The Misguided Role of Institutional Investors in Climate Change

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsOn October 22, 2020, in a history-changing remark during an election debate with President Donald J. Trump at Belmont University in Nashville, Tennessee, presidential candidate Joseph R. Biden, leading strongly in the polls, said he would transition away from fossil fuels.

The world hardly blinked.

That is a measure of how far the movement to slow and stop climate change has come. Recently, one of the chief drivers of that movement has been institutional investors.

And yet, the institutional investor’s role in this matter is misplaced. I will get at that in this article.

Part I: The background

Fossil fuels have powered almost all of civilization’s economic development.[i] For millennia prior to about 200 years ago, global economic growth was nearly zero. The overwhelming majority of all of the world’s growth – both in its economy and in its population – has occurred in the last 200 years. This was the period during which fossil fuels were intensively put to use. Now, a prospective American president was declaring that soon, we would no longer use them or need them.

An alphabet soup of organizations of institutional investors, and of investment strategies and philosophies has helped to bring matters to this point, by endorsing the science and lending credibility to calls for action. One leading group is Climate Action 100+, which is coordinated by five partner organizations: Asia Investor Group on Climate Change (AIGCC); Ceres; Investor Group on Climate Change (IGCC); Institutional Investors Group on Climate Change (IIGCC) and Principles for Responsible Investment (PRI).

Investment strategies and philosophies, broadly called “social investing,” that are intended in part to combat climate change, include socially responsible investing (SRI), impact investing, ethical investing, and most prominently of late, environment, social, and governance (ESG) investing, also known as sustainable investing.

A new report has provided further mainstream investment industry validation of investors’ role in the movement. It is “Climate Change Analysis in the Investment Process,” from the CFA Institute, the professional organization that offers the Chartered Financial Analyst designation, whose stated mission is “To lead the investment profession globally by promoting the highest standards of ethics, education, and professional excellence for the ultimate benefit of society.”

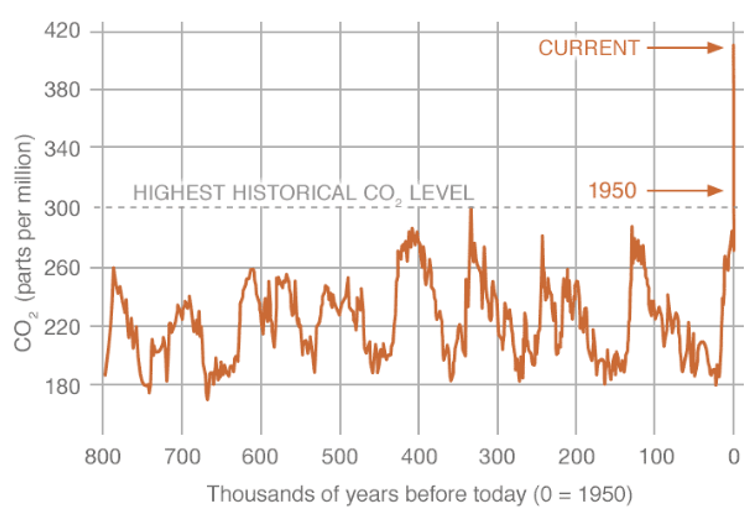

The CFA Institute report begins by going through the basics of climate change. A greenhouse effect is enhanced by emissions into the atmosphere of several greenhouse gases created by industrial processes. These gases cause heat to be trapped in the atmosphere and in the oceans by retarding the escape of heat radiation from earth to outer space. The greenhouse gas whose emission causes most of the effect, directly or indirectly – more than 80% of it – is carbon dioxide or CO2, which results from the burning of fossil fuels.[ii] The presence of these greenhouse gases in the atmosphere – chiefly CO2 – has for tens of thousands of years moderated Earth’s temperature so that it has been ideally conducive to human and animal life. But their rapid increase in the last 200 years, particularly the last 50 years, threatens to raise that temperature to a dangerous level (see graph).

https://climate.nasa.gov/vital-signs/carbon-dioxide/

The anticipated result, according to the CFA Institute report, is that “A hotter planet means more drought, more famine, more extreme weather events, more property damage, and more dislocation of humanity than any of us have seen in our lifetimes. We cannot know when on the calendar these disasters will arrive, but we can be confident that they will.”

