A Quarter Century of Data Says the Airline Opportunity Could Just Be Getting Started

Membership required

Membership is now required to use this feature. To learn more:

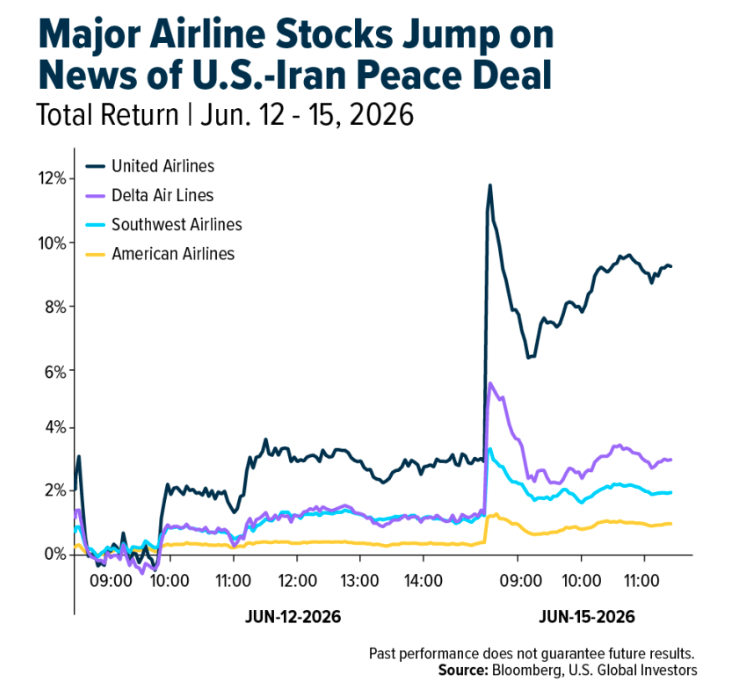

View Membership BenefitsLast Monday, President Donald Trump announced that the U.S. and Iran have reached a peace deal to reopen the Strait of Hormuz, the 21-mile chokepoint through which roughly 20% of the world’s oil supply normally flows.

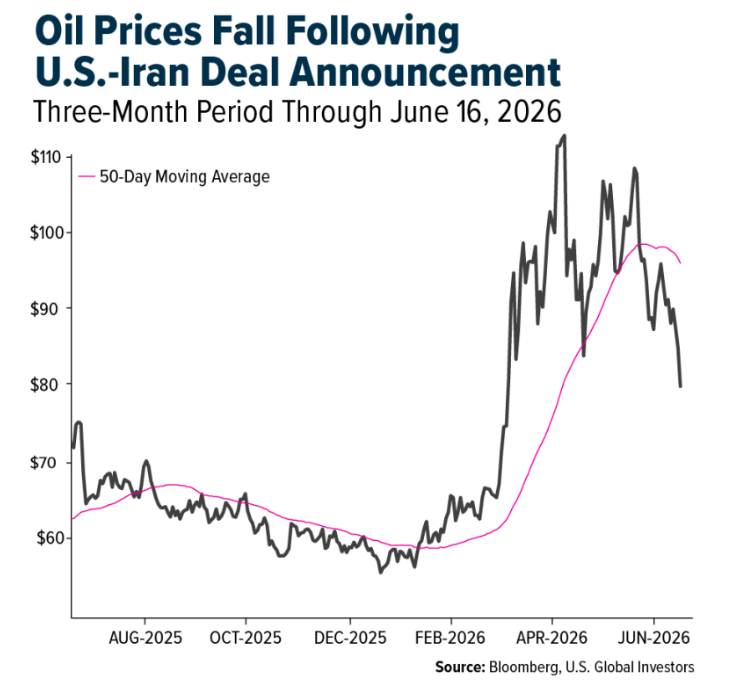

By mid-morning, Brent crude had dropped nearly 5% to $83 per barrel, and by Tuesday, it traded below $80 for the first time since early March. Shares of major airlines jumped on the news, led by United Airlines, which closed at a new record high. Delta Air Lines also hit a fresh all-time high.

For investors who have spent the last three-and-a-half months watching the airline sector sail through the turbulence, this week feels like confirmation of something. But confirmation of what, exactly? That’s the more interesting question.

Not All Oil Drops Are Created Equal

I’ve spent over a decade analyzing the relationship between energy prices and airline stocks, and the single most important thing I’ve learned is that falling oil and rising airline stocks are not the same thing.

Sometimes the two are correlated. Sometimes they’re not. And the difference almost always comes down to why oil is falling.

When oil drops because the economy is contracting—the way it did after the September 11 attacks in 2001, or when the global financial system seized up in 2008—airlines don’t benefit much from cheaper jet fuel.

Why? Well, if people aren’t flying, empty seats and low fuel costs still don’t add up to a good business.

But when oil falls because the supply side normalizes—an oversupply problem, a geopolitical disruption that resolves—something different happens. Travel demand stays intact, and airlines begin pocketing the spread between what passengers are paying and what carriers are now paying for fuel.

