In August 2020, as the global pandemic was straining emerging countries’ ability to make debt payments, we published a white paper – “Sovereign Contingent Bonds: How Emerging Countries Might Prepay for Debt Relief” – introducing the concept of “sovereign coco bonds,” a way for countries to structure bond agreements to allow for more flexible policy options in the face of a crisis.

2022 has hit investors with an unprecedented 1-2 punch of sharply negative returns in both the equity and fixed income markets, but our Strategic Income team feels the selloff has created attractive opportunities in high yield bonds.

Senior Sovereign Analyst Jon Levy tackles three big questions on the Bank of England's recent operations.

Medical Properties Trust (MPW) claims to be the second largest nongovernmental owner of hospitals in the world.

After enjoying a long period of deflationary conditions, the global economy is being pushed by a wide range of forces toward a new and more difficult equilibrium.

What I want to talk about today is this moral panic we’re having about inflation.

The strong dollar remains a risk to corporate profits and asset prices as the impact on the global economies grows.

The Fed’s inflation-fighting efforts have resulted in a stronger dollar relative to most other major currencies.

U.S. stocks are mixed and subdued as the markets digest another hot inflation report in the form of the September Producer Price Index.

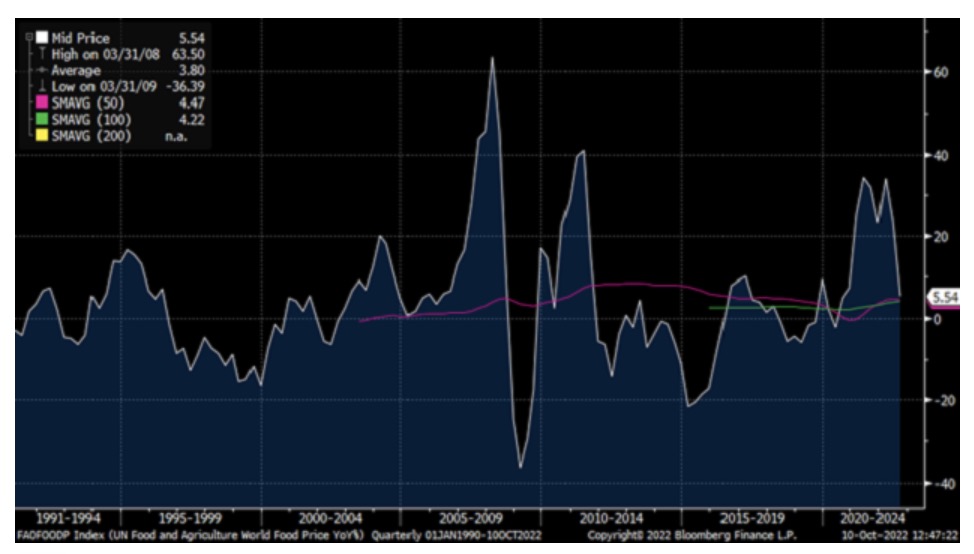

The OPEC+ plan to curb oil production complicates the global economic, inflation, and geopolitical outlook and will likely lead to higher prices for key commodities.

"Carry on!!" was the gruff but oh so welcomed command screamed at me by Marine drill Sergeant Jo Quinn Cruz in October of 1967.

A couple weeks ago, in our quarterly strategy report (see: QSR-Has Innovation Bottomed?), I argued that it appeared that innovation had bottomed.

Robert Leroy Higgins, owner of precious metals dealer Argent Asset Group and the First State Depository (FSD) in Delaware, is in hot water with the Commodities Futures Trading Commission (CFTC).

The era of “TINA”—short for “there is no alternative” and describing a phenomenon where bond yields were so low that many investors felt they had no choice but to invest in stocks, even at stretched valuations—has given way to a market where they can “pay attention to the yield(s).” Or “PATTY,” for short.

