The Pool of Tradable Stocks Is Shrinking. Here’s What Investors Can Do

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Elon Musk is no stranger to making controversial and outlandish comments, and his tweet earlier this week is no exception. As you probably know by now, the perennial entrepreneur announced to his more than 22 million Twitter followers that he is “considering taking Tesla private at $420.”

Despite the Herculean challenge—such a move would be the largest leveraged buyout in history—and despite Musk’s history of being a provocateur, Wall Street seemed to take his comment seriously. Tesla stock rose close to 11 percent on Tuesday to end at $379, a few bucks shy of its all-time high of $385, set in September 2017.

There are many reasons why investors should take note. For one, Musk and Tesla are now likely to face heightened scrutiny from securities regulators.

My reason for bringing it up is that, should Musk follow through and take the electric carmaker private, the already shrinking universe of investable U.S. stocks will lose yet another name.

This is a trend that cannot continue indefinitely.

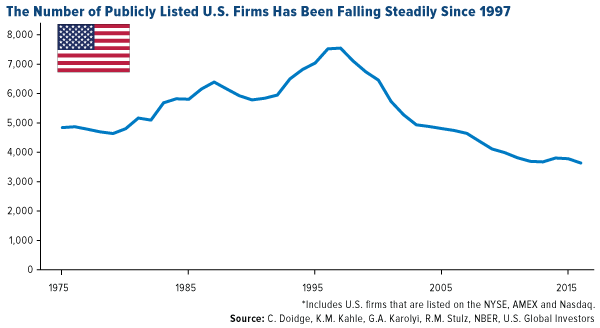

As I wrote in May 2017, the number of publicly listed companies in the U.S. has fallen steadily since 1997. More companies have delisted, in fact, than gone public in every year of the past 20 years except one, 2013.

Put another way, the pool is getting smaller even while the population and economy are expanding.

The U.S. Has 5,000 Fewer Listed Companies Than It Should

In 1976, there were about 23 listed companies per 1 million U.S. citizens. Today, it’s closer to 11 per million.

That’s according to a new National Bureau of Economic Research (NBER) report by respected financial economist René Stulz, who adds that the U.S. has roughly 5,000 fewer companies listed on exchanges than you would normally expect, given the country’s size, population, economic and financial development and respect for shareholder rights.

Are we seeing the same phenomenon in other countries, developed or otherwise?

“There are other countries that have lost listings since 1997, but few have experienced a greater percentage decrease in listings,” Stulz writes. “Further, the U.S. is in bad company in terms of the percentage decrease in listings—just ahead of Venezuela.”

Given that Venezuela’s economy is in freefall, with inflation forecast to hit 1 million percent this year, I would call it bad company indeed.

So why is this happening?

A Record $2.5 Trillion in M&A Activity

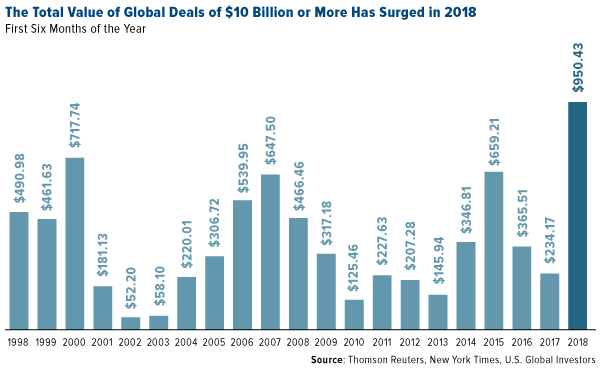

One of the main causes of fewer listings is the explosion in mergers and acquisitions (M&As). When one company acquires another, or when two companies merge, that lowers the number of tradeable stocks—assuming they were available to be traded to begin with. So far this year, worldwide M&A activity has been very robust, with a record $2.5 trillion in deals announced in the first six months alone. That puts 2018 on track to surpass $5 trillion, which would be the most ever recorded.

What also makes 2018 different from past years is the high number of mega-deals that exceed $10 billion. Together, these deals total $950 billion, more than in any past first-six-month period.