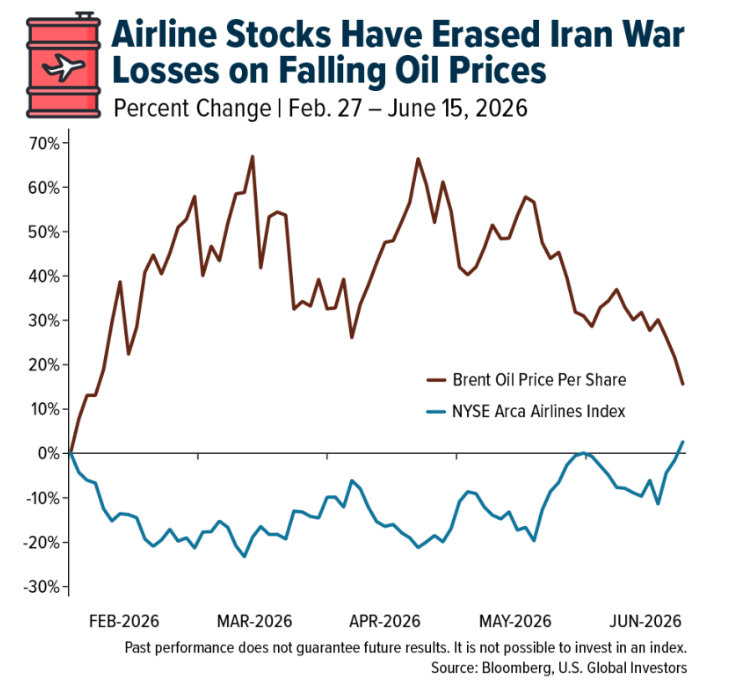

That’s what’s happening today. Airline stocks, as measured by the NYSE Arca Airlines Index, have now erased their losses from the Iran conflict as oil prices decline and demand remains strong.

What a Quarter Century of Data Tells Us

Working through daily Brent crude oil prices and the NYSE Arca Airlines Index going back to January 2000, I looked at what happened to airline stocks following four major oil price crashes.

The two demand-driven crashes told a cautionary tale. After the September 11 attacks in 2001, investors who bought airlines at the oil price trough saw a modest 20% gain over three months… then gave it all back (and then some), losing 45% over the following 12 months as the travel recession ground on.

The 2008 financial crisis told a similar story. Oil fell 74%, but airlines were still down almost 40% three months after the oil trough, as collapsing consumer confidence kept seats empty. Patient investors who held on eventually saw rebounds of 47% and 62% at the 12- and 18-month marks.

The supply-driven episodes, on the other hand, painted a completely different picture. When Saudi Arabia blocked OPEC production cuts in 2014 to defend market share, Brent crude fell 75% from peak to trough over 18 months. Airlines near the January 2016 oil price trough returned 28% over three months, 52% over 12 months, and 59% over 18 months.

Then came 2020. The pandemic crashed oil to $19 a barrel and temporarily shut down global aviation.

But once the demand catalyst became visible—vaccine approval on the horizon—the recovery was historic. Buying airlines at the April 2020 oil trough returned 21% in three months and a massive 132% over the following 12 months. That was the best 12-month return for airline stocks in the 30 years of data I looked at.

Why 2026 Belongs in the Supply Shock Column

The war in Iran created one of the most dramatic oil supply shocks in recent memory. Iran’s retaliation sent Brent to $146 a barrel, its highest level since 2008. Airline stocks fell as fuel costs compressed margins.

Unlike past episodes, though, travel demand hasn’t collapsed. Airlines have raised airfares to offset surging fuel costs… and passengers are paying them. As someone who travels often, I’ve seen packed planes all throughout this disruption.

The 2026 episode belongs firmly in the supply shock column. It was an external disruption to fuel costs that’s now coming to an end, with passenger demand fully intact.

Why the Window Matters Now

Across numerous oil price drawdowns since 2000, the historical data shows that the strongest entry point for airline stocks was not at the start of the oil decline or during the peak of the fear. It was near the oil price trough, after the big move had already happened and the situation was stabilizing. The average 12-month return from that entry point, across all 34 episodes I counted, was 19%.

With Brent back near $80 today—still above its pre-war level of roughly $64 to $67, but well off the $146 peak—and the Strait of Hormuz reopening, we appear to be in the early phase of what history suggests could be a sustained period of margin recovery for airline stocks.

Based on what 26 years of data show about how airline stocks behave after supply shocks end with demand intact, this may well be the starting gun.

Airlines and Shipping

Strengths

- The best-performing airline stock for the week was Frontier, up 14.8%. According to Goldman, industry capacity is continuing to ease as higher jet fuel prices push airlines to scale back. Supply and demand are tightening further following the exit of Spirit, a leisure-focused carrier, in May. For the third quarter of 2026, year-over-year capacity has been reduced by three percentage points since early May, with about half of that reduction driven by Spirit shutting down operations.

- According to Morgan Stanley, shipping rates rose 3.7% week-over-week on North America routes and were up 5.7% on Europe routes. The group believes the recent increase in container spot freight rates reflects stronger demand driven by an earlier-than-usual peak season, as well as the introduction of surcharges by container shipping companies.

- The fare trend set up in the second quarter of 2026 is generally favorable for all airlines analyzed, reports Raymond James, but best for Sun Country/Allegiant when taken together, along with Delta Air Lines.

Weaknesses

- The worst-performing airline stock for the week was Tongcheng Travel, down 5.1%. China domestic-operated flights declined 8% year-over-year (YoY) for the week, narrowing from a 12-14% YoY decline over the previous four weeks. Taking capacity cuts into account, Morgan Stanley still expects a YoY margin contraction for Chinese airlines at current ticket prices.

- Hormuz transit data remains low (<5% of normal), although channel checks suggest a growing number of vessels transiting via the Oman corridor in the past few weeks not captured in official tracking data. Red Sea container transits are limited to smaller liners and CMA CGM for now, but a finalized Iran deal is likely to prompt more to return, according to Bank of America.

- May’s Canadian cardholder spending data is incrementally negative for Air Canada in RBC’s view. Travel was the weakest category in the report, with the three-month average being negative at -2%, a step-down from +0.7% in the February read-through. This is consistent with risks that RBC flagged previously, that rising gasoline costs are compressing household budgets, with essentials spending, ex-gasoline, essentially flat at 0.1% in May, leaving less room for travel.