The economic impacts

The CFA Institute report says, “Climate change may be the most economically impactful event in human history.” The report estimates the present value of the cost, quoting Sarah Breeden, former executive director of the Bank of England’s International Banks Supervision, at from US$4 trillion to US$20 trillion.

Citing a JPMorgan study, the report notes that although climate change will impact GDP growth, “At a growth rate of 2% a year, global GDP would reach around US$500 trillion at the end of the century. A loss of even 7% … would still leave the level of GDP in 2100 over four and a half times higher than today.”[iii]

Thus, while climate change will cause global GDP to be 7% lower at the end of the century than it would be otherwise, GDP will still be four and a half times as high as today – a substantial rise in spite of the impact of climate change.

Nevertheless, three additional concerns arise. First, the CFA Institute report laments the fact that the discount rate implies that, “cash flows far into the future have next to no present value.” Investor and climate change research philanthropist Jeremy Grantham points out that therefore, “grandchildren have no value.” (But see here the difficulty with assigning them too much value.)

Second, the report notes that the models “all have the handicap of being based on the assumption that societies will go on as they have before, just at a slightly slower pace. But climate change is seen as a potential threat to our very existence.”

This is the “tail event” concern about climate change. It can justify a large investment in climate change mitigation and prevention as a form of insurance against that low-probability but catastrophic threat. This argument was best stated in Gernot Wagner’s and Martin L. Weitzman’s 2016 book, Climate Shock: The Economic Consequences of a Hotter Planet.

The third concern, not stated in the CFA Institute report or almost anywhere else for that matter, is that GDP projections like these are simply wrong, or at least not truly meaningful. The “costs” of battling or adapting to climate change will be contributions to GDP, not subtractions from it, just as the costs of cleaning up environmental damage are contributions to GDP because they are expenditures that are counted as “consumption” in the calculation of GDP. This is a common criticism of GDP itself as a measure of economic well-being. Nevertheless, projections of GDP are made as if it were something separate and apart from the figure as it is actually calculated.

The investor movement against climate change

Over the last several years the movement by institutional investors organized against climate change has gathered pace. Numerous organizations of institutional investors like those mentioned above have formed, and have issued statements and guidelines for investors and for the companies they invest in.

The acceleration of this movement can be seen especially strongly in the proliferation of ESG funds and ESG or “sustainability” advertising by investment management firms. A recent study by Boston College’s Center for Retirement Research (CRR) reports that, “In 2018, money managers applied some kind of ESG criteria in their investment decisions for about $12 trillion of assets.” This figure was up from $8.7 trillion in 2016, $6.6 trillion in 2014, and $3.7 trillion in 2012.

An industry of ESG rating agencies has arisen, including such firms as MSCI, Sustainalytics, Bloomberg, and Thomson Reuters. An ESG rating is assigned to each listed corporation – and by computing a weighted average of the constituent companies, to an entire stock or bond portfolio. Thus, a portfolio’s favorable ESG rating is a result of ESG-friendly stock picking.

The “environment, social, and governance” aspects of ESG encompass a variety of criteria. In the “environment” category is included not only a score on how well the company abates carbon emissions[iv], but also its handling of other environmental inputs and outputs, such as water and plastic waste. In the “social” category the company may get a rating on such measures as inclusion or diversity, based on the percentages of its employees who are minorities and women and on its stated hiring policies. In the “governance” category are measures presumed to be of good governance, and may include the ratio of executive-level compensation to the compensation of the average employee, or how many independent board members the company has. All of those ESG criteria vary from rater to rater.

A perusal, however, of the MSCI ESG Funds Rating Summary – for example – tends to reveal that the most prominent features of ESG ratings relate to the reduction of carbon emissions. These can include a company’s carbon footprint (how much carbon it emits or causes to be emitted, per unit of revenue or profit) and its commitments to alternative energy – the purpose of which, of course, is to lower carbon emissions.

Emphasis in these evaluations is placed on disclosures and transparency, goals, five-year plans, and the signing on to resolutions drawn up by recognized bodies or organizations that target the reduction of carbon emissions, or other ESG-friendly goals.

Formulating such goals and being transparent about it is not synonymous with achieving such goals. It is implicitly assumed, nevertheless, that aspiration will translate sooner or later into action. But investors cannot tell whether such an assumption is correct.

