Greece and the King of Asteroid 325 (and The One Lesson to Learn Before a Market Crash)

Last week, the price of Greek government debt soared on hopes of an 11th hour stick-save bailout by the European Union. Unfortunately, that price jump still left Greek bonds priced to reflect a default probability of 100% at every maturity. The jump only reflected an increase in the amount that bondholders evidently expect to recover in default, raising the implied recovery rate from the recent low near 30% to something closer to 50%. Put another way, the bond market has fully priced in the likelihood of a default coupled with a major haircut on Greek debt. What prices may not reflect is that the style of that haircut could be modeled after former finance minister Yanis Varoufakis.

While a can-kicking bailout is still possible, it’s not at all clear that it would be desirable for anyone in the longer-run. Meanwhile, in my view, the blame and finger-pointing being aimed at Greece is not only unfortunate but unjust. In Antoine de Saint Exupery’s The Little Prince, the King of Asteroid 325 asks, “If I ordered a general to change himself into a sea bird, and the general did not obey me… which of us would be in the wrong?”

The fact is that the entire structure of the euro itself is wrong – flawed – because it demands exactly that sort of transformation by any country that is not sufficiently similar to stronger European countries such as Germany, France and Finland. One of the first things that international economists learn to appreciate is the idea of an “adjustment variable.” When two countries differ significantly in their growth, productivity, tax structure, demographics, and other factors, the relative differences are typically resolved by changes in exchange rates, interest rates, and price levels. Those adjustment variables provide a buffer for each country that allows them to adapt individually to economic differences and shocks.

The problem with the euro is that the treaty that allowed each country entry into the system was much like an errant request by the King of Asteroid 325: transform yourself into a sea bird. The prerequisite for a common currency is that countries share a wide range of common economic features. A single currency doesn’t just remove exchange rate flexibility. It also removes the ability to finance deficits through money creation, independent of other countries. Moreover, because capital flows often respond more to short-term interest rate differences (“carry trade” spreads) than to long-term credit conditions, the common currency of the euro has removed a great deal of interest rate variation between countries. It may seem like a good thing that countries like Greece, Spain, Italy, Portugal, and others have been able to borrow at interest rates close to those of Germany for nearly two decades. But that has also enabled them to run far larger and more persistent fiscal deficits than would have been possible if they had individually floating currencies.

The euro is essentially a monetary arrangement that encourages and enables wide differences in economic fundamentals between countries to be glossed over and kicked down the road through increasing indebtedness of the weaker countries in the union to the stronger members. This produces recurring crises when the debt burdens become so intolerable that even short-run refinancing can’t be achieved without bailouts.

Greece isn’t uniquely to blame. It’s unfortunately just the first country to arrive at that particular finish line. Greece is simply demonstrating that a common currency between economically disparate countries can’t be sustained without continuing subsidies from the more prosperous countries in the system to less prosperous ones.

Extreme debt burdens can be eliminated in only one of three ways: default, money creation, or austerity (budget cuts, pension reductions, wage cuts, and tax increases). Greek membership in the euro has made the first two options very difficult, and periodic bailouts only discourage more durable policy changes. Meanwhile, austerity policies and repeated episodes of crisis create nearly intolerable instability in the Greek economy. Constant demands for more austerity fuel animosity with other European countries, and discourage long-term planning and stable, productive investment.

In our view, it is in the best interests of Greece to have its own currency, so that interest rates, exchange rates, and if necessary, even domestic inflation can act as shock absorbers for its economy, rather than forcing human beings to become the only shock absorbers that Greece has left.

What is the greatest concern we should have about a Greek default, and a Greek exit from the euro? What is the greatest concern we should have if the global economy doesn’t continue down the road of financial distortion and stick-save bailouts at every turn? The answer is implicit in the question. The greatest concern is that we will have to face reality, and that we will have to adjust to reality in what will hopefully be a sustainable way instead of kicking that can down the road until no other options are available but large scale default, austerity, or inflation.

Greece is simply a microcosm for an economic dynamic that has infected the entire global economy, including the United States. Over nearly two decades now, the growth of productive investment has slowed to a crawl, replaced by speculative malinvestment and extraordinary monetary distortions at every turn. As productive investment has slowed, productivity growth has also slowed, job growth has slowed, wage growth has stagnated, and income disparities have soared. For a detailed discussion of how this dynamic has played out in the U.S. economy, see Eating Our Seed Corn: The causes of U.S. stagnation, and the way forward.

