Last week, the spread between bullish and bearish sentiment widened substantially, pushing market conditions to what I’ve often described as an “overvalued, overbought, overbullish” syndrome. While our general outlook has remained rather neutral in recent weeks, this shift pushes our immediate outlook back to hard-negative. However, I should emphasize that this outlook is not particularly robust at present. Indeed, we could soon find ourselves back to a neutral outlook in the event of a moderate further improvement in market internals. As I’ve emphasized regularly since mid-2014, when we adapted our methods to address the key challenges we encountered in the half-cycle since 2009 (see the Box in The Next Big Short for a detailed narrative), the advancing half-cycle since 2009 has been different from market cycles across history, in that aggressive central bank easing has persistently deferred the typical consequences of overvalued, overbought, overbullish conditions. In the face of QE, one had to wait until market internals deteriorated explicitly (indicating a shift toward risk-aversion among investors) before adopting a hard-negative outlook.

While the recent market advance appears driven by little but trend-following and short-covering, moderate further improvement in market internals could return us to a fairly neutral near-term outlook. Beyond encouraging a neutral stance with a small “tail-risk” hedge about the 1980-2015 area on the S&P 500 (the area where nearly all our trend-sensitive measures would pile onto the negative side) we won’t fight risk-seeking behavior in the event it reemerges in the form of uniform market internals. Still, even if the major indices were to register fresh highs, my impression would remain that the market is in the process of tracing out the arc of an extended top formation.

It’s largely forgotten that during the 2000 top formation, the S&P 500 lost 12% from July-October 1999, recovered to fresh highs, retreated by nearly 10% from December 1999 to February 2000, recovered to fresh highs, experienced another 10% correction into May, recovered to a new high in total return (though not in price) on September 1, 2000, retreated 17% by December, and by January 2001 had recovered within 10% from its all-time high, and was unchanged from its level of June 1999.

Likewise, during the 2007 top formation, the S&P 500 corrected nearly 10% from July to August, recovered to a fresh high in October, corrected over 10% into November, recovered nearly all of it by December, followed with a 16% loss, and by May 2008 had recovered within 9% of its all-time high, and was unchanged from its level of October 2006.

In 1954, John Kenneth Galbraith offered a similar narrative of the top-formation leading up to the 1929 crash: “The temporary breaks in the market which preceded the crash were a serious trial for those who had declined fantasy. Early in 1928, in June, in December, and in February and March of 1929 it seemed that the end had come. On various of these occasions the Times happily reported the return to reality. And then the market took flight again. Only a durable sense of doom could survive such discouragement. The time was coming when the optimists would reap a rich harvest of discredit. But it has long since been forgotten that for many months those who resisted reassurance were similarly, if less permanently, discredited.”

I continue to have little doubt that the current market cycle will be completed by a 40-55% market collapse, with near-zero total returns for the S&P 500 on a 10-12 year horizon. Meanwhile, however, we have to accept that central banks have wreaked havoc on the ability of the financial markets to usefully allocate capital toward productive ends. Relevant warning signs that would normally prevent misallocation and malinvestment have been repeatedly disabled in the advancing half-cycle since 2009.

There’s a story of an American golfer playing a Scottish course, and having hit the ball perfectly, a massive gust of wind carries the ball wildly off-course. The golfer complains “Did you see that wind take my ball?” The caddy looks at him, unfazed, “Aye, now you’ve got to play the wind too then, don’t you?” We feel the same about central bank distortions.

The upshot here is that while our immediate outlook is hard-negative, moderate further improvement in market internals from here could suspend that outlook and shift us back to an essentially neutral stance - not because we would expect the completion of the current market cycle to be any less catastrophic, but because we’ve learned well enough that central banks are blind to the risks of speculative bubbles, and are perfectly willing to sacrifice long-term economic stability in pursuit of reckless and empirically baseless theories. We won’t get in the way again, and the fact that value-conscious investors have learned not to do so - that they have been forced not to do so - is to concede tragedy for the financial markets in the longer-run. Meanwhile, we’ll carefully walk the paths that emerge.

