The US equity market, with the S&P 500 hovering near all-time highs, is expensive. This isn’t controversial. Depending on which measure you use, US stocks have arguably been overpriced for several years.

Central bankers expect de-dollarization to continue over the next several years, with gold and other currencies taking on a growing role in the global monetary system, according to a survey by the Official Monetary and Financial Institutions Forum (OMFIF).

Almost two decades ago, when trillions of dollars in private housing debt proved unsustainable, governments had to step in to prevent the worst financial crisis since the Great Depression from eclipsing it.

As economies become increasingly electrified and power demand grows, the transmission, storage and infrastructure needed to support reliable electricity delivery are evolving. In our view, these trends are creating attractive opportunities across the technologies and infrastructure that underpin the energy transition.

The capital markets have become an increasingly complex space for investors, complexities that are heightened by the sheer number of ways one can invest.

When Mark Zuckerberg gets a bold new business idea, he likes to throw money at it. Last summer, he dropped $14.3 billion for a 49% stake in Scale AI, allowing him to poach its wunderkind founder Alexandr Wang to lead a new project to build artificial-intelligence systems that surpass human intelligence.

Private equity may be our No. 1 economic boogeyman. It is blamed for rising real estate prices, poor medical care, and ruining many of the businesses we used to love.

Chris Galipeau discusses high-conviction insights that go beyond media headlines.

Close to 40 years ago, I moved from Canada to the U.S. after acquiring a controlling interest in U.S. Global Investors. I’ve built my entire life and career here, and in all that time, I’ve never stopped marveling at my adopted country.

What is remarkable about Livermore is that his rules are still incredibly valuable. The markets he traded in no longer exist. The technology, the communication speeds, and the regulatory framework of his day are unrecognizable compared to today. But the principles and behavioral patterns he identified are as operational in 2026 as they were a hundred years ago.