Opportunities

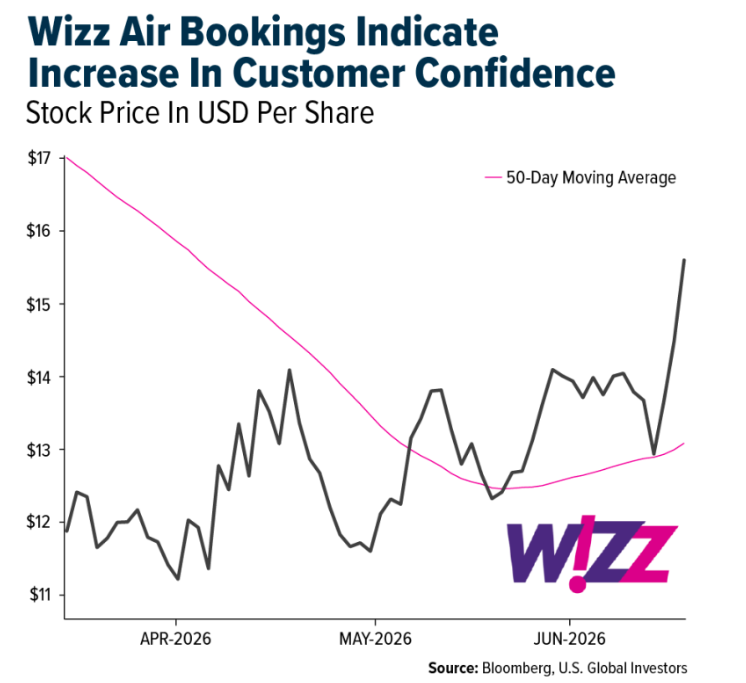

- Wizz Air’s observed advance bookings have crept back into positive territory starting in May following a shortening of the booking curve in March/April. This suggests consumers are adjusting to the news cycle and regaining confidence to plan, explains Raymond James.

- The U.S. and Iran have reportedly reached a preliminary peace framework to end the conflict, reopen the Strait of Hormuz, and lift the U.S. naval blockade of Iranian ports, with a formal signing expected in Switzerland on Friday, June 19. Morgan Stanley sees a potential spot rally if the Strait reopening materializes. Spot rates will likely stay elevated for months amid potential global oil re-stocking.

- According to BMO, looking toward third quarter 2026, forward curves are, on average, 10% below consensus forecasts, including 7% at Delta and Alaska, 10% at JetBlue, 11% at United and American Airlines, and 13% at Southwest Airlines. In total, forward curves now price in a 25% quarter-over-quarter decline in jet fuel costs for the third quarter, with Singapore and European prices moving 30% lower.

Threats

- The Port Authority of New York and New Jersey had objected to Spirit’s plan to auction its La Guardia slots, reports TD. The U.S. Bankruptcy Court for the Southern District of New York approved Spirit’s plan to sell its La Guardia slots as well as its corporate campus in Florida and its loyalty program, but the Port Authority wants to see the slots sold to Frontier.

- According to UBS, global new ship orders rose 146% YoY at 10.9 million tons in May as energy security concerns and high freight rates drove tanker (+344% YoY) and LNGC demand, while containership orders remained surprisingly resilient. This lifted year-to-date orders to 103.6 million tons (+128% YoY).

- Air India is reportedly looking to delay/defer hundreds of aircraft deliveries and cut flights. The airline has the world’s third largest orderbook at 539 aircraft, composed of 344 Airbus and 195 Boeing. The current fleet size is 296 aircraft, according to UBS.

Luxury Goods and International Markets

Strengths

- Eurozone industrial production increased 0.1% in April 2026, following a 0.4% increase in March, marking a second consecutive monthly gain. Major economies such as Germany and Italy also reported increases in industrial output during April.

- Sephora, the global beauty retailer owned by luxury conglomerate LVMH, launched its Major Summer Deals event, offering discounts of up to 50% across a broad range of beauty and skincare products. The promotion highlights continued consumer interest in premium beauty products, one of the most resilient categories within the luxury sector. Sephora’s loyalty program incentives are also helping drive customer engagement and repeat purchases during the summer shopping season.

- RealReal Inc, an American luxury goods marketplace, gained 21.11% over the past five trading days, making it the top performer in the S&P Global Luxury Index. The advance was driven by continued optimism around the company’s profitability turnaround, strong recent operating results, and positive earnings estimate revisions that boosted investor confidence in its growth outlook.

Weaknesses

- China’s latest economic data came in weaker than expected this week, highlighting ongoing softness in the world’s second-largest economy. Retail sales growth slowed to 6.4% year-over-year in May, below consensus expectations, while industrial production rose 5.8%, also missing forecasts.

- Ferrari’s first fully electric vehicle, the €550,000 Ferrari Luce, has received mixed reviews from collectors and enthusiasts, raising concerns about demand for the brand’s EV strategy. Reports suggest Ferrari is encouraging clients to purchase the model to maintain priority access to future limited-edition vehicles. The challenge comes as Ferrari shares have declined approximately 22% over the past 12 months, despite the company maintaining a market capitalization of roughly €56 billion. For a manufacturer that produces fewer than 14,000 vehicles annually and relies heavily on exclusivity, the reception of its first EV will be closely watched by investors and the broader luxury sector.

- Citychamp Watch & Jewellery, a Chinese watch manufacturer and distributor, was the worst-performing stock in the S&P Global Luxury Index over the past five trading days, with shares falling 22.64%. The company reported a 52-week low on June 18 with a stock price of USD$0.00829.