Across the pond in London, my friend Albert Edwards at Societe General notes the increase in political extremism, including the extreme right-wing Alternative for Germany party, and observes that much of this shift can be linked to economic policies that focus on nothing but debt expansion and financial-market distortion. “Quick-fix monetary QE nonsense has made virtually no difference to the economic recoveries other than to inflate asset prices, make the rich richer, inequality worse and make Joe and Joanna Sixpack want to scream in rage. They are doing so by rejecting the establishment political parties and candidates at almost every electoral turn and seeking out more extreme alternatives at both ends of the political spectrum. I have not one scintilla of doubt that these central bankers will destroy the enfeebled world economy with their clumsy interventions, and that political chaos will be the ugly result.”

I have to agree. This wouldn’t be the first time in history, nor even in the past century, that inept economic policy, class divisions, and growing nationalism led humanity to choose leaders that seduced them to abandon the better angels of their nature.

The same trend is apparent in our own political process. Speaking as someone who values human rights and diversity, some elements strike me as more offensive than others, but the current environment is bathed in the language of “enemy,” of division, of coercion, and of simplistic solutions. It also largely ignores the Federal Reserve’s role in creating the bubbles and crashes that still weigh on the economy, and now threaten a third act.

Lessons From The Iron Law of Equilibrium

Among the themes I’ve emphasized in three decades as a professional investor is what I’ve called the “Iron Law of Equilibrium” - every security that is issued must be held by someone until it is retired. The corollary is that there is no such thing as money going “into” or “out of” a secondary market. Rather, every share that is purchased by one investor is sold by another. Every dollar that comes into the market in the hands of a buyer goes out in the hands of the seller. As a result, we cannot, and should not, think of markets advancing or declining because “investors” as a whole have done anything. Rather, day-to-day changes in market prices reflect whatever movement is necessary to ensure that every buyer is matched with a seller, and vice versa. The net change in investment positions across all participants in a secondary market is always zero. If you instead take the absolute value of all individual changes in investment positions throughout the day, add them up, and divide by two, the resulting figure is trading volume.

When trading volume is low, it reflects a situation where most market participants are not changing their positions at all, so price movements are driven whether the small minority of traders who are most willing to buy are more eager, or less eager, than the small minority of traders who are most willing to sell. A large price movement on light trading volume indicates relatively high agreement among traders that the latest price movement is “right,” and requires no further change in their existing position (even if their existing positions are heavily long or short). In contrast, a large price movement on heavy volume typically indicates disagreement. This typically reflects a situation where trend-following and greed/fear trades have been triggered (buying on advances, selling on weakness) and prices have to move a great deal in order to induce value-conscious investors to make the opposite trades (selling on advances, buying on weakness).

