250 Years In, and the Case for America Has Never Been Stronger

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsClose to 40 years ago, I moved from Canada to the U.S. after acquiring a controlling interest in U.S. Global Investors. I’ve built my entire life and career here, and in all that time, I’ve never stopped marveling at my adopted country.

There’s something here you just can’t find anywhere else: the idea that an ordinary person can show up with a little energy and a lot of conviction and build something great.

That idea has a name, and this month, we’re celebrating its 250th anniversary.

See more: Celebrate Financial Independence Day: What True Freedom Looks Like for High Earners

Americans Are Gloomy, but the Fundamentals Tell Another Story

Sadly, many Americans have strong doubts about the nation’s future. Responding to a recent Gallup poll, over three quarters of Americans said they believed the Founding Fathers would be disappointed in how things have turned out, up from 42% back in 2001.

This gloom isn’t confined to just one party or age group.

Not to disqualify how other people feel, but I happen to agree with Warren Buffett. In his 2020 letter to shareholders, Buffett, who stepped down as CEO of Berkshire Hathaway last year, wrote that there’s never been an “incubator for unleashing human potential like America… Never bet against America.”

The Numbers Behind American Exceptionalism

Consider what the U.S. actually produces. We’re home to roughly 4% of the world’s population yet we generate about 26% of its GDP… and more than half its total market capitalization.

Late last year, the Economist pointed out that wages in Mississippi, the poorest U.S. state, now exceed average wages in Britian, Canada and Germany.

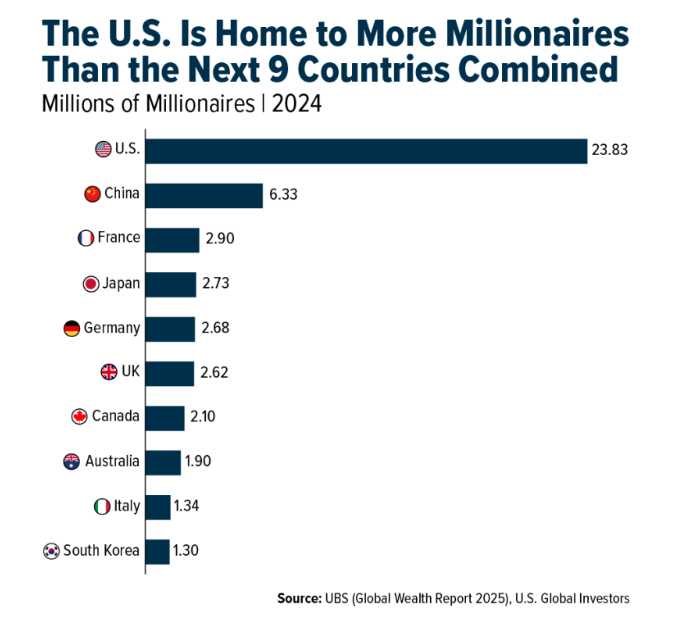

Wealth has inevitably followed. UBS reports that the U.S. is home to roughly 24 million millionaires, which is about 40% of the world’s total and more than Western Europe and China. We have more millionaires, in fact, than the next nine countries combined.

The World Keeps Voting for America

After 250 years, how does the U.S. keep the engine humming?

The beauty of American innovation is that it’s decentralized and resilient to political cycles. From the railroads of the 1800s to power grids, aviation, the telephone, the integrated circuit, the internet and now artificial intelligence (AI), private capital has financed wave after wave of progress. The World Intellectual Property Organization (WIPO) ranked the U.S. third in the world for innovation, first in market and business sophistication, with Silicon Valley among the most innovation-intensive places on earth.

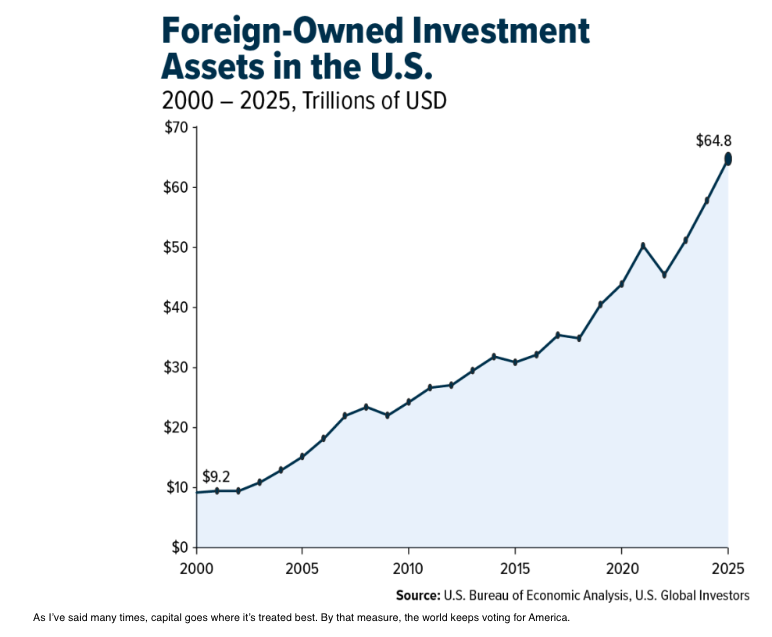

Even if certain Americans don’t always see it, international investors sure do. Foreign capital invested in the U.S. climbed to nearly $65 trillion at the end of 2025, a seven-fold increase from the beginning of the century, according to data from the Bureau of Economic Analysis (BEA).

