to the amount of base money as a fraction of GDP. Though 0.25% was quite a low level of interest, it was still enough to make the marginal holder of zero-interest money indifferent between holding that money and chasing yield in Treasury bills. The quantity of zero-interest liquidity in the economy drives the level of short-term interest rates and the pace of yield-seeking speculation. As the amount of zero-interest liquidity increases, investors chase market interest rates such as Treasury bill yields toward zero, and speculate in risker assets as well.

Since 2009, the repeated episodes of quantitative easing by the Federal Reserve have driven short term interest rates from 0.25% all the way to zero by creating an additional $1.7 trillion in monetary base (currency and bank reserves). This raised the total amount of zero-interest hot potatoes flooding the financial markets to over $4 trillion. The discomfort of holding that much zero-interestmoney helped to encourage the third speculative bubble since 2000, featuring the highest median equity valuations in history (the second-highest on reliable capitalization-based measures), along with heavy issuance of junk and covenant-lite debt.

Understand that QE only “worked” to encourage speculation by creating a pool of over $4 trillion of zero-interest assets that someone had to hold at every point in time, in a market environment where investors were inclined to seek risk (which is most reliably inferred from the uniformity of market internals across a broad range of individual stocks, industries, sectors, and asset classes, including debt securities of varying creditworthiness). Zero interest rates also infected the entire stock of Treasury bills with maturities of 3 months or less, creating the sense among investors that they were “forced” to take risk in more speculative securities.

As a side note, the incremental effect of additional QE became weaker once market interest rates hit zero, because at that point, additional Fed liquidity yielding nothing to investors became indistinguishable from Treasury bills yielding nothing to investors. In other words, once market interest rates hit zero, the extra $1.4 trillion dollars in QE that followed was no different than if the Treasury had decided to fund an extra $1.4 trillion of the $18 trillion U.S. debt using zero-yielding T-bills instead of low-yielding Treasury notes.

Last week, without taking any care to reduce the size of its balance sheet, the Federal Reserve instantly changed the monetary environment to one that is observationally equivalent to the one that prevailed in 2009. By raising interest rates artificially (through interest payments on reserves and reverse repurchases) and applying those payments to everything but currency in circulation, the Fed has neutralized the misguided speculative prop it created through 6 years of policy distortion, and it did so in one fell swoop. That prop was the presence of $4 trillion in zero-interest money, plus zero yields on the entire outstanding stock of Treasury bills with maturities of 3 months or less. In the blink of an eye, short-term market rates and fed funds are back to 0.25% as they were in 2009, and the remaining stock of zero-interest hot potatoes has suddenly contracted below the 2009 level of $2.3 trillion because total U.S. bank reserves are eligible to earn interest, and even base money outside the U.S. banking system is eligible for 0.25% interest via RRPs.

From the standpoint of investors, the overall effect is just as if the Fed had suddenly reversed every dollar of quantitative easing since 2009 ($1.7 trillion). That statement may seem preposterous, but what other function was there for trillions of dollars of idle zero-interest assets, compared with the 0.25% world that existed in 2009, except to create perpetual distress for the holders, and force them to decide that speculation was their only alternative? Undoubtedly, even a 0.25% yield would still encourage speculation if investors were predisposed to seek risk here (market internals suggest they presently are not), but in any event, it's nothing like the speculative pressure that existed only a week ago.

The central point is this. From 2009 to 2015, sequential rounds of quantitative easing took the financial system from 0.25% market interest rates and $2.3 trillion in zero-interest assets to a world of 0% market interest rates and over $4 trillion of zero-interest Fed assets, plus trillions more in zero-interest Treasury bills and money market fund assets. This created a massive pool of zero-interest hot potatoes that fueled yield-seeking speculation. But because the liquidity preference curve is so flat at the zero bound, increasing the yield on short-term liquidity to even 0.25%, while dramatically reducing the quantity of zero-interest assets outstanding (as the Fed effectively did last week) reverses the speculative effect of QE back to 2009 levels. My impression is that one doesn’t want to be holding a significant position in risk-assets when investors figure out what just happened.

In my view, the proper order of policy normalization should have started by gradually running down the size of the Fed’s balance sheet. Inexplicably, the Fed seems to believe that raising market interest rates to 0.25% by directly paying interest to every Joe in sight is materially different from a world where investors instead simply hold Treasury bills yielding 0.25%. But consider a quick thought experiment. Suppose that the Fed was to immediately contract its balance sheet by $1.7 trillion, reducing the amount of Fed-created liquidity, and instead placed $1.7 trillion more Treasury bills into the hands of the public, yielding the same 0.25%. From the standpoint of the public and the financial markets, nothing would change, except that $1.7 trillion of 0.25% base money sitting idle in the financial system would now instead be held by the public in the form of T-bills with the same yield.

In recent years, the Fed’s reckless expansion of zero-interest liquidity encouraged so much yield-seeking speculation that the prospective 10-12 year total return of the S&P 500 was also driven to zero, along with the prospective return of junk debt, where risk premiums were compressed to razor-thin levels. The true policy error of the Fed was that it embarked on years of financial market distortion in the first place. The arrogant refusal to shrink the balance sheet before raising rates was simply a continuation of that misguided thinking.

Moreover, with reliable valuation measures at obscene levels, with weak market internals already signaling increasing risk aversion among investors, and with the most reliable early-warning measures suggesting an increased likelihood of a new recession, a reversal of last week’s move would only signal panic, confusion, and a lack of credibility at the Fed. Our outlook was hard-negative even before last week’s policy shift, because in an environment of rich valuations and increasing risk aversion, even easy Fed policy doesn’t support stocks, because safe-low interest liquidity is viewed as a desirable asset, not an inferior one, under those conditions.

All of this said, we would significantly reel back our hard-negative outlook (probably at least to a neutral one) if market internals were to improve on our measures, even given current valuations and economic data. Here and now, however, we don’t believe that investors should rule out the potential for steep market losses in equities, low-grade debt, and other risk-sensitive assets that have been the beneficiaries of yield-seeking speculation in recent years.