Among the biggest deals is AT&T’s takeover of Time Warner, valued at $85 billion. Coincidentally, that’s about $80 billion less than the deal that merged Time Warner and America Online (AOL) back in 2000, still the largest in history.

There’s nothing wrong with M&As, of course. The problem arises when there aren’t enough initial public offerings (IPOs) to replenish the pool and give investors early access to new firms.

At the most basic level, fewer stocks means fewer options. It becomes more difficult to build a diversified portfolio when you don’t have a diversity of stocks to choose from.

Consider how many companies Warren Buffett’s Berkshire Hathaway has acquired over the years. It owns recognizable brands like Duracell, Dairy Queen, GEICO, Fruit of the Loom and more, not to mention is the majority owner of a number of other companies. There’s even talk that Buffett might buy a domestic airline outright, possibly Southwest.

But at more than $311,000 a share right now, Berkshire’s A stock is out of most Main Street investors’ price range. How long until they’re priced out of participating in the entire market?

What’s more, profits are being divided among fewer winners. This is contributing to inflated valuations and market frothiness. In many ways, Apple can thank its $1 trillion market cap largely on the fact that there’s less competition now among equities—specifically tech equities. Uber, Airbnb, Pinterest, Coinbase, and many other huge tech unicorns have delayed or put off getting listed altogether.

Tougher Regulations Have Contributed to Private Equity Boom

So why would a company like Uber or Airbnb choose not to seek public funding? We can point to two related causes: stricter regulations on publicly traded firms, and the boom in private equity.

The most reported among these regulations is the Sarbanes-Oxley Act. More commonly known as SOX, the law was passed and signed in 2002 in response to major accounting scandals that brought down WorldCom and Enron.

In May 2017, I named SOX one of the five costliest financial regulations of the past 20 years. Its notorious Section 404, which requires external auditors to report on the adequacy of a firm’s internal controls, disproportionately hurts smaller companies, costing them six times as much in accounting fees in relation to larger firms, according to estimates by the Securities and Exchange Commission (SEC).

Because of these added costs, many smaller companies and startups are opting not to raise funds from public capital markets—or at least to delay it.

|

|

click to enlarge |

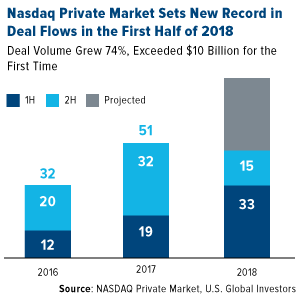

In the meantime, firms are finding it easier to get adequate private financing—which Main Street investors don’t have access to. According to Reuters, the global private equity industry raised $453 billion from investors in 2017, a new record. And this week, Nasdaq Private Market (NPM), which helps companies facilitate shareholder liquidity, announced it conducted a record 33 company sponsored liquidity programs in the first half of 2018. Deal volume grew 74 percent compared to the same period last year and exceeded $10 billion for the first time.

You can see now why some companies like Uber are staying private for longer. Some prefer not to have added costs associated with compliance. Others might not want to answer to a board or share financial details publicly.

These are among the things Elon Musk apparently wants to bring to an end by taking Tesla private. He’s become more combative with analysts and shareholders, especially short sellers, going so far as to tell listeners during a May conference call to “sell [Tesla] stock and don’t buy it” if they’re concerned about volatility.

Before SOX, the average age of a company at the time of its IPO was 3.1 years. Today, it’s more like 13.3 years, according to S&P Global Market Intelligence.

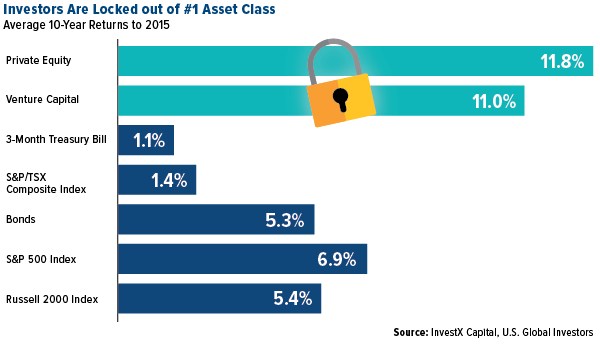

This hurts Main Street investors. Because they’re generally not able to invest in private equity, they lack access to companies when they might be expanding at their fastest pace.

