As leaders in manager research, we have unique insight into the implementation of big data in equity portfolios. Today, we share our key observations.

A look at how low interest rates have led to a surge of money losing companies, and what that may mean as interest rates move higher.

The car you drive isn’t just a status symbol. In the age of digital communication, Bluetooth and wired vehicles, advisors can use their cars to drive leads by converting boring downtime during a commute into active prospecting.

A couple of weeks ago I was called for jury duty. I learned a valuable lesson about the jury-selection process that explains why advisors often fail at networking events.

U.S. consumer prices rose more than expected in July, reinforcing our view that the Fed will continue its gradual pace of interest rate hikes, at least for now.

The number of publicly listed companies in the U.S. has fallen steadily since 1997. More companies have delisted, in fact, than gone public in every year of the past 20 years except one, 2013. Put another way, the pool is getting smaller even while the population and economy are expanding.

This year at "Camp Kotok," I quickly sensed a more upbeat mood. Not that many that were wildly bullish, but most were positive or at least neutral. There weren’t nearly as many bears as I expected. “Cautious optimism” seemed to be the theme. That led me to refine my own views with a wide variety of participants. Today, I’ll do the same for you.

To end the week, I have a couple of quick takes on some hot topics from the financial news. Let’s start with inflation.

Value investing is a proven long-term investing strategy that produces above-average results at below-average risk – if engaged in properly. However, there are four primary advantages to investing in undervalued dividend growth stocks that facilitate strong long-term performance while simultaneously lowering risk.

It’s one of those things you’re told never to do. But here’s an example when crying in front of a client led to a breakthrough I never would have made dry-eyed.

The Brexit clock is ticking as the United Kingdom’s departure from the European Union (EU) is set to take place in March 2019. But is the UK ready to leave? And is there still a chance it won’t?

In this issue, Research Affiliates discusses positioning in emerging markets and why investors should care about the distinction between real and nominal returns.