How does such an economic dynamic hold together over the shorter-run? The answer should be obvious by looking around the globe: debt-financed consumption, massive increases in the volume of debt obligations, and frantic efforts by monetary authorities to suppress interest rates in order to avoid default events. This is not a sustainable dynamic, but an illusory stability that relies on constant accumulation of debt burdens by the middle class; by countries that don’t look like Germany, France, and Finland. Nobody wants to consider how or whether these debts can be repaid; only whether they can be refinanced over the shorter-run. That’s the same material from which the global financial crisis was built, because much of the debt is owed to financial institutions that have all lobbied their governments for the most lenient capital buffers possible.

What is the greatest near-term concern we should have about a Greek exit from the euro? Obviously there would be disruption, but the Greek government is still capable of introducing scrip (essentially IOUs to its citizens), creating a new currency, and bailing in the bank deposits of citizens with claims on the domestic currency. So the human impact could be managed. Beyond Greece, the greatest concern is the fact that much of the Greek debt burden is held by financial institutions that have inadequate capital buffers. The largest European banks today have higher gross leverage ratios than similar U.S. financial institutions did at the peak of the housing bubble. Greece is not large relative to global financial markets, but it is large enough to create disruptions and capital inadequacy at major banks across Europe. Larger and more prosperous European countries will not avoid having to spend billions of euros in transfer payments, bailouts and subsidies as a result of the faulty structure of the euro. It’s just that these euros will go directly to bail out the European financial system rather than first taking a summer holiday in Mykonos.

The one lesson to learn before a market crash

There is one lesson to learn immediately – one that makes sense of the speculative yield-seeking market advance of recent years; one that makes sense of every market bubble on record; and most importantly, one that makes sense of the collapse of every speculative episode in history, including the 2000-2002 and 2007-2009 collapses. For those of you who have followed me over three decades as a professional investor, you’ll observe that my own successes and occasional stumbles over that time can be almost perfectly distinguished by the extent to which my own investment outlook lined up with this lesson. It is presently the most important thing I have to offer you:

The long-term returns that you enjoy on your investments over time are primarily determined by the level of valuation that you pay for those investments. However, market outcomes over shorter horizons are determined by the preferences of investors toward risk-seeking or risk-aversion, and the most reliable measure of investor risk preferences is the behavior of market internals across a broad range of individual securities, industries, sectors, and security types.

That’s it. Valuations control long-term returns. Investor risk-preferences control outcomes over shorter horizons. The best measure of risk-preferences is the uniformity or divergence of market action across a wide range of market internals, credit spreads, and other risk-sensitive measures.

At present, U.S. market internals continue to deteriorate, while credit spreads remain wide. On the measures that have the most historically reliable correlation with actual subsequent market returns, valuations are obscene (see When You Look Back On This Moment In History). Meanwhile, China has now resorted to legal threats, market closure, and restrictions on selling in a frantic effort to keep its own margin-fueled speculative bubble from collapsing. These conditions may change. Until they do, equity investors are facing the most unfavorable combination of valuations and market internals we identify.

Just as the near-term response of the market to overvaluation or undervaluation is dependent on investor risk-preferences, the response of investors to monetary interventions and other efforts to distort the financial markets is also dependent on investor risk preferences. When investors are inclined toward risk-seeking speculation, safe and low-interest cash is viewed as an inferior holding. As a result, injecting safe and low-interest cash into the financial system (via Fed purchases of government bonds) creates a pile of hot potatoes that investors sequentially try to pass off onto other holders by chasing riskier securities. Each new buyer of risky securities passes their cash off to the next seller, and those sellers look for yet other ways to get rid of the undesirable cash by chasing something else.

In contrast, and investors should (but don’t) vividly remember this from the 2000-2002 and 2007-2009 market collapses when the Fed was persistently and aggressively easing the whole time: Easy money does very little to counter a market collapse once investors have become risk-averse. When investors are inclined toward risk-aversion, safe and low-interest cash is viewed as a desirable asset. As a result, injecting safe and low-interest cash into the financial system (via Fed purchases of government bonds) simply substitutes one safe-haven asset for another, and aside from very short-term knee-jerk effects, does nothing to support the market.

