The Rebalancing Premium in Risk Parity Portfolios

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This short article investigates the rebalancing premium that investors may expect from risk parity portfolios1. It is offered as an appendix to the paper, “Risk Parity: Methods and Measures of Success”.

I define rebalancing premium as the difference between the compound return on a portfolio, and the weighted average compound returns produced by the underlying investments in a portfolio.

I examine the distribution of rebalancing premiums for a simple risk parity implementation (a version of the Permanent Portfolio) consisting of US stocks, gold and bonds from 1982 through May 2020. I then proceed to analyze historical and expected future rebalancing premia for a variety of global risk parity strategies composed of 64 futures markets from June 1985 through May 2020.

When applied to the three markets in the Permanent Portfolio I surface a rebalancing premium of approximately 1.2% per year. The most diversified risk parity portfolios produced a rebalancing premium of more than 3% per year.

In the current low return environment, a diversified risk parity portfolio with a 2-3% rebalancing premium may represent an attractive alternative to global 60/40, with the added benefit of owning a diverse set of markets that benefit from a wider range of economic outcomes.

Introduction

When scaled to the same volatility as S&P 500 futures2, the compound excess returns on S&P 500, gold, and 10-year Treasury futures from June 1982 through September 2020 were 7.2%, 0.6%, and 12.4%, respectively.

One might expect that a portfolio that preserved a one-third allocation by regularly rebalancing back to target weights would have produced a return equal to the average of their constituent compound returns: 6.74%. In fact, a strategy that rebalanced at the end of each month to preserve equal risk weighting produced a compound return of 7.93, a full 1.19% per year higher than the average of the three.

This effect is referred to variously as the “rebalancing premium,” “volatility harvesting,” “volatility pumping,” or “gamma scalping.” It emerges mechanically from the process of continuously selling uncorrelated assets with gains to purchase assets with losses (and vice versa) from period to period.

Returns from uncorrelated volatility

Importantly, the rebalancing premium is not a property of markets per se. Rather, it emerges directly from entropy – the unleashed potential of randomness itself. I can observe this directly from the properties of portfolios consisting of synthetic markets with random returns.

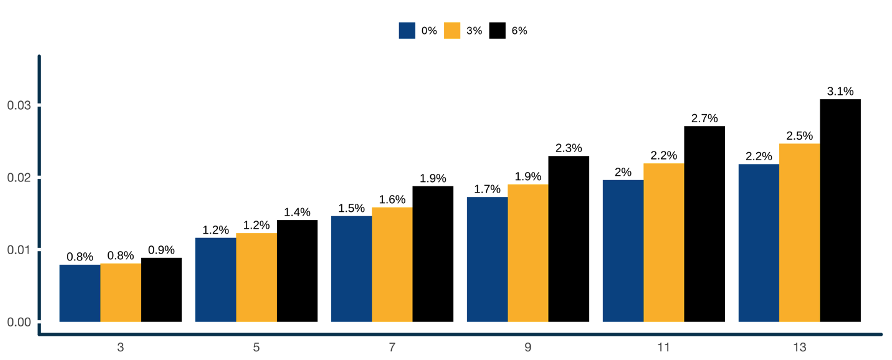

To illustrate, I simulated random monthly returns (i.e. synthetic market returns) by sampling from a random normal distribution. Specifically, I generated synthetic returns for a ‘market’ by drawing 461 random returns3 from a normal distribution consistent with the monthly standard deviation of S&P 500 futures. I analyzed portfolios with two ‘markets’ through 13 ‘markets’ to observe how the rebalancing premium scales with the addition of new independent (i.e. uncorrelated) investments. All portfolios were scaled to the same 10% annualized volatility. In addition, I observed the rebalancing premium when I set average returns to 0, 3, or 6% compounded annually4.

