In economics, we often describe “equilibrium” as a condition where demand is equal to supply. Textbooks usually depict this as a single point where a demand curve and a supply curve intersect, and all is right with the world.

In reality, we know that economies often face a whole range of possible equilibria. One can imagine “low level” equilibria where producers are idle, jobs are scarce, incomes stagnate, consumers struggle or go into debt to make ends meet, and the economy sits in a state of depression – which is often the case in developing countries. One can also imagine “high level” equilibria where producers generate desirable goods and services, jobs are plentiful, and household income is sufficient to demand all of that output.

The problem is that troubled economies don’t just naturally slide up to “high level” equilibria. Low level equilibria are typically supported and reinforced by a whole set of distortions, constraints, and even incentives for the low level equilibrium to persist. In developing countries, these often take the form of legal restrictions, price controls, weak property rights, political and civil instability, savings disincentives, lending restrictions, and a full catastrophe of other barriers to economic improvement. Good economic policy involves the art of relaxing constraints where they are binding, and imposing constraints where their absence allows the activities of some to injure or violate the rights of others.

In the United States, observers seem to scratch their heads as to why the economy has shifted down to such a low level of labor force participation. Even after years of recovery and trillions of dollars directed toward persistent monetary intervention, the economy seems locked in a low level equilibrium. Yet at the same time, corporate profits and margins have pushed to record highs, contributing to gaping income disparities.

From our perspective, the fundamental reason for economic stagnation and growing income disparity is straightforward: Our current set of economic policies supports and encourages a low level equilibrium by encouraging debt-financed consumption and discouraging saving and productive investment. We permit an insular group of professors and bankers to fling trillions of dollars about like Frisbees in the simplistic, misguided, and repeatedly destructive attempt to buy prosperity by maximally distorting the financial markets. We offer cheap capital and safety nets to too-big-to-fail banks by allowing them to speculate with the same balance sheets that we protect with deposit insurance. We pursue easy monetary fixes aimed at making people “feel” wealthier on paper, far beyond the fundamental value that has historically backed up that wealth. We view saving as dangerous and consumption as desirable, failing to recognize a basic accounting identity: there can only be a "savings glut" in countries that fail to stimulate investment. We leave central bankers in charge of our economic future because we're too timid to directly initiate or encourage productive investment through fiscal policy. When zero interest rates don't do the trick, we begin to imagine that maybe negative interest rates and penalties on saving might coerce people to spend now. Look around the world, and that same basic policy set is the hallmark of economic failure on every continent.

Four paragraphs from my March 30 comment Eating our Seed Corn: the causes of U.S. economic stagnation, and the way forward, summarize the situation:

“One of the central policy errors since the global financial crisis, and indeed since the collapse of the technology bubble after the 2000 market peak, has been the notion that economic problems caused by financial crisis must be fixed by financial means; monetary policy in particular. Unfortunately, this line of thinking has progressively weakened the U.S. economy, making it increasingly dependent on debt, encouraging the diversion of scarce savings to speculative purposes, promoting beggar-thy-neighbor monetary policies abroad that encourage the substitution of domestic jobs with cheaper foreign labor, and creating what is now the third U.S. equity valuation bubble in 15 years.

“The U.S. has become a nation preoccupied with consumption over investment; outsourcing its jobs, hollowing out its middle class, and accumulating increasing debt burdens to do so. Making our country stronger will require us to turn our backs on paper monetary fixes that discourage saving while promoting speculation and debt-financed consumption. It will also require us to turn toward policies that encourage productive investment – public (e.g. infrastructure), private (e.g. capital investment and R&D), and personal (e.g. education).