Now, that’s not to say there can’t be a feedback from monetary policy and investor risk-preferences. It’s perfectly reasonable to allow for the possibility that monetary easing can help to shift investor preferences from risk-aversion to risk-seeking. But the central point is this: the best measure of that sort of shift is not the behavior of monetary authorities, but the behavior of market internals themselves. If the Fed is easing but market valuations and internals are still negative, the historical evidence is that the market continues to fall. We’ve reviewed that evidence numerous times, but we continue to see comments that implicitly reflect the belief that market outcomes are directly determined by the Fed, rather than being dependent on the state of investor risk tolerance.

Look back to the 2007-2009 market collapse, and you’ll notice something. Despite repeated monetary and fiscal interventions, a positive shift in market internals didn’t happen until March-April 2009. In hindsight, it was none of those interventions that produced the shift, but instead the change in accounting rule FAS 157 in the second week of March 2009 that finally ended the collapse. That accounting change eliminated the “mark-to-market” rule that had required banks to report the value of their assets at market value, and instead allowed banks considerable discretion to choose the value at which those assets were reported. With the stroke of a pen, banks that were insolvent on a mark-to-market basis became whole on a mark-to-model basis. In hindsight, regulatory authorities used that change to abandon any further action that might have put those insolvent banks and financial institutions into receivership or conservatorship. In the end, it was not monetary easing, nor troubled-asset relief, that ended the collapse. It was a change in accounting rules.

A similar failure of memory seems to prevail when the media incorrectly suggests that the collapse of the market in 2008 began with the Lehman bankruptcy on September 15. The fact is that the market fully recovered to even higher levels the following week as the government banned short selling of financial stocks (much like China is doing more broadly at present). Weeks later, in a wicked case of “sell the news,” the actual collapse started literally 15 seconds after the TARP bailout was passed by Congress. Investors want to tie market outcomes to very specific events or catalysts. But history suggests a different lesson: once extreme valuations are joined by a shift toward risk-aversion among investors, the specific events become irrelevant. One way or another, the market is likely to get hit by a truck.

