Here's the situation. Even if the Fed reduces the pace of quantitative easing, there is virtually no chance that short-term interest rates will be raised in the foreseeable future. As I observed last week, "Investors who believe that 'QE makes stocks go up' – with no other condition required – just got a handwritten, perfumed note from Bernanke to keep buying. The fact that we are instead seeing broad internal deterioration here is of some concern, because it smacks of something more afoot. It might be the increasing credit strains in China. It may be growing expectations for disappointing earnings preannouncements. It may be economic weakness that finally catches up to the general (though not uniform) deterioration that we’ve seen across leading measures of economic activity. My own litany of concerns is well-known (seeClosing Arguments – Nothing Further, Your Honor). But whatever the reason, investors appear to be shifting from risk-seeking to risk-aversion."

Market internals remain broken here. That may change, and it might even change soon. Until it does, we would be inclined to tread carefully, because this may be the highest level investors will see on the S&P 500 for quite some time. Choosing between potential catalysts - credit strains in China, the risk of disappointing earnings, or economic weakness, the incoming data is consistent with one conclusion: all of the above.

On the economic front, I noted last month that broad coincident and leading measures of economic activity continue to slump (employment is decidedly a lagging economic indicator), with the main bright spot being a jump in the Chicago Purchasing Managers Index that diverged significantly from other measures. As I noted at the time (seeFollowing The Fed to 50% Flops), “When we plot ‘outliers’ (where the Chicago PMI deviates from the average of the other surveys), against subsequent changes in the Chicago PMI, what results is a clearly downward-sloping scatter, meaning that positive outliers, as we presently observe, are typically corrected by subsequent disappointments in the Chicago PMI. Conversely, however, outliers in the Chicago PMI are typically not related to subsequent positive surprises in the other indices.”

On Friday, the June Chicago PMI was reported. Reversing the May surge from 49.0 to 58.7, the index dropped back to 51.6. This was the largest monthly drop in four years. Both production and new orders declined, and order backlogs slipped into the deepest contraction since September 2009.

Based on a broad range of measures, economic activity continues to waver in a narrow band that has historically marked the border between expansion and recession. While quantitative easing has produced enormous financial distortion and very little growth, it has been successful – at least in fits and starts – in kicking the economic can along this band for a few months at a time. Historically, recessions have usually followed deterioration to this band fairly quickly. The QE-induced delay in the present cycle has put a temporary cloud over economists like Lakshman Achuthan atECRIand I, despite accurately warning of the2000-2001and2007-2008recessions.

It’s probably needless to say that I continue to view recession risk as palpable. Still, our concerns about the equity market are not driven by that consideration. Instead, we’re concerned about a host of reliable, testable, historically validated measures that – in combination – are associated with a dismal estimate of prospective return/risk here. This combination of measures will change over time, and as it does – in proportion to the change in those return/risk estimates – so too will our investment outlook. Presently, we are hard-defensive.

While emphasizing that our position is driven by observable measures that might be different even a week from now, if I was to venture a guess, that guess would be that the completion of the present half-finished market cycle will include a blindside recession and a plunge in earnings that will somehow come as an enormous “surprise” to investors. As the cycle completes, I would expect it to wipe out all of the market’s gains since at least 2010. Note that even a run-of-the-mill bear market decline would also put the S&P 500 behind Treasury bills for the entire span since about 1997, without even getting close to valuations that have typically existed at the beginning of secular bull markets (on measures that have the most reliable relationship with subsequent long-term returns). History is awfully unkind to the idea that even half of the gains from a bull market are actually retained by investors over the completion of the market cycle.

I’ll note in passing that both the 2001 and 2008 recessions began with a slight negative quarter for GDP growth, a positive quarter, and another negative quarter. In fact, the 2001 recession did not include two consecutive negative quarters at all (having long ago spent part of my doctoral studies at Stanford working with the Chair of the NBER Business Cycle Dating Committee, I can assure you that the NBER doesn’t use the journalistic myth of "two negative quarters" to date recessions). In a $16 trillion economy, fourth-quarter 2012 GDP was less than $16 billion from a negative print in real GDP. Meanwhile, real personal consumption in the second quarter (through May) is running at an annual rate of less than one-half of one percent, and industrial production has slipped since March. Europe remains in recession. China is facing credit strains following years of massive overinvestment in still-empty buildings. The first day of government furloughs was May 24, and the largest furlough in the Defense department doesn’t kick in until July 8, so it’s difficult to assess the impact of sequestration as yet. If the economy is not already in recession, we are clinging as close to a non-recession as any non-recession in post-war data.