As I’ve said many times, capital goes where it’s treated best. By that measure, the world keeps voting for America.

Why the Rule of Law Comes First

To be clear, the U.S. faces real headwinds, some of them genuinely without precedent: mounting debt, an erosion of public confidence in our institutions and capitalism itself, and a creeping willingness on both sides of the aisle to treat the rule of law as optional when it’s inconvenient.

Let’s remember where the American experiment actually comes from. Long before 1776, the Magna Carta established the principle that even a king is bound by the law, that the people may assert their rights against an oppressive ruler, and that government power can be checked to protect those rights.

Those ideas flow directly into the Declaration of Independence and the Constitution: due process, trial by jury, no taxation without representation. No person may be deprived of life, liberty or property without the law’s protection. As Thomas Paine put it in Common Sense, “law is king.”

I believe the Magna Carta is the source code. Nothing that we enjoy as Americans would exist without bedrock guarantees that the rules apply equally and won’t be changed by force.

Protect that guarantee, and prosperity takes care of itself. Neglect it, and no amount of economic oomph will save us.

Capitalism Widening the Circle

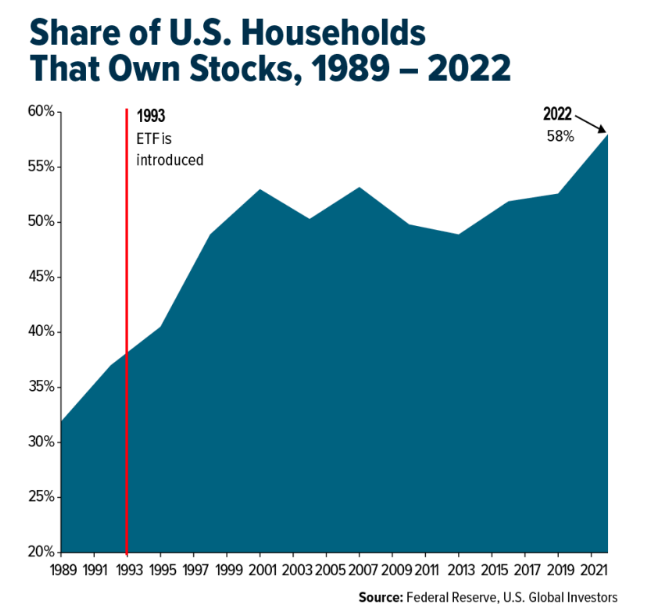

There’s one more reason why I remain bullish on America, and it’s personal. The U.S. is a relentless wealth generator for literally millions upon millions of people. Since the exchange-traded fund (ETF) arrived in 1993, ownership of stocks has exploded. Nearly six in 10 U.S. households now own stocks, and the Investment Company Institute (ICI) notes that fund ownership has grown fastest over the past two decades among middle- and lower-income families.

This is capitalism doing what its critics swear it can’t: widening the circle.

That’s the country I chose almost 40 years ago, and it’s the country I’d choose again tomorrow.

So, as we mark 250 years, remember, it’s not unpatriotic to acknowledge the challenges. But don’t confuse a bad mood with a bad bet. I encourage you to hold true to the ideals carved into our founding documents… and never bet against America.

Airlines and Shipping

Strengths

- The best performing airline stock for the week was Make My Trip, up 9.2%. According to Raymond James, good operational performance is foundational for a strong premium offering. Based on year-to-date data, Allegiant stands out as the best operator across these metrics while Southwest Airlines screens second best, albeit materially underperforming in departure delays particularly in the second quarter of this year.

- The cost of freight shipping has risen to its highest since the Red Sea crisis two years ago as businesses rush to stockpile inventory ahead of a fresh round of U.S. tariffs. Rates on routes between Asia and the U.S. East Coast, and Asia and Europe, last week hit their most expensive levels since the summer of 2024, explains Morgan Stanley.

- A Financial Times article cites top shareholders as coalescing around a price tag of at least £5.3B for easyJet. “The view about £7 is largely consensus,” said one significant investor in the airline. Another, who is also in the top 20 shareholders, said: “I don’t think Sir Stephen Hester will accept below £7. He’s very shareholder focused.”

Weaknesses

- The worst performing airline stock for the week was China Eastern, down 7.8%. The union representing Air Canada’s maintenance and ground handling employees voted to reject a tentative agreement reached earlier in June. The vote was close with 51% voting against. The parties will likely now have to return to the bargaining table.

- Alphaliner’s latest quarterly report on operating margins for the big carriers showed that Asian lines are generally doing better than their European counterparts. One of the reasons is that Europe-based operators deploy more tonnage on services to and from Europe, where exports have been sluggish.

