How to Invest Smarter in the Race for Electrification

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAs economies become increasingly electrified and power demand grows, the transmission, storage and infrastructure needed to support reliable electricity delivery are evolving. In our view, these trends are creating attractive opportunities across the technologies and infrastructure that underpin the energy transition.

Power Needs Are Growing

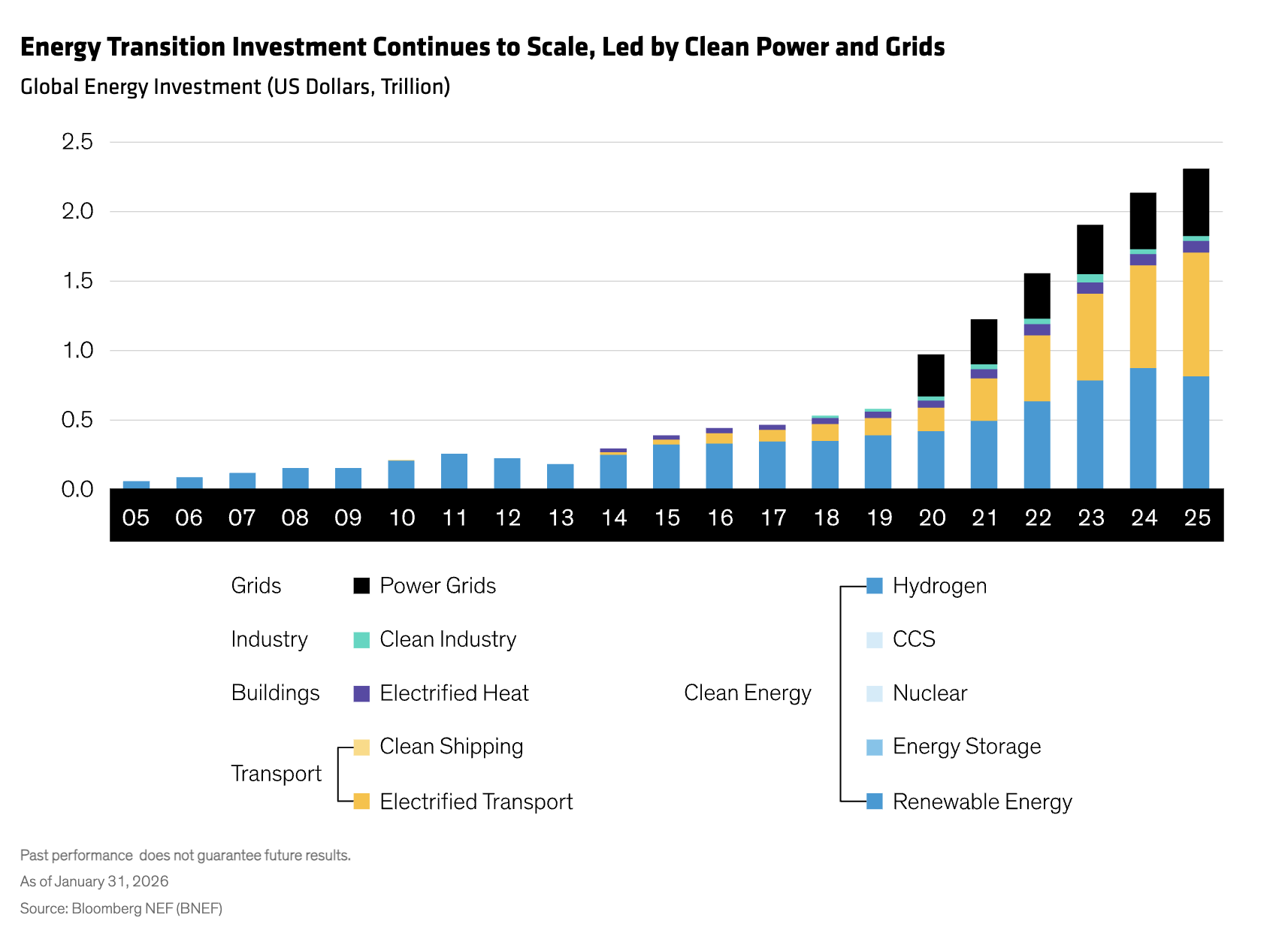

Power needs across the world are growing at a pace and scale that will require multiple sources of generation. Renewable energy projects are set to become a much larger part of the energy mix because of two key advantages: low costs and speed to market. While market and policy conditions may influence deployment in some regions, we believe renewable energy’s long-term growth trajectory remains intact (Display).

