On the first day of March 2017, the combined market capitalization of U.S. nonfinancial and financial stocks reached $34 trillion. Those trillions of dollars in paper wealth filter down to the investment statements of millions of investors, reflected in quotes on computer screens and blotches of ink on paper. Over the completion of the current market cycle, we estimate that roughly half of U.S. equity market capitalization - $17 trillion in paper wealth - will simply vanish. Nobody will “get” that wealth. It will simply disappear, like a game of musical chairs where players think they've won by finding chairs as the music stops, and suddenly feel them dissolving as if they had never existed in the first place.

As I noted in 2015, because equities are correlated with other assets, the total private net worth of U.S. households and corporations tends to change by about $1.50 for every dollar that U.S. equity market capitalization changes. With total U.S. private net worth currently at about $120 trillion, it would currently take an equity market loss of only about 20% to wipe out $10 trillion in U.S. private net worth (0.2 x 1.5 x 34). By contrast, an expected 50% loss of U.S. equity market capitalization over the completion of this market cycle (a decline that would not even bring historically reliable valuation metrics below their long-term historical norms), would produce an expected loss of over $25 trillion in U.S. total private net worth.

To understand how paper wealth vanishes, recognize that market capitalization is merely the product of two objects: the number of shares outstanding, and the price of those shares. For example, there are currently nearly 9 billion shares of General Electric outstanding. If a dentist in Poughkeepsie sells a single share of GE to some buyer, just 10 cents below the price of the preceding trade in the stock, fully $900 million dollars of market capitalization is instantly erased from the U.S. stock market as a result of that one $30 stock trade. Nobody “got” the $900 million. The lost market capitalization didn't "go into" bonds, or real estate, or gold, or cash on the sidelines, or anything else. It just plain vanished. Conversely, if our dentist buys a single share just 10 cents above the preceding trade in the stock, fully $900 million dollars of market capitalization is instantly “created” as a result of that one $30 stock trade.

Because of those fluctuations, investors across the nation imagine that they are actually gaining or losing “wealth” as market capitalization appears and vanishes. They alternately celebrate and suffer because they can’t distinguish wealth from the illusion of wealth. When one understands how ephemeral market capitalization can be, it may become clear why I’m so adamant about the actual claim that investors actually obtain by owning a share of stock.

See, the actual “wealth” inherent in a share of stock is embodied in the very long-term stream of future cash flows that the company will actually deliver into the hands of investors over time. As long as a share of stock is outstanding, somebody has to hold it at every point in time, and that long-term stream of cash flows is actually what’s being traded. Everyone who owns the stock owns a divided claim to those cash flows. Investors don’t get to claim those future cash flows until they actually buy, and they don’t get to claim the market price until they actually sell. Put another way, the only investor who has a reliable claim to the current market price is an investor who is selling at that price.