“In an economy where wages and salaries are depressed, but government transfer payments and increasing household debt allow households to bridge the gap and consume beyond their incomes, companies can sell their output without being constrained by the fact that households can’t actually afford it out of the labor income they earn. Meanwhile, our trading partners are more than happy to pursue mercantilist-like policies; exporting cheap foreign goods to U.S. consumers, and recycling the income by lending it back to the U.S. in order to finance that consumption. This dynamic has helped to turn the U.S. from what was once the largest creditor nation in the world to what is now the largest debtor. Debt-financed consumption, while it proceeds unhindered, is a central driver of elevated corporate profits.

“What raises both real wages and employment simultaneously is economic policy that focuses on productive investment – both public and private; on education; on incentivizing local investment and employment and discouraging outsourcing that hollows out middle class jobs in preference for cheap foreign labor; on international economic accords that harmonize corporate taxes, discourage corporate tax dodging and beggar-thy-neighbor monetary policies, and provide for offsetting penalties, import tariffs and export subsidies when those accords are violated. What our nation needs most is to adopt fiscal policies that direct our seed corn to productive soil, and to reject increasingly arbitrary monetary policies that encourage the nation to focus on what is paper instead of what is real.”

When a country allows its central bank to encourage yield-seeking speculative malinvestment; suppresses interest rates in a way that punishes those on fixed incomes and destroys the incentive to save; allows too-big-to-fail institutions to use deposit insurance as a public subsidy to expand trading activity instead of traditional banking; focuses fiscal policy on boosting transfer payments to make up for lost income without at the same time encouraging investment – both private and public – that could create new sources of income; that country is going to keep failing its people.

Every economy funnels its income toward factors that are most scarce and useful. If a country diverts its resources toward consumption and speculation rather than productive investment, it shelters the profitability of existing companies by making their capital more scarce and therefore more profitable, while at the same time discouraging new job creation. A vast pool of unused labor also has little ability to demand more compensation. In contrast, when an economy encourages productive investment at every level, more jobs are created, and yet capital becomes less scarce – so profit margins fall back to normal. The income from economic activity is then available to both labor and capital, rather than funneling income into a basket that reads “winner-take-all.”

We need to re-think which constraints are actually binding us. With trillions of dollars sitting idly in bank reserves, and interest rates next to zero, the Federal Reserve continues to behave as if bank reserves and interest rates are a binding constraint – that somehow loosening those further might free the economy to grow. This is lunacy. Fed policy is no longer relieving constraints; it is introducing distortions. That – not the exact level of wage growth, inflation, or unemployment – is the primary reason to normalize policy, and to start along that path as soon as possible. Current Fed policy discourages saving while diverting the little saving that remains toward yield-seeking malinvestment. If the members of the FOMC cannot restrain themselves from extraordinary policy distortions on their own, it may be time for legislation to explicitly remove the discretion from their hands.

Meanwhile, gross private and public investment has languished over the past 15 years. More thoughtful policy would provide tax incentives and accelerated depreciation for new private investment, encourage education and job training (which is the central form of investment at the personal level), and channel new funds toward public infrastructure, clean energy and other initiatives. Deficit spending is harmful when it is used for unproductive purposes, but as with private investment, the productive use of borrowed funds can provide for their own repayment. The promise of a better economic future is to ease the constraints that bind us, and turn our backs on the distortions that have driven the U.S. into stagnation. The promise of a better economic future is to reduce our dependence on debt-financed consumption, and shift our focus toward encouraging productive investment at every level of the economy.