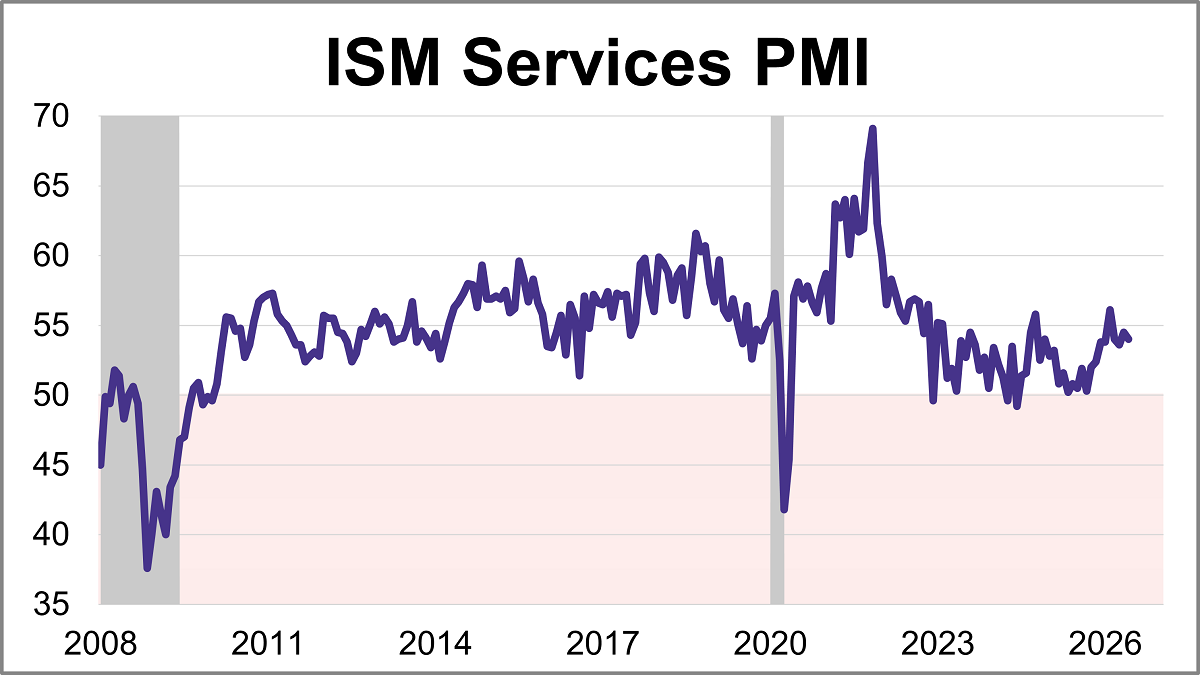

The Institute for Supply Management (ISM) released its June Services Purchasing Managers' Index (PMI), with the headline composite index at 54.0. This was slightly lower than the forecast of 54.2 but keeps the index in expansion territory for a 24th consecutive month.

The US industrial robot industry is characterized by low growth and highly customized projects. Artificial intelligence holds out the hope to change that, especially when it comes to robots that can move and work safely around humans.

Today’s market backdrop reflects a tension between expectations and reality. Despite higher oil prices and plenty of geopolitical noise, the US economy remains resilient and durable, supported by steady consumer spending, a labor market finding its footing, ongoing fiscal support and a surge in AI and infrastructure investment.

The second quarter wraps up today, and it was a good one. With the S&P 500 having returned more than 14% (including dividends) with just one trading day left, it will almost certainly end up being the best quarter for the index since the second quarter of 2020. Technology was the leader despite the June weakness.

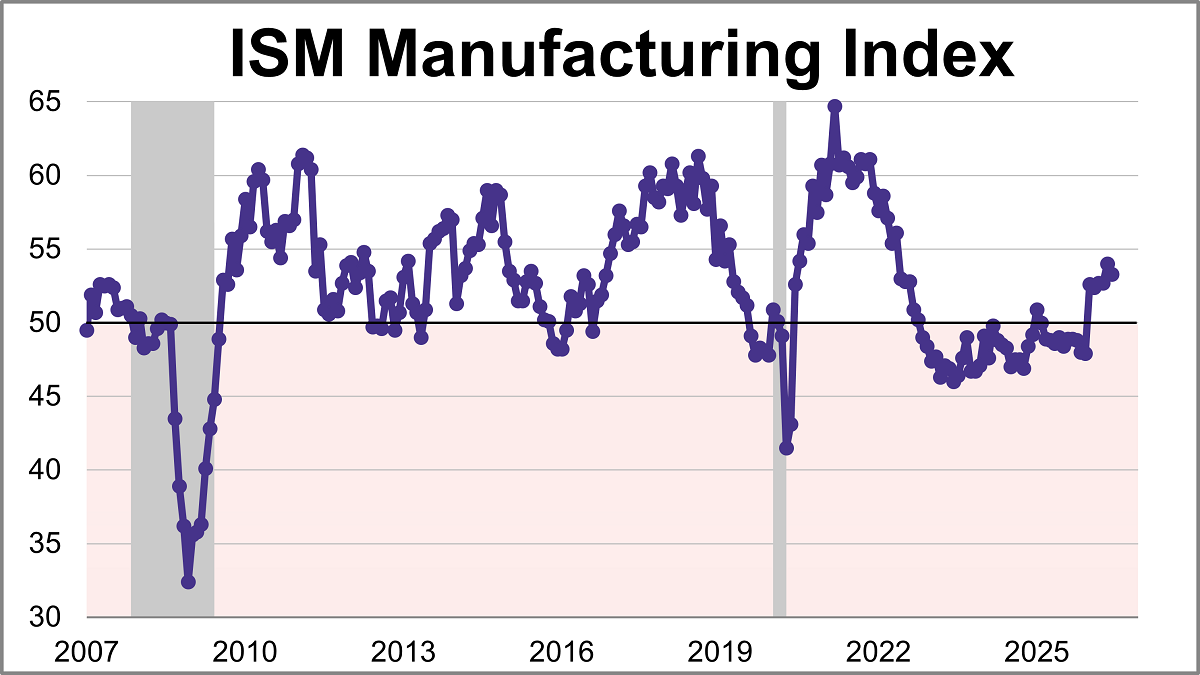

The Institute for Supply Management (ISM) manufacturing purchasing managers index (PMI) came in at 53.3 in June, down from 54.0 in May, marking slightly slower growth. The latest reading was just below the 53.8 forecast and is the index's sixth straight month in expansion territory.