Opportunities

- Following the announcement of a peace framework between the United States and Iran, oil prices have retreated as markets price in lower geopolitical risk. While the agreement remains fragile and key details still need to be implemented, it represents a constructive step toward restoring stability in the Middle East and ensuring the safe passage of energy shipments through the Strait of Hormuz. If the ceasefire holds and regional tensions continue to ease, consumer confidence could improve, supporting stronger travel demand and broader consumer spending.

- The 2026 FIFA World Cup began last week and is already driving increased travel and consumer activity across host markets. As one of the world’s largest sporting events, the tournament is attracting millions of fans, boosting demand for flights, accommodations, entertainment, dining, and premium experiences. The event highlights the strength of global travel demand and provides a positive backdrop for growth across the travel, tourism, and luxury spending sectors.

- L Catterton, the consumer-focused private equity firm backed by the family behind LVMH, is reportedly close to acquiring a significant stake in HYROX, one of the world’s fastest-growing fitness competitions. The deal highlights how luxury and premium consumer investors are increasingly targeting wellness, fitness and experiential lifestyle brands as consumers allocate more spending toward health-focused experiences. The trend creates new avenues for luxury groups to diversify beyond traditional fashion and accessories while strengthening engagement with younger and affluent consumers.

Threats

- The luxury handbag market is showing signs of structural change as consumers increasingly turn to resale and vintage products instead of buying new items directly from brands. According to Bain & Company, luxury handbag sales have fallen nearly 10% from their 2023 peak, representing an estimated $8 billion decline in annual spending. Meanwhile, luxury handbag sales on resale platform The RealReal have risen 20% since 2023, while searches for vintage bags surged 131% year-over-year in May. The trend poses a risk for luxury companies, as handbags remain one of their most profitable categories and a key entry point for attracting new customers.

- Burberry is facing shareholder opposition ahead of its annual meeting after proxy advisory firm ISS recommended voting against the company’s new executive compensation policy. The proposal would significantly increase potential payouts for CEO Joshua Schulman as the company works through a turnaround strategy. Investor concerns over governance practices and executive compensation could create additional uncertainty at a time when luxury brands are already navigating slower consumer demand and uneven global growth. Negative shareholder sentiment may also weigh on management credibility and strategic execution.

- Stellantis CEO Antonio Filosa confirmed that Maserati is in discussions with two potential partners as the luxury automaker seeks new technologies and strategic support. The move comes as Maserati continues to struggle with weak performance and underutilized production capacity, prompting concerns about the brand’s long-term competitiveness in the global luxury vehicle market. While Stellantis has ruled out the sale of Maserati, the need to seek external partnerships highlights the challenges facing some luxury brands as they navigate slowing demand, electrification investments and growing competition from both established and emerging manufacturers.

Energy and Natural Resources

Strengths

- The best-performing commodity for the week was coffee, up 7.10%. Coffee is the standout performer this week, with traders pricing in robust demand growth. Rising incomes and shifting consumer habits are driving more people toward the drink, and there’s still plenty of room to run given how far behind it sits versus tea consumption in major emerging markets like India. Starbucks is capitalizing on this by targeting 100 storefronts in India annually.

- The green economy hit a record $10 trillion in market value as revenue from climate-related products and services grew to $5.5 trillion last year, at its fastest pace since 2022, with companies deriving over 20% of income from green activities outperforming the broader market. LSEG’s report highlights EVs/batteries as standout growth areas and points to NextEra’s ~$67 billion stock deal for Dominion Energy as a sign that M&A is accelerating consolidation in the space, even as U.S. policy has tilted toward oil and gas.

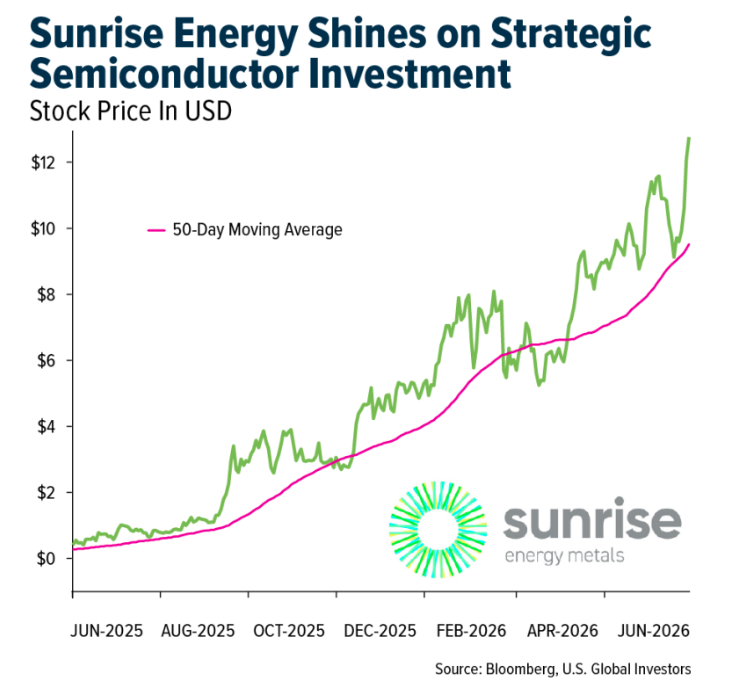

- Sunrise Energy Metals agreed to a $5 million strategic investment in Agni Semiconductor, a Philadelphia-based developer of next-generation memory using aluminum scandium nitride (AlScN), securing roughly 17–18% ownership with a path to 30%. The deal positions its Syerston Scandium Project—one of the world’s largest high-grade resources—to supply a key input as the global memory market faces its tightest supply in 15 years; while AlScN is still pre-commercial and scandium use per wafer is modest, broader adoption could drive meaningful new demand.