- Preliminary delivery data from Cirium shows that deliveries from aircraft manufacturer Cessna were below consensus estimates for the second quarter (Q2). Preliminary data shows Q2 Cessna deliveries of 37 compared to the Morgan Stanley estimate of 45 and consensus of 46.

Opportunities

- Southwest Airlines’ management believes its recent commercial initiatives have driven a meaningful improvement in corporate demand, resulting in market share gains. Management is particularly excited about the upcoming high-speed Wi-Fi rollout and continues to evaluate additional strategic initiatives, including airport lounges, first-class cabins, and transatlantic service, to ensure the airline remains competitive and aligned with evolving customer preferences, reports Morgan Stanley.

- The Nikkei reported that Nippon Yusen is considering significantly increasing its investments under its next medium-term business plan, which begins in fiscal year 2028. According to the report, the company could invest approximately ¥500 billion annually, including potential acquisitions, and plans to rely more heavily on debt financing to support this spending. The article also noted that management believes the company has room to increase its net debt-to-equity ratio to around 1.0x while maintaining a healthy balance sheet. In addition, Nippon Yusen may consider raising its current minimum annual dividend of ¥200 per share, potentially returning more capital to shareholders.

- Air France-KLM CEO Benjamin Smith sees strong growth prospects in Latin America, particularly in Brazil, where the group is operating its highest number of flights in its 90-year history in the country. The airline plans to introduce its new La Première first-class cabin on Brazilian routes within the next 12 months, amid robust demand from premium travelers. Smith said the group is doubling down on industry consolidation and is confident about its moves involving Scandinavian Airlines System and Portugal’s TAP, according to Morgan Stanley.

Threats

- Theo Panagiotoulias, chief executive of Star Alliance, warned that the £33bn runway and new terminal at Heathrow risks pricing out airlines. He added: “We think expansion is the right thing for the market. It’s the right thing for the airlines, because the airlines want to grow at Heathrow, but there’s no simple solution to this. This is going to cost a lot of money.”

- As reported by Morgan Stanley, air freight momentum is now stabilizing/slightly deteriorating from the May peak. Average full-market rates rose to $3.17/kg, +28% year-over-year (YoY) versus +12% in March; by mid-June, rates remained elevated at $3.23/kg, +34% YoY, though flat week-over-week.

- Sueddeutsche Zeitung reported that Lufthansa plans to further reduce its short- and medium-haul fleet next year, citing comments from CEO Carsten Spohr at an internal company event. According to the report, the airline could retire up to 15 aircraft if operating costs do not decline. The planned reductions are part of Lufthansa’s broader effort to improve profitability and increase efficiency in response to continued cost pressures.

Luxury Goods and International Markets

Strengths

- Saks Fifth Avenue’s parent company has emerged from bankruptcy under a new name Saks Global, with a significantly leaner store footprint, reducing its total number of locations by more than half. The restructuring enables the company to focus on its highest-performing stores, improve profitability, and strengthen its position in the luxury market by delivering a more exclusive, upscale shopping experience.

- China’s economic activity was stronger-than-expected in June, with the official manufacturing PMI rising to 50.3 from 50.0 in May, beating economists’ forecasts of 50.0 and returning to expansion. Meanwhile, the official non-manufacturing PMI, which includes the services sector, edged up to 50.2 from 50.1.

- Amorepacific, a South Korean beauty and personal care company, rose 22.9% over the past five trading days, making it the top performer in the S&P Global Luxury Index. Shares surged after analysts highlighted strong demand for South Korean skincare and beauty products during Amazon Prime Day. South Korean brands accounted for 29% of the top 100 products in Amazon’s U.S. Beauty & Personal Care category and 38% of the top 100 skincare products, strengthening investor sentiment toward South Korean cosmetics companies, including Amorepacific.

Weaknesses

- On Thursday, Tesla shares fell despite the company reporting a record 480,126 vehicle deliveries for the second quarter. Deliveries exceeded Wall Street’s consensus estimate of 406,024 vehicles by 74,102 vehicles (about 18%), but investors took profits as the strong results had already been priced into the stock, highlighting concerns about Tesla’s high valuation and future growth expectations.

- While the luxury sector is showing signs of recovery, the rebound remains uneven. This week, Bain & Company noted that Europe continues to face weak tourist spending, while the industry has lost approximately 70 million luxury consumers since 2022 after years of aggressive price increases. Bain also highlighted that brands need to rebuild their broader customer base rather than rely on top-spending clients.

- Norwegian Cruise Line fell 7.1% over the past five trading days, making it the worst performer in the S&P Global Luxury Index. Shares declined as investors continued to weigh the company’s weaker 2026 outlook, including softer European booking trends, higher fuel costs, and ongoing execution challenges, despite expectations that management’s cost-cutting initiatives could support a recovery in 2027.

Opportunities

- According to the latest Bain–Altagamma Luxury Goods Market Study, global personal luxury goods spending is expected to grow 2–4% this year. In the most optimistic scenario, spending could increase 4–6%, supported by easing geopolitical tensions, a rebound in U.S. consumer demand, and a faster-than-expected recovery in China.