In our view, this divergence continues to reflect how the buildout of artificial intelligence (AI) is influencing both the economy and markets as it progresses across the value chain, even as the associated costs continue to climb.

Chip stocks are heading for their best quarter ever, extending an extraordinary start to the year driven by insatiable demand for artificial intelligence equipment. But after recent jitters sent the stocks tumbling, investors are wondering how much further the rally can go.

The money is REAL. The question was never whether it exists. It’s who’s spending it, and what they borrowed to do it. When the wall of cash and the bottom half finally commit to risk at the same moment the Fed turns hawkish, that’s not the start of something. That’s the part of the cycle where the careful investor gets paid to be careful.

Ten years ago this week, the world watched the United Kingdom vote to walk away from the European Union. While the political class was clutching its pearls and every talking head on television was promising Armageddon by Christmas, I told you something different.

Jesse Livermore’s prolific trading stories about the fortunes he made and lost are well documented in two books. While his career was marked by the incredible volatility of his wealth, and some consider him a failure as he died broke, his market knowledge is invaluable. Accordingly, we share his 21 market rules.

European firms in critical sectors like nuclear energy and quantum computing are flocking to the US, despite efforts by European authorities and bourses to make the region’s markets more appealing and accessible.

The Federal Reserve’s new chairman, Kevin Warsh, plans to convene no fewer than five task forces to review the central bank’s methods and operations. They will ask how the Fed can improve its communications, balance-sheet policy, use of data, understanding of “productivity and jobs in an era of transformation,” and delivery of price stability.