Figure 1: Expected rebalancing premium conditioned on number of uncorrelated markets and average compound drift

Analysis by ReSolve Asset Management. Data from CSI. Past performance does not guarantee future results. SIMULATED RESULTS

Some readers may be surprised to learn that a portfolio, which rebalances between three uncorrelated return streams, each with a zero compound return, can produce a 0.8% annualized return purely from rebalancing. More dramatically, an investor who can find 13 uncorrelated investments that average 3% compound returns may generate 2.5 percentage points extra yield per year in rebalancing premium.

It may seem far-fetched to find 13 uncorrelated return streams. I will show that thoughtful investors can manufacture over a dozen uncorrelated investments from a diversified risk parity universe consisting of global stock and bond indices, and individual commodities.

Minimizing volatility drag

While many dynamics interact to produce a rebalancing premium, an important contributor is the reduction in portfolio volatility that manifests as a function of portfolio diversification. Remember that while financial papers often cite arithmetic average returns to determine the statistical significance of various effects, this is not the rate that investors actually grow wealth in practice. Rather, investors experience a series of returns, which compound over time.

A portfolio with an expected arithmetic mean return of μ percent per year and a standard deviation of returns of 𝜎 percent per year will actually be expected to compound at a rate of

![]() percent per year5.

percent per year5.

Thus, if we compare two investments with the same mean expected return, say 3% per year, but portfolio A has a volatility of 5% and portfolio B has a volatility of 20%, the lower volatility investment will produce a higher expected wealth.

An investment of $100,000 in portfolio A would be expected to grow to $176,278 while an investment in portfolio B would be expected to grow to just $122,019.

It follows that if you can combine volatile investments in such a way that diversification reduces overall portfolio volatility, the portfolio will produce a rate of growth that is greater than the sum of its parts.

In the following pages you will see that sufficiently diverse portfolios with optimal diversification may produce well over 2% per year in rebalancing premium. In the current environment, with many stock markets trading at relatively low earnings yields despite record profit margins, and global bond markets trading near the lowest yields in history, the ability to generate 2% or more in excess compound returns, with no expected increase in risk, should not be overlooked.

Rebalancing the Permanent Portfolio

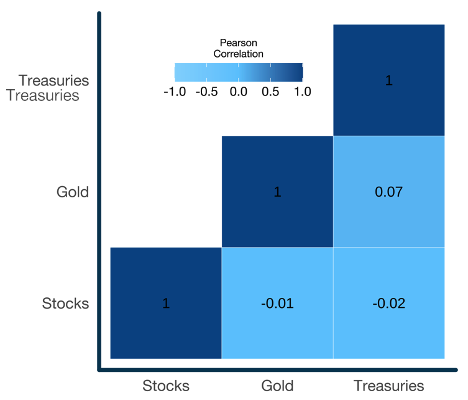

Let’s observe the rebalancing premium produced by a real portfolio of uncorrelated markets. For our case study I examine a simple version of Harry Brown’s Permanent Portfolio. My implementation holds equal volatility weighting in S&P 500, gold, and U.S. Treasury futures, for which we have daily total return data from June 1982 through September 2020. Figure 2 shows the daily pairwise correlations over the full sample period, which are effectively zero.

Figure 2: Daily Pearson correlations, June 1982 – September 2020

Analysis by ReSolve Asset Management. Data from CSI. Past performance does not guarantee future results. SIMULATED RESULTS.

To be consistent with the experimental design above stocks, gold and Treasury returns are levered to the same long-term average daily volatility. There are negligible excess costs on leverage for futures contracts.