Weaknesses

- The worst-performing commodity of the week was WTI Crude Oil, declining approximately 12.22%. Oil is the worst performer this week, with Brent futures down about 11% as the U.S.-Iran peace deal reopened the Strait of Hormuz and sent tankers flowing again, easing fears over the fifth of the world’s oil supply that route handles. Prices have now slipped to roughly $78 a barrel, just a few dollars above pre-war levels, as traders price in the return of shuttered production from Saudi Arabia, the UAE, and Iraq, even though full normalization of flows is still expected to take months.

- Oil prices tumbled to their lowest levels since early March after the U.S. and Iran reached an interim agreement, scheduled to be signed June 19 in Switzerland, that could pave the way for a reopening of the Strait of Hormuz and a lift of the U.S. blockade on Iranian oil traffic. The IEA’s June Oil Market Report cut its 2026 demand forecast by 700,000 b/d while projecting supply will rebound by roughly 8 mb/d in 2027 against only 2 mb/d of demand growth, signaling a significant surplus emerging next year even as inventories are first drawn to historic lows.

- China’s aluminum processing sector weakened sharply heading into the summer off-season, with the June Aluminum Processing PMI falling 9.7 percentage points month-over-month to 40.1%, below the boom-bust threshold, as new orders dropped significantly across all downstream segments. SMM analysts see little improvement near-term, reinforcing signs of soft physical demand in China even as global aluminum prices remain elevated on Middle East-linked supply disruptions.

Opportunities

- The Pentagon’s Office of Strategic Capital has conditionally committed a $500 million loan to rare-earth refiner Phoenix Tailings to build a “Freedom Facility” for domestic midstream separation and metallization, part of a roughly $1 billion push to rebuild the U.S. rare earth supply chain and reduce reliance on Chinese processing. The facility, targeted to begin operations in 2028, will process diverse feedstocks, including mined concentrates and recycled materials, into light and heavy rare earth metals for defense, manufacturing, and allied supply chains.

- State-owned Vattenfall selected Rolls-Royce over GE Vernova to supply three 470-megawatt small modular reactors on Sweden’s west coast, citing a stronger supply chain, timing, and returns, with power generation targeted for the mid-2030s. The deal extends Rolls-Royce’s SMR momentum following prior selections by the UK and the Czech Republic, while project company Videberg Kraft will be majority state-owned alongside Vattenfall and industrial consortium Industrikraft.

- Canadian PM Mark Carney granted Italy priority access to Canada’s critical mineral reserves during G7 talks with PM Giorgia Meloni in Évian, building on growing bilateral ties that include Eni’s nearly C$100 million graphite investment in Québec and Italy’s entry into the Critical Minerals Production Alliance. The two leaders also launched negotiations for Canada to purchase Leonardo’s M-346 jet trainers and discussed defense financing, Ukraine, and the Middle East.

Threats

- Bougainville Copper Ltd. lost its exploration permit for the Panguna mine after the Autonomous Bougainville Government rescinded it, transferring full mining rights to local company Bougainville Minerals Ltd., sending the firm’s shares down nearly 36%. The move comes as India’s Lloyds Metals and Energy explores partnering on the redevelopment, having beaten out China’s CMOC Group for the role, in a project central to Bougainville’s push for independence from Papua New Guinea.

- Protesters from the Radical Reform Movement blocked the road used to export copper concentrate from Rio Tinto’s Oyu Tolgoi mine in Mongolia, demanding a larger share of mining revenues and renewing scrutiny of the country’s mineral wealth distribution. The blockade adds to existing friction between Rio Tinto and Mongolia, which is already suing the company over alleged tax underpayments and separately seeking to renegotiate Oyu Tolgoi’s commercial terms ahead of national elections next year.

- China formalized sweeping control over 36 mineral resources—including rare earths, critical metals, battery materials, and energy commodities—under a national strategic minerals framework within its Mineral Resources Law, Morgan Stanley reports. The revised regulations centralize regulatory authority to set annual mining quotas, consolidate approval for new mining and exploration rights at the central level, limit licenses granted per deposit, and require joint Ministry of Commerce/Ministry of Natural Resources approval for exports of dual-use materials. This gives Beijing a stronger legal foundation to manage output, reserves, and trade flows across a near-monopoly supply chain.

Bitcoin and Digital Assets

Strengths

- SpaceX’s recent SEC filing confirmed that the company continues to hold 18,712 BTC on its balance sheet, valued at approximately $1.3 billion as of March 31. The position has remained unchanged since its initial purchase in 2021, demonstrating a long-term commitment through multiple market cycles. Together, SpaceX and Tesla now hold more than 30,000 BTC, reinforcing Bitcoin’s growing role as a corporate treasury asset among major technology companies.

- The crypto industry’s political arm secured another victory as pro-crypto candidate Barry Moore won Alabama’s Republican Senate primary after receiving strong support from Fairshake and affiliated PACs. Fairshake spent more than $12 million backing Moore and currently holds nearly $150 million in cash for future races. The win reinforces the industry’s growing influence in U.S. politics as it works to build what supporters call the largest pro-crypto caucus in congressional history.

- More than 200 crypto firms have urged the U.S. Senate to advance the Digital Asset Market Clarity Act, legislation designed to establish a federal framework for digital assets and clarify regulatory responsibilities between the SEC and CFTC. The bill, which already passed the House of Representatives, could provide greater legal certainty for blockchain networks, developers, and digital asset businesses. The broad industry support emphasizes growing momentum toward comprehensive crypto regulation in the U.S.