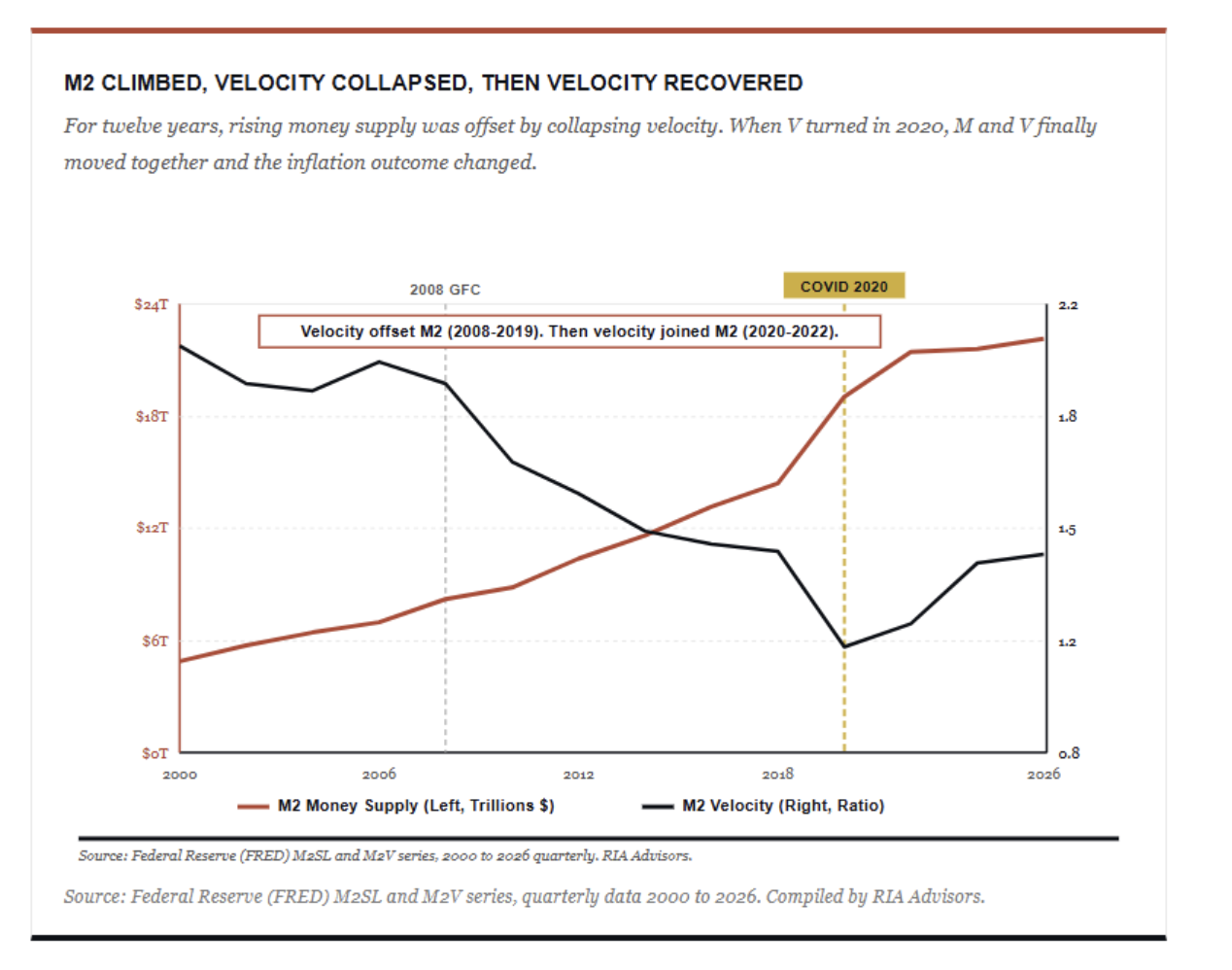

Friedman was reasoning from the equation of exchange, MV = PQ. Money times velocity equals prices times real output. It’s an identity, not a theory. Where it gets interesting is when you ask which variable does the work.

The dominant theme this week was a tug of war between improving macroeconomic conditions and weakness in parts of the technology sector.

The dollar is wrapping up one of its best months in a year as a raft of Wall Street banks see a turnaround of fortunes for the US currency.

As the market continues to broaden in 2026, a balanced approach matters more than ever.

AI is both a foundational technology and the ultimate replacement product, which we believe explains why it has attracted unprecedented levels of capital and why the investment opportunities are so compelling.

Halfway through 2026, this market perspective is harder to write with confidence than most. That’s not a phrase I use lightly. Over four decades of markets, there have been plenty of uncertain moments, but the number of significant, unresolved issues I’m watching right now is unusually high.