How speculative distortion ends: the critical importance of market internals

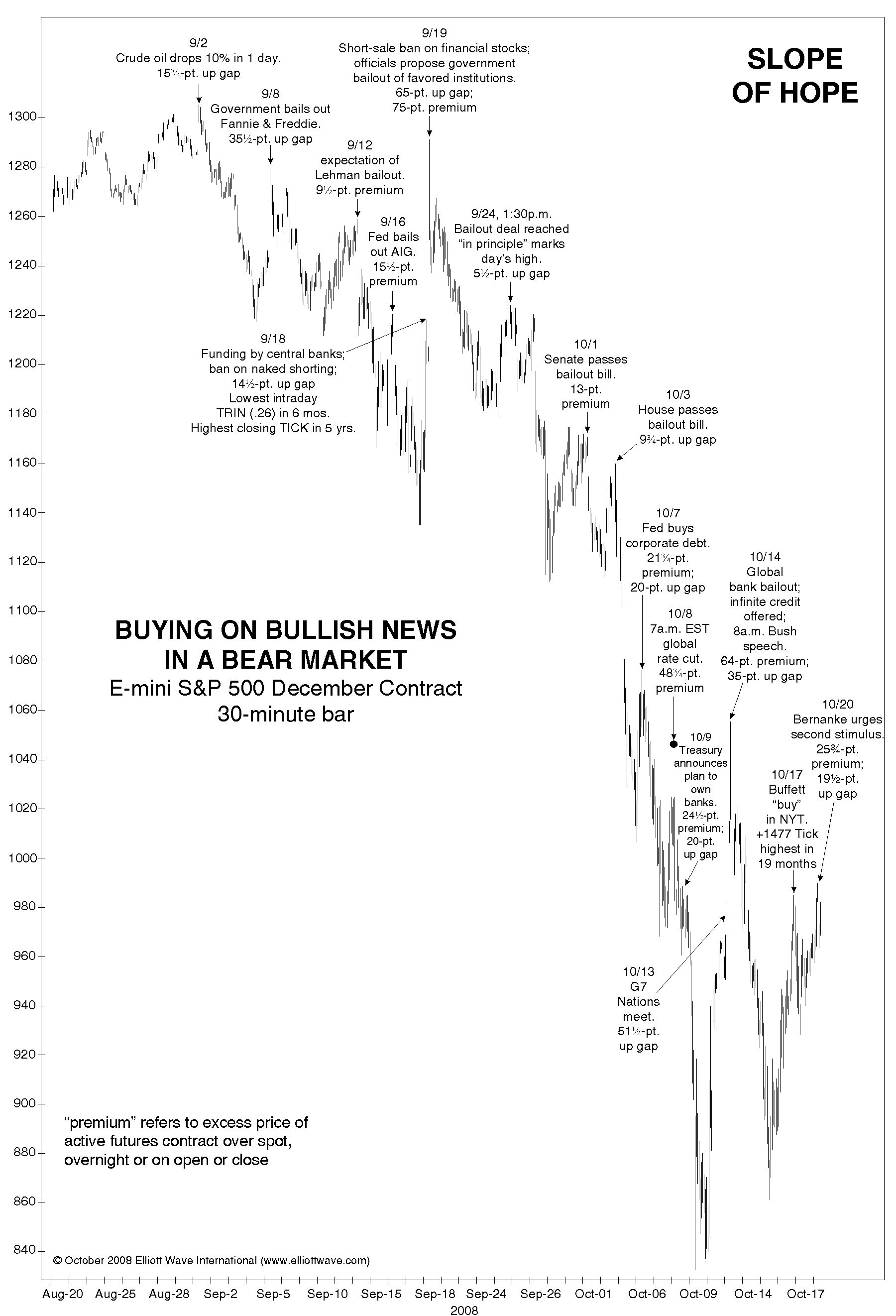

The difficulty with creating a bubble of speculative distortion is that there is always hell to pay, and once valuations have already been driven to extreme levels, that hell is baked in the cake. It can’t be avoided, and once investors have shifted toward risk-aversion, history indicates it can’t even be managed well. Recall that the Fed was easing persistently and continuously throughout the 2000-2002 and 2007-2009 market collapses.As a reminder of how fruitless official interventions can be once investors have shifted to risk-aversion, I’ve reprinted the instructive chart that Robert Prechter of EWT published in October 2008, as the S&P 500 was on its way to the 700 level. Investors who actually believe that Fed easing creates a “put option” for stocks have a very short memory of the past two bear market collapses.

