We continue to view the equity market as tracing out an extended two-year top formation, at what is presently the third most extreme level of market overvaluation in history. Enthusiasm about a runaway market “breakout” to the upside is clearly evident in fresh sentiment extremes, with advisory bullishness rising to 55.9% and bearishness down to 21.6% (Investors Intelligence), but the fact is that the S&P 500 Index closed Friday less than 4% above its May 2015 high, and just 1% above its August 2016 high. The broader NYSE Composite Index remains below the level it set in July 2014, though with a slightly positive return including dividends. The stock market has reestablished an extreme overvalued, overbought, overbullish syndrome of conditions that - unlike much of half-cycle advance from 2009 to mid-2014 - lacks internal uniformity, particularly among interest-sensitive and globally-sensitive sectors. For that reason, the recent marginal highs are more consistent with a “blowoff” than a “breakout.”

From a short-term perspective, it’s important to emphasize that if market internals were to become more uniformly favorable, we could infer a more robust shift toward risk-seeking among investors. That, in turn, could encourage a more neutral or constructive near-term view despite offensive valuations. As the data stand, however, the recent post-election advance appears much like the post-Brexit rally in global markets, where nearly all of the gains were compressed in the first 12 trading days, after which the enthusiasm flamed out.

Frankly, regardless of how market action plays out on a shorter horizon, I still expect the S&P 500 to surrender its entire total return since 2000 over the completion of the current market cycle. The interim returns are likely to represent little but temporary paper gains, except for investors who exit. Even in that event, some other investor would then be in the position of holding the bag. In aggregate, the U.S. equity market is unlikely to avoid a roughly $10 trillion paper loss by the completion of this market cycle.

The chart below shows a 10-year view of the FTSE All-World Index, which represents about 95% of tradeable global equity market capitalization. This profile also remains consistent with an extended top formation, following a broad peak in mid-2015. I’m certainly not tied to that view, but again, an improvement in market internals across a wider range of security types and sectors would be the main reason to adopt a more balanced outlook.

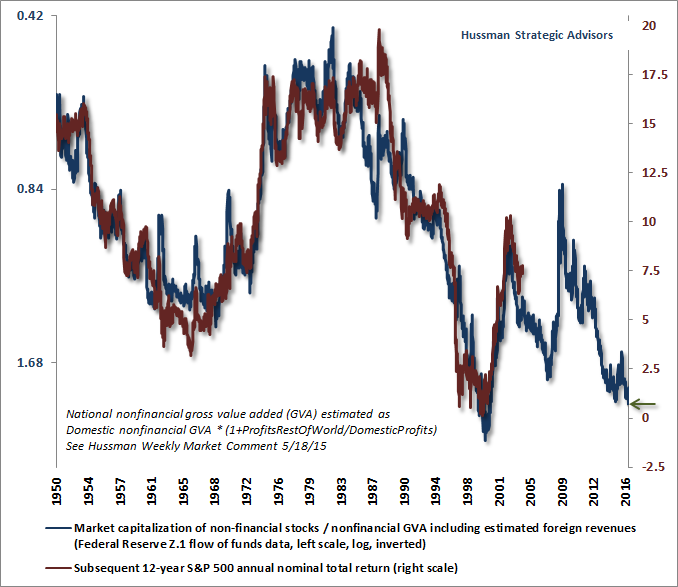

All of the most reliable equity market valuation measures we track (as measured by their relationship with actual subsequent market returns across history) are offensively overvalued from a long-term and full-cycle perspective. The most accurate measure we’ve developed over time - the ratio of U.S. nonfinancial market capitalization to corporate gross value-added - has now marginally eclipsed its 2015 high, placing it at a level consistent with expectations of S&P 500 12-year nominal total returns averaging less than 1% annually.

Having driven valuations to current extremes almost exclusively on the basis of yield-seeking speculation, it’s somewhat ironic that Wall Street analysts are now suggesting that the new administration will bring higher GDP growth that will presumably enable valuations to be sustained or extended, despite higher interest rates. Unfortunately, even if we enjoy faster economic growth with only marginally higher interest rates, we already know that those same economic conditions have historically been associated with market valuations averaging less than half of present levels (though those lower valuations would come with the corresponding benefit of 12-year expected stock market returns centered around 10% annually, rather than the current 1%).

Simply put, history instructs investors that they should expect dismal market returns in the coming 10-12 years, regardless of economic growth. Over a century, a difference of even one percent annually in economic growth would carry enormous implications for society (not that I'm convinced there's much basis for that hope on the current policy menu). Over a 10-12 year period, however, even much larger variations in economic growth have virtually no impact on market returns compared with the effect of valuations, particularly because terminal valuations are negatively, not positively, correlated with nominal growth over the preceding decade (see Rarefied Air: Valuations and Subsequent Market Returns for more detail on this regularity). A century of data is clear that stocks will not be again poised for adequate long-term returns until we observe a steep retreat in valuations. Even a full normalization of economic activity isn’t likely to change the mapping between current valuation extremes and weak market returns in the years ahead.

The chart below shows MarketCap/GVA on an inverted log scale (blue line, left), along with the actual subsequent S&P 500 12-year nominal total return (red line, right). The current level of valuations, noted by the green arrow, is consistent with expected total returns averaging less than 1% annually in the years ahead.