Part II. Past failures and a new metaphor

Some of the current approach to reducing greenhouse gas emissions has evolved without much plan or strategy. Many efforts have failed in the past but little appears to have been learned from those failures. The 1997 Kyoto Protocol, subscribed to by 84 signatory nations, who agreed to limit their carbon emissions over the 2008-2012 period resulted in almost none of them meeting the commitments to which they had agreed.

It is generally assumed that the Paris Agreement of 2016, in which numerous countries were to submit their plans and goals for limiting carbon emissions, will not achieve its objectives – but the participants believe it is important to continue with the process anyway, because, again, aspiration will eventually turn into action. They believe it is better to do something even if only setting unreachable targets, rather than to do nothing – the danger, of course, being that this approach will, sooner or later, render targets and resolutions less credible.

Germany, a leader in committing to an energy transition toward renewable energy, or Energiewende, while massively increasing energy output from wind and solar panels – and at the same time helping to decrease their costs precipitously by outsourcing manufacturing to an innovative China industry – has failed so far to meaningfully reduce carbon emissions, because it simultaneously phased out its zero-carbon-emitting nuclear power plants.

What is going on here? An observer might understandably conclude that all the efforts to reduce carbon emissions – and all the advertising for ESG-certified investing – amount to “a tale told by an idiot, full of sound and fury, signifying nothing.”[v] It is because of awareness of these failures that a Swedish teenager named Greta Thunberg was invited to address world leaders about the lack of progress on climate change at meetings of the World Economic Forum and the United Nations, where she angrily declared, “How dare you – you have stolen my dreams and my childhood.”

In a section titled, “Can Social Investing Solve Social Problems,” the Boston College CRR report states flatly that stock selection is unlikely to slow global warming.[vi] The problem, it concludes, is twofold. ESG ratings tend to vary widely from rater to rater, partly because the ESG categories cover such a broad range of goals, and address different categories that are themselves extraordinarily diverse. Second, there is little or no evidence that ESG-based stock selection has any impact on stock prices.

Statements and expressions of intent, and requirements for disclosures, it would seem – sometimes dismissed as mere “virtue-signaling” – are substituting for meaningful action. Perhaps the movement against climate change has veered off into some fantasy land. It might be necessary to back off, detach ourselves momentarily from this movement, and try a new tack in our thinking about the issue.

I will make an attempt to do this by shifting attention to a different scenario, one that is not global warming or climate change but has similar characteristics. Perhaps by doing this we can free ourselves of the enormous burden of accumulated baggage that has accompanied the climate change discussion. The baggage includes on the one hand – among some of the advocates of climate change action – increasingly shrill alarms based on too-dire projections of doom and too sweeping labeling of skeptics of such action “climate deniers.” On the other hand – among some of the skeptics about such action – objections based not so much on the threat of climate change itself but on the ancillary concerns and demands with which it is packaged.

This burden of baggage has skewed the debate so that entirely unrelated issues, for example, imperfect ESG ratings[vii], have become an integral part of it for no good reason. As a result, exaggerated objections are raised on the one hand, and panic alarms are sounded on the other that have little to do with the reality of the problem.

I shall paint this metaphorical alternative scenario. I will do this with the help of a web-based tool that you may find a handy substitute for a video game.

Scientists discover a new existential threat

Astronomers are constantly scanning the heavens. They are searching for many things – clues to the origins of the universe; the chemical makeup of various types of heavenly bodies; the possibility of life on planets somewhere else in the firmament.

But they are also looking out for the possibility that an asteroid, comet, or large meteor may be on a trajectory that could intersect with earth’s.

In the early months of 2021, as if not enough had happened worldwide in 2020, astronomers begin to perceive a worrisome object. It appears to be five kilometers in diameter and composed of dense rock. And its trajectory will bring it uncomfortably close to the earth in the year 2082, most likely on a collision course. The astronomers name the asteroid Cassandra.

This asteroid is at least, fortunately, not as big as the one that at the end of the Mesozoic era 66 million years ago created the Chicxulub Crater in Mexico and destroyed the dinosaurs. But it is big enough to cause grave damage to the earth and to our civilization if it hits the earth or even grazes it.