Weaknesses

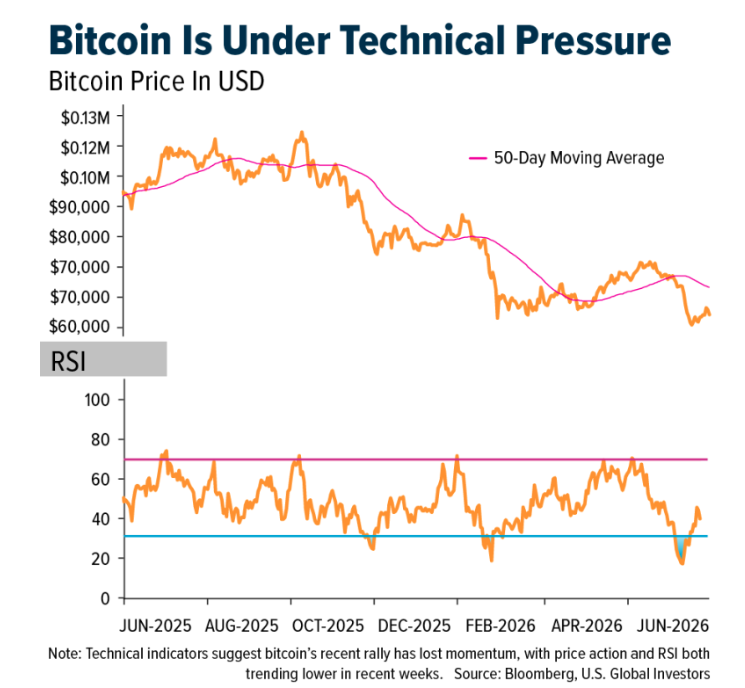

- Bitcoin’s 11% decline in June has significantly impacted investor positioning ahead of the June 26 options expiration. Approximately $8.6 billion, or 80% of the $10.6 billion in outstanding options contracts, are currently out of the money and could expire worthless if prices do not recover. The data suggests that many traders expected bitcoin to trade well above current levels near $65,000, highlighting weaker market sentiment and increasing the potential for heightened volatility as expiration approaches.

- Forward Industries, the largest publicly traded Solana treasury company by SOL holdings, failed to secure any of its three proposed stock-for-stock acquisitions after all targets either rejected or ignored its offers. The company holds nearly 7 million SOL acquired for approximately $1.6 billion at an average price of $232 per token, leaving it with more than $1 billion in unrealized losses at current market prices. The outcome raises questions about the viability of its consolidation strategy and investor confidence in SOL-backed corporate structures.

- U.S. spot Bitcoin ETFs experienced persistent investor withdrawals in early June, posting net outflows in 11 of 13 trading sessions between May 29 and June 16. The largest daily redemption reached $519 million on June 2, while BlackRock’s IBIT accounted for a significant share of the withdrawals. The trend suggests weaker investor demand for bitcoin exposure and reflects a more cautious market environment amid ongoing price volatility.

Opportunities

- Coinbase unveiled a broad suite of new products as it advances its vision of becoming an “everything exchange.” New offerings include tokenized U.S. stocks, stock and crypto options trading, AI-powered investment advice, prediction markets, and perpetual futures linked to private companies such as SpaceX, with OpenAI and Anthropic expected to follow. The expansion shows the growing convergence of traditional finance, artificial intelligence, and digital assets within a single platform.

- Prediction markets experienced a surge in activity during the 2026 FIFA World Cup, with Polymarket’s tournament winner market alone generating more than $2.5 billion in trading volume. The event has attracted multi-million-dollar wagers, including one trader who earned $9.24 million in a single day after correctly predicting four match outcomes.

- Hyperliquid, a leading decentralized perpetual futures exchange, surpassed $10 billion in open interest as demand grows for blockchain-based trading of equities, commodities, indexes, and pre-IPO markets. According to Talos, a digital asset trading and infrastructure provider serving institutional investors, roughly $4 billion of open interest is tied to non-crypto perpetual products, while pre-IPO contracts attracted more than $250 million ahead of SpaceX’s public listing. The trend stresses increasing demand for 24/7 access to financial markets and the growing convergence of traditional finance and digital asset infrastructure.

Threats

- Binance may face restrictions on operating across the European Union after Reuters reported that Greece’s regulator is expected to reject the exchange’s MiCA license application ahead of the June 30 deadline. MiCA, the EU’s new regulatory framework for crypto assets, requires firms to obtain authorization to serve customers across member states. If denied, Binance could lose access to one of the world’s largest crypto markets.

- Illinois approved a new 0.2% tax on digital asset business activity, including the exchange, transfer, or custody of crypto assets on behalf of customers. The measure applies to firms generating at least $100,000 in gross receipts from Illinois residents and is expected to raise approximately $60 million annually. Industry groups have criticized the law for imposing a unique tax burden on digital assets that does not apply to stocks, bonds, or derivatives, raising concerns that similar measures could spread to other jurisdictions.

- Major U.S. gaming organizations are urging lawmakers to prohibit sports-related prediction markets through pending crypto market structure legislation. The groups argue that platforms such as Kalshi and Polymarket are offering nationwide sports wagering without the regulatory safeguards applied to traditional gaming operators. The proposal comes as prediction markets continue to grow rapidly, with Kalshi generating $16.8 billion in trading volume and Polymarket $7.1 billion in May, raising the risk of new restrictions on one of the fastest-growing segments of the digital asset ecosystem.