See more: The Energy Pivot: Establishing Supply in the Face of Historic Demand

The Need for Speed

Speed to market is an important consideration. In the US, for instance, AI is substantially increasing power demand even as older, higher-cost coal-fired power plants are being retired.

Rising power needs have been driving demand not only for renewable energy but also for gas-fired generation, reciprocating gas engines and nuclear power.

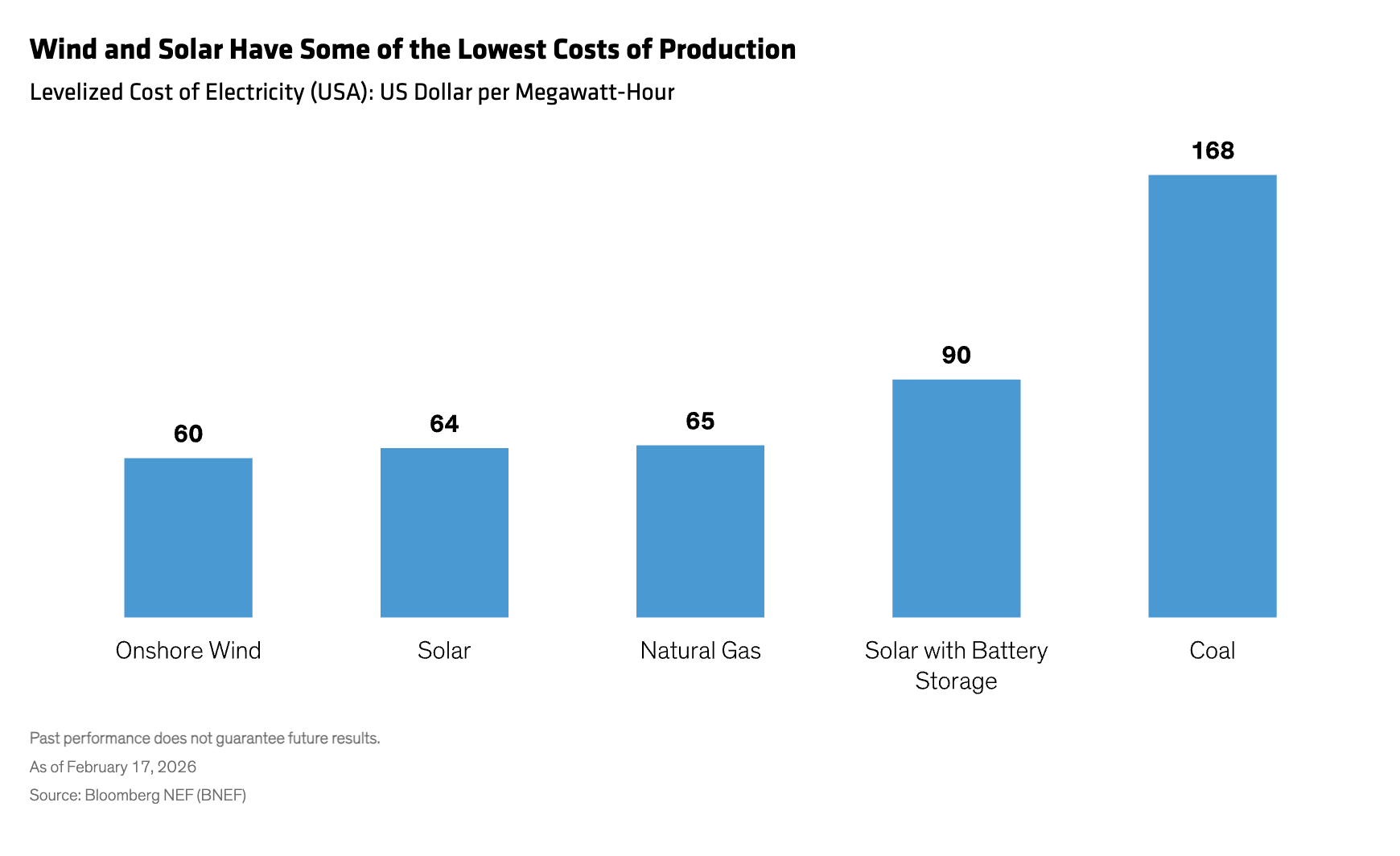

Even so, wind and solar are often the most viable additions to the power mix for two reasons. They can come online quickly and, when paired with battery storage, remain cost-competitive with fossil-fuel alternatives even without subsidies.

For instance, because order books for natural gas turbines are sold out for many years, adding fossil-fuel power often takes longer. And while adding battery storage increases the cost per megawatt-hour, it helps make renewable power more reliable. As a result, regulators may allow data-center projects faster grid connections if they include on-site battery storage. In addition, equipment costs have fallen to historic lows, and the cost of producing clean power continues to decline globally (Display).

All else equal, a loss of US government subsidies for renewables would make gas relatively more attractive. But in our analysis, wind and solar remain viable based solely on economics, and continued robust state and utility spending further supports utility-scale, commercial, industrial and community projects.

Of course, the path to renewable profits and returns hasn’t been smooth. Some renewable-energy developers have been badly hurt by post-COVID interest-rate rises and cost inflation, and even at current share price levels we believe investors should be highly selective in this subsector.