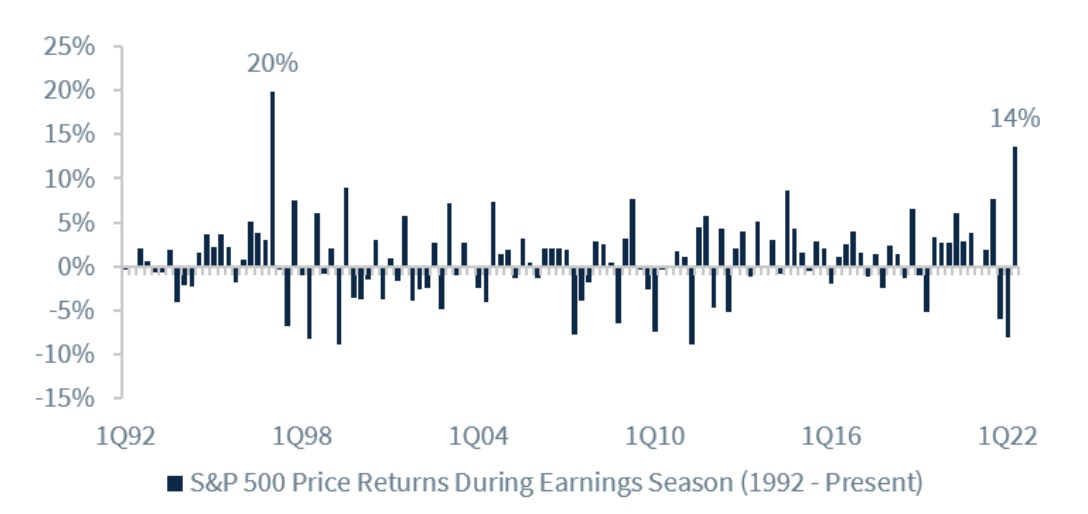

When you look at expectations for corporate earnings for the third quarter, you get a bunch of mixed messages.

Cannabis stock Innovative Industrial Properties Inc. (IIPR) claims to be “the leading provider of real estate capital for the regulated cannabis industry.”

U.S. equities are mixed as investors await this week’s highly anticipated September inflation data.

It is as though the finance world decided to take a page out of the music industry's book by recycling a melody with only slight variations.

The World Bank should be a major vehicle for crisis response, post-conflict reconstruction, and, most importantly, for supporting the huge investments necessary for sustainable and healthy global development.

We do not expect the current environment of weakening economic growth to dislodge the long-term staying power of our investment themes and have also taken great care to try to insulate against the most pernicious risks that inflation poses to equity investments.

In recent months, the economy has shown remarkable resilience in the face of a cyclical downturn.

Growth stocks enjoyed a supercharged post-COVID rally before higher rates and inflation dealt a heavy blow in 2022.

Recent economic reports further undermine the politically-motivated argument from earlier this year that the US was already in a recession.

Irvine, California-based Masimo makes non-invasive patient monitoring, measuring and sensing technologies that improve patient care in the hospital, the home, and on the go.

“Market instability” remains the most significant risk to central banks globally.

The Great Moderation has given way to the Great Stagflation, which will be characterized by instability and a confluence of slow-motion negative supply shocks.