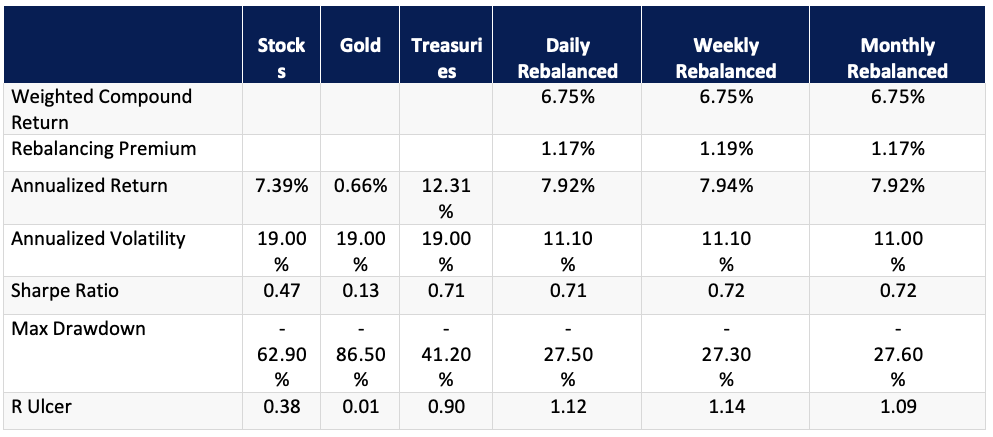

I plot the performance of the constituent markets and the equally risk-weighted portfolios rebalanced at daily, weekly and monthly frequencies in Figure 3.

You’ll note that the weighted average sum of constituents’ compound returns for the portfolios (average of daily weights x annualized compound returns for each market) was about 6.75% per year. Rebalancing between the assets added about 1.2% per year so that the portfolio compounded at just shy of 8% per year.

Figure 3: Cumulative growth and performance statistics for Permanent Portfolio and constituent assets, 1982 – May 2020. SIMULATED RESULTS

Analysis by ReSolve Asset Management. Data from CSI. Past performance does not guarantee future results. SIMULATED RESULTS.

Rebalancing risk parity

I investigate the properties of the rebalancing premia for a variety of global risk parity implementations as described in the reference paper.

Recall that our investment universe for analysis consists of 64 futures markets. I eliminate currency markets because there is no coherent way to define long or short exposure. Allowing for a one-year estimation window for portfolio parameters I start tracking all simulations in 1985. Markets are added once they have one year of returns.

Continuous contract returns are computed by rolling front-month contracts when two consecutive days of both volume and open interest have migrated to the next contract.

Setting expectations

Let’s take a moment to estimate the rebalancing premium that I might expect given the distribution of historical compound returns and the effective number of uncorrelated assets.

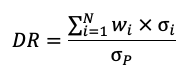

I derive the effective number of uncorrelated assets by taking the square of the diversification ratio of the most diversified portfolio.

where 𝑤i is the weight on asset 𝜎i, is the standard deviation of asset i, and 𝜎p is the standard deviation of the portfolio.

where 𝑤i is the weight on asset 𝜎i, is the standard deviation of asset i, and 𝜎p is the standard deviation of the portfolio.

Of course, in practice we must estimate the most diversified portfolio from historical returns6. These estimates are imperfect so we will not get the full benefit of all potential diversification. When I solve for the most diversified portfolio at the end of each month and apply the estimates to returns in the next month I observe the time-series of effective bets described in Figure 4.

Figure 4: Number of out-of-sample independent bets through time, rolling 252-day average. SIMULATED RESULTS

Analysis by ReSolve Asset Management. Data from CSI. Past performance does not guarantee future results. SIMULATED RESULTS.

On average we are able to extract approximately 13 independent bets from the 64 markets in our risk parity universe. The weighted average annual compound return of the markets is just over 3%. If we refer back to Figure 1, and perform the same computation for 13 uncorrelated markets with compound returns of 3%, and scale the portfolio to 10% volatility, we would expect a diversified risk parity strategy to produce an annual rebalancing premium of about 2.5% per year.

Empirical results

Now let’s examine how the rebalancing premium contributes to realized performance for each of our risk parity implementations.

To recap the simulation methodology, at each daily time step I solve for the portfolio that meets the target objective based on volatility and covariance estimates derived from historical returns. Portfolio weights are scaled to target 10% annualized volatility as a function of the weights and the estimated covariance matrix. I then rebalance to the target portfolio at the close of the following day’s trading.