Fortunately, scientists have developed a model[1] to help assess the damage that Cassandra could do. Since the earth’s surface is two-thirds water, the greatest likelihood is that it will crash into the ocean. Let us suppose, using that model, that the depth of the water where it lands is 1,000 meters and that it hits at an angle of 45 degrees at 20 km/sec (the estimated speed at impact of the Chicxulub asteroid).

Then according to the model, as far as 1,000 kilometers away there will be a tsunami with a height of between 31.8 and 63.6 meters (104 to 208 feet). (By comparison, the tsunami that hit Fukushima, Japan, in 2011 killing an estimated 16,000 people reached a maximum height of 38 meters.) A fine dusting of ejecta with occasional larger fragments with an average thickness of 1.64 cm will arrive 1,000 km away eight and a half minutes after impact. The maximum wind velocity at that location will be 62.3 m/s (139 mph).

Economic impact

Although initially little is known about where the asteroid will impact and therefore what kind of damage it will do, scenarios can be constructed and their estimated probabilities. A probability-weighted average over those scenarios estimates that the damage will cause an expected 7% reduction in global GDP.

Over time, more will be learned about Cassandra’s trajectory. These scenarios can be narrowed down, and their probabilities and their impacts can be calculated more precisely.

In the meantime, preparations must be made. It may seem that the incident being forecast is a one-time event, but that would be mistaken. For many years and in fact decades, preparations will have to be made, both for the mitigation of the effects of the impact – perhaps even its prevention – and the adaptation to its effects and aftereffects.

As the asteroid nears and calculations of the location of impact and the implications thereof become more accurate, preparations must be made for the evacuation, migration, and/or protection of the affected populace and their structures and industries.

Simultaneously, scientific, technological, and engineering research and development will focus on whether and how Cassandra can be deflected so that it can either be made to miss the earth completely, or to land where the effects of its impact will be more manageable.

Plans will have to be put in place long in advance of Cassandra’s impact, especially once it is determined more accurately where it will hit and what the consequences will be, to relocate affected populations and rebuild their habitats, either before or after impact. After impact, these plans will be altered as necessary, refined and implemented over the subsequent years.

Cost-benefit analyses can be performed to determine how much it is worth spending to facilitate these adaptations, or to mitigate or even prevent the damage that Cassandra could inflict on impact.

Sectors of the economy to be engaged in these efforts

Let us consider how the economy, governments, and industry should respond to these challenges. And what is the role of institutional investors?

It is hard to see a central or even major role for most institutional investors. What could be the role for an industry whose key expertise lies in setting unrealistic goals (principally for investment performance) and then creating sophistic explanations for why those goals have failed to be achieved – or to claim achievement of goals that are not in fact the original ones but result from subtly moving the goalposts? Assigning too much responsibility to such an industry would seem a recipe for pretending to meet, but failing to meet the objectives – much as the objectives have so far failed to be met in the fight against climate change.

When the former Soviet Union launched Sputnik, its earth-orbiting satellite, in 1957 – demonstrating technology in space superior to that of the United States – the U.S. met the challenge with the obvious response: heavily fund science and technology research and development. Within a year after Sputnik’s orbital flight on October 4, 1957, the Eisenhower administration launched NASA, the National Aeronautics and Space Administration. Scarcely a decade after that the United States landed two men on the moon, decisively winning the technological battle for space supremacy and challenging the Soviet Union to an expensive technology race that contributed to its ultimate downfall. And NASA produced a cornucopia of technological innovations that venture capitalists have been exploiting beneficially ever since.

It did not propose to meet the challenge by involving institutional investors, finance professionals, or even economists, though economists managed to get a piece of the action by increasingly mathematizing their research. The sectors of the economy chiefly mobilized were the scientists, the technologists, the engineers – and their government sponsors and funders.

And those, if we were to think through the response to Cassandra in a rational manner, would be the sectors that should be involved in the response to Cassandra.

But in today’s world, when “the market” is thought to be the supreme driver, and institutional investors are believed to be the lords of the market – when in fact they do not drive the market but are, for the most part, little more than its absurdly well-compensated factotums – the unfortunate government response might be to default to the market, which would not, of course, be in a position to meet the challenge of Cassandra very well.