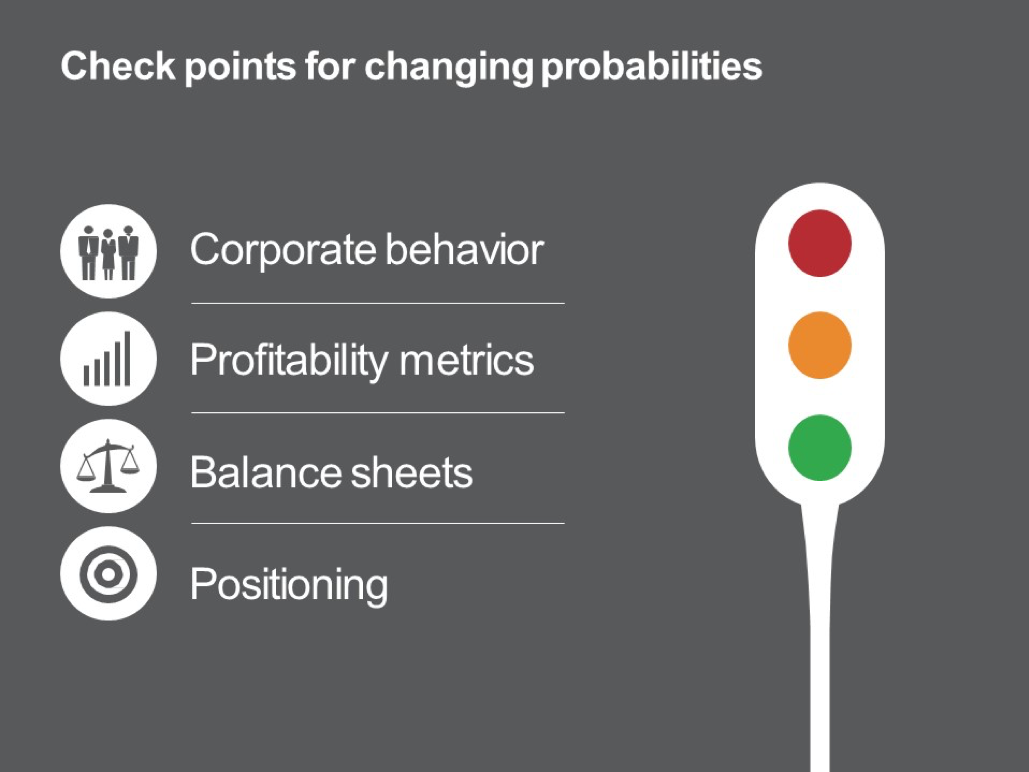

Senior Portfolio Manager David Vickers discusses the difficulties of predicting stock market crashes, while offering up four watchpoints that could help fuel the next one.

For advisors who work with people in transition, there is no more transitory place than an elevator. Here’s how I nabbed a prospect while scaling 20 floors – and some steps you can follow to meet prospects in an elevator.

Synchronized global growth was one of the main themes coming into 2018. In the second quarter GDP in the U.S. was the strongest since 2014, even as growth around the world downshifted. While global growth will be decent in the second half of this year, growth has already slowed in the U.K, Europe, China, and Japan.

We don’t know how long ago we met Frederick “Shad” Rowe, but we are glad we did, because our conversations with him have been net worth changing.

Something strange happened after last Friday's jobs report - the yield on the 10-year Treasury Note fell, finishing Friday at 2.95%, down four basis points from Thursday's close. To us, this makes no sense. If anything, it serves to reinforce our view that the bond market is making a big mistake.

The decade after the financial crisis has been marked by low inflation and investment spending, lagging income growth and a strong U.S. dollar. We expect these trends to reverse direction and potentially surprise investors who aren't prepared.

Adam S. Abelson is the chief investment officer for the Stralem Funds. Since its inception on January 18, 2000, as of May 31, 2018, the Stralem Equity Fund (STEFX) had an annualized return of 5.78%, versus 5.51 % for its benchmark, the S&P 500 total-return index, for an outperformance of 27 basis points.

This has been an unusually fruitful season for books for and about financial planners. Four absolute masters of the financial planning universe have published books that add to your chances of success as you grow your business and career.

This week I have something special for you: an update of “The Distribution of Pain,” one of 2017’s most popular letters. I say “popular” just in terms of feedback and reprint requests. It was thought-provoking but also sobering. I started with the original version, re-edited to clarify a few points, and added some new comments. It is still a timely, important topic.

Last month in Venezuela’s capital city of Caracas, a cup of coffee would have set you back 2 million bolivars. That’s up from only 2,300 bolivars 12 months ago, meaning the price of a cup of joe has jumped nearly 87,000 percent, according to Bloomberg’s Café Con Leche Index. And you thought Starbucks was expensive.

The Northern Trust economics team explores India, recaps revisions to U.S. economic measurements, and gauges potential future economic growth.

The macro data from the past month continues to mostly point to positive growth. On balance, the evidence suggests the imminent onset of a recession is unlikely. The largest risk to the economy is the escalation in trade war rhetoric.

Introduction Relative to historical norms the overall stock market as measured by the S&P 500 is overvalued with the current blended P/E ratio of 19.2. Historically, the S&P 500 would be considered fairly-valued when its P/E ratio was between 15 to 16.

As we begin August, let’s take a look back at the markets in July, plus what to expect in the month ahead.

A single line chart is keeping an awful lot of investors up at night: the US Treasury yield curve. It’s been flattening steadily since the end of 2016 and is nearly the flattest it’s been since 2007. We all remember what happened after that.

How are today’s fixed income managers integrating ESG factors into their investment practices? Learn what our latest ESG survey reveals.

The domestic economy is functioning as well as any period since 2007, however we expect economic growth to slow next year. Measured by GDP, we expect the economy grew by a solid 4.0% in the second quarter and is growing at a rate of 2.7% with most sectors performing well.

Just as investors have beliefs that limit their ability to grow their portfolio, advisors have beliefs that limit their ability to grow their practices. Those who overcome resistance get the most business. Here’s how the cycle of resistance works and what you can do about it.