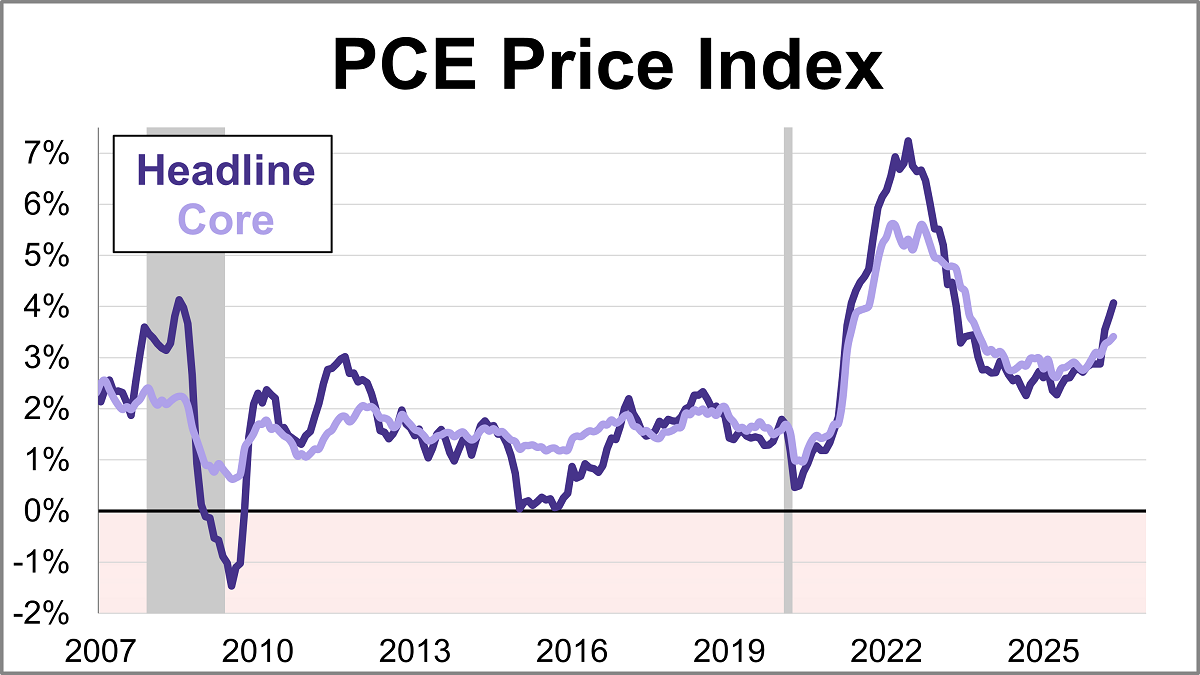

The Federal Reserve’s preferred inflation gauge, the core PCE price index, climbed 3.4% year-over-year in May. This marks the highest level since October 2023 and marks a pickup from April's 3.3% reading. On a monthly basis, core prices rose 0.3%.

What if the debt crisis investors have feared is not still ahead, but already here, unfolding in plain sight? In his June insight, Richard Bernstein, Global Head of Macro & Customized Investing, makes the case that the market may already be penalizing U.S. fiscal excess, not through a dramatic collapse, but through a slow burn with real consequences for investors and the broader economy.

According to Gleason, the freezing of Russian assets following the 2022 invasion of Ukraine accelerated the global push toward de-dollarization. Nations around the world took notice that access to the dollar-based financial system could be restricted, increasing the appeal of gold as a reserve asset that cannot be frozen or sanctioned by foreign governments.

In a digital-first environment, reputation is no longer a byproduct of success; it is an asset class in its own right. For ultra-high-net-worth families, reputation capital can influence investment opportunities, business partnerships, philanthropic impact, and multigenerational legacy. It can also be exposed, amplified, or undermined in real time.

A massive profit warning from BMW AG last week delivered yet more evidence that Germany’s automaking business model is broken. With Volkswagen AG’s top executives reportedly worried about existential threats to their company, BMW’s woes aren’t isolated.

Here’s the setup most investors are underrating right now. Over the next two weeks, the tape will trade on plumbing rather than fundamentals. We just cleared the largest options expiration in history. Quarter-end pension selling comes next, and then July 1 reopens the passive-money firehose into a market that already routes forty cents of every S&P 500 dollar into ten stocks.

On Monday, President Donald Trump announced that the U.S. and Iran have reached a peace deal to reopen the Strait of Hormuz, the 21-mile chokepoint through which roughly 20% of the world’s oil supply normally flows.

Alan Greenspan, the Federal Reserve chairman proclaimed a wizard for guiding a then-record US economic expansion, only to see his luster dimmed by the financial crisis that erupted less than two years after he stepped down, has died. He was 100.

SpaceX is selling investment-grade bonds for the first time in what’s expected to be the start of a massive borrowing spree to fund the company’s AI ambitions following its record $75 billion IPO.

As the summer economic landscape takes shape, investors are navigating shifting monetary policy, stubborn inflation pressures, and unexpected market momentum. This week’s snapshot breaks down the most critical updates and data releases from the past week to give you a clear view of where the economy is heading.

Co-packaged optics, the technology of integrating lasers and optical components directly into network switches rather than using pluggable modules, is becoming the standard architecture for large-scale GPU clusters, and Nvidia needed to lock in supply for the buildout it is planning.