The obvious metaphorical correspondence

Should it need to be said, the purpose of this metaphor was to posit a threat that is in many ways like the threat of climate change. It was to introduce a “change of venue” to get our thinking free of the mire of associated but irrelevant concerns that has burdened the furor over climate change.

We are only beginning to try to identify and work our way out of that mire. But first let us draw the parallel more explicitly.

The Cassandra threat – though its primary impact, unlike climate change, will be concentrated at a single moment in time – will have aftereffects on the environment that could last decades. And it will be preceded by efforts over decades to research it, attempt to abate it, and prepare to adapt to it. Its estimated expected impact on future GDP is about the same as the expected impact on GDP of climate change, if nothing were done to mitigate it. And even more drastic negative effects are possible though unlikely. (For example Cassandra could impact earth tangentially, possibly boring a 250 km groove in its surface to a maximum depth of 5 km.) More will be known over time about its trajectory, as further research and observations are performed in the future.

An array of experiments and pilot projects will be necessary. In the case of Cassandra, experiments and pilot projects will test the possibility of altering the path of the asteroid (research is already being conducted into this possibility, though at a low level of funding), and to plan the fortification or protection and/or migration of populaces, cities, and industries.

The climate change response

In the case of climate change many experiments and pilot projects are necessary both to reduce the emissions of greenhouse gases and, as with the Cassandra challenge, to plan the fortification or protection and/or migration of populaces, cities, and industries. There is no certainty what combination of strategies will best meet the challenge, so research on all of them needs public investment.

Development of lower cost, and reliably manufacturable and replicable designs for nuclear power plants need to be researched, developed, and built, as a way to back up and complement renewable energy expansion. For greater flexibility in its role in the electric power grid, research and development of the nascent industry of small modular nuclear power plants needs to be accelerated. Research and efforts to scale up carbon capture and storage projects is needed[viii], in partnership perhaps with the private conventional energy industry, such as oil companies, whose fossil fuel resources will be stranded if they cannot be utilized. Research on battery technology and its cost reduction needs to be better funded. Development of alternative fuels, such as hydrogen produced from low-carbon electricity and their means of delivery needs to be scaled up. Also needed is extensive research and development of software and hardware to reduce energy demands and shift the times of their impacts. Development of the electric power grid with both high transmission wires and expanded distribution networks is essential to enable the dovetailing of different sources of energy, especially those with variable patterns of output over time such as wind and solar.

Precedent exists for these investments, such as the Tennessee Valley Authority and national rural electric cooperatives, government projects that enhanced the United States electricity grid and extended it nationwide. Both were highly successful.

An argument could be made, nevertheless, that instead of establishing a new government agency like NASA to deal with the problem – Cassandra in one case, climate change in the other – we could instead do nothing, or “leave it to the market.” After all, the expected impact is only 7% of GDP. It will cost trillions to try to prevent that. Is it really worth it?

But would we really do nothing in the face of a likely collision with a five kg-diameter asteroid in 60 years? Would we really “leave it to the market” – would we believe that would work? Perhaps we would wake up.

Conclusion: The guilt project

Whatever the response to Cassandra, would we lay on top of that response, or in combination with it a program to also increase the racial, ethnic, and gender diversity of work forces in public companies, and to improve the representativeness of corporate boards and reduce disparities of incomes between corporate executives and employees?

This is unlikely. The one has nothing to do with the other.

Then why are we combining the response to climate change with those other goals, in the form of ESG investing?

The answer, I believe, lies in what I will call the ”guilt project.”

It has become conventional wisdom that we, modern civilization, especially in the developed West, should be feeling guilty about a number of things – most prominently our history of slavery, but also the near-genocide of Native Americans, the colonization and merciless exploitation of less-developed countries, and the enduring trace negative consequences of those evils, and the yawning gap in levels of wealth that exists now.

And among those ills we do indeed have much to feel guilty about – and to atone for and to repair.

But we have no need whatsoever to feel guilty about the exploitation of fossil fuels, any more than we should feel guilty now about our use of whale oil 200 years ago. It doesn’t belong in the guilt project.

Had we not transitioned from using whale oil to fuels derived from petroleum, and if our economies were still, now, almost entirely dependent on whale oil, perhaps we should feel guilty – and we would have been the poorer for it. But we did transition. And we have benefitted luxuriously from our use of fossil fuels. And there is no reason at all to feel guilty about that – and certainly not if we transition from their use now, when we need to.