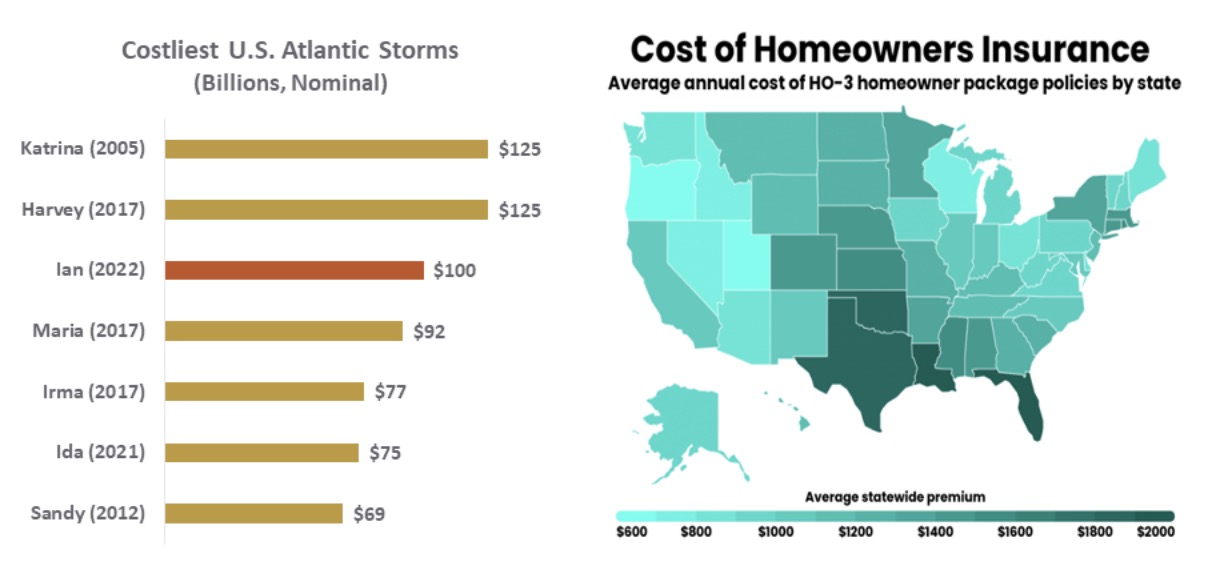

Hurricane Ian has laid bare the challenges facing Florida’s insurance industry.

Evidence of a cooling labor market is emerging.

The worst may be behind gold mining stocks. Since hitting a 52-week low on September 26, they’ve risen about 18% and today notched their second straight week of positive gains.

Today I want to talk about why the labor market is so out of balance. Some of this is new and some has been brewing for many years. We will end with some commentary on yesterday’s unemployment report.

Review the latest Weekly Headings by CIO Larry Adam.

A recent MarketWatch article discussed JPMorgan’s Chief Operating Officer, Daniel Pinto, views about a coming mild recession.

October will test the Fed’s resolve.

The fourth quarter is starting with a bang for precious metals markets.

The world seems an increasingly uncomfortable place for traditional stock and bond investments.

The latest jobs market headlines have been discouraging.

One of the themes I’ve discussed in recent months is the disconnect between a 40 year high in inflation and the lack of experience money managers have in understanding the monetary policy required to deal with such high inflation, including managers with 25 to 30 years of experience

For the last decade, central bank gold purchases have accounted for between 10% and 15% of total gold demand. George Milling-Stanley of SSGA takes a look at historical gold purchasing cycles over the past 50 years…

We are in the middle of a giant short squeeze, and it is going to get even bigger.

U.S. stocks are trading modestly lower in pre-market action with the markets awaiting tomorrow's key September nonfarm payroll report.

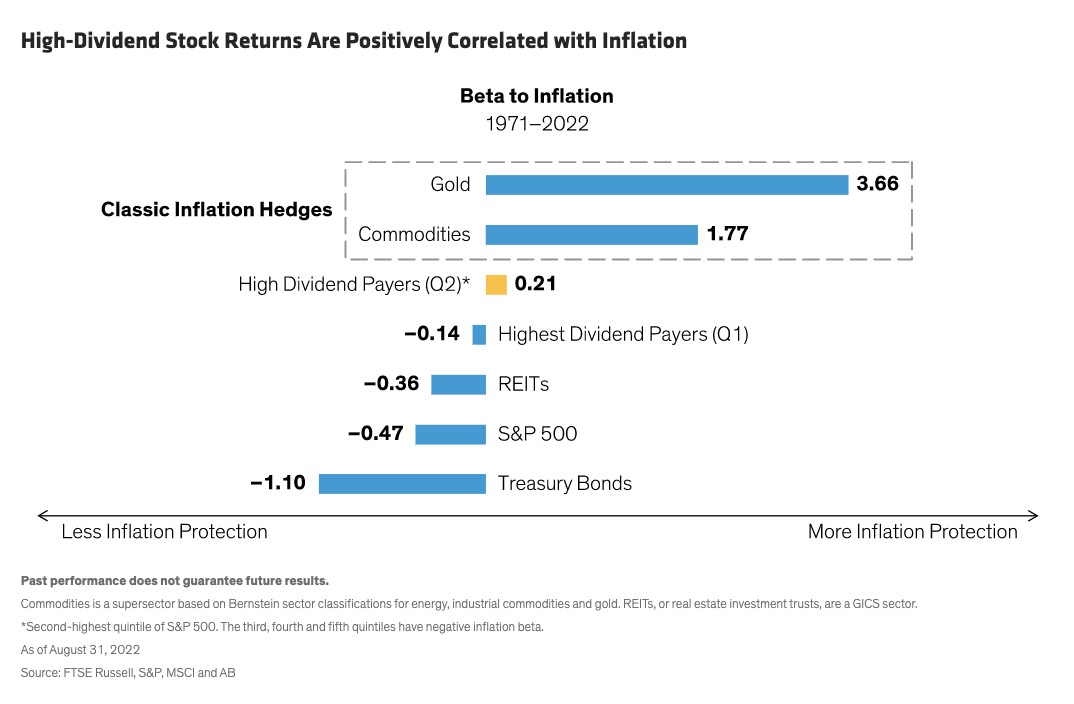

Many investors are searching for assets that can help protect portfolios from inflation.