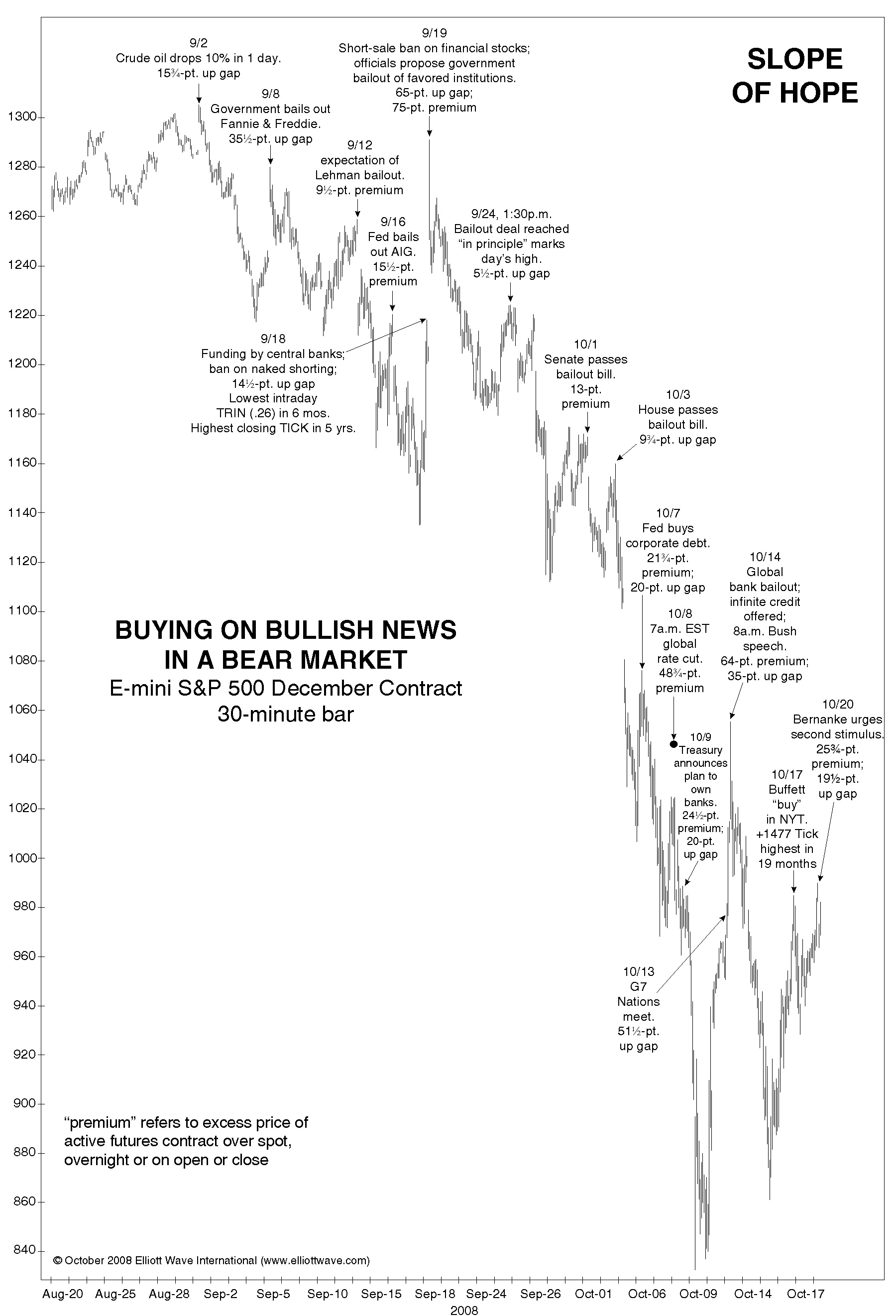

In October 2008, as the global financial crisis was in full force, Robert Prechter of EWT published a very instructive graphic illustrating how the accumulating market losses were descending along a “slope of hope” (the corollary to bull markets climbing a so-called “wall of worry”) despite repeated official interventions. Notice that aside from very short-term rallies following various interventions, the market kept collapsing. We encourage investors to learn from this now.

The S&P 500 would ultimately plunge below 700 by March 2009. Importantly, investors who “followed the Fed” during the 2007-2009 collapse would have done so through the 55% loss in the S&P 500, because the Fed began easing weeks before the 2007 peak, and kept easing all the way down. As in every other market cycle across history, it was far better to follow the condition of investor risk-preferences directly.

Don’t make the mistake of getting the relationship between monetary interventions and the risk-preferences of investors backwards. Monetary easing and other interventions can be very effective when they occur against a backdrop of risk-seeking investor preferences, but history shows that they regularly fail when they occur against a backdrop of risk-aversion among investors. The best measure of investor risk preferences is the uniformity or divergence of market internals across a broad range of risk-sensitive securities. Prechter describes the prevailing psychology of investors with the term “socioeconomic orientation,” and his observations on this, I think, are exactly correct:

“People keep asking, ‘What effect will the next central-bank plan have on the stock market’s behavior?’This is the wrong question. The socioeconomic orientation turns the question around: ‘What effect will the next stock market move have on the central bank’s behavior?’ Just study [the chart above] and you can see that the authorities are not pushing the stock market around; the stock market is pushing the authorities around. Sadly, when markets push authorities around, authorities push people around. All it does is make things worse.”

Now, if we were to observe a favorable shift in market internals and credit spreads, it would not ease the obscene overvaluation of the market, but it would substantially ease the immediacy of our downside concerns. A shift toward investor risk-seeking could again create an environment where risk-free liquidity is viewed as an inferior asset and a hot potato. That’s the central feature that characterized most of the period from early 2009 through mid-2014 (with a few exceptions such as mid-2011 when internals deteriorated and the S&P 500 subsequently dropped nearly 20%). I certainly don’t believe that a fresh reflation of an already obscene financial bubble would strengthen the global economy. In any event, however, our focus should not be on central bank actions, but directly on the uniformity or divergence of market internals.

When to become constructive

The single most favorable moment in the market cycle to accept risk is when a significant retreat in valuations is joined by an improvement in market internals. The single most dangerous moment in the market cycle is when persistent overvalued, overbought, overbullish extremes are joined by deterioration in market internals. Align your outlook with prevailing, observable conditions. Shift your outlook when prevailing, observable conditions shift. No forecasts are required. We certainly believe that we have better proprietary measures of these factors than others may, but those differences are secondary to getting the main lesson right.