As I’ve repeatedly noted in recent months, the response of the market to both overvaluation, and to Federal Reserve easing, is dependent and conditional on the attitude of investors toward risk, and the best measure of those risk-preferences is the behavior of market internals across a broad range of individual stocks, industries, sectors, and security types. There’s a pernicious idea that as soon as a given risk is even discussed, it becomes irrelevant. We know from numerous cycles that this isn’t true. Discussion of the extreme valuations of dot-com and tech stocks didn’t prevent their complete collapse in 2000-2002; discussion of sub-prime valuations, mortgage debt instability, and rich equity valuations didn’t prevent the global financial crisis in 2007-2009.

Be careful here – deteriorating internals matter. The condition of market internals is precisely the same hinge that – in market cycles across history – has separated overvalued markets that continued to advance from overvalued markets that collapsed through a trap door. That’s not to say that stocks must collapse immediately; market peaks are a process, not an event. That’s also not to say that market internals could not improve, which wouldn’t relieve extreme valuations, but could very well defer their immediate consequences. We’ll take our evidence as it arrives, but at present, we view the condition of the equity market as precarious.

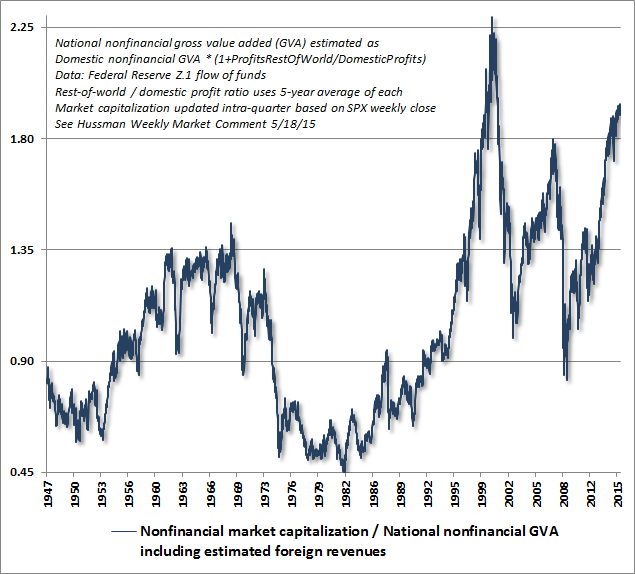

As a guide to how we expect the current market cycle to be completed, the chart below presents the ratio of market capitalization/gross value added, which has the strongest correlation with actual subsequent S&P 500 10-year nominal total returns of any valuation ratio we’ve examined across history (including Shiller P/E, market capitalization/GDP, price/revenue, price/dividend, price/book, Tobin’s Q, price/trailing earnings, price/forward earnings, the Fed Model, and other variants). On reliable measures available since the late-1880’s, as well as estimates imputed from historical data, current valuations now easily exceed the 1907 peak, the 1929 peak, the 1937 peak, the 1973 peak, the 1987 peak, the 2007 peak, and indeed every market peak in history except 2000. Moreover, the valuation of the median stock on the basis of price/earnings and price/revenue ratios considerably exceeds the 2000 peak here – because the 2000 peak was more focused on large-capitalization stocks, particularly in the technology sector. Put simply, the recent market peak represents the second most overvalued point in history for the capitalization-weighted stock market, and the single most overvalued point in history for the broad market.

The road to current extremes has been as challenging for investors who understand valuation and financial history as it has been glorious for investors who do not. I’ve tried to be very open about my own stumble in the half-cycle since 2009, when my insistence on stress-testing our methods of classifying market return/risk profiles against Depression-era data (following a financial collapse that we fully anticipated) produced an initial miss and additional knock-on effects that we finally resolved in mid-2014. The central problem was that in prior cycles across history, the emergence of a syndrome of extreme overvalued, overbought, overbullish conditions was typically either accompanied or closely followed by a deterioration in market internals, so the methods that came out of our stress testing encouraged us to take a hard-defensive stance immediately. The one thing that quantitative easing did to make the recent half-cycle legitimately “different” from history was that the Fed intentionally encouraged continued yield-seeking speculation even after those syndromes emerged. Since 2009, it has only been when market internals actually deteriorated (e.g. 2011) that stocks have followed by losing ground.