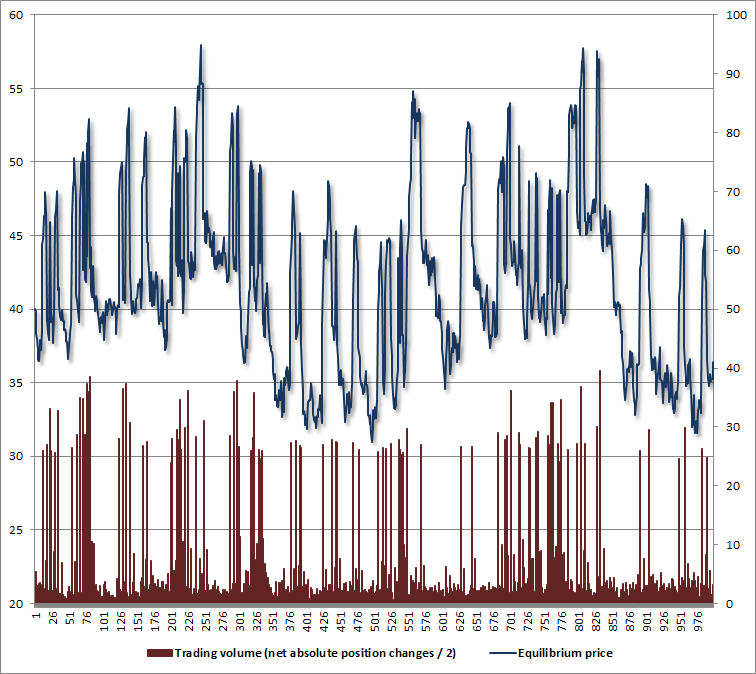

To illustrate these points, I put together a fairly straightforward simulation below. We assume a security that throws off a stream of cash flows that are subject to random shocks but mean-revert over time. One can work out the discounted value of the expected stream of cash flows algebraically. I’ve assumed two types of value-conscious traders - long-term investors that demand stock in proportion to its deviation from fair value, and short-term traders who accumulate the stock when it is oversold and go short when it is overbought. I’ve also assumed two types of trend-sensitive investors - one group that buys or sells in binary fashion depending on whether the price is above or below a moving average, and another group that sets demand based on rate-of-change momentum. At each point in time, the price is calculated by iteration: setting an initial candidate price, calculating the desired positions of each investor, and converging on an equilibrium price by numerical approximation until every buyer is matched with a seller. For simplicity, positions are measured as deviations from an equal allocation across investors.

Here’s a graph of what the resulting process looks like. I could make it all smoother by reducing the random component and slowing the mean-reversion, but this version makes some of the features we’re discussing easier to observe.

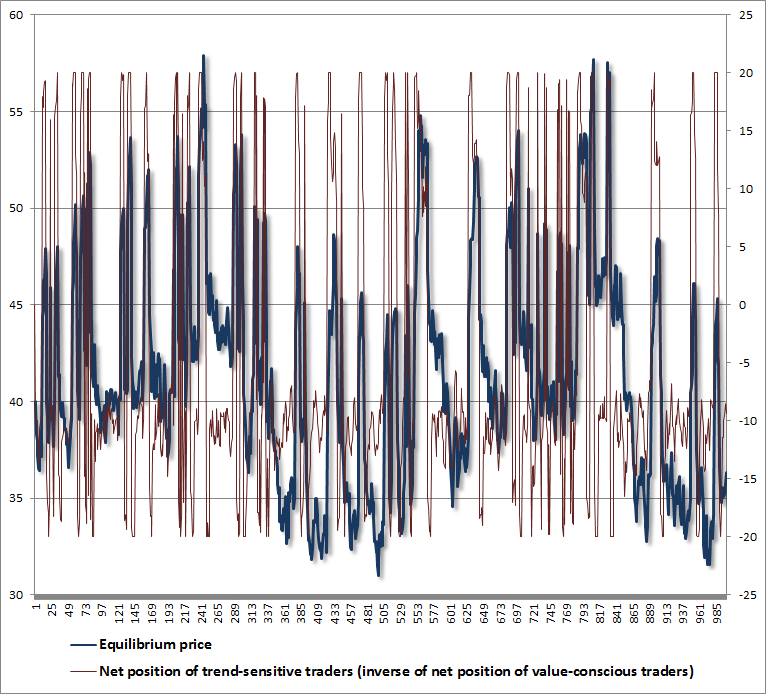

Because trading volume is based on the absolute changes in positions across traders, it’s not obvious what’s going on underneath the surface in terms of the desired positions of each group. The chart below breaks this out, and illustrates what’s driving price behavior. When prices are unusually elevated relative to the norm, it’s almost always because trend-followers (and other price-insensitive buyers) are “all in.” Those positions are - and in fact have to be - offset by equal and opposite underweights by value-conscious investors. A sudden increase in the desired holdings of trend-sensitive traders has to be satisfied by inducing a price increase large enough to give value-conscious investors an incentive to sell. Conversely, a sudden decrease in the desired holdings of trend-sensitive traders has to be satisfied by inducing a price decline large enough to give value-conscious investors an incentive to buy. Any tendency of investors to buy on greed and sell on fear obviously amplifies this process.

From this perspective (and one can show this in simulation), what we’re really interested in is not the balance between bulls and bears per se, but the balance of sentiment between trend-sensitive and value-conscious investors. Market tops emerge when trend-followers are beating their chests while value-conscious investors are nursing bruises from their shorts. Market bottoms are formed when trend-followers wouldn’t even touch the market, and value-conscious investors are bleeding from all of the falling knives they’ve accumulated. As I’ll note below, it’s best to combine aspects of both approaches.