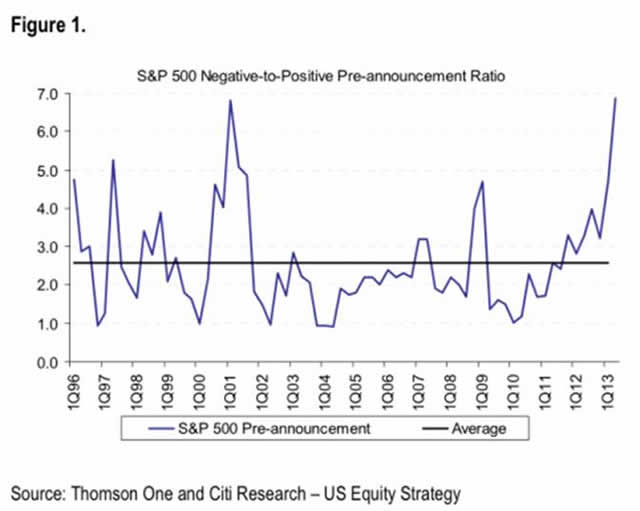

On the earnings front, profit margins have already peaked, and though S&P 500 earnings benefited from front-loading a year’s worth investment-tax incentives into the first quarter, profits economy-wide were actually down 1.4% in the first quarter GDP report. Margin pressure and slow revenue growth may make a mess of earnings in coming quarters. Last week, CITI reported that it was “shocked” by the surge in negative earnings preannouncements for the second quarter, now running 7-to-1 versus positive preannouncements.

What to watch, and in what order

One of the results of writing on a wide range of economic and financial topics is that investors sometimes assume that my market views are dependent on some particular data point or Fed decision. Current events are interesting in the sense that they can affect the various measures that we use to classify market conditions, but those measures are actually what matter most because they can be tested and validated across history. In a nutshell, here are some of the basic conditions that I believe are relevant for risk-taking in stocks, and the order in which I tend to consider them:

First, an overvalued, overbought, overbullish syndrome of conditions has historically trumped all other considerations – on average – particularly when yields are rising and price momentum has flattened. Market crashes are always driven by a spike in risk premiums from previously inadequate levels. Never forget that. When risk premiums are squeezed to deeply depressed levels (as QE has done) and upward pressures on those risk premiums then emerge, markets collapse.

Absent that syndrome, favorable market internals and trend-following conditions generally dominate other considerations. Valuations are the primary determinant of long-term returns, but over shorter horizons, valuations are essentially a “modifier” – meaning that the stocks typically enjoy the strongest gains of the market cycle when broad market action is positive and favorable valuations provide a tailwind.

The lesson from Depression-era data isn’t different in this regard. Rather, Depression-era data teaches that neither favorable trend-following measures (which were heavily whipsawed) nor favorable valuations were enough to avoid deep losses until they were confirmed by positive divergences in market internals and other measures. I think that’s probably what Jesse Livermore had in mind when he wrote “It isn’t as important to buy as cheap as possible as it is to buy at the right time.” Livermore also observed that his worst losses were the result of lapses in the discipline of investing “only when I was satisfied that precedents favoured my play.” Few things in finance are truly unprecedented – including the Depression and QE – once you quantify how they exert their influence on the variables that determine prices (cash flows, growth rates, risk-free discount rates and risk premiums).

In the absence of favorable market internals, easy monetary policy is far less helpful than investors believe. From an asset allocation perspective, even simple trend-following methods have performed far better than following monetary policy. QE has undoubtedly complicated the period since 2010, but a good part of that difficulty was actually during periods when market internals were favorable while an overvalued, overbought, overbullish syndrome was absent. Most of the remaining difficulty has been over the past year, as stocks have advanced despite a persistent overvalued, overbought, overbullish syndrome – contrary to average historical outcomes. Then again, I suspect that it will be striking how quickly those gains are surrendered if market internals remain broken.

What’s disturbing, if you actually examine the historical evidence, is that while favorable market action tends to be favorable regardless of the monetary policy stance, unfavorable market action coupled with easy money is actually more hostile than unfavorable market action coupled with tight money. As I noted inFollowing the Fed to 50% Flops, “Strikingly, the maximum drawdown of the S&P 500, confined to periods of favorable monetary conditions since 1940, would have been a 55% loss. This compares with a 33% loss during unfavorable monetary conditions. This is worth repeating – favorable monetary conditions were associated with far deeper drawdowns.”