Defense and Cybersecurity

Strengths

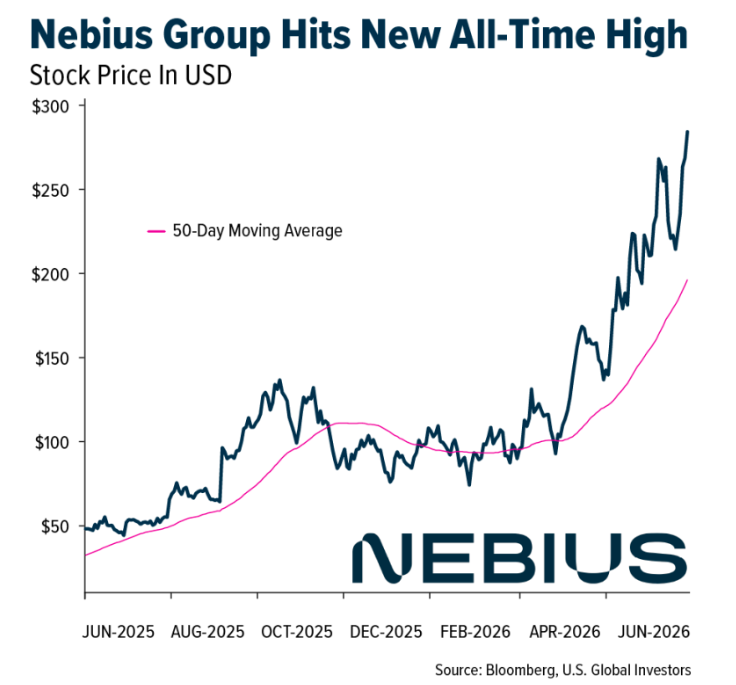

- Nebius Group is experiencing a powerful surge driven by strong fundamental growth. The climb is highlighted by a staggering year-over-year first quarter revenue jump as the company’s AI and high-performance cloud infrastructure scales rapidly across Europe and the U.S. This operational momentum is further accelerated by Wall Street prestige, as the company’s upcoming inclusion in the Nasdaq 100 Index on June 22 triggers massive, forced buying from passive investment funds and ETFs tracking over $800 billion in assets.

- The first batch of Polish F-35 fighter jets has officially entered service, marking Poland as the first country on NATO’s eastern flank to field the U.S.-made, fifth-generation combat aircraft.

- Sikorsky won a $525 million contract to develop advanced technologies for the CH-53K King Stallion fleet, including support for the U.S. Marine Corps, the Navy, and a foreign military customer. The contract will run through June 2031.

Weaknesses

- On Thursday, Moscow was hit by its largest-ever drone strike, targeting a major oil refinery and signaling a severe escalation in aerial warfare, while a separate, disputed drone strike hit a Belarusian youth football team’s bus in the Bryansk region. In response, Alexander Lukashenko directly accused Kyiv of “open fascism” and banned unauthorized trips for children abroad, while Russian officials warned of severe retaliation. For Ukraine, this dual crisis—intensifying strikes on the Russian capital alongside accusations of targeting Belarusian civilians—raises the risk of a new wave of massive Russian missile strikes on its infrastructure and threatens to draw Belarus deeper into the active conflict.

- OpenAI’s newly leaked financial report revealed a $38.5 billion net loss for 2025, driven largely by one-time, non-cash accounting charges from its corporate restructuring. Despite these steep paper losses, the company is moving toward an IPO, fueled by massive revenue growth that jumped to $13.07 billion.

- Microsoft canceled a $3 billion cloud deal with Oracle due to security and compliance concerns. Brazil fined major tech firms, including Microsoft, R$298 million for loot-box practices, reflecting increased regulatory scrutiny in the tech industry.

Opportunities

- The UK has opened what it describes as Europe’s largest drone testing facility, aiming to speed up the development and deployment of new capabilities for its armed forces. Backed by Defense Secretary Dan Jarvis MP, the new Uncrewed Systems Centre intends to help move emerging technologies from testing to operational use within weeks rather than years.

- Electro Optic Systems has completed its acquisition of MARSS’ defense business to offer integrated counter-drone capabilities under a single provider.

- NVIDIA has planned a $20 billion investment‑grade bond offering, marking the largest and first corporate bond sale in five years to refinance debt and fund expanded AI-related investments.

Threats

- Poland has paused plans to supply its remaining Mikoyan MiG-29 combat aircraft to Ukraine due to an unresolved agreement on drone technology sharing.

- The U.S. Supreme Court’s decision to allow a New York law that lets victims sue firearm manufacturers has direct implications for Smith & Wesson’s legal exposure.

- A B-52 Stratofortress bomber crashed shortly after takeoff from Edwards Air Force Base with emergency crews responding. The crash resulted in eight fatalities, which included two Boeing employees, leading to the airfield’s closure and an investigation of the incident.

Gold Market

This week gold futures closed the week at $4,236.40, up $122.40 per ounce, or 2.98%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 7.91%. The S&P/TSX Venture Index came in up 1.84%. The U.S. Trade-Weighted Dollar rose 0.95%

Strengths

- The best-performing precious metal for the week was palladium, up 3.27%. Palladium-backed ETFs added 4,411 troy ounces in the latest session. That single-day inflow contrasted with gold, which saw its eighth consecutive day of outflows, with silver’s total holdings now at roughly 785.6 million troy ounces worth about $53.37 billion.

- According to Scotia, Tether has emerged as a new gold buyer, adding further to official-sector-adjacent demand. Tether purchased six tons of gold in the first quarter of 2026, lower than 27 tons purchased in the fourth quarter of 2025, with gold holdings equivalent to 132 tons. Including Tether’s XAUT gold token (22 tons), Tether’s combined gold holdings are estimated at 154 tons, placing it among the top 20 official holders.