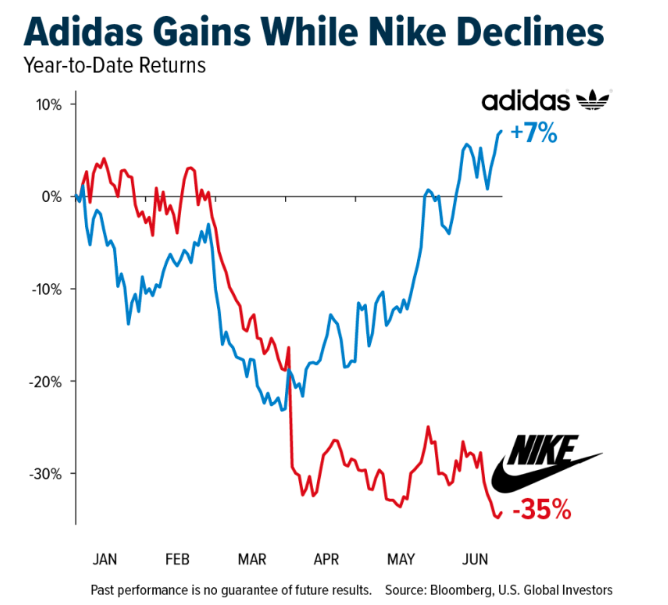

- Adidas has significantly outperformed Nike this year, with its shares up about 7% year-to-date compared with Nike’s 34% decline. Investors are rewarding Adidas for stronger product momentum, World Cup-driven demand, and better global execution, including a successful turnaround in China. While both companies generate about 15% of their revenue from China, Adidas has been winning back consumers with stronger localized products and execution, whereas Nike continues to face weaker demand, tougher competition from domestic brands, inventory issues, and pressure on margins.

- RH has opened its first London flagship, RH London, The Gallery at Mayfair, marking another milestone in its international expansion. The flagship spans an 18th-century Palladian mansion and two adjacent Grade II-listed buildings in one of the world’s premier luxury shopping districts, targeting affluent consumers. The opening strengthens RH’s global brand, expands its addressable market beyond North America, and supports long-term growth through premium pricing and future expansion across Europe.

Threats

- Volkswagen is considering a major restructuring that could include cutting up to 100,000 jobs worldwide and closing four factories in Germany. The proposed changes are intended to reduce costs and improve competitiveness as the company faces weaker demand in Europe, increasing competition from Chinese automakers, and higher trade barriers. While the plan has not been finalized, it would represent one of the largest restructurings in the automotive industry’s history.

- Mexico has declined to approve Royal Caribbean’s Perfect Day Mexico project in its current form, potentially delaying the cruise line’s new destination by at least one year. The proposal was rejected due to concerns that it could damage protected mangroves, coral reefs, and other sensitive ecosystems, with regulators determining that the proposed environmental safeguards were inadequate.

- Recent U.S.-Iran talks have shown tentative progress, with both sides continuing negotiations on a ceasefire, nuclear issues, and security in the Strait of Hormuz, helping ease immediate concerns over global oil supply disruptions. However, the discussions remain fragile, and any breakdown in the negotiations could quickly drive oil prices higher, reignite inflation concerns, and weaken consumer confidence by increasing energy costs and broader economic uncertainty.

Energy and Natural Resources

Strengths

- The best performing commodity this week was coffee, up 8.97%. Coffee prices have surged this week as wet weather slows harvesting and prompts farmers to hold back sales. The rally continued as adverse weather in key growing regions—including Brazilian rain delays and low exchange stockpiles—fueled ongoing supply concerns.

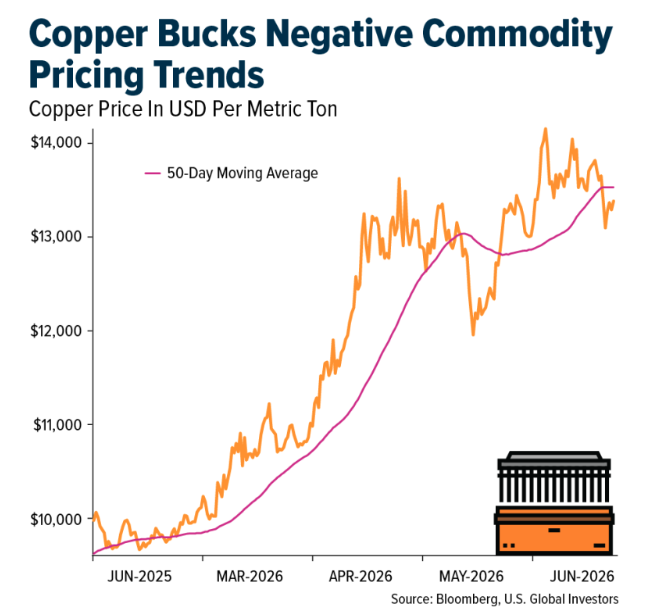

- According to UBS, demand prospects remain strong for copper due to electrification, arguably more compelling post-Iran conflict. Supply is constrained and there are deficits for one to three years with prices above $6 per pound.