Still, the main benefit of a stumble is to learn the right lesson. The central lesson of the half-cycle advance since 2009 is not that Fed easing creates a “put option” for the market. We know from history – even from the two market collapses since 2000 – that this simply isn’t true. Rather, the central lesson is that in the face of intentional Fed-driven yield-seeking speculation, one had to wait until market internals actually deteriorated before taking a hard-defensive outlook. Pre-emptive action on the basis of even the most extreme overvalued, overbought, overbullish conditions was ineffective, in hindsight.

A century of evidence validates this lesson: what distinguishes an overvalued market that continues higher from an overvalued market that collapses is the attitude of investors toward risk; and the most reliable measure of investor risk-attitudes is the behavior of market internals. In mid-2014, we imposed the requirement that market internals or credit spreads must actually deteriorate in order to establish a hard-defensive market outlook. That adaptation restored the same features that were responsible for our long success prior to that 2009 stress-testing decision. In contrast, we see no evidence at all that investors have learned a thing from the two 50% market collapses since 2000, and it’s not at all clear that they’ve learned a thing from other collapses across history either. If they did, investors would recognize that compared with most of the bull market period since 2009, market internals no longer convey risk-seeking preferences among investors. Again, when investors are risk-seeking, as conveyed by the behavior of market internals, overvalued markets simply tend to become more overvalued. When internals break down following a period of overvalued, overbought, overbullish conditions, those same markets have become vulnerable to deep collapses.

Market internals are equally important on the downside. The legendary value investor Benjamin Graham lost 65% of his assets during the market collapse of the Great Depression, even after stocks had retreated to historically reasonable valuations, while economist John Maynard Keynes was devastated during the same period as a result of buying stocks on margin (an overuse of leverage that prompted his famous observation “the market can remain irrational longer than you can stay solvent”). By our analysis, both Graham and Keynes could have avoided those stumbles had they recognized the dismal state of market internals at the time, rather than acting on the basis of valuation alone. Compared with post-war data, one needed very robust measures of market internals during the Depression to avoid interim losses, even after valuations became favorable. The same lesson was true in late-October 2008. Fools are content to criticize the stumbles of others. The wise make an effort to learn from them.

When market internals are uniformly favorable, “buy the dip” is often a reliable strategy, because even extremely overvalued markets tend to be resilient provided that investors are strongly inclined toward risk-seeking. When market internals have deteriorated, it’s a signal that investors are shifting toward greater selectivity and risk aversion. You’ll still find bulls, of course – there has to be a buyer for every stock that is sold – and one can rely on the talking heads of financial television to be most arrogant toward skeptics at the very top of the market. But examine periods where overvaluation has been met by deterioration in market internals, and you’ll repeatedly find that persisting in a “buy the dip” mentality leads speculators to accumulate the very stock that the smarter money is getting rid of before a crash.

While our measures of market internals include a rich breadth of considerations, the essential feature is to capture the behavior of numerous individual stocks, industries, sectors and security types. When investors are risk-seeking, they tend to be risk-seeking in everything, so increased selectivity is a warning sign. Currently, fewer than half of all stocks are above their 200-day moving averages, for example. Last week, I shared Bill Hester’s observation that when weak participation has been accompanied by rich valuations, scarce bearish sentiment, and recent market highs, the number of instances narrow to some of the worst points in history to invest.