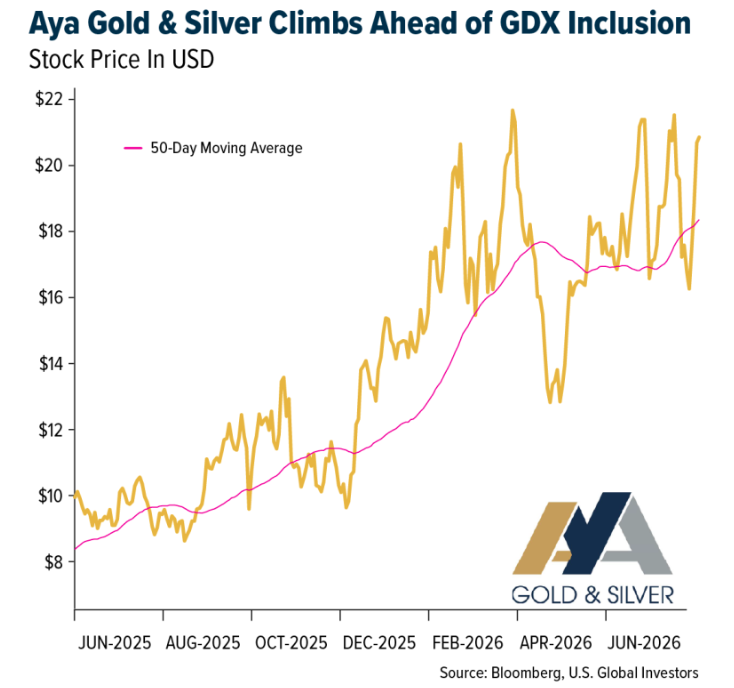

- Aya Gold & Silver is showing strength on its addition to the VanEck Gold Miners ETF (GDX), effective June 19, which should boost the stock’s liquidity and visibility among a broader investor base. The company continues to advance its strategy around its Boumadine polymetallic project in Morocco alongside its existing Zgounder silver mine, building on the momentum from the index inclusion.

Weaknesses

- The worst performing precious metal for the week was platinum, still up 1.97%. Valterra Platinum CEO Craig Miller suggested central banks could eventually add platinum to their reserves as a natural extension of the de-dollarization trend that has already driven heavy gold buying, with reserve banks adding roughly 1,000 tonnes of gold over the past four years. Platinum’s spot price more than doubled in 2025 on precious metal and industrial demand.

- Bolivia’s central bank fulfilled the first delivery under its gold forward sales program on Monday, transferring 4.3 tons of gold, according to a statement. The delivery corresponds to a transaction arranged in June 2025 by the previous administration as part of a broader agreement to sell 6.6 tons of gold forward to raise cash amid a shortage of foreign currency, reports Bloomberg.

- According to UBS, investors remain focused on whether recent PGM price weakness reflects underlying demand or inventory-driven effects, particularly given uncertainty around recycling flows and the impact of U.S. policy incentives. Management teams broadly challenged assumptions around accelerating recycling growth for PGMs.

Opportunities

- Scotia expects central banks to remain active net buyers in 2026, with estimated purchases of 650 tonnes. They see this demand as supportive for bullion and factor it into a 30% risk premium in their gold price versus fair value model, noting that official-sector buying is strategic—driven by diversification away from the U.S. dollar and gold’s role as an alternative reserve asset.

- Silvercorp reported an updated technical report for the Ying Mining District, highlighted by a 50% increase in mineral reserve tons and a 20% increase in contained silver to 106 million ounces. The update also includes a 90% increase in resource tons, at lower average grade due to lower cut-off grades. They outline a 17-year mine life to 2042, with production growth from higher throughput and further upside potential from resource conversion and exploration, according to BMO.

- More central banks than ever expect to increase their gold reserves, a sign that one of the key forces behind bullion’s record-breaking rally remains intact despite this year’s pullback. In a survey of 74 central banks, 45% said they plan to buy in the coming year, the biggest-ever share in data collected by the World Gold Council and YouGov Plc since 2018.

Threats

- As per World Gold Council (WGC) data, global production in 2025 totaled 3,817 tons, a 2.0% year-on-year increase. The growth can be attributed to production increases in Ghana (+32.6 tons), Russia (+15.0 tons), and Canada (+10.5 tons); partially offset by material declines in Indonesia (-34.4 tons), the United States (-6.0 tons), and Mexico (-4.0 tons). China remained the top global gold producing country with 384 tons of gold production in 2025.

- Zijin’s planned $4 billion all-cash acquisition of Allied Gold has cleared host-country regulators but is now stalled in Beijing, where Chinese authorities are reportedly questioning the price and political risk of the assets. This raises the risk of further delays or even cancellation, with some estimates suggesting more than a 50% chance that the NDRC rejects the deal or only approves it with strict conditions.

- Interest rates are turning into a headwind for gold after Fed Chair Kevin Warsh’s hawkish debut sent traders piling into rate-hike bets, with two-year Treasury yields jumping the most since April 2025 and half of Fed members now projecting a hike by year-end. Higher rates raise the opportunity cost of holding a non-yielding asset like gold, making the renewed conviction behind the Fed’s inflation fight a real threat to the metal’s appeal even as some of that repricing has eased slightly alongside falling oil prices.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2026):

Allegiant Travel Co.

Delta Air Lines

Air Canada

American Airlines

Southwest Airlines

United Airlines

JetBlue Airways Corp.

Alaska Air Group Inc.

Frontier Group Holdings Inc.

Airbus SE

Boeing Co/The

Tesla

LVMH Moet Hennessy Louis Vuitton

Ferrari NV

Burberry Group PLC

Nebius Group NV

Nvidia Corp.

Sunrise Energy Metals

Aya Gold & Silver

Valterra Platinum

Silvercorp Metals Inc.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The Nasdaq-100 Index is a stock market index that tracks the performance of 100 of the largest non-financial companies listed on the Nasdaq exchange, with a heavy emphasis on technology and growth-oriented firms.

The NYSE Arca Airline Index (ticker: XAL) is an equal-dollar-weighted stock market index that tracks major U.S. and overseas passenger airline companies.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting our prospectus page or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Read additional important information. +

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All