For weekly rebalanced portfolios, each day I rebalance to the optimal daily weights averaged over the previous five days. This approximates the effect of rebalancing weekly, on each day of the week. For monthly rebalanced portfolios I rebalance to the optimal daily weights averaged over the previous 21 trading days. This approximates the effect of rebalancing monthly, on each day of the month. In Figure 5 I decompose the total compound annual returns of each risk parity implementation into those attributable to the sum of weighted geometric returns for each market, and the rebalancing premium. Results may be slightly different than those reported in the reference paper due to rounding and differences in rebalancing.

Figure 5: Decomposing total compound returns into weighted average market returns and the diversification premium. SIMULATED RESULTS

Analysis by ReSolve Asset Management. Data from CSI. Past performance does not guarantee future results. SIMULATED RESULTS. Please see details of methodology and disclaimers in the reference paper.

All things equal, rebalancing premia are a function of the dispersion in risk-adjusted returns across portfolio constituents, and how well the constituents diversify one another to lower overall portfolio volatility7.

Where implementations resulted in more concentrated allocations toward markets with very high in-sample Sharpe ratios (such as Inverse Variance [INV-VAR] or Hierarchical Risk Parity [HRP-VAR] methods, which typically concentrate risk in bonds), I observe that rebalancing was actually detrimental to portfolio returns.

As noted in the reference paper, historical results for these methods probably substantially overstate what investors should expect from bond-heavy portfolios going forward because historical returns benefited from high average yields in the sample period. In contrast, at time of writing the Vanguard Total World Bond ETF currently boasts a Yield to Maturity of 0.75% with an average duration of 7.6 years, implying less than 1% expected returns over the next 15 years8. In addition, a high concentration in bonds makes these methods especially vulnerable to inflation.

On the other hand, maximum diversification methods produced the highest rebalancing premium. The average premium across MAX- DIV and HRSS MAX-DIV methods was 2.3%. They achieved this high rebalancing premium by creating the effect of maximizing weighted average portfolio volatility while minimizing the volatility drag on the portfolio.

This high premium is the icing on the cake for maximally diversified portfolios. These methods were above-average performers in the historical sample in terms of returns and drawdown risk, without relying on high exposure to bonds. Moreover, by virtue of their extreme levels of diversity and balance, they produced highly persistent positive returns across economic regimes.

Note also that monthly rebalancing produced the highest rebalancing premium. This may be due to several interacting effects. First, rebalancing is more effective if the relative returns to time-series are trending between rebalances and mean-reverting after. There is evidence that futures exhibit momentum9 and trending10 behavior at monthly horizons.

In addition, recall that I construct the monthly rebalanced strategies by averaging the optimal daily weights over 21 days. This averaging acts as a shrinkage method or regularization step on the weight vector, which may produce a less biased estimator of out-of- sample covariances, and allow portfolios to better capture available diversification opportunities.

Do the results generalize?

It is reasonable to wonder whether the magnitude of the observed rebalancing premia and the ordered ranking of premia across the different risk parity methods is an artifact of luck. Should we expect, for example, maximum diversification type methods to dominate Hierarchical Risk Parity in general?

To address this query I conducted two related analyses: a bootstrap analysis of re-ordered historical returns; and a Monte Carlo analysis of random returns drawn from a multivariate normal distribution with the same means and covariances as the historical sample.

My analyses are complicated by the fact that different markets have different starting dates. I decided to use January 2000 as my cutoff date, as it represents a convenient trade-off between number of markets and length of sample. I have continuous daily data for 53 markets starting January 2000.

