Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

As an institutional investor, wealth advisor or portfolio manager, you are hired to understand market drivers. You must know how these drivers influence investing and risk management in order to make intelligent financial decisions. One of the most important drivers is volatility, a characteristic of all markets. Volatility-informed strategies are an asset class that, when embedded in a portfolio, can be instrumental to success. Yet the strategy of managing and trading volatility is sophisticated and should be left in the hands of professionals. When traditional diversification is not enough, the managers you choose can make the difference between a beat the benchmark portfolio and a smart portfolio.

The volatility trio: Realized, historical and implied

Volatility is an unobservable continuous variable defined over a period of time.1 While volatility can be challenging to conceptualize, visualization can help. Picture a man dozing off on the beach. He awakens to an ocean’s tide that has advanced, leaving his towel and newspaper a soggy mess. Like volatility, the tide ebbs and flows, oftentimes unexpectedly. Storms, like news cycles, can develop rapidly in quiet markets.

Assume the man, prior to visiting the beach, gathered data on the average magnitude of the tide, regardless of direction (ebb or flow), on that particular calendar day, for the last 25 years. That data are what’s referred to as realized volatility – the magnitude of daily movements, regardless of direction, of some underlying, over a specific period.2 Alternatively, he may have gathered data on the beach’s tide at 4pm, every day for the last year. This is historical volatility.

While similar to realized volatility, historical volatility in financial terms, calculates the standard deviation of logarithmic returns based on daily closing prices over a given period of time.3 In both cases, with the data, he can calculate how the tide has deviated from its normal state during a selected period. With this information, he might have placed his towel closer to the shoreline or further from it, in expectation of the tide’s actions. These expectations are incorporated in implied volatility.

Historical volatility is often compared to implied volatility to determine if a security is overvalued or undervalued. Implied volatility is not based on the historical pricing data on a security, but rather on what the marketplace is “implying” the volatility of the security will be in the future. It’s derived from that security’s option prices.

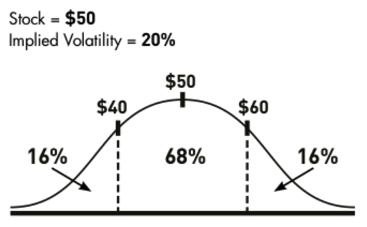

If security XYZ is trading at $50, (figure 1) and the implied volatility of an XYZ option is 20, the marketplace consensus is that a one standard deviation move over the next 12 months will be plus or minus $10 (20% * $50 = $10). Thus, there is an expected 68% chance that at the end of one year the stock will trade between $40 and $60, and a 32% chance it will trade outside this range.4

Figure 1: Normal Distribution of a Security Price

Put volatility to work

The most widely used tool that measures implied volatility is the Cboe Volatility Index® (VIX® Index). Created by the Chicago Board Options Exchange (Cboe), the VIX Index is a real-time market index that represents the market's expectation of 30-day forward-looking volatility. A VIX of 22 translates to implied volatility of 22% on the S&P 500® Index (SPX). It rises when put option buying increases and falls when call buying increases.

While the VIX is monitored by a wide range of investors, as it provides a measure of market risk and investor sentiments, it’s not itself investable.5 The VIX Index, designed to replicate the VIX as a tradeable security, was developed in 1993 by Robert E. Whaley, the Valere Blair Potter professor of management and director of the financial market research center at the Owen Graduate School of Management at Vanderbilt University.

The VIX Index is commonly referred to as the “fear gauge.” Professor Whaley argues, “While it’s a fun name, I see the VIX Index as the price of insurance. The VIX is based on SPX options prices, which reflect what market participants are actually willing to pay to hedge their risk”.

Exchange-listed VIX futures were launched in 2004 and VIX options in 2006. During the 2008--2009 financial crisis, VIX futures and options experienced rapid growth, as interest in and use of index-based products, such as exchange traded products (ETPs), exchange-traded notes (ETNs) and exchange-traded funds (ETFs) increased rapidly.