Check out the chart below. In the 10-year period through 2015, private equity and venture capital averaged 11 percent or more annually. They far outperformed stocks and bonds, sometimes by more than double.

What Investors Can Do

Ideally, regulations would be streamlined to lower the costs of going public. I believe this would encourage more firms to get list earlier in their existence.

Outside of that, investors should take the long-term view and diversify in domestic and emerging market stocks, municipal bonds and gold.

As for domestic stocks, I think it’s important to focus on companies that are consistently raising their dividends on an annual basis and buying back their own stock. We’ve found that companies that are growing their revenue streams, quarter after quarter, and that show strong free cash flow generation have tended to outperform over the long run. Our funds favor these metrics.

I’ll have more to say about dividends and free cash flow next week, so stayed tuned!

Meanwhile, watch my video on the just-released inflation number, and its implications on gold!

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.59 percent. The S&P 500 Stock Index fell 0.25 percent, while the Nasdaq Composite climbed 0.35 percent. The Russell 2000 small capitalization index gained 0.80 percent this week.

- The Hang Seng Composite gained 2.76 percent this week; while Taiwan was down 0.26 percent and the KOSPI fell 0.21 percent.

- The 10-year Treasury bond yield fell 7.6 basis points to 2.874 percent.

Domestic Equity Market

Strengths

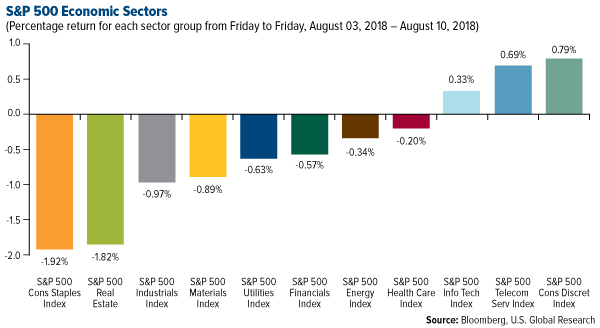

- Consumer discretionary was the best performing sector of the week, increasing by 0.79 percent versus an overall decrease of 0.25 percent for the S&P 500.

- Centurylink was the best performing stock for the week, increasing 13.54 percent.

- Data and analytics company Dun & Bradstreet Corp. says it will go private. It agreed to be acquired by an investor group led by CC Capital, Cannae Holdings, and funds affiliated with Thomas H. Lee Partners LP, along with a group of other investors.

Weaknesses

- Consumer staples was the worst performing sector for the week, decreasing by 1.92 percent versus an overall decrease of 0.25 percent for the S&P 500.

- Newell Brands was the worst performing stock for the week, falling 21.64 percent.

- Zillow fell 19 percent after revenue guidance missed expectations. The online real estate database said it saw third quarter revenue coming in between $337 million and $347 million. Analysts had estimated $408.4 million, according to Bloomberg.

Opportunities

- Apple is reportedly planning to open retail stores in India next year, in an effort to stop losing ground in the country. According to Bloomberg, Apple is also considering offering holiday-style discounts all year round.

- Samsung unveiled its Galaxy Note 9 and its answer to the Apple Watch and the HomePod. The company announced a slew of new products at an event in Brooklyn, New York on Thursday.

- The CEO of MoviePass said ‘very big media companies' offered to acquire the service, claiming that 'you would recognize them.' He also said the company would be profitable in six to nine months, and that its cash burn had been reduced by 60 percent.

Threats

- Bank of America asked 65 investors their biggest fear and the top response shows just how vulnerable markets are. A sharp loss of liquidity is now their biggest worry.

- Snap beat second quarter earnings estimates, but reported its first drop in daily active users. The stock initially gained as much as 13 percent in after-hours trading before giving back the gains. Investors are now concerned about future growth for the company.

- Disney earnings missed expectations. Second quarter profit was weaker than forecast due to higher programming costs and a drop in ESPN subscribers.