My bootstrap analysis followed this procedure:

1. Subset the returns matrix to contain all 53 markets with continuous history back to at least January 2000

2. Create a sample returns matrix by drawing rows at random from the returns matrix, with replacement

3. Solve for the optimal ex post portfolios based on five objectives

• Equal Weight

• Inverse Volatility

• Equal Risk Contribution

• Hierarchical Risk Parity

• Maximum Diversification

4. Scale the weights to target a 10% ex post annualized volatility

5. Measure the realized rebalancing premium for each optimization

6. Repeat 10,000 times

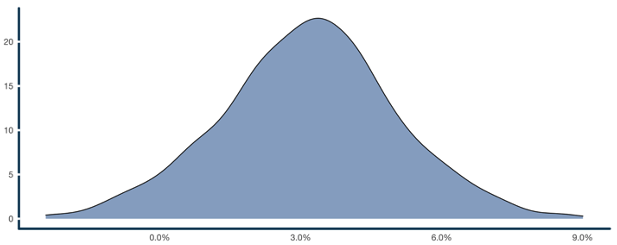

Figure 6 describes the distribution of rebalancing premia observed for all 10,000 samples sorted by optimization method.

Figure 6: Row-wise bootstrap distributions of rebalancing premia for different risk parity methods, 10,000 samples. SIMULATED RESULTS

Analysis by ReSolve Asset Management. Data from CSI. Past performance does not guarantee future results. SIMULATED RESULTS. Please see details of methodology and disclaimers in the reference paper.

Most of the risk parity methods have a very high probability of producing a large and positive rebalancing premium when targeting a 10% annualized volatility. The equal weight method produced a rebalancing premium greater than 1.2% per year, and the Maximum Diversification method produced a premium greater than 1.68% per year, in over 95% of samples, respectively. In contrast, the highly concentrated Hierarchical Risk Parity [HRP-VAR] portfolio produced a negative rebalancing premium about 49% of the time.

The expected value for the rebalancing premium of the Maximum Diversification risk parity portfolio is a very material 2.69%. The weighted average compound return of risk parity portfolio constituents is about 8% in the historical sample. As such, this magnitude of rebalancing premium represents a 33% boost to total compound portfolio returns, in excess of the returns generated from exposure to the underlying assets themselves.

My second test involves a Monte Carlo analysis of random returns drawn from a multivariate normal distribution with the same means and covariances as the historical sample. I followed this procedure:

1. Subset the returns matrix to contain all 53 markets with continuous history back to at least January 2000

2. Find the monthly mean returns and covariances for all 53 markets over the full sample period

3. Draw a random sample from the multivariate normal distribution with the same dimension as the original sample (i.e. 53 markets and 245 months)

4. Solve for the optimal ex post portfolios for the sample returns, based on five objectives

• Equal Weight

• Inverse Volatility

• Equal Risk Contribution

• Hierarchical Risk Parity

• Maximum Diversification

5. Scale the weights to target a 10% ex post annualized volatility

6. Measure the realized rebalancing premium for each optimization

7. Repeat 10,000 times

Figure 7: Multivariate Monte Carlo distributions of rebalancing premia for different risk parity methods, 10,000 samples. SIMULATED RESULTS

Analysis by ReSolve Asset Management. Data from CSI. Past performance does not guarantee future results. SIMULATED RESULTS. Please see details of methodology and disclaimers in the reference paper.

The results from the multivariate Monte Carlo model mirror the results from the bootstrap test above. Equally-weighted portfolios produced a rebalancing premium greater than 1.2% per year, and the maximum diversification method produced a premium greater than 1.68% per year, in over 95% of samples, respectively. Hierarchical Risk Parity [HRP-VAR] portfolios produced a negative rebalancing premium about 64% of the time.

Consistent with bootstrap results, the analysis indicates that the expected value for rebalancing premium of the maximum diversification risk parity portfolio is a very material 2.57%. The weighted average compound return of risk parity portfolio constituents is about 8% in the historical sample. As such, this magnitude of rebalancing premium represents a 32% boost to total compound portfolio returns, in excess of the returns generated from exposure to the underlying assets themselves.