The year 2020 has been rife with uncertainty – a pandemic, trade wars, raging fires, growing racial inequality, a fractured Congress and a U.S. presidential election, resulting in the VIX well over 20. The all-time highest VIX-Index close was 82.69 on March 16, 2020. But intraday trading this year has surpassed 85. The current backdrop of uncertainty contributes to broad ranges for bull, bear, and base cases for earnings and index levels over the coming 12 months translating to expectations for strong volatility.

Row versus sail: Return to sender, address unknown

Ed Easterling, author, market climatologist and investment philosopher, discussed his book, Unexpected Returns and Probable Outcomes. In chapter 10, “Row Not Sail,” he explains, “The environment does not control investors; they are essentially in control of their portfolios within that environment.” With that sense of empowerment, the investor can choose appropriate strategies.6

Rowing, according to Easterling, is the boatman’s analogy of periods in time where returns are relatively low. “You can’t always be in the position to have the wind at your back; thus, you’ve got to pull out the oars and row in order to achieve a diversified actively managed portfolio.” Sailing, in Easterling’s example, represents a passive approach. “If the market winds are at an investor’s back, then just open the sail, and – like the ’80s and ’90s – enjoy the ride.”

When asked, whether an investor can sail and yet still be tactical, Easterling affirmed, “Absolutely, they are not inconsistent. The wind at your back is a primary driver, as in a buy and hold strategy. It’s is a higher order distinction. When the wind is not at your back, you take a tactical and more active approach. You have to find alpha when there is no beta. If you are in the early phase of a bear market, the question is, how do you row? Lots of ways.”

Easterling’s rowing references the many tools available to a trader, more so today, he emphasizes, than in 2004, when he published the book. In today’s highly uncertain markets, investors should be set for rowing – providing the opportunity to be in control and to look across different investment alternatives.

How to master troubled waters

“We can battle the sea, or we can embrace it. Sometimes she will be sweet and sometimes mean as a snake. We must embrace the experience and trust we will get through it.”—Michelle Segrest

Volatility is a concept that investors either don’t understand, fear, or aim to hedge out of their portfolios, because they associate it with market loss. Others, more comfortable with volatility, attempt to trade the VIX Index, only to discover that it’s not like trading an equity and face significant losses.

Managers of VIX-informed strategies have nuanced understanding of volatility, utilizing it as a tool in all market cycles. They integrate volatility into portfolios and capitalize on it by analyzing the information that volatility reveals.

Information content captured by VIX and volatility signals

The cyclical dynamics of volatility provide clues as to when and how to position for higher or lower volatility regimes. Movement around the volatility’s resting state can inform exposure decisions. Here are five stylized facts when considering market volatility:

1. Equity implied volatility tends to fluctuate as a function of volatility in the underlying drivers of market activity: earnings, macroeconomic data and monetary policy (figure 2). In markets such as the current one, the uncertainty around these macro drivers, fuels equity implied volatility.

Figure 2: VIX Index versus Macro Volatility Indexes

Source: Morgan Stanley Wealth Management

2. Historically, the VIX has been negatively correlated with price movements of stock indexes. This negative correlation tends to increase in times of market turbulence, such as 2008 and 2020. When stock markets suffer sharp declines, expected volatility tends to rise, reflecting an increase in demand for protecting a stock portfolio with SPX put options and the associated increase in option prices as a result of heightened risk aversion.

3. Historically, implied volatility has closely tracked realized volatility, but notable gaps can emerge when investors express greater uncertainty about the future. Over time, VIX index levels reflect volatility expectations that are, on average, higher than realized S&P 500 volatility. This difference is the volatility risk premium. The VIX may stay below average for long periods but will rise to multiples of average levels. It tends to cluster over time into periods of high and low market fluctuations, more so than price returns (figure 3).