The Economy and Bond Market

Strengths

- U.S. consumer prices rose in July and the underlying trend continued to strengthen, pointing to a steady increase in inflation pressures that should keep the Federal Reserve on track to gradually raise interest rates. The Labor Department said on Friday its consumer price index (CPI) advanced 0.2 percent, the majority of which was due to a rise in the cost of shelter. In the 12 months through July, the CPI increased 2.9 percent. Excluding the volatile food and energy components, the core CPI rose 0.2 percent. The annual increase in the core CPI was 2.4 percent, the largest rise since September 2008.

- The number of Americans filing for unemployment benefits unexpectedly fell last week, suggesting that a strong economy was helping the labor market weather ongoing trade tensions between the United States and a host of other countries. Initial claims for state unemployment benefits slipped 6,000 to a seasonally adjusted 213,000 for the week ended August 4, said the Labor Department on Thursday. The claims data is being closely watched for signs of layoffs as a result of the Trump administration's protectionist trade policy, which has left the United States embroiled in tit-for-tat tariffs with major trade partners including China, Mexico, Canada and the European Union.

- U.S. consumer sentiment advanced to a 17-year high, elevated by rosier views of the economy and personal finances, the Bloomberg Consumer Comfort Index showed Thursday.

Weaknesses

- U.S. mortgage application activity decreased to its lowest in 2 and a half years last week as loan requests to refinance existing homes fell to their weakest level since December 2000, said the Mortgage Bankers Association on Wednesday.

- U.S. wholesale inventories were slightly higher in June than previously reported, with sales posting their biggest drop in five months. On Thursday, the Commerce Department said wholesale inventories edged up 0.1 percent instead of being unchanged as it reported last month.

- U.S. producer prices were unchanged in July for the first time in seven months as a modest increase in the cost of goods was offset by a drop in services. On Thursday, the Labor Department said that, in the 12 months through July, the Producer Price Index (PPI) advanced 3.3 percent. Economists polled by Reuters had forecast the PPI increasing 0.2 percent in July and rising 3.4 percent year-on-year.

Opportunities

- The Leading Index release next week is slated to show growth of 0.4 percent. That would keep it in line with continued strength in the economy going forward.

- Germany will report its second quarter gross domestic product figures next week. The German data should be given special attention from the markets in many respects. Germany is by far the biggest economy of the Eurozone and has been the engine of the economy so far. Additionally, as the “global export champion,” it is the best indicator of how the trade disputes, which have existed since spring, affect the economy.

- Next week’s University of Michigan Sentiment report is anticipated to hold near the highs it has seen for the last couple of months. That would be well received as a sign of resilience in the face of the trade disputes.

Threats

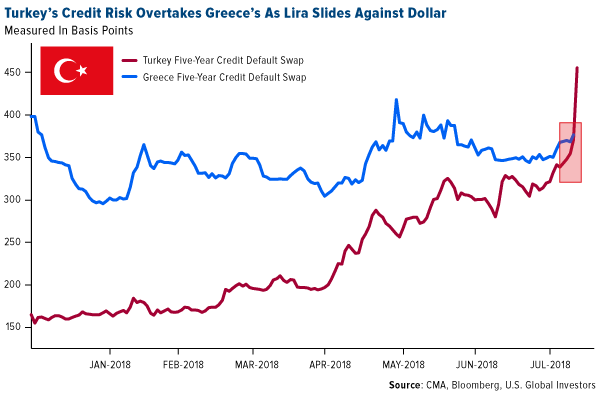

- The cost of insuring against a debt default in Turkey overtook that of Greece, which is rated four notches lower by Moody’s Investor Service. The lira has slumped against the dollar to record lows this week, fueled by concern about the nation’s worsening relationship with the U.S. and authorities’ ability to anchor the nation’s assets.

- The pace of retail sales growth has been moderating in the last months. Next week’s July release is forecast to keep that trend intact.

- Housing starts have fallen off a cliff as supply/demand imbalances, pricing pressures and mortgage rates have all coalesced in a negative feedback loop. Next week’s release forebodes a continuation of the same.