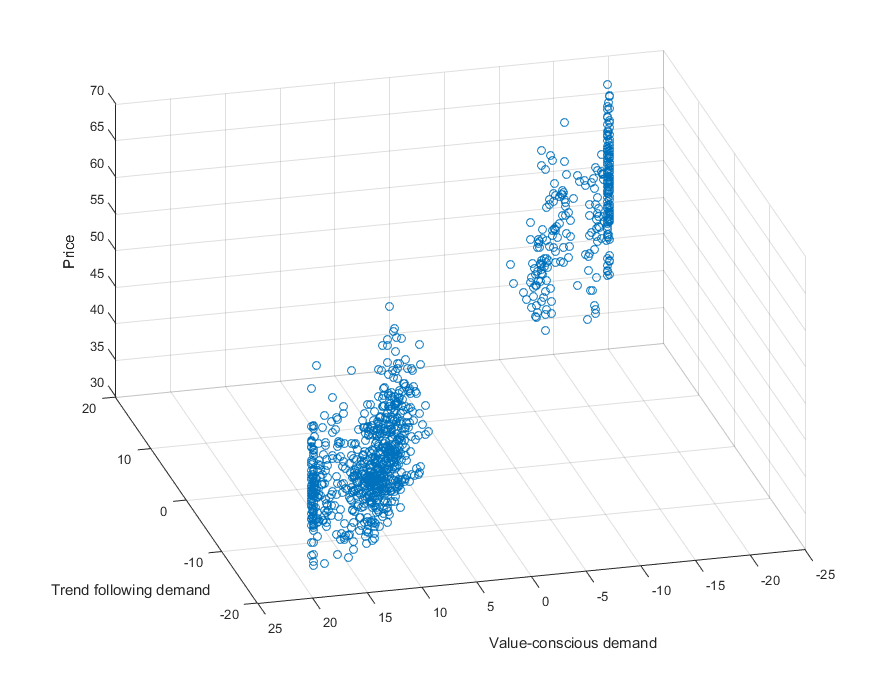

The chart below provides some additional insight in three dimensions. Trend-following demand and value-conscious demand are plotted along the bottom axis. You’ll notice that they are mirror-images of each other, as they have to be in equilibrium. Price is presented on the vertical axis. Note in particular that elevated prices are associated with heavy positioning by trend-following investors and underweighting or net-short positions among value-conscious investors. The reverse is true at depressed prices.

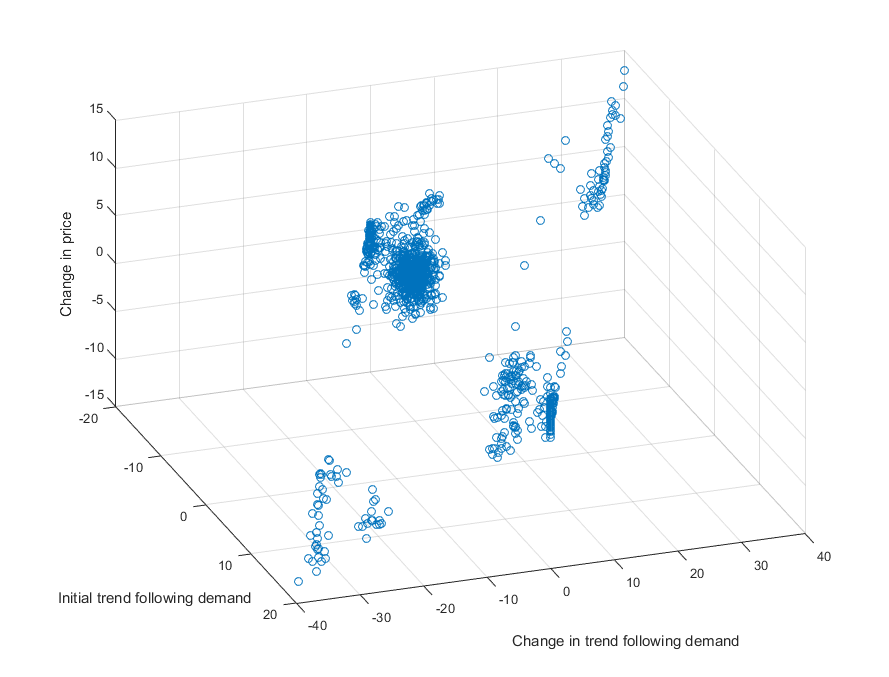

Following on this point, understand that the worst market declines typically emerge from conditions where value-conscious investors have been defensive for quite some time, and where trend-following speculators have been rewarded for quite some time.