Rising rates hurt investors; claims on profits in the future are simply worth less if you discount them at a higher rate.

Bonds are typically considered safe investments. However, there were decades of negative real returns. Drawdowns reached 50% for U.S. Treasuries and Bonds.

Stocks extend yesterday’s gains as rates continue to ease.

As billions of fans eagerly await the 2022 World Cup, CIO Larry Adam draws parallels between the globe’s most popular sport and the current investing environment.

The list of assets that have risen year-to-date is both short and odd: energy, broad commodity indexes and the dollar.

After enjoying a long-running bull stock market, the recent drop in stock prices is causing investor angst.

Last night, the Reserve Bank of Australia stopped short of another 50bps hike to its overnight cash rate.

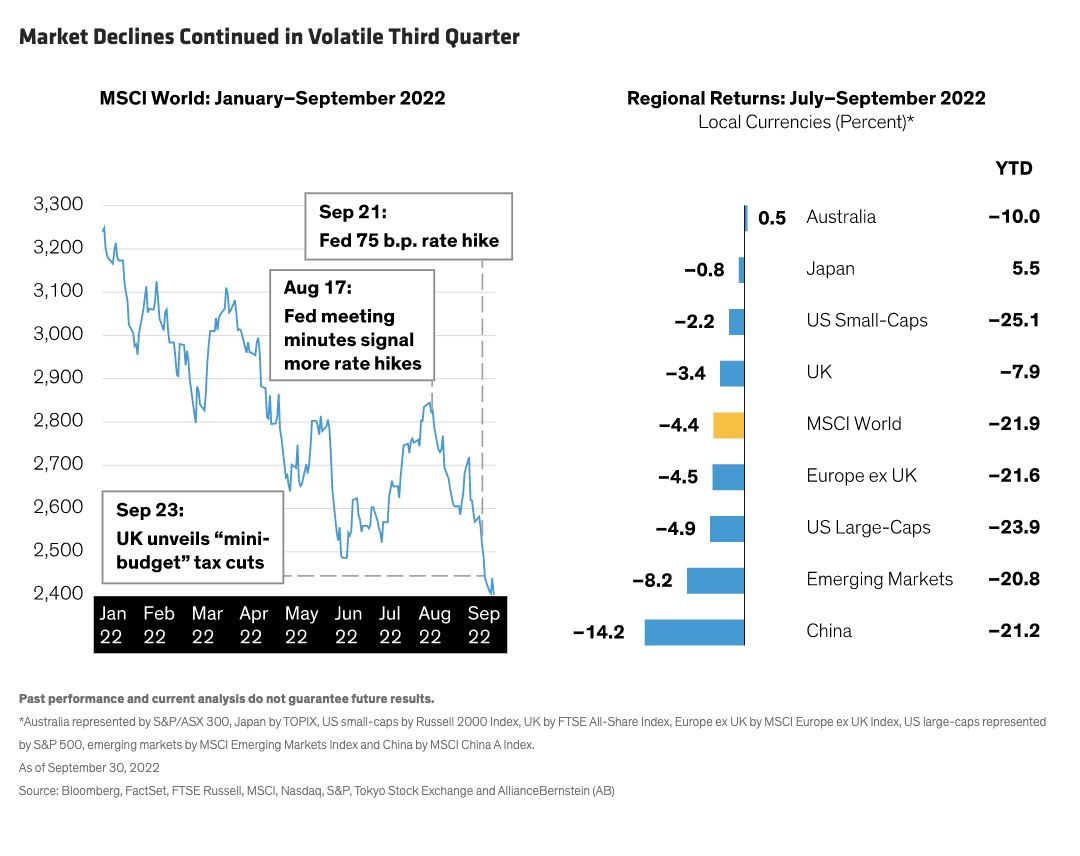

Equity market volatility persisted in the third quarter as investors came to terms with a new reality of high inflation and rising interest rates.

On August 16th, President Joe Biden signed the Inflation Reduction Act into law, ending months of uncertainty over whether congressional Democrats would ever reach agreement on a compromise budget reconciliation bill.