We’ve shown similar and only slightly less accurate relationships back to the early 1900’s using other valuation measures. Nothing - not the Great Depression, penicillin, World War II, the digital computer, the atomic bomb, Mr Potato Head, the microprocessor, the 1970’s inflation, the Cold War, the breakup of the Soviet Union, the expansion of global trade, the tech bubble, 9/11, the global financial crisis - nothing - has durably changed the mapping between reliable valuation measures and subsequent 10-12 year market returns. We cannotsay the same thing for shorter segments of the market cycle, where speculation, panic, and shifts in investor risk-preferences play a critical role. But to imagine that stocks are priced as desirable long-term investments here is a denial of every lesson of market history.

We constantly emphasize that valuations are not sufficient to evaluate market return/risk prospects over shorter segments of the market cycle. On that front, investor sentiment, and specifically their preferences toward risk-seeking or risk-aversion, is what primarily drives returns over those shorter horizons. It’s there that we absolutely have to keep some flexibility, particularly because novelty can affect waves of investor psychology. Novelty can be taken as a signal that “this time is different” even if the difference is an irrelevant one. It can encourage investors to adopt new-era “concepts,” but can also encourage the imagination to run toward fear and worst-case scenarios. If there’s one thing investors can count on in the coming years, it will be novelty. It remains to be seen whether it will arrive in the form of beneficial policy surprises, disruptive errors in judgment, or a parade of rubber chickens. My impression is that we may be in for all three.

Taking evidence as it arrives

Overall, present market conditions feature a combination of extreme valuations, a fresh syndrome of overvalued, overbought, overbullish extremes, divergent market internals, and hostile yield trends. This is fairly similar to the environment we observed in October 2000, when I wrote “Valuations, trend uniformity, and yield pressures are now uniformly unfavorable, and the market faces extreme risk in this environment.” Still, given that investors still seem to be adapting to the election results, it’s not entirely clear that the wide dispersion across market internals will continue. While valuations already imply a high likelihood of steep losses over the completion of the current market cycle, and dismal returns on a 10-12 year horizon, we can’t rule out a resumption of risk-seeking among investors over a shorter segment of the market cycle. The uniformity or divergence of market internals is a key measure of those risk-preferences. For that reason, we will continue to take the evidence as it arrives.

It may be useful to push back on some misconceptions. Our assertion is not that stocks will immediately collapse from present extremes. Rather, our assertion is simply that we presently identify a negative expected near-term market return/risk profile based on our classification of observable data, in the context of extreme valuations that also have unfavorable long-term implications. Next week, and the week after, and the week after, we will do that same kind of classification. As the evidence changes, we will align our market outlook accordingly.

Do we presently allow for a market collapse? Sure; given extreme valuations, lopsided bullishness, hostile yield trends and divergent internals, we have to. Are we pounding the table about a collapse? No; we’d look for even greater internal deterioration first. Near-term, we’re more inclined to expect an air-pocket than a crash.

Would we allow for an oncoming recession? Given that year-over-year growth rates in real GDP, industrial production, and real final sales are already at the border of where most recessions have started, we have to be vigilant. Are we pounding the table about a recession? No; we’d look for fresh deterioration across new orders, production, real sales, and personal income, coupled with widening credit spreads and a material break in the S&P 500 (at least below its level of 6-months prior), before becoming aggressive about recession concerns.

To attribute to me some constant, dire expectation of imminent collapse is to oversimplify the current facts. Some of these facts are yes, years of speculative yield-seeking have established the third financial bubble since 2000, the third most extreme level of general market valuation in history, and the most offensive valuation extreme in history from the standpoint of the median stock. Another fact is that credit burdens have never been higher, and much of that credit is of the covenant-lite variety, issued to satisfy speculative yield-seeking demand (much as low-grade mortgage securities were issued during the housing bubble). But still another fact is that investor attitudes toward risk can substantially affect the outcome of such extremes over shorter segments of the market cycle. The tendency toward risk-seeking has clearly been extended by monetary policy in the half-cycle since 2009, and we need to balance the likelihood of a disastrous full-cycle outcome with the constant potential for investors to adopt a fresh inclination to speculate over shorter horizons. That’s why we have to evaluate observable market conditions week-to-week.

We certainly take a much more defensive outlook (as we have at present) when valuations are extreme, internals are divergent, and yield trends are hostile. Conversely, as I’ve often emphasized, the strongest market return/risk profiles we identify are associated with a material retreat in valuations that is then joined by an early improvement in market internals. We’ll get to those opportunities soon enough.

The fact is that I’ve encouraged a constructive or leveraged market outlook after every bear market decline in 30 years as a professional investor (even late-2008 after the S&P 500 lost over 40% of its value). While my insistence on stress-testing our classification methods against Depression-era data in 2009 bared an Achilles Heel during the half-cycle advance that followed, I've detailed exactly what that challenge was, why it emerged, and the adaptations we made in mid-2014 to address it (see the “Box” in The Next Big Short for the full narrative). It’s admittedly difficult to demonstrate much benefit in a hypervalued two-year top-formation with diverging internals, but it’s worth noting that our present methods would encourage a constructive or aggressive market outlook across about 70% of market history. Again, I expect that we’ll see those constructive opportunities, at least moderate ones, soon enough. In the interim, some of the most useful assets to investors will be patience, discipline, and flexibility toward changing their investment outlook as the evidence itself changes.

© Hussman Funds

© Hussman Funds

Read more commentaries by Hussman Funds