Energy Infrastructure Needs Upgrading

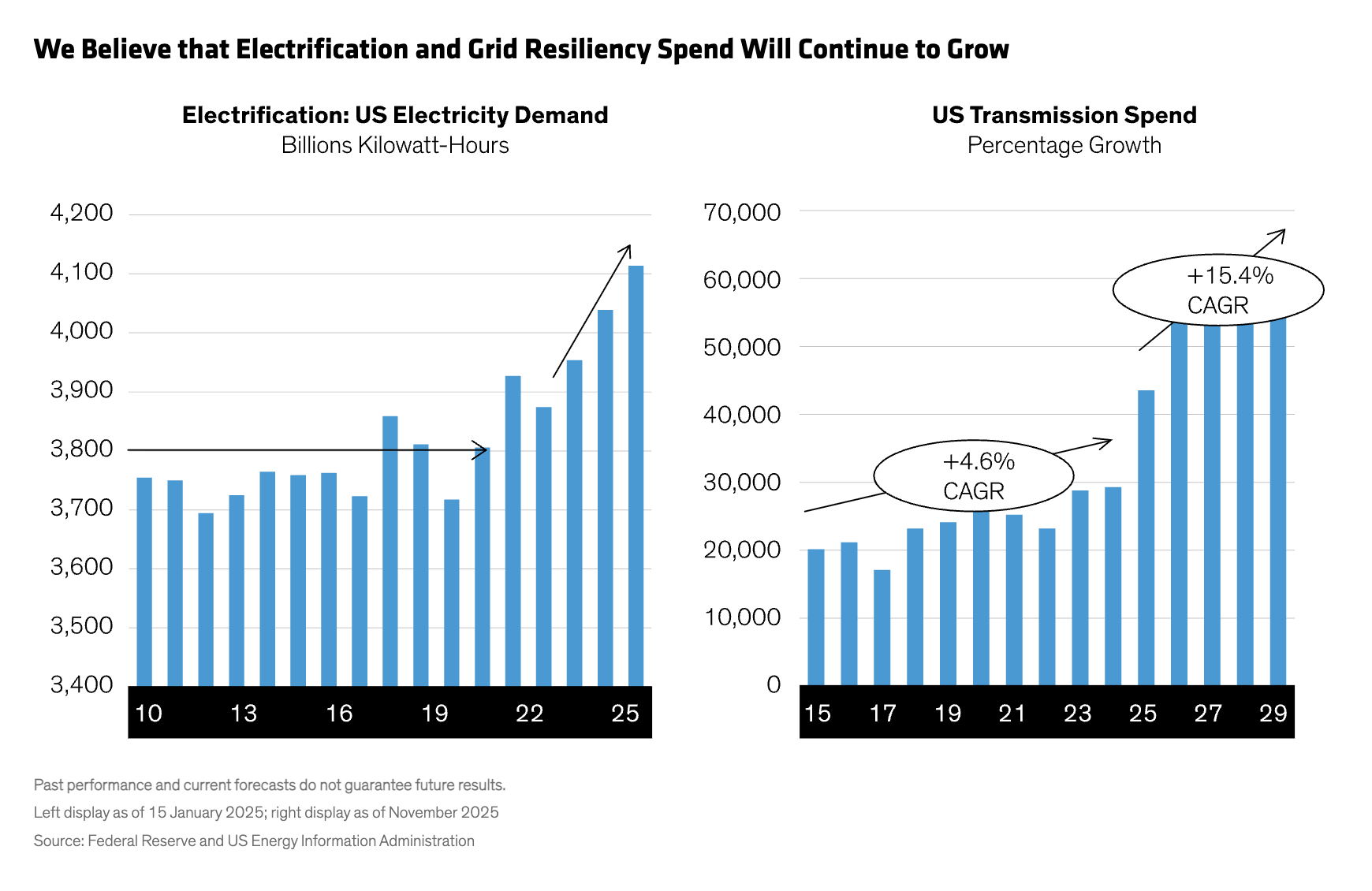

Grid upgrades and reinforcement will be critical to meeting rising power demand (Display). In the US and much of the developed world, grids are approaching or have exceeded their planned life. Yet these aging grids must carry massively increased loads, driven by AI-related power demand and the growing need for resilience against climate, geopolitical and other risks.

Companies such as Prysmian (copper and fiber cables, systems and accessories), Hitachi (cables and transformers), Hubbell (cable distribution) and Schneider (smart-grid solutions that improve grid reliability and flexibility) have benefited from increased grid spending. In many cases, demand remains strong and order backlogs extend several years into the future. In China, Contemporary Amperex Technology (CATL: battery manufacturing) also has a substantial order backlog. Investors will need to be selective, however, as not all component suppliers benefit from the same competitive advantages.

Watch Points for Investors

Investors should pay particular attention to companies’ operational efficiency metrics and to the regulatory, competitive and market factors that could materially affect potential investments.

Given the global nature of many of these businesses, it’s important to ensure that companies across the supply chain provide adequate data disclosures. Countries outside the US may have stringent sustainability requirements that require companies with supply chains in their jurisdictions to comply with local sustainability regulations. Offenders may face fines and greater difficulty raising capital.

Selectivity Is Key

Some of the early optimism around clean energy companies has dissipated, and certain segments of the market continue to face challenges, including input cost fluctuations. That said, the power transition remains underway and continues to create a wide range of opportunities, in our view.

For investors, the keys to success will be thorough analysis and continued vigilance. That means focusing not only on business models and company fundamentals but also on competitive positioning, execution and the long-term trends shaping the energy transition.

References to specific securities discussed are for illustrative purposes only and are not to be considered recommendations by AllianceBernstein L.P.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

David Wheeler is a Portfolio Manager for the Sustainable Climate Solutions Portfolio and Senior Research Analyst for the Sustainable Thematic Equities Portfolios, covering the energy, industrials and materials sectors for the portfolio team.

Ian McNaugher is a Research Coordinator (US) and Senior Research Analyst on the Strategic Core Equities investment team, covering US utilities and aerospace & defense.

Jayme Lisiewski is a Senior Research Analyst on the Strategic Core investment team.

Patrick O’Connell is a Senior Vice President and Director of Responsible Investing Portfolio Solutions and Research.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All