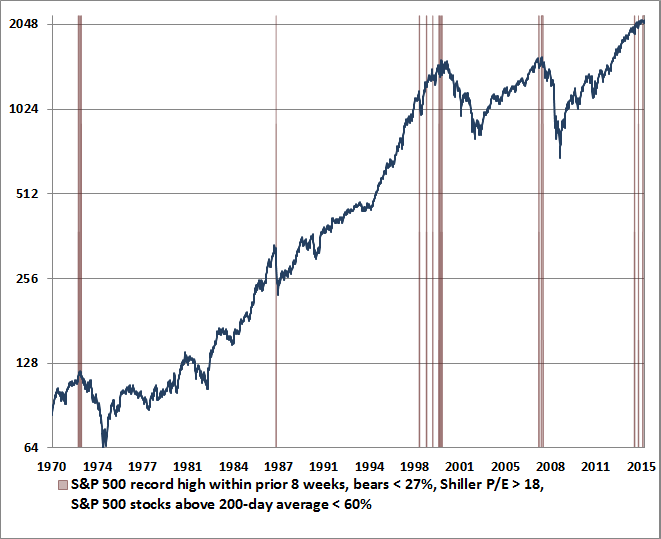

I noted in last week’s comment that it’s rare for the S&P 500 to register a new high when more than 40% of its components are already in a downtrend. When weak participation, rich valuations and scarce bearish sentiment accompanied a record high in the same week, the handful of instances diminish to surround the precise market highs of 1973, 2000, and 2007, as well as 1929 on imputed sentiment data – and the week ended July 17, 2015. Market analyst Dana Lyons identified the same instances using entirely different measures of market internals followed by market technicians. The only points that the S&P 500 was near a record high, coupled with negative readings on the McClellan summation indices for NYSE advances-declines and new highs-new lows, were immediately surrounding the market peaks of 1973, 2000, 2007 and today. Understand that the present deterioration of market internals is broad-based, unusual, and historically dangerous.

Now, maybe market internals will improve, and similar outcomes might be deferred for a while. We’ll take the evidence as it arrives. But investors should understand this in any event: given the extreme market valuations that have already been established, an awful completion to the current cycle is already baked in the cake. Current valuations suggest that even assuming 6% nominal economic growth and zero interest rates for years to come (an optimistic combination, to be sure), the nominal total return of the S&P 500 over the coming decade is still likely to be negative (see When You Look Back on This Moment in History). There will certainly be numerous points in the coming years where some combination of valuations and market internals will encourage a constructive or even aggressive outlook for the market, but here and now, investors should recognize that the downside risks are enormous.

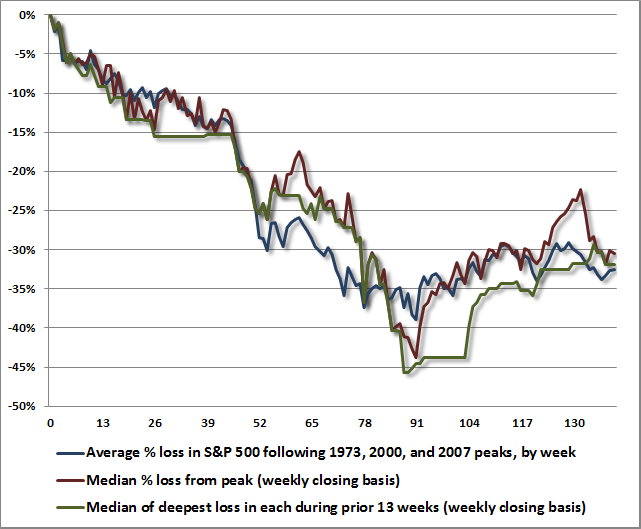

Finally, to offer a historical reminder of how the 1973, 2000 and 2007 peaks were resolved over the completion of those respective market cycles, the chart below shows the average and median cumulative drawdown losses starting from those market peaks. Barring a clear improvement in market internals, which could defer the immediacy of our downside concerns, our general expectation is that the coming 7-10 quarters are more likely than not to resemble the outcomes that these other cycles experienced once persistent overvalued, overbought, overbullish extremes were joined by deteriorating market internals.