Is the rotation toward value here to stay? What could stall the economic recovery? In the first in a four-part series of blog posts, we explore the key issues that are likely to impact the investment landscape in 2021.

We believe traditional fixed income should continue to provide a reliable source of diversification against a growth shock, but low rates and the risk of an inflation shock necessitate broadening the menu of diversifiers.

Managers of VIX-informed strategies have nuanced understanding of volatility, utilizing it as a tool in all market cycles.

Of the many tales being told to justify record equity valuations, low interest rates are among the more popular. However, that is only half the story.

Many market participants expect major economies to follow a path to recovery similar to China’s, but we see three key factors that suggest China’s recovery may be on its own trajectory.

Although investors don’t normally think about trash when they’re looking for growth stocks, we believe the solid waste industry is well-positioned to outperform. In our view, the combination of high barriers to entry, stable demand, and opportunities for consolidation should provide reliable revenue growth for the foreseeable future.

Industrial metals are well on their way to being among the top performers of 2020, supported by red hot demand from China and global supply concerns.

The virus—or specifically the political response to it—is causing a mass extinction event for small businesses in certain sectors. At the same time, some large businesses are reaping a bonanza of revenue from the same pandemic.

If global growth resumes in 2021, aided by the rollout of vaccines and the Fed’s continued commitment to ultra-low interest rates, some developing countries may be able to avoid default, because yield-hungry investors will continue to buy their bonds. But other countries will not be so lucky.

In Europe, investors like Alessandro Tentori are starting to say their goodbyes to the region’s bond market, worried that soon there may not be any place left for them.

More than most years, it’s hard to look ahead to the next year, to 2021, without looking back at 2020. A global pandemic, a massive economic collapse, a bear market, a surprisingly sharp reversal, a hotly contested election where passions ran high, the impact of lockdowns—it was an unusual year of extraordinary challenges.

We highlight the reasons behind our pro-risk stance in our 2021 outlook in the weekly commentary.

Measured by the bushel, the U.S.-China relationship has never been stronger.

There appears to be a few huge statistical bargains available in the stock market based on the simplified version of Benjamin Graham’s intrinsic value calculation.

Low interest rates and massive stimulus-fueled debt raise investor concerns about potential long-term fallout. But when the cost of capital is this low, it revs up funding for innovation that ultimately fills the pipeline with robust opportunities, especially in technology.

Franklin Small Cap Value Fund Assistant Portfolio Manager and Research Analyst Nick Karzon gives five reasons why we continue to see attractive long-term opportunities for select small-capitalization (small-cap) P&C insurers.

Inflation expectations as priced by the Treasury market are hitting 18 month highs just now. As the reader can see, inflation expectations across all treasury maturities are at cycle highs.

We anticipate that COVID-19 vaccines and the easing of lockdowns will allow for a return to more normal economic activity by mid-2021.

Some changes unfold over time and it’s possible to see them coming. There are demographic changes coming in the next decade that will change the direction of the U.S., since the Silent generation and the Baby Boomers hold a different view of government than Gen Z’s and Millennials.

Whether you’re looking to dust off your CRM software and learn to better use its features, or you’re looking to make a CRM investment for the first time, here’s what you need to know.

Macroeconomists broadly agree that productive infrastructure spending is welcome after a deep recession, especially when interest rates are at record lows. But in advanced economies, any new project typically requires navigating difficult right-of-way issues, environmental concerns, and objections from apprehensive citizens.

In a fascinating little book, The Psychology of Money, the investment manager Morgan Housel provides more useful self-help advice than most authors who explicitly set out to do so.

“Dr. Copper,” so named for the metal’s ubiquitous use in many different applications, has been ripping higher since its 52-week low in March, thanks to a number of factors including promising economic data.

Two weeks ago I talked about Peter Turchin’s idea of “elite overproduction” leading to social and economic crisis. While he doesn’t have any solutions, Turchin helps illuminate how we reached this point. Today we’ll go a little deeper and think about the implications.

Some changes unfold over time and it’s possible to see them coming. There are demographic changes coming in the next decade that will change the direction of the U.S. since the Silent Generation and the Baby Boomers hold a different view of government than Gen Z’s and Millennials.

The better informed the investor is, the better the investment decisions they can make. But being an informed investor can be a very arduous task, and some would even say that conducting research on common stocks is a real snoozer.

Over the last six months, my firm has skewed its portfolio towards defense companies. We have done this intentionally. The world is less safe today than at any time since the Berlin Wall came down.

I see four critical challenges for wealth managers arising from the pandemic.

With the 2020 elections, we are hearing a lot about socialism. Many fear that, should the Democratic party sweep the White House and Senate, an inevitable march toward the US becoming a socialist country will begin.

Zombies are firms that are neither dead or alive. They are in so much debt that virtually all their free cash is used to service their debt, and that is very damaging to GDP growth. This month, we explain why there are more and more zombies all over the world, and why they do immense damage to the global economy.

The institutional investor’s role in the effort to combat climate change is misplaced.