I’ll end by repeating what I view as the most important risk at present. Hands-down, the worst-case scenario for investors is a market that comes off of a syndrome of overvalued, overbought, overbullish conditions and then breaks trend-support in the context of an economic downturn. Market crashes are always driven by a spike in risk premiums from previously inadequate levels, and that sequence of events would be the perfect storm.

Notes on fruitless monetary policy

The prospect of continued tepid economic growth, if not recession, might be taken as evidence that the Fed will not taper its program of quantitative easing anytime soon. I actually think this inference is incorrect. It’s important to distinguish between two policy responses – one being a reduction in the pace of new purchases of Treasury and agency securities by the Fed, and the other being actual sales to reduce the size of the Fed’s balance sheet. Based on the tight historical relationship between the monetary base (per dollar of nominal GDP) and short-term interest rates, we estimate that the Fed would have to actually reduce its balance sheet by over $400 billion simply to nudge short term interest rates up by 0.25%. This is nowhere in the Fed’s plans, and numerous statements from Fed governors have made that clear. The Fed has no plans – zero – to raise its policy rates in the foreseeable future. Accordingly, material reductions in the size of the Fed’s balance sheet are highly unlikely. Any economic weakness will push off the date of even the first tiny hike in short-term interest rates even further.

However, “tapering” really has nothing to do with raising interest rates. It simply implies a reduction in the pace of new purchases. As we’ll probably find in the minutes of the last Fed meeting, many members of the FOMC are increasingly concerned about the distortions created by QE, along with the fact that even the present near-frantic purchases are having diminishing effect. A reduction in the pace of purchases is long overdue absent a full-blown economic crisis. The Fed can and should be expected to reduce the pace of new purchases in the next few months. It may even stop new purchases sometime in 2014, though I doubt that will happen until Bernanke is gone.

On the inflation front, we’ve always argued that the price level is the ratio of two marginal utilities – the extra benefit people get from an additional unit of goods, divided by the extra benefit that people get from an additional unit of money. A unit of money throws off benefits by providing a store of value and a means of payment, and each successive holder gets a tiny bit of that benefit. The marginal utility of an additional unit of money is just the appropriately discounted sum of all of those tiny bits. Inflation actually reflects an increase in the marginal value of goods at a faster rate than the marginal value of money. Creating huge quantities of money when interest rates are near zero and where there is a great deal of economic slack is far less inflationary than creating the same quantity of money when interest rates are high and the economy faces supply constraints.

I doubt that QE will produce material inflation pressures in a weak, crisis-prone economy. Nor will it produce economic growth. It is simply fruitless policy that fails to address any economic constraint that is actually binding, and it insults the economy by encouraging the diversion of scarce savings to speculative and unproductive activities. To borrow a line from Keynes, “when the capital development of a country becomes a by-product of the activities of a casino, the job is likely to be ill-done.”

Larger inflationary risks will most likely be in the back half of this decade, after the next recession ends. The argument for reducing the pace of QE is not that it is creating inflation. Rather, pace of QE should be reduced because the risk of systemic disruption and financial distortion grows with every new purchase, along with the difficulty of eventually normalizing policy. Untethered inflation could certainly emerge if the present monetary policy stance was met with some kind of supply shock, but that would require an unexpected event that constrains output (like the OPEC shock or the strike of German workers in the Ruhr in the 1920’s).

The bottom line is this. Short-term interest rates will be pegged at zero for quite a long time, because raising them even slightly would require not just tapering, but a massive reduction in the Fed’s balance sheet. The securities that compete most closely with default-free short-term money is default-free long-term money, which is why I view Treasury bonds as increasingly compelling as interest rates rise, particularly in a tepid economy with no material inflation pressures. Security types that normally carry significant risk premiums (like stocks and corporate bonds) have already seen all of the likely benefits of QE, and any return to historically reasonable risk premiums is likely to batter these securities.

So while I view a reduction in the pace of the Federal Reserve’s quantitative easing purchases as likely in the months ahead, regardless of the course of the economy, an actual reduction in the amount of those holdings seems unlikely for years. As a result, short-term interest rates are likely to be pegged near zero for a very long time, and the lack of yield on short-term default-free investment options is likely to support demand for the most comparable default-free options – namely medium and long-term Treasury debt. I don’t believe that the same argument extends well to securities such as stocks or corporate bonds that have traditionally been priced to reflect significant risk premiums, and where we estimate present risk premiums to be extraordinarily thin.