Put simply, there’s one central lesson to learn from both my major successes and my occasional stumbles. That lesson is free to learn the easy way, or the hard way, or not at all, but there it is. For a detailed narrative of how and why my 2009 insistence on stress-testing our methods against Depression-era data led to a stumble in the recent half-cycle advance, and how that issue was addressed in mid-2014, see A Better Lesson Than “This Time is Different” and Voting Machine, Weighing Machine.

When we shift our outlook over the completion of the current market cycle and begin encouraging a constructive or even leveraged stance, those who’ve incorrectly inferred that I’m some sort of “permabear” may become bewildered, or even believe that I’ve abandoned my investment discipline. The permabear label may be satisfying in a sort of “kick him when he’s down” kind of way, but it doesn’t explain the success prior to 2009. The way to avoid confusion is to understand the narrative of the awkward transition from our pre-2009 methods to our present methods of classifying market return/risk profiles. I expect that our response to the completion of the current cycle will be much as it was after every other bear market plunge in recent decades, when I also encouraged a constructive or leveraged stance after correctly defending against losses (e.g. becoming a leveraged bull for years after the 1990 bear market, mostly unhedged in April 2003 after avoiding the 2000-2002 plunge, and constructive in late-2008 after the market collapsed by more than 40%, though that constructive shift was truncated by my stress-testing decision in 2009).

Investors are free to draw whatever alternative lesson they choose. They are free to decide that this time is different and an understanding of history has nothing to offer them. They are free to decide that the economy has entered some new era. They are free to decide that Fed easing always creates a floor for the market. They are free to decide that valuations don’t matter. They are free to choose all kinds of lessons – but understand that those are the same fallacies that have led investors to misfortune in prior cycles throughout history.

Despite the rather unfavorable conditions we observe at present, an improvement in market internals would defer the immediacy of our downside concerns. More importantly, we fully expect that the completion of the current cycle will provide more than enough opportunities to shift to a constructive or even aggressive investment outlook for stocks, particularly once a material retreat in valuations is followed by an improvement in market internals.

A final note – if you go back and read what I wrote at the extremes of prior market cycles, the lesson that I’m emphasizing here is precisely the same one I encouraged investors to recognize at the 2000 and 2007 market peaks. The most dangerous market environments on record are those where extremely overvalued, overbought, overbullish market conditions have been joined by a deterioration in market action (what we used to call “trend uniformity” in the late-1990’s):

“Historically, when trend uniformity has been positive, stocks have generally ignored overvaluation, no matter how extreme. When the market loses that uniformity, valuations often matter suddenly and with a vengeance. This is a lesson best learned before a crash rather than after one.”

Hussman Investment Research & Insight, October 3, 2000

“We can rarely predict that the market will reliably advance or decline over the next week or month or quarter. What we can say is that the average return/risk profile varies substantially across buckets. Given observations over at least one complete market cycle, we regularly find that the strongest average return/risk profile was associated with periods that one could identify in advance as having favorable valuation and (already) favorable market action, and that the poorest subsequent return/risk profile was associated with the bucket of periods having unfavorable valuation and unfavorable market action. Over the complete market cycle, this knowledge has generally been enough to achieve strong full-cycle returns with moderate risk.

“Presently, the price/peak earnings multiple of the S&P 500 is at 18.4 even without normalizing the level of profit margins. The S&P 500 is at a record high, is clearly overbought, and is pushing the upper Bollinger band at every horizon (daily, weekly, and monthly). Treasury yields provide no assistance, with the 10-year yield about the same level as 6 months ago and well off of its lows, while Treasury bill yields are also well off their lows. Sentiment readings from Investors Intelligence indicate 60.2% bulls and just 18.3% bears. Finally, we have what has historically been a sharply negative additional feature: our measures of market action are unfavorable (this is in contrast to points earlier this year, when we could infer the risk of abrupt corrections despite constructive internals).”

Warning – Examine All Risk Exposures, Hussman Weekly Comment, October 15, 2007

If you’ve decided to ignore all of this, don’t worry – you won’t be alone. Of course, you wouldn’t have been alone then either.

Past performance does not ensure future results, and there is no assurance that the Hussman Funds will achieve their investment objectives. An investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted above. More current performance data through the most recent month-end is available at www.hussmanfunds.com. Investors should consider the investment objectives, risks, and charges and expenses of the Funds carefully before investing. For this and other information, please obtain a Prospectus and read it carefully.

Site and site contents © copyright 2003 Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law.