After a difficult winter, we expect the global economy to rebound strongly next year. But structural headwinds remain. Will the post-pandemic bounce trigger a durable and broad-based global reflation?

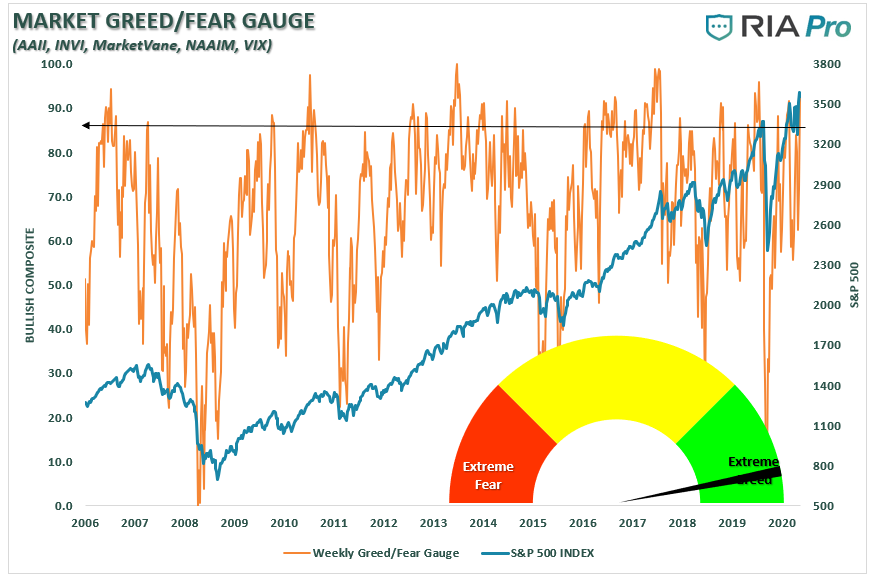

We have recently written a couple of posts about the “exuberance” that has invaded the market since the election. Such is often seen near short- to intermediate-term peaks in markets as investors go “all-in” without a net.

So far this year, shares of HIVE Blockchain Technologies have soared an incredible 715%, well past Ethereum’s gain of 273%. 2020 has been marked by healthy expansion in mining capacity, the most recent example being HIVE’s acquisition of additional access to low-cost green energy.

Recovery from COVID-19 has been a mix of successes and setbacks.

A Happy Thanksgiving weekend to all my US friends. This year was different for many of us—sometimes by choice, sometimes not. But there’s one bit of good news I think we can all share: The holiday season means 2020 is almost over. Soon, we’ll be able to turn the page.

Since early August the “barbarous relic” has corrected some 9% while many other assets have ascended to all-time highs. This has no doubt caused a bit of consternation for holders of gold who have been using the metal not as a hedge, but as a capital appreciation vehicle unto itself.

I’m going to teach you how to communicate successfully with any prospect in two sentences or fewer.

In RBA’s latest report, Rich revisits the "Earnings Expectations Life Cycle" from the perspective of growth versus value investors and outlines why growth investors need to be contrarians in 2021.

Gold “is a hedge on policymakers screwing up, and there has been a lot of screwing up in the last 20 years.”

Today I’m going to blend a few thoughts about The Great Reset with some other historical analysis I recently discovered. It adds up to a disturbing outlook, even if (as seems likely, given the latest vaccine news) we’re past the pandemic by late next year. We’ll find different challenges on the other side.

Trading over the holidays? You’ll want to check this list—errr, article—twice.

In calling the current market the third “Real McCoy” bubble of recent decades, Jeremy Grantham described, in his own words, what I call the Iron Law of Valuation: a security is nothing more than a claim on some set of future cash flows that investors expect to be delivered into their hands over time. The higher the price an investor pays today for some amount of cash in the future, the lower the long-term return the investor can expect on that investment.

Restaurants already endured lengthy shutdowns that hobbled the industry. Now, a new wave of bans on indoor dining from Philadelphia to Seattle is threatening the weakened industry.

As expected, the medical news continues to get worse. New infections hit all-time highs last week as the third wave of the pandemic has accelerated around the country. Case growth in many states remains at levels that threaten health care systems.

There is new reform legislation making its way through Congress which will significantly affect how many of us save for retirement and specifically how, and how much, we can contribute to our retirement accounts and at what ages. This is the most significant retirement saving reform legislation in years. I’ll break it all down for you below.

Investors in exchange-traded funds are clinging to their bets on big tech even as the high-flying sector has lagged behind the broader market over the past week.

This short article investigates the rebalancing premium that investors may expect from risk-parity portfolios.

America, and the world, received a huge shot of hope this week. The $210 billion drugmaker Pfizer announced on Monday that its coronavirus vaccine is 90% effective at preventing COVID-19.

Election results (a divided Washington) and good news on a potential vaccine boosted share prices, although there were some concerns about surging COVID-19 cases (163,402 reported on November 12) and possible difficulties in distributing the vaccine.