- In the U.S., pipelines are built in three to four years with permitting approvals taking 50-70% of project time, explains Bank of America. Construction time for a pipeline in the Middle East is generally shorter at two to three years, as they are state-owned, and permitting is generally not a bottleneck. Faster builds mean the region can respond more quickly to supply disruptions. While bypass costs via the Red Sea added $2-3 per barrel during the recent war, they believe the strategic value of pipelines over the long-term outweighs the potential crude oil export disruption risks for the region.

Weaknesses

- The worst performing commodity this week was WTI crude oil, off 4.78%. Oil headed for the biggest quarterly decline since the pandemic as flows through the Strait of Hormuz accelerated following progress on a peace deal, with Morgan Stanley warning of a potential glut ahead. Brent’s more-active September contract traded near $74 a barrel, with front-month futures down almost a third this quarter, the biggest decline since 2020.

- Aluminum fell to the lowest since mid- February as a strengthening U.S. dollar and the easing of tensions in the Middle East continued to pressure commodities. The industrial metal extended losses after dropping by 16% in June, the biggest monthly decline since 2008, according to Bloomberg.

- At one point this past week, the Bloomberg Commodity Index was down 15% over trailing five weeks. Outside of economic crises (where demand destruction is the driving concern – e.g. 2020, 2008), this type of rapid commodity drawdown has only occurred one other time in the past 35 years: the summer of 2022. Ironically, that drawdown took place over almost the exact same seasonal period: beginning late May/early June and ending in early July, according to JP Morgan.

Opportunities

- The USDA unveiled the $500 million FIELDS program to expand domestic fertilizer manufacturing and reduce reliance on foreign suppliers, creating a potential tailwind for North American producers such as Nutrien. Nutrien shares were also upgraded by Scotiabank, with analyst Ben Isaacson noting that fertilizer supply remains constrained even as the Strait of Hormuz reopens, while highlighting upside risk from drought conditions and El Niño.

- Cheniere’s Stage 3 expansion at its Corpus Christi LNG export facility in Texas is 98% complete and remains ahead of schedule. Meanwhile, Europe received less than half of U.S. LNG exports in June for the first time since July 2024, as stronger Asian spot prices—JKM at $17.33/mmBtu versus TTF at $13.19/mmBtu—and record demand from Egypt redirected more cargoes east. Total U.S. LNG exports still increased to 10.6 million tons as Cheniere’s and Freeport LNG’s facilities returned from maintenance.

- Despite June’s pullback in spot lithium prices, underlying demand fundamentals remain solid, with electric vehicle (EV) and battery energy storage system (BESS) markets continuing to show durable growth into the second half of the year. That demand outlook is supported by accelerating global EV adoption, including in the UK, where EV sales have surpassed diesel vehicle sales over the past 12 months, suggesting the recent weakness in lithium prices may represent a buying opportunity rather than a structural shift in demand.

Threats

- The global oil market is expected to swing back into oversupply as the impact of the Iran conflict fades and traffic through the Strait of Hormuz recovers, according to Goldman Sachs. While purchases of crude oil to replenish strategic reserves are expected to tighten the market to some extent, they are likely to only partially offset the anticipated surplus, Samantha Dart, co-head of global commodities research, said in an interview with Bloomberg Television.

- According to UBS, the coal pricing backdrop remains challenging for U.S. producers. Ample spot supply and weak Atlantic demand are forcing producers to discount cargoes and redirect volumes to Asia, while a persistent gap between buyers and sellers continues to constrain market liquidity despite benchmark prices holding near $240 per ton.

- Data centers’ growing demand for electricity is driving up power costs for steel producers by tens of millions of dollars annually and threatening industry operations, according to a new report from the Steel Manufacturers Association. “We as an industry are very reliant on electricity to make steel,” said Rob Simon, CEO of JSW Steel USA.

Bitcoin and Digital Assets

Strengths

- Crédit Agricole, France’s second-largest bank by assets, has launched EURXT, a euro-backed stablecoin fully compliant with the EU’s MiCA framework. The token debuted with 20 million EURXT in circulation and has already been used to settle a subscription into a tokenized Amundi money market fund, highlighting growing institutional adoption of tokenized finance.

- The EU’s Markets in Crypto-Assets (MiCA) regulation is now fully in force, requiring crypto firms to obtain a license to operate across the bloc. Industry leaders say the unified framework strengthens transparency, investor protection and banking relationships, marking a major milestone in the maturation of Europe’s digital asset market.

- Ethereum Institutional has launched as an independent nonprofit to help financial institutions adopt Ethereum for tokenization, stablecoins and onchain finance. Backed by industry leaders including Ethereum co-founder Joseph Lubin, the initiative provides enterprises with a dedicated gateway to the Ethereum ecosystem, reinforcing Ethereum’s position in institutional digital finance.