Figure 3: VIX (CBOE Volatility Index) and SPX (S&P Index) Percent Change

Source: CBOE

4. Understanding contango and backwardation is a requirement for volatility traders. Futures are in contango when long-term contract prices are higher than those with a shorter time to expiration, and in backwardation when longer-term futures prices are lower than short-term futures prices. VIX futures returns are positively correlated with the VIX but their prices can be significantly above or below spot market VIX levels. When prices are above, its forward curve is in contango, (upward-sloping), and when they are below spot VIX, the curve is in backwardation (downward sloping). A contango curve is by far the norm, but in rare cases of extreme volatility, backwardation can occur, meaning, the opportunity to profit from backwardation is largely limited.

Owners of VIX futures face the cost of rolling VIX futures positions (roll yield). To maintain a constant exposure, the owner must periodically “roll over” to the next contract. In contango, when the next contract’s value is greater than the current one, each “roll” thus exposes an investor to more potential losses if the VIX does not rise (figure 4). During contango when prices are at a premium to the VIX index, buying VIX futures – even in a rising volatility market – can be a dangerous prospect.

|

Figure 4: Price Difference Between First- and Second-Month VIX Futures

|

|

How to source, search and select volatility specialists In sum, volatility-informed strategies are a tradeable asset class that can strengthen portfolios in all market cycles. They can provide meaningful opportunities to source both returns premia and portfolio protection. Harness the power of volatility to let it work for your clients but leave the heavy lifting to experienced volatility traders. Choosing the right asset managers will inspire the confidence needed to orchestrate optimal risk-responsive investment outcomes in varied market regimes. “There is no better tool or equipment you can have on board than a well-trained crew.” —Larry Pardey With VIX-informed strategies, like any investment strategy, some managers are just plain better than others. With proven volatility traders, you can be assured they’re frequently on the right side of a trade. By harnessing and harvesting volatility premiums on behalf of your clients, you can focus on running your practice and coaching clients to stay the course. Choose VIX-informed portfolio managers with well-conceived approaches, experts capable of blending extensive portfolio management experience with deep expertise. They should understand how the VIX Index and VIX-linked securities can serve as tools for tactical trading of volatility, alpha generation and diversification as well as tail-risk hedging in multi-asset portfolios. Risk management must be an asset manager’s first priority. Managers should marry quantitative analytics with tactical expertise built on a fundamental foundation of risk-responsive, cost-conscious, risk mitigation. Strategies built to strengthen portfolio resilience must buffer against major market downturns at a fraction of the cost of buying put protection on the market. A robust system is a pre-requisite to successful implementation. Managers with consistent returns tend to have a repeatable method of analysis and position-sizing – not necessarily a rote, black-box trading system. With a rules-based strategy, an asset manager can create the potential to profit regardless of market direction, using a mix of tactical long/short allocations in equities and VIX-linked derivatives. Seek volatility managers who are versatile and flexible at meeting various investor objectives. Some investors seek uncorrelated return sources differentiated from stock and bond premia. Others may seek risk-managed exposure to major equity indexes for example, to achieve correlation to the underlying equity index only during rising markets. A mixture of volatility management strategies can assist advisors in orchestrating investment outcomes for clients whose objectives run the gamut. Ad a combination of volatility-informed products including funds, exchange traded products (ETPs) and separately managed accounts (SMAs). An SMA for an institutional investor provides a level of transparency and control that investments in traditional limited partnership products may not. And SMAs can provide retail clients access to a variety of volatility strategies otherwise unavailable to them. For portfolio model-makers, SMAs provide access to alternative investments in the context of portfolio completion. Portfolio completion may include tail-risk hedging and capital preservation, harvesting variance risk premiums or portfolio efficiency and risk management. Shelley Goldberg was a commodities strategist for Brevan Howard Asset Management and Roubini Global Economics, a hedge fund manager for G3 Capital Partners and a contributing writer to Bloomberg Opinion. |

1 https://quant.stackexchange.com/questions/37557/criticise-garch-relative-to-realized-volatility

2 https://www.realvol.com/Realizedvolatilitydefinition.htm

3 https://www.macroption.com/historical-volatility-calculation/

4 https://www.optionsplaybook.com/options-introduction/what-is-volatility/

5 https://www.thestreet.com/topic/47306/vix.html

6 https://mebfaber.com/2017/05/31/10168/