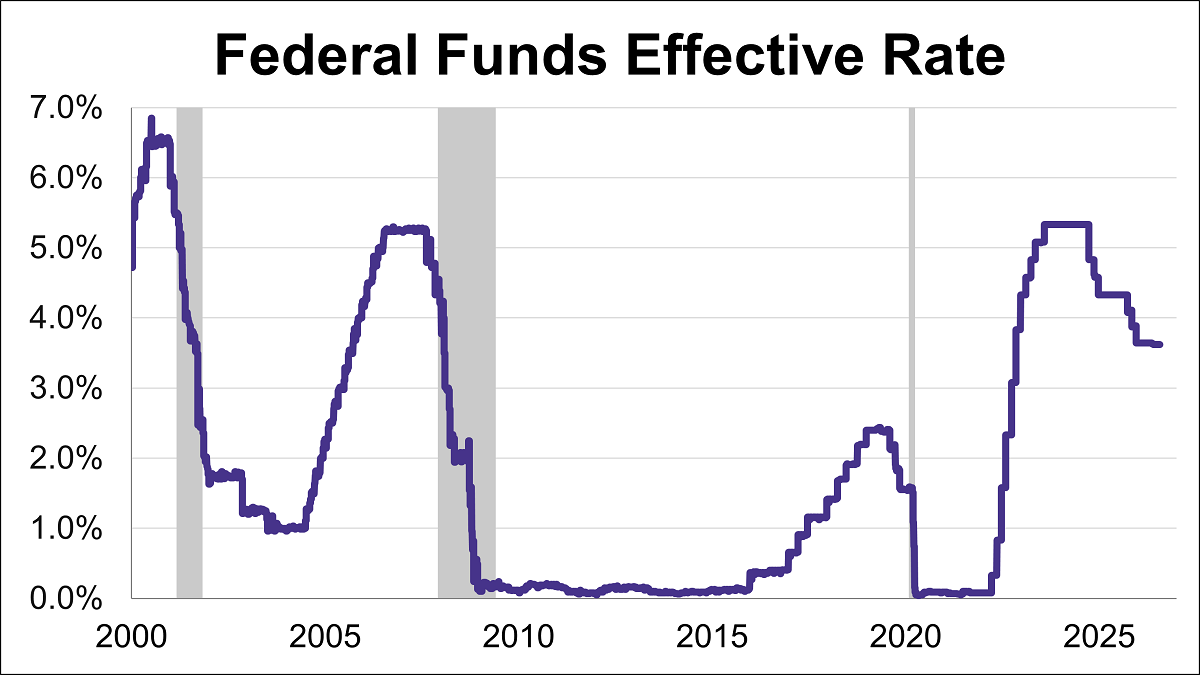

The Federal Reserve concluded its fourth meeting of the year by holding the federal funds rate (FFR) steady in the 3.50%-3.75% range.

Participate in artificial intelligence (AI) investing long enough and you’re apt to hear plenty about this disruptive technology’s substantial power demands. Market participants know the anecdotes. For instance, some data centers consume more power than states. Another one: Data centers in aggregate consume more power than nearly all of the world’s countries.

In my 45 years in the investment business, we’ve observed numerous peaks of excitement. In 1987, a bull market that started at a 1982 bottom below 800 on the Dow Jones Industrial Average (DJIA) peaked at 2,722. It then crashed 43% in 78 days.

The instinct when deploying any new technology is to start small. Run a pilot. Test with a subset of data, a single team, or a simplified version of the real workflow. That instinct is sensible — but with AI agents, it carries different risks than those that exist with traditional software.

The catalyst that turns a healthy pullback into something deeper won’t be a single oil-soaked CPI print. It’ll be the moment forward earnings expectations start to roll over while valuations sit at the high end of history. We aren’t there yet.

A massive advisor retirement wave is reshaping wealth management. Discover how $2.5 trillion in assets may fuel industry transformation.

What prediction markets add is something equities never offered: a way for thousands of people to sell small bits of information — a logistics clerk’s observation, a local journalist’s hunch — that are individually worthless and collectively a forecast.

Gold has always had a way of testing investors’ expectations. Just when the headlines appear most supportive—inflation is rising, geopolitical risk is escalating and confidence in fiat currency is being questioned—gold can suddenly move in the opposite direction.

The IPO market is bubbling with excitement. The headlines surrounding the IPOs are hyperbolic, banker fees are enormous, and social media is teeming with bullish sentiment on how high the new shares may trade after going public. While that is all great for clickbait, nobody is asking the most important question. Where will the money come from?

This is the underlying question in several books and articles that have been published recently, most notably Kenneth Rogoff’s “Our Dollar, Your Problem,” and Barry Eichengreen’s “Money Beyond Borders: Global Currencies from Croesus to Crypto” — the latter of which is the subject of this review.