In my view, much of the recent selling has been based on the idea that the 30-year secular bull market in bonds is over. The more relevant issue is that there are no material upward pressures on short-rates, inflation, or economic growth here, the difference in yield between 10-year Treasuries and 3-month Treasury bills is already greater than the long-term norm of 1.4%, and the potential for credit shocks remains material. In that environment, I believe the main consideration is to have the flexibility to extend durations on spikes in yields and reduce durations when yields are depressed.

For example, consider a 10-year Treasury bond with a face value of $100 and a coupon of 2.5%. If the yield-to-maturity remains at 2.5% for a year, the total return on that bond would be 2.5%. An increase in the yield to 3.0% over the course of a year would produce a capital loss, offset by interest income, for a total return of -1.4%. A decline in the yield to 2.0% over the course of a year would produce a total return of 6.58%. The corresponding figures for a 100 basis point increase and decrease in yield are -5.11% and 10.86% respectively. A lower coupon would widen that range of outcomes slightly, while a higher coupon would narrow it. Given that I view economic risk to be asymmetrically to the downside, I would not rule out those lower ranges for yield.

With regard to stocks, we're sometimes asked how the level of interest rates affects our estimates of 10-year prospective returns for the S&P 500. This is a little bit like asking, for example, how the yield on a 30-year Treasury affects the calcuation of the yield on a 10-year Treasury. It doesn't. Instead, the prospective returns on other securities come into play once the estimated return for stocks is in hand. At present, for example, we estimate a 10-year nominal total return for the S&P 500 over the coming decade of about 3.5% annually. It is only here, when this prospect is compared with the prospects for other securities, that interest rates come into the picture. The yield-to-maturity on a 10-year Treasury bond is about 2.5% (though with a small fraction of the volatility and drawdown risk). If both are appealing to you relative to other alternatives, considering all of the prospects and risks, then there's nothing wrong with holding both, and you might even say that stocks are "fairly valued" in your world. They're certainly overvalued in ours, because we view a 3.5% prospective return for stocks as both presently and historically inadequate given the risks and alternatives. Prices move inversely to expected returns. Since I expect the inadequate prospective returns of stocks to be drawn higher in the next 1-2 years, but bond yields to move sideways or be drawn lower, I view Treasuries as having a much better return/risk tradeoff on horizons shorter than 10 years.

Put another way, if you begin with the assumpton that given the level of interest rates, the 10-year prospective return on the S&P 500 should be 3.5%, then you could work backwards and get a "fair value" equal to the current price. For our part, we prefer to work directly with prospective returns and evaluate them side-by-side. Keep in mind, however, that comparing stock returns and bond returns is more like comparing apples and oranges than investors sometimes imagine. For example, earnings yields and stock yields were actually negatively correlated prior to about 1970 (even in post-war data) and have also been negatively correlated since the late-1990's (SeeInvestment, Speculation, Valuation and Tinker Bellfor more).

Last week, the Bank for International Settlements – essentially the central bank of central banks – made the following observations in itsAnnual Report. They are the most concise evaluation of Fed policy I’ve seen. A few excerpts:

“Originally forged as a description of central bank actions to prevent financial collapse, the phrase ‘whatever it takes’ has become a rallying cry for central banks to continue their extraordinary actions. But we are past the height of the crisis, and the goal of policy has changed – to return still-sluggish economies to strong and sustainable growth. Can central banks now really do ‘whatever it takes’ to achieve that goal? As each day goes by, it seems less and less likely. Central banks cannot repair the balance sheets of households and financial institutions. Central banks cannot ensure the sustainability of fiscal finances. And, most of all, central banks cannot enact the structural economic and financial reforms needed to return economies to the real growth paths authorities and their publics both want and expect.

“What central bank accommodation has done during the recovery is to borrow time – time for balance sheet repair, time for fiscal consolidation, and time for reforms to restore productivity growth. But the time has not been well used, as continued low interest rates and unconventional policies have made it easy for the private sector to postpone deleveraging, easy for the government to finance deficits, and easy for the authorities to delay needed reforms in the real economy and in the financial system. After all, cheap money makes it easier to borrow than to save, easier to spend than to tax, easier to remain the same than to change.

“Alas, central banks cannot do more without compounding the risks they have already created. Instead, they must re-emphasise their traditional focus – albeit expanded to include financial stability – and thereby encourage needed adjustments rather than retard them with near-zero interest rates and purchases of ever larger quantities of government securities. And they must urge authorities to speed up reforms in labour and product markets, reforms that will enhance productivity and encourage employment growth rather than provide the false comfort that it will be easier later.”

© Hussman Funds