Accounting for dynamic portfolio construction and leverage

The bootstrap and Monte Carlo analyses above provide useful estimates for the distribution of rebalancing premia available from appropriately diversified portfolios of our core asset universe assuming constant weights. However, they do not account for the interaction effects of dynamic portfolio rebalancing.

In practice many risk parity strategies constantly update the optimal portfolio weights, and target portfolio leverage, in response to changes in estimated covariances. It is not clear how this dynamic portfolio formation and scaling impacts the expected rebalancing premium.

To better understand these interactions, I performed the following test using the market returns and portfolio weights for the staggered monthly rebalanced HRSS MAX DIV risk parity method from 1985 to May 2020:

- Draw a random sample (with replacement) of blocks of rows of the daily returns/weights matrices. The sample length is equal to the number of rows in the returns/weights matrices

- Create new returns and weights matrices based on the sample row index

- Calculate the rebalancing premium for this sample

- Repeat 10,000 times

Figure 8: Distribution of empirical rebalancing premium from row-wise resampled weights and returns for monthly rebalanced HRSS MAX DIV portfolio. SIMULATED RESULTS

Analysis by ReSolve Asset Management. Data from CSI. Past performance does not guarantee future results. SIMULATED RESULTS. Please see details of methodology and disclaimers in the reference paper.

With reference to Figure 5, the realized annual rebalancing premium for the monthly rebalanced HRSS MAX DIV risk parity implementation was 3.3%. The average annual rebalancing premium realized across our 10,000 samples was 3.17%, which is very close to the realized value. In our bootstrap, the probability of a negative realized rebalancing premium was less than 5%.

My analysis reveals that the dynamic rebalancing and scaling activity in the dynamic risk parity portfolio may improve on the rebalancing premiums generated by fixed-weight methods, with an expected premium of 3.17% for the dynamic method versus 2.57 – 2.69% for the fixed-weight version.

Concluding thoughts

With balanced allocations to a wide variety of commodities as well as stock and bond indices from around the world, risk parity strategies are designed to thrive in any future economic regime.

I examined the distribution of rebalancing premiums for a simple risk parity implementation (a version of the Permanent Portfolio) consisting of US stocks, gold and bonds from 1982 through May 2020. I then proceeded to analyze historical and expected future rebalancing premia for a variety of global risk parity strategies composed of 64 futures markets from June 1985 through May 2020.

The rebalancing premium when applied to the three markets in the Permanent Portfolio was over 1% per year. The most diversified risk parity portfolios produced a rebalancing premium of more than 3% per year.

I analyzed the distribution of expected rebalancing premia for our futures universe using three different methods. Every model yielded a very high probability of realizing a positive rebalancing premium. The expected value of the premium was at least 2.5% per year, and over 3% per year for the dynamic approach.

As with most sources of excess return, what appears to be a “free lunch” often requires a different kind of sacrifice. The rebalancing premium is no different. The diversified risk parity portfolio explored in this article has many attractive properties, but it is expected to behave quite differently from traditional portfolios. This may lead to multi-year periods of underperformance relative to a domestic 60/40 portfolio. Investors must have the discipline and internal fortitude required to suffer the tracking error to common benchmark portfolios.

In a low return world, the ability to generate 2-3% per year in excess return with no expectation of higher volatility is very attractive. As of mid-2020 Vanguard forecasts that a global 60/40 portfolio may produce an expected annualized return between 3.5% and 5.5% (before costs) over the next ten years. If an optimal risk parity portfolio may produce 2.5% per year or more in rebalancing premium in excess of returns produced by the underlying investments, at approximately the same long- term volatility, this may represent an attractive alternative to global 60/40, with the added benefit of owning a diverse set of markets that benefit from a wider range of economic outcomes.

Adam Butler, CFA, CAIA, is co-founder and chief investment officer of ReSolve Asset Management. ReSolve manages funds and accounts in Canada, the United States, and internationally.

Disclaimer

Confidential and proprietary information. The contents hereof may not be reproduced or disseminated without the express written permission of ReSolve

Asset Management Inc. (“ReSolve”). These materials do not purport to be exhaustive and although the particulars contained herein were obtained from sources ReSolve believes are reliable, ReSolve does not guarantee their accuracy or completeness.