Weaknesses

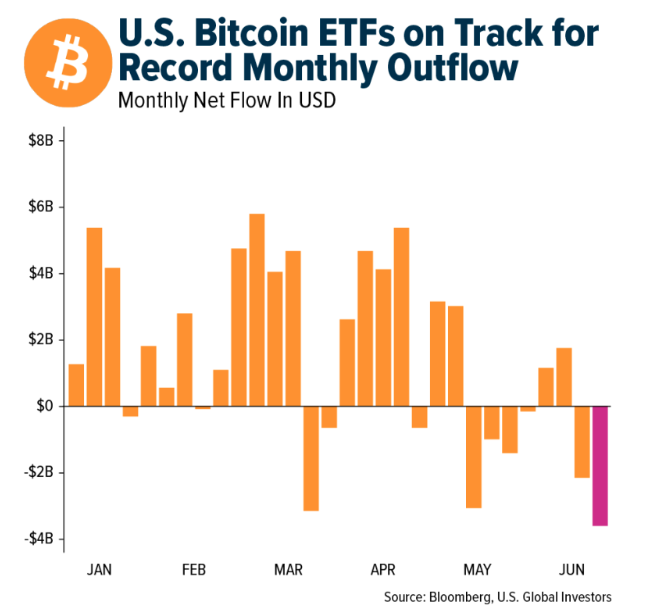

- U.S. spot Bitcoin ETFs are on pace for a record $4.1 billion in monthly outflows, with BlackRock’s IBIT accounting for nearly $3 billion. At the same time, uncertainty surrounding Strategy’s financing model has raised concerns over one of Bitcoin’s largest corporate buyers, signaling weaker institutional demand for the cryptocurrency.

- Binance withdrew its MiCA license application in Greece after European regulators raised concerns over the exchange’s history of financial crime compliance. The setback temporarily limits Binance’s ability to operate across the European Union under the new Markets in Crypto-Assets (MiCA) regulatory framework, highlighting how stricter compliance standards are reshaping competition in the crypto industry.

- Crypto infrastructure firm BitGo cut 15% of its workforce as it refocuses on security, stablecoins, settlement and AI-powered infrastructure. The restructuring follows a quarter in which revenue grew 112.6% year-over-year, but net losses widened to $60.7 million, emphasizing ongoing profitability challenges.

Opportunities

- More than 100 financial institutions, fintechs, banks and crypto firms, including Visa, Stripe, BNY Mellon, BlackRock and Coinbase, have joined the Open Standard initiative to launch a U.S. dollar-backed stablecoin later this year. The alliance aims to build an open, interoperable payment infrastructure, expanding enterprise adoption and accelerating the mainstream use of stablecoins for global transactions.

- The SEC has opened a 60-day public consultation to modernize ETF regulations, potentially expanding eligibility to crypto, prediction markets and other novel assets. The review comes as the U.S. ETF market has grown from $4 trillion in 2019 to $12 trillion in 2025, signaling continued regulatory support for product innovation and market expansion.

- The UK’s Financial Conduct Authority finalized a comprehensive regulatory framework covering crypto trading platforms, stablecoins, custody, staking and market abuse. The new regime provides greater regulatory certainty ahead of mandatory authorization in October 2027, supporting innovation while strengthening investor protection and market integrity.

Threats

- Edel Finance paused its lending protocol after an attacker manipulated the collateral value of a tokenized Google stock, creating approximately $403,000 in bad debt. The incident highlights persistent security risks in tokenized assets and DeFi, where pricing manipulation remains one of the industry’s most common smart contract vulnerabilities.

- South Korea’s Financial Services Commission referred two individuals for prosecution over alleged crypto market manipulation, including a whale accused of accumulating nearly half of a token’s circulating supply before executing a pump-and-dump scheme. The cases highlight ongoing market integrity risks despite increasing regulatory oversight.

- A Florida man pleaded guilty to operating a crypto Ponzi scheme that caused at least $250 million in investor losses after raising more than $400 million through false promises of returns from crypto liquidity pools. The case emphasizes that fraud remains a significant threat to investor confidence despite the industry’s growing institutional adoption.

Defense and Cybersecurity

Strengths

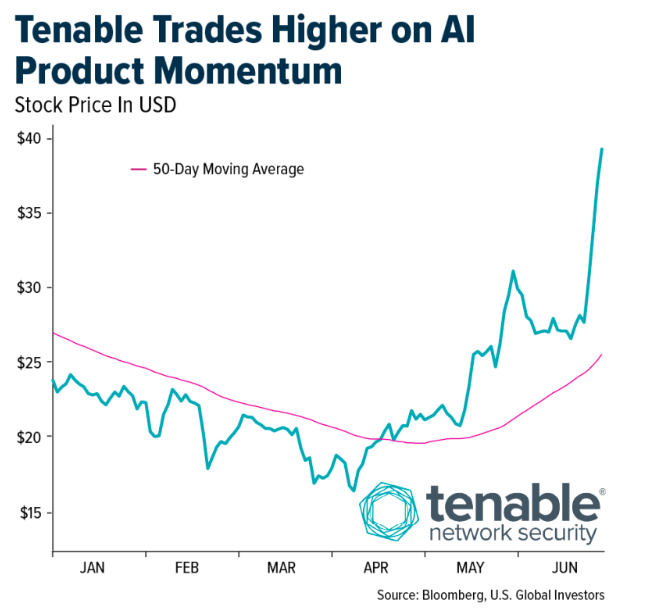

- Tenable gained another AI-driven growth catalyst after Gartner identified the company as a leader in AI-powered exposure assessment, highlighting its broad attack surface visibility, AI-driven risk prioritization capabilities, and execution of its AI strategy. The recognition follows recent milestones, including the launch of Tenable Hexa AI, expanded AI exposure capabilities, participation in Anthropic’s Project Glasswing and OpenAI’s Daybreak Cyber Partner Program, and the achievement of FedRAMP High and DoD Impact Level 5 authorization for Tenable One Cloud Exposure, strengthening its position in government and enterprise cybersecurity markets.

- NASA awarded approximately $590 million in contracts to Intuitive Machines and two other providers for upcoming lunar lander missions under the Commercial Lunar Payload Services program. These missions are intended to support the Artemis lunar exploration program, positioning Intuitive Machines as a key commercial partner in NASA’s long-term plans for the Moon.

- Akamai signed a $1.8 billion, seven-year cloud computing deal with Anthropic, its largest customer agreement to date, strengthening its position in AI-focused cloud infrastructure and potentially improving investor perceptions of its growth and valuation profile.

Weaknesses

- In a recently disclosed incident update, enterprise software company ServiceNow confirmed a significant data breach affecting its cloud-based operations. Threat intelligence reports indicate that more than 10 gigabytes of internal corporate data were exposed, including names, phone numbers, and over 450,000 unique corporate email addresses, in what appears to be an aggressive supply-chain exploit targeting enterprise workflow platforms.

- Texas Governor Greg Abbott issued a broad policy directive aimed at protecting the ERCOT power grid from surging industrial electricity demand, requiring data centers to fully fund their own grid connection infrastructure and adopt water-efficient closed-loop cooling systems. The order also seeks to eliminate longstanding sales tax exemptions and utility incentives for data center projects across Texas.

- Palantir CEO Alex Karp criticized the token-based pricing models used by AI competitors such as Anthropic and OpenAI, arguing that they create significant and unpredictable cost burdens for enterprise customers. He advocated for outcome-based AI pricing, contending that businesses should pay for measurable results rather than token usage.

Opportunities

- Micron and General Motors have entered a strategic customer agreement for the long-term supply of memory and storage solutions to strengthen automotive semiconductor supply chains and support future vehicle development with advanced memory technologies.

- On June 30, the U.S. Department of Commerce officially lifted temporary national security export controls on specific high-end AI architectures. Following the decision, Anthropic restored global enterprise access to its premium Claude Fable 5 and Mythos 5 models, which had previously been restricted for foreign nationals.

- A new partnership has been formed with OpenAI to co-develop AI solutions for national security and critical infrastructure use cases. The collaboration includes expanded access to OpenAI’s technical tools and roadmap insights to accelerate AI development and deployment across client missions.

Threats

- On June 30, Ukraine placed a major order in the high double-digit millions of euros for Rheinmetall’s specialized long-range 155mm ER02A1 artillery ammunition to be manufactured in Spain. Designed for high-effectiveness counter-battery warfare and scheduled for production through Q1 2027, the contract signals long-term logistical planning that extends well beyond the current year.

- An S&P Global Ratings report noted that large-scale modern AI campuses, with valuations reaching $20 billion to $30 billion, have created capacity bottlenecks in the reinsurance sector. As a result, hyperscalers are increasingly required to retain tail risks—such as power outages and IT failures—on their own balance sheets or through captive insurance structures.

- On Friday, June 26, the FBI issued a Public Service Announcement warning that multiple Russian state-sponsored cyber threat clusters, including FSB and military-linked actors, are running an active phishing campaign targeting high-value political, military, and diplomatic targets. The attackers are impersonating support tools on messaging platforms such as Signal to obtain backup recovery keys and bypass end-to-end encryption, enabling access to historical messages and full account compromise.

Gold Market

This week gold futures closed the week at $4,134.80, up $87.20 per ounce, or 2.15%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 3.42%. The S&P/TSX Venture Index came up 2.06%. The U.S. Trade-Weighted Dollar fell 0.56%.

Strengths

- The best performing precious metal for the week was palladium, up 6.23%. Palladium rallied alongside gold, silver, and platinum after softer U.S. jobs data pointed to slowing economic momentum, boosting demand for precious metals as stores of value. With weaker payroll growth reviving expectations for Fed rate cuts and weighing on the dollar, palladium is benefiting as investors rotate into hard assets to hedge against a softer growth backdrop.

- Gold and the rest of the precious metals got an extra lift on Friday when Change in Nonfarm Payrolls came in at only 57K vs expectations of 113K. In addition, the prior two monthly reading were revised down, which previously showed a rising trend in hiring which could be inflationary if the economy is heating up. The weaker numbers give the Fed some reason to pause considering a rate hike at their next meeting.

- Heraeus reported that China imported 162.6 metric tons of gold in May, up from 99.5 metric tons in May 2025, representing a 63% year-over-year increase. Year-to-date, China’s non-monetary gold imports total 691.6 metric tons, up 76% from 393.6 metric tons during the January–May period last year, although still below the 840.6 metric tons imported during the same period in 2024.