What we need to understand about “sustainability” – the new Holy Grail – is that it is not some Utopian end-stage we will ultimately reach, in which we will use each and every resource sustainably and our economy will achieve a steady state. Even in a rainforest, ecologists tell us, the ideal of a “climax” forest that is in a steady state and perfectly sustainable is a myth.

Sustainability is not a steady state; it is nothing but an endless procession of temporary but unsustainable measures, each substituting for the one that came before.

It is time to substitute a new energy economy for the one that came before, even though that one has sustained us so well for the last 200 years. This will take a massive transition, on the order of the energy transition from whale oil and wood to fossil fuels that powered the industrial revolution in the 19th century. There is no reason to believe this transition will be harmful to the economy.

But that transition will not happen all by itself. The path to it is not sufficiently or even necessarily paved by virtue-signaling statements and resolutions made by groups of institutional investors, no matter how prestigious they may be.

We need to re-establish the obvious fact that while institutional investors have supporting roles, the bedrock of civilization’s advancement is science and technology – not finance and economics.

Economist and mathematician Michael Edesess is adjunct associate professor and visiting faculty at the Hong Kong University of Science and Technology, chief investment strategist of Compendium Finance, adviser to mobile financial planning software company Plynty, managing partner and special advisor at M1K LLC, and a research associate of the Edhec-Risk Institute. In 2007, he authored a book about the investment services industry titled The Big Investment Lie, published by Berrett-Koehler. His new book, The Three Simple Rules of Investing, co-authored with Kwok L. Tsui, Carol Fabbri and George Peacock, was published by Berrett-Koehler in June 2014.

[1] May need to enable flash: In Google Chrome, click on the lock icon to the left of the url and Allow Flash.

[i] “Fossil fuels” are those believed to have been formed millions of years ago from decaying biological matter: coal, oil, and gas. Fossil residues formed more recently, on a scale of years or decades (such as wood and other biofuels), are considered carbon-neutral (i.e., emitting no long-term carbon) because more biological matter will grow in their place, absorbing CO2.

[ii] Part of the effect is due to the fact that some warming enables the atmosphere to hold more water vapor, which is itself a greenhouse gas and thus leads to more warming – this is called a positive feedback loop.

[iii] Estimates of the loss of GDP due to climate change range widely but one typical academic study projection is that in a “business as usual” scenario (i.e. no action taken to prevent climate change) temperature would rise more than 4 degrees Celsius by the year 2100 and GDP would be reduced by climate change by about 7 percent.

[iv] “Carbon emissions” generally refers to emissions of greenhouse gases including but not limited to carbon dioxide. Other greenhouse gases such as methane and nitrous oxide also have a greenhouse gas effect when emitted into the atmosphere. Their warming impact is measured in units of “carbon dioxide equivalent” or CO2e. All greenhouse gases are often bundled under the simplifying term “carbon” as in “carbon emissions,” even if the emissions are not of CO2 itself.

[v] Macbeth, William Shakespeare, Act 5 Scene 5.

[vi] It also reports that ESG funds, and those directed to make certain investments by state mandates, reduce annual returns by 70 to 90 basis points. It further reports that the fees paid by these funds are roughly 80 basis points higher than their low-cost Vanguard mutual fund counterparts; thus, these funds underperform by the amount of their fees while doing little to achieve their vaunted goals. It would seem that the ESG industry is a bonanza for ESG investment managers and the ESG rating industry. Money managers might be embracing ESG as a salvation from the recent landslide toward low-cost index investing. Evidence of this can be found in the proliferation of advertisements for ESG investing.

[vii] Boston College CRR’s report notes that MIT researchers looked at the methods used by six different ESG-rating providers and found that their assessments differed significantly. (Berg, Florian, Julian Kölbel, and Roberto Rigobon. 2020. “Aggregate Confusion: The Divergence of ESG Ratings.” Available at: https://ssrn.com/ab- stract=3438533)

[viii] The only real hope for meeting the most ambition mid-term (a few decades) climate stabilization goals is direct removal of carbon dioxide from the atmosphere and/or the ocean. In that area, this is the most promising development I have seen. But it will require a massive increase in zero-carbon energy generation, such as from nuclear energy and renewables.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All