The following chart offers further insight on that front. Initial trend-following demand and the subsequent change in demand are along the bottom axis, and the change in price is on the vertical axis. The most severe price losses are those where trend-followers are “all in,” followed by an initial deterioration in market action that prompts them to reduce their desired holdings. On the chart below, the worst outcome can be seen on the bottom left, when a high initial level of trend-following demand is followed by a significantly negative change in demand (essentially, a concerted attempt to exit). In contrast, the strongest market advances are those where trend-followers are out (offset by value-conscious investors being all-in) and an initial improvement in market action prompts trend-followers to abruptly increase their desired holdings. The most bullish situation can be seen in the back, upper right corner of the chart below.

The analysis above demonstrates why, in market cycles across a century of history, the strongest market return/risk profiles we identify are associated with a material retreat in valuations that is then joined by an early improvement in market action. By the time value investors are all-in, trend-followers are out. They then have to pry stock away from committed value investors once market action begins to improve, driving prices sharply higher. Conversely, the most severe market collapses are associated with steep overvaluation that is then joined by initial deterioration in market action. By the time trend-followers are all-in, value investors are out, and attempts by trend-followers to exit require prices to decline until skittish value-conscious investors are willing to absorb the shares being offered for sale.

This dynamic is why I expressed concern in February about the prospect for a market crash if the widely-followed support area around 1820 on the S&P 500 was broken. This concern will return if we approach that area again. Indeed, even a break of the 200-day moving average around 2015 could trigger binary (“all or none”) exit attempts. We’ve been fairly neutral in recent weeks, largely because improvement in various trend-following measures suggested we stand aside until that trend-following demand was exhausted, as indicated by a fresh overvalued, overbought, overbullish syndrome. In prior market cycles, the emergence of this syndrome would usually be the end of the matter, and would set the market up for a steep “air pocket” decline or worse.

The main wild card here is that a moderate further improvement in market internals could signal a more durable shift toward risk-seeking among investors. That could return us to a largely neutral near-term outlook. We’ll take the evidence as it comes, but we can’t rule that out. In the face of ridiculous statements by Janet Yellen that there are no warning signs apparent in the equity or credit markets, we have to allow for the possibility that the Fed is blind enough to encourage speculation until another financial crisis becomes unstoppable.

Valuations remain obscene from a historical standpoint, and my sense is that trend-following and greed-trades are most probably “all in." Yet despite a fresh "overvalued, overbought, overbullish" syndrome, we'll yield to a relatively neutral near-term outlook if market internals improve much from here. At present, Investors Intelligence reports that only 21.7% of investment advisors are bearish, and put/call ratios are severely skewed to the bullish side. The themes cited by bulls feature trend-following considerations and statements like “this chart is bullish.” The themes cited by bears feature value-conscious considerations and statements like “at 38.3%, the value of stocks as a percentage of household financial assets is at the second-highest level in history.” This is a setup that, like 2000 and 2007, cannot help but invite collapse over the completion of the market cycle. The pent-up risks will become increasingly difficult to stem the longer central bankers attempt to “talk” the market higher at every retreat.

In recent years, disciplined, value-conscious investors have been attacked with a bat by central bankers insistent on encouraging speculation as a policy tool. Undoubtedly, the hesitation of value-conscious investors to lean against a hypervalued market (and even we’ve abandoned that willingness in periods where market internals are uniformly favorable) has contributed to yet further misvaluation. All of this will end badly. Again, our immediate view is hard-negative, but we’ll be alert to any improvement in market internals. Regardless of near-term prospects, I have little doubt that the S&P 500 will complete the current cycle by losing half of its value, as it has always done from similar valuations on historically reliable measures (see last week’s comment), even in periods prior to the 1960’s when interest rates often visited similarly low levels.

© Hussman Funds