Gold Market

This week spot gold closed at $1,211.70, down $1.95 per ounce, or 0.16 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 2.45 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index was lower by 1.18 percent. The U.S. Trade-Weighted Dollar Index surged 1.22 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Aug-9 | Initial Jobless Claims | 220k | 213k | 219k |

| Aug-9 | PPI Final Demand YoY | 3.4% | 3.3% | 3.4% |

| Aug-10 | CPI YoY | 2.9% | 2.9% | 2.9% |

| Aug-13 | China Retail Sales YoY | 9.1% | -- | 9.0% |

| Aug-14 | Germany CPI YoY | 2.0% | -- | 2.0% |

| Aug-14 | Germany ZEW Survey Current Situation | 72.1 | -- | 72.4 |

| Aug-14 | Germany ZEW Survey Expectations | -20.7 | -- | -24.7 |

| Aug-16 | Initial Jobless Claims | 215k | -- | 213k |

| Aug-16 | Housing Starts | 1267k | -- | 1173k |

| Aug-17 | Eurozone CPI Core YoY | 1.1% | -- | 1.1% |

Strengths

- Spot gold was the best performing precious metal for the week. Gold is putting up a fight against the U.S. dollar, according to Ole Hansen, head of commodity strategy at Saxo Bank. The yellow metal is showing resistance near $1,200 an ounce, which suggests that prices are, for now, finding a floor, reports Bloomberg. Midweek gold rose for a second day from the lowest in more than 16 months. Investors are weighing the escalation of trade wars along with the U.S. stating it will impose 25 percent duties on an additional $16 billion in Chinese imports in two weeks (in addition to investors assessing U.S. sanctions on Russia).

- Indian gold imports are said to have increased in July, reports Bloomberg, after declining every month in the first half of 2018. Imports expanded 21 percent to 65.6 metric tons from a year earlier, as jewelers prepare for a “revival in demand during the festival season that starts in about three weeks.”

- The European Parliament has agreed to ease liquidity rules for banks trading gold, reports CNBC, marking a success for the London Bullion Market Association’s (LBMA) campaign to revise the plans. As part of regulations known as Basel III, the proposed rules should come into effect in the European Union around the year 2020. “The proposals treat physically traded gold like any other commodity, meaning banks would have to hold more cash as a proportion of their gold exposures as a buffer against adverse price moves,” the article reads. On another note, Russia’s Finance Ministry said in a statement that gold output in the first half of the year was little changed at 122.5 metric tons year-over-year, Bloomberg reports.

Weaknesses

- Silver was the worst performing precious metal for the week, with a loss of 0.56 percent as hedge funds boosted their bearish view to a 12-week high. As of Friday, exchange-traded funds (ETFs) cut 6,184 troy ounces of gold from their holdings, making this the seventh straight day of declines, according to Bloomberg. In addition, commodity-focused ETFs saw withdrawals over the last week, with those investing in precious metals leading the decline. Data compiled by Bloomberg shows that outflows from U.S.-listed commodity ETFs totaled $538 million in the week ended August 9. This compares to withdrawals of $280 million in the previous period. A silver lining to this news is seen in the VanEck Vectors Gold Miners fund, which added $102.2 million in the latest session. This increases the fund’s assets by 1.2 percent to $8.83 billion. “This was the 17th straight day of inflows, totaling $944.1 million,” Bloomberg writes.

- Pandora, the world’s biggest jewelry maker, plunged this week after cutting its profit and sales forecasts, Bloomberg reports. The company has seen pressure in key markets such as the U.S. and China. Shares fell more than 20 percent, the most in seven years. Just three months ago, investors saw the same slump when the company’s first-quarter report disappointed, the article continues.

- New Gold’s technical report for the Rainy River mine resulted in even lower valuation, writes Bloomberg. This raises the potential for further impairment charges, Eight Capital said. In addition to this news, New Gold’s stock got two downgrades.