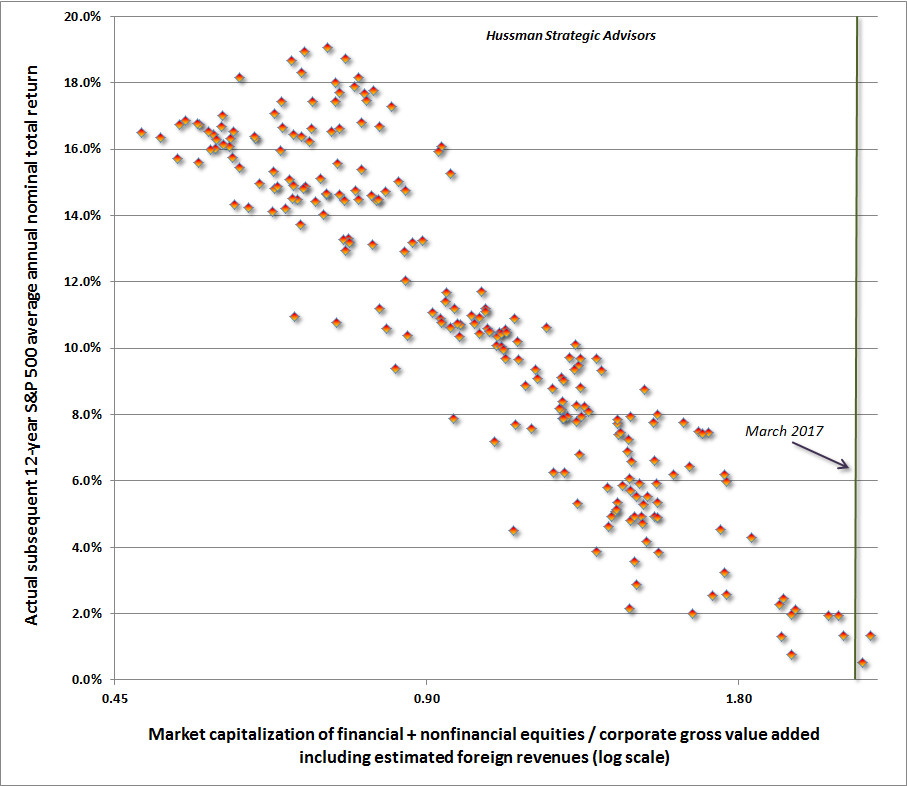

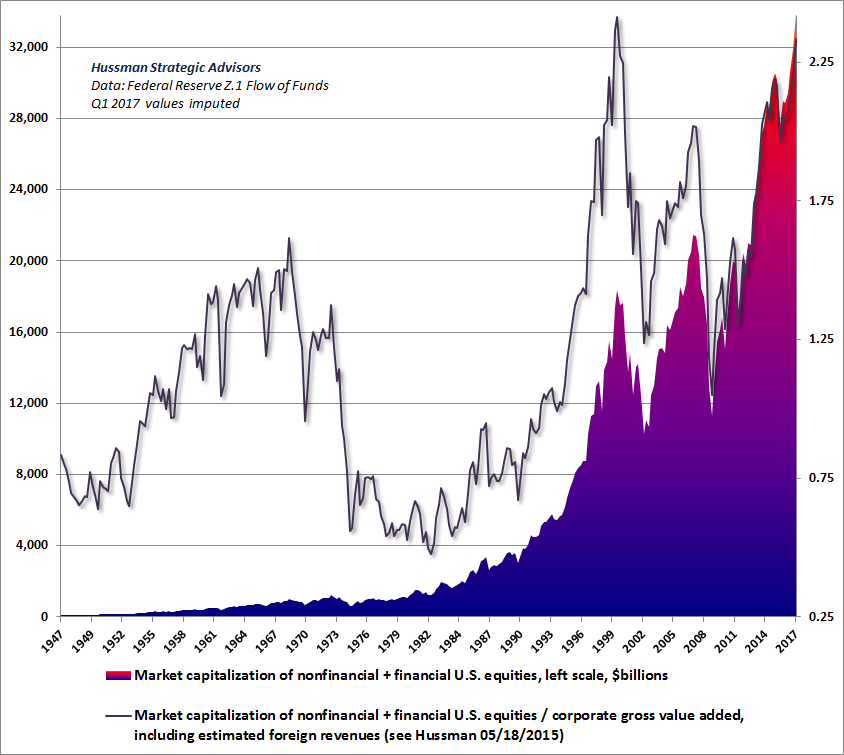

Let’s pause to recognize the opportunity, and the risk, that investors face at the obscene levels of valuation that have been created by years of Fed-induced yield-seeking speculation, coupled with Wall Street’s enthusiasm over largely imaginary prospects for a sustained acceleration in economic growth (more on that below). The chart below presents the market capitalization of U.S. equities (left scale, $billions). The thin line shows the ratio of market capitalization to corporate gross value added (right scale) to offer an additional valuation perspective. On this measure, current valuations now rival those of the 2000 market extreme, standing at more than double the historical norm (including the bubble period since the late-1990’s), and about 160% above pre-bubble norms. Put simply, the U.S. equity market could lose $17 trillion in value - over 50% of its market capitalization - even without taking reliable valuation measures below their historical norms.

[I also created a chart showing total market capitalization on log scale: click here]

A few of the preceding comments will benefit from some amount of additional support (see the links in the text for charts and data). I’ve previously detailed the arithmetic of U.S. real GDP growth, including demographic constraints on labor force growth and productivity relationships that make a sustained acceleration to even 2.7% real GDP growth unlikely. Likewise, I’ve detailed the impact of interest rates on equity valuations, the fact that the Fed Model is wholly an artifact of the 16-year disinflationary period from 1982-1998, and the earnings dynamics that make popular measures such as “forward operating earnings” such poor sufficient statistics for the long-term stream of cash flows that investors actually stand to receive over time.