The material has been provided to you solely for information purposes and does not constitute an offer or solicitation of an offer or any advice or recommendation to purchase any securities or other financial instruments and may not be construed as such.

This information is not intended to, and does not relate specifically to any investment strategy or product that ReSolve offers. It is being provided merely to provide a framework to assist in the implementation of an investor’s own analysis and an investor’s own view on the topic discussed herein. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation.

ReSolve is registered as an Investment Fund Manager in Ontario, Quebec and Newfoundland and Labrador, and as a Portfolio Manager and Exempt Market Dealer in Ontario, Alberta, British Columbia and Newfoundland and Labrador. ReSolve is also registered as a Commodity Trading Manager in Ontario and Derivatives Portfolio Manager in Quebec. Additionally, ReSolve is a Registered Investment Adviser with the SEC. ReSolve is also registered with the Commodity Futures Trading Commission as a Commodity Trading Advisor and a Commodity Pool Operator. This registration is administered through the National Futures Association (“NFA”). Certain of ReSolve’s employees are registered with the NFA as Principals and/or Associated Persons of ReSolve if necessary or appropriate to perform their responsibilities. ReSolve has claimed an exemption under CFTC Rule 4.7 which exempts ReSolve from certain part 4 requirements with respect to offerings to qualified eligible persons in the U.S.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS

General information regarding hypothetical performance and simulated results.

It is expected that the simulated performance will periodically change as a function of both refinements to our simulation methodology and the underlying market data. Equity line results show the growth of $1 or $100 assuming the purchase and sales of securities were executed at their daily closing price. Profits are reinvested and the simulation does not reflect commissions or transaction costs of buying and selling securities, and no management fees were deducted. Any strategy carries with it a level of risk that is unavoidable. No investment process can guarantee or achieve consistent profitability all the time and will necessarily encounter periods of extended losses and drawdowns. These results are not specific to any investment strategy ReSolve actually trades and are simply proof of concept for illustrative purposes only.

The universe of markets used in risk parity simulations consists of the following futures. For computation of returns, futures were rolled monthly once both Open Interest and traded volume were larger on the back month than the front month.

1 This paper is not intended to be a comprehensive analytical treatment on stochastic portfolio theory and the mathematics of rebalancing. Readers who are interested in more comprehensive treatments and proofs are invited to read “Stochastic Portfolio Theory” by Fernholz, “The Ex-Ante Rebalancing Premium” by Hillion and “Demystifying Rebalanc- ing Premium: A Methodological Path to Risk Premia Engineering” by Dubikovsky and Susinno.

2 Importantly, all of the returns cited in this article are excess returns (i.e. net of borrowing costs) since the cost of leverage is built into futures returns.

3 There are 461 monthly returns from inception of the S&P 500 e-mini futures contract.

4 Specifically, we took the median result from 10,000 simulations for each combination of number of assets and average compound return.

5 This is an approximation, but it is quite accurate when applied to typical investment portfolios with modest means and variances

6 Or derive estimates from options or swaps markets.

7 The rebalancing premium is also impacted by whether markets were dominated by cross-market trending or mean-reverting behavior, and interactions between these behaviors and volatility scaling activity.

8 See Lozada, Gabriel A. (2015) “For Constant-Duration or Constant-Maturity Bond Portfolios, Initial Yield Forecasts Return Best near Twice Duration”. See also Leibowitz, Martin L., Anthony Bova, and Stanley Kogelman (2014), “Long-Term Bond Returns under Duration Targeting,” Financial Analysts Journal 70/1: 31—51

9 See Asness, Clifford S., Moskowitz, Tobias T., & Pedersen, Lasse H. (2013) “Value and Momentum Everywhere”

10 See Pedersen, Lasse H. (2012) “Time-Series Momentum”

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits