Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- Anticipating a mild recession in 2023

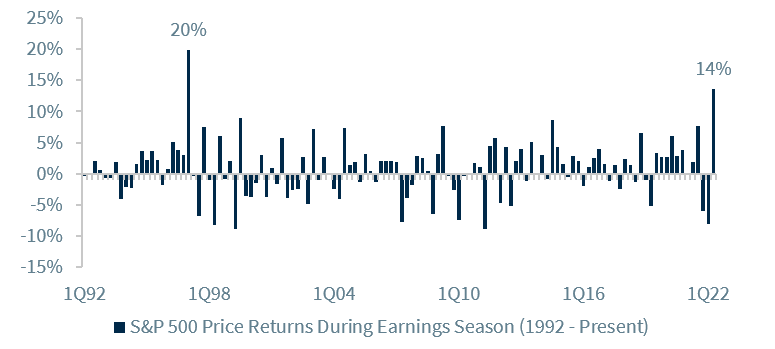

- The third quarter 2022 earnings season could be better than feared

- Inverted yield curve has us focusing on quality

Are you ready for some football? Not American football, but European football — otherwise known as soccer! For the five billion spectators awaiting the start of the 2022 World Cup in Qatar this November, the sport is the epitome of speed and agility. But for the players on the 32 participating teams, it is so much more. It is years of training to perfect field awareness and anticipation. It is making decisions not only quickly, but under pressure. The World Cup coincides with a time of significant awareness and anticipation in the markets, and investors are questioning their decision making in the midst of so many unknowns. Will the economy enter a recession? How high will the Fed raise interest rates? When will inflation abate? As we enter the final quarter of 2022 and look to the months ahead, navigating these markets will prove to be a time for finesse, and we will borrow from the sport of soccer to articulate why.

- We May Not Want The Fed To Win The Golden Boot | In the World Cup, the top scoring player is awarded with the Golden Boot, and if there was such an award for tallying interest rate hikes, the Federal Reserve (Fed) woulddefinitely be in contention. However, investors want to see the Fed as a well-rounded player — not only scoring rate hikes to tame inflation but also defend against the feared end of the economic expansion. The Fed’s third consecutive 75 basis point interest rate hike lifted rates well into restrictive territory, and the further the Fed moves above the 4% threshold the greater the likelihood of a recession. Since our peak fed funds forecast is 4.5%, we are anticipating a mild recession beginning in the first quarter of next year. However, we do not think the economy will experience a severe recession as there are no ‘excesses’ like the excessive leverage, over hiring (we still have over 10 million job openings!), or bubble-like valuations (e.g., dot.com and housing bubbles).