Infrastructure is not a glamorous topic — it isn’t satirized on late-night TV, nor is it trending on social media. But the need for increased infrastructure investment is real across the globe. Given expected demographic trends, disruption by new technology and insufficient spending in the past, we at Invesco Real Estate believe infrastructure-related companies could be poised for decades of growth.

Turkish asset prices have plummeted this year, bringing their valuations to historically low levels. That presents potentially attractive opportunities to investors looking for quality stocks at bargain-basement prices. Yet some selloffs don’t necessarily end with stocks and bonds at oversold levels if their prices largely reflect current or near-term risks, both company specific and macroeconomic.

The price of bitcoin surged above $8,000 on Tuesday for the first time since May after the Group of 20 (G20) meeting in Argentina concluded last weekend with little urgency to take regulatory action on cryptocurrencies. In a communiqué, finance ministers and central bank governors expressed confidence that the technology underlying alt-coins “can deliver significant benefits to the financial system and the broader economy.”

Roboadvisors don’t cause fee compression; when used correctly by advisors, they are the solution.

Since we are necessarily in the predictions business, this letter offers our expectations for equity market returns. We admit our crystal ball is typically cloudy when it comes to what markets will do in the near term. While nothing is ever for certain, we can better view the potential for longer-term stock market returns from a couple of perspectives.

We see key factors beyond Brexit affecting the medium-term economic outlook for the U.K.

Market returns and economic growth have underlying drivers. At their core, extended periods of extraordinary growth and disappointing collapse reflect large moves in those drivers from one extreme to another. Extrapolation becomes a very bad idea once those extremes are reached.

Geopolitics dominates the news these days, over-shadowing what remains a fundamentally solid global economy. As always, Donald Trump is at the center of most of the “noise”...

Fears of an imminent U.S. recession are premature; tax policy and a more business-friendly regulatory environment provide long-term catalysts for the economy. Although conditions outside the U.S. are less encouraging, positive global growth should continue, albeit with growing divergence among countries.

As stated in our fourth quarter 2017 commentary, we believed the tax cuts would benefit small-cap stocks. This benefit has been the case for some names following recent results, but not all companies.

We believe detailed conversations with managers are crucial to developing informed opinions on investment strategies. Here’s how our manager meeting process typically unfolds.

We answer some of today’s most pressing investor questions—from the effect of trade wars with China to our expectations for rising rates and a correction in high yield.

We think the US economy remains in good shape, with the rate of growth potentially picking up, a labor market that is tight but attracting new workers, and inflation that still seems relatively subdued. Boosted by tax cuts and spending increases, these favorable conditions could continue for some time.

During the second quarter the equity market as measured by the S&P 500 Index had a total return of 3.4%, bringing the year-to-date total return to 2.6%. Second quarter performance reflects the continued low-inflationary expansion of the U.S. economy and the attendant growth in corporate profits. All else being equal, we would expect these trends to persist. The question, of course, is whether “all else is equal.”

Despite plenty of news, there was little market reaction. In a summer week including many vacations, we have a modest economic calendar but plenty of earnings news.

If you want to see who the real victims of tariffs are, go look in the mirror.

What we can learn about the current state of our economy by traveling and visiting with others outside of our home turf is amazing. For many of us in the investment business, our view of the economy is easily warped by statistical reports and interpretations prepared by professional economists.

US equities have gained every month since April, and are up over 3% so far in July. Our long term view remains that SPX will make a new all-time high in the months ahead. The short term is less clear.

Looking spiffy for work as an advisor doesn’t mean taking out a second mortgage on your home. Here are some high-end brand picks that I saw at my local Goodwill store.

There are a number of changes taking place in the investment environment and they are likely to have an influence on the returns on financial assets for some time to come. When the world’s leading economy, with more than a fifth of global GDP, does not participate in major alliances dealing with matters of security and the environment, this has longer-term investment implications.