Weaknesses

- The worst performing precious metal for the week was platinum, still up 0.75%. Platinum also advanced alongside its precious metals peers on the soft jobs data, but its move lagged the sharper gains in gold, silver and especially palladium pointing to more tepid participation. That relative underperformance suggests the marginal buyer has yet to fully return to platinum, even as the broader rate-cut narrative lifts the complex.

- Exchange-traded funds cut 403,509 troy ounces of gold from their holdings in a recent trading session, bringing this year’s net sales to 2.21 million ounces, according to data compiled by Bloomberg. This was the biggest one-day decrease since March 4.

- According to BMO, Silvercorp announced that it has temporarily suspended operations at its Ying and GC mines in China to ensure compliance with new nationwide safety regulations. Production is expected to decline 40-50% at Ying from July to September 2026, with a 10-15% impact in the current quarter, leading to an overall reduction to its NAV of 1.4%.

Opportunities

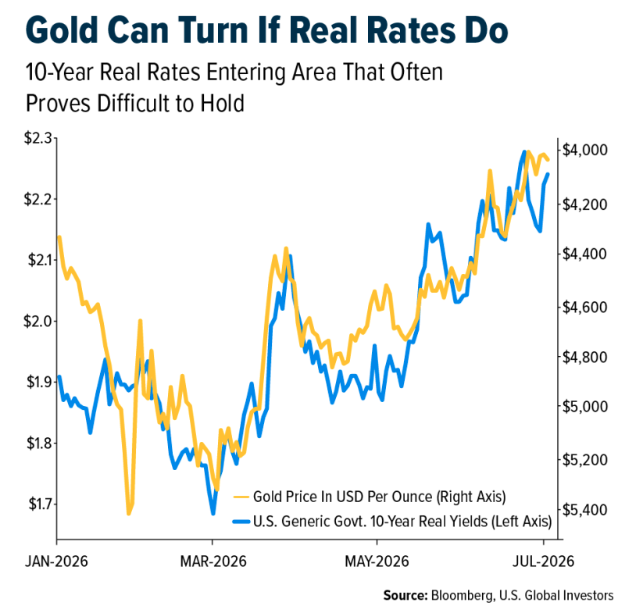

- Real interest rates have moved higher since the conflict with Iran began, coinciding with the appointment of a new Fed chair whom some investors view as more hawkish on inflation. However, Bloomberg’s Brendan Fagan noted that 10-year real yields have repeatedly struggled to break above 2.2% in the post-pandemic period, helping gold stabilize around $4,000. Fed Chair Warsh also struck a more constructive tone midweek, noting that inflation risks have eased in recent weeks while expressing optimism about AI’s potential to boost productivity. If real yields have peaked in the near term, gold may have established a durable price floor.

- According to Scotiabank, every $100 per ounce increase in the gold price raises resource ounces by approximately 4%. With gold averaging about $4,700 per ounce year-to-date, which would bring the three-year average to roughly $3,500 per ounce, the firm expects higher reserve and resource price assumptions at year-end 2026. Scotiabank also highlighted that gold producers currently trade at an average P/E ratio of approximately 11x—the lowest level relative to history since its data series began in 1985. By comparison, the S&P 500 trades at roughly 25x earnings and the Nasdaq at approximately 34x, suggesting gold mining stocks remain attractively valued despite the strong rally in gold prices over the past four years.

- Gold’s 50-day moving average is approaching a crossover below its 200-day moving average, a technical pattern known as a “death cross.” However, historical data suggest the signal has not consistently been bearish. According to Bloomberg, of the 28 death crosses recorded since January 1981, gold prices were higher one month later 57% of the time, higher six months later 57% of the time, and higher one year later 46% of the time.

Threats

- India’s restrictions on gold imports are projected to reduce the country’s demand for the yellow metal by about 10% year over year, according to a World Gold Council report. Demand for gold jewelry, bars, and coins is expected to decline by 50–60 tons year over year due to the import duty hike alone, World Gold Council analysts wrote, citing their econometric analysis.

- According to Goldman Sachs, over the past 3–5 years the capital intensity of building Australian gold projects has roughly doubled across both greenfield and brownfield developments, with rising costs for processing mills being a key driver. Despite this increase, they note that it remains generally more attractive to build than acquire assets, as higher gold prices through the cycle continue to outpace cost and capital expenditure inflation.

- UBS believes rising cost pressures in the gold sector remain underappreciated by the market. While consensus assumes costs have peaked, they expect sector-wide all-in sustaining costs (AISC) to rise by approximately A$110 per ounce year over year in FY27, leading to roughly 5% EPS downside and continued margin compression. While gold is facing near-term pressure from higher yields and shifting rate expectations, UBS maintains a constructive longer-term outlook supported by potential Fed easing and ongoing diversification demand, though the timing of price recovery may be more uncertain.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2026):

Allegiant Travel Co.

Southwest Airlines

easyJet PLC

Air Canada

Air France-KLM

Nippon Yusen KK

Deutsche Lufthansa AG

Tenable Holdings Inc.

Intuitive Machines Inc.

Micron Technology

Royal Caribbean

Volkswagen

Adidas

Nutrien Ltd.

Cheniere Energy Inc.

Silvercorp Metals

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting our prospectus page or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Read additional important information. +

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All