Opportunities

- According to ICBC Standard Bank, gold’s plunge to the lowest level in more than a year is close to ending, and the price of the yellow metal has the potential to climb back to $1,300 by December. London-based commodities strategist Marcus Garvey said, “We are going to see almost certainly two U.S. interest rate hikes come this year, but they are already, if not fully priced, fairly nearly. So there isn’t a huge scope for a surprise here.” Another comment on gold’s next move comes from ANZ strategists Daniel Hynes and Soni Kumari. The two wrote in a report on August 7 that the possibility of a short-covering rally in the coming months is seen on expectations of U.S. dollar depreciation amid rising inflation, economic growth peaking and increasing geopolitical uncertainty. On a related note, London-based Bullion Vault reported that the number of those buying gold through the company has exceeded the number of sellers by more than four to one in July, making it the widest margin since 2008. Lastly, Northern Star Resources CEO Stuart Tonkin told Bloomberg TV that the gold price has bottomed as output peaks.

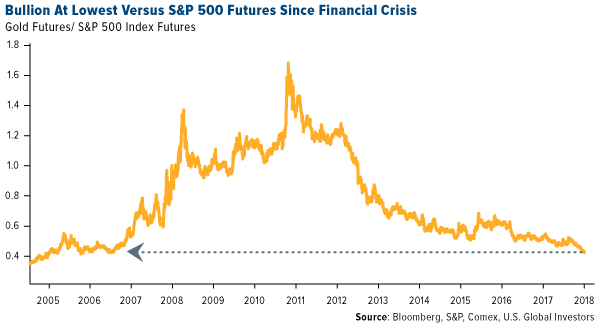

- A strong stock market has been causing gold some pain, reports Bloomberg, as the metal falls toward $1,200 an ounce, a level not seen since March of last year. As you can see in the chart below, this slump has put gold bullion near the lowest relative to the S&P 500 Index futures since the global financial crisis. “Investors are abandoning the non-interest-bearing commodity for riskier assets amid higher U.S. rates and a solid global economy,” the article continues. Mike McGlone, BI Commodity Strategist, adds that good support and extremely short net positions is a recipe for a sharp gold-price recovery.

- The U.S. midterm elections could play a big part in shaping the outlook for gold, reports Bloomberg. As Richard Hayes, CEO of Australia’s Perth Mint, points out, demand for coins and minted bars was a bit sluggish over the past year as President Donald Trump’s earlier win in the presidential poll prompted investors to divert funds into stocks, bonds and property. “If the Democrats do particularly well, that will spark a renewed sense of demand in the States for both gold and silver and that will then flow over into Europe and the rest of the world,” Hayes continued.

Threats

- According to one Bloomberg headline, gold may lose a third of its value by the end of next year. The yellow metal is moving inversely to U.S. two-year yields with a 30-day correlation of 0.87. This could mean losses ahead as short-term Treasury yields rise. As MLIV discussed previously, and as Bloomberg notes, those yields are poised to push higher based on the expected Fed funds rate peak, likely something close to 3.5 percent. Rates were this high back in 2007, and gold traded at $802 an ounce. Wes Goodman points out another headwind for gold: the fact that holders of bullion-backed ETFs are sitting on about 150 tons of loss-making metal. This is nearly 5 percent of annual global mine supply, so if all that metal comes back to the market, it could prove a big swing factor, Goodman reasons.

- A liquidity crunch is the new worry for credit investors. “It’s not trade wars or an equity market correction that look to be keeping credit investors up at night,” Bank of America strategists wrote in a note this week. “The concern is a more pervasive rush for the exit at some point in the future.” An otherwise healthy economic backdrop is being overshadowed by extreme moves that are haunting cross-asset investors, Bloomberg reports, with illiquidity fears rising across the board. “It’s especially a concern in high-yield credit, where investors holding cash bonds can face steep penalties if they rush for the exit,” the article reads.

- A trade war between the world’s two biggest economies continues to escalate as the U.S. said it will begin imposing 25 percent duties on an additional $16 billion in Chinese imports in just two weeks, reports Bloomberg. Items on the new list range from motorcycles to steam turbines to railway cars. Even though American companies have complained that such moves will raise business costs and eventually consumer costs, this will be the second time the U.S. places duties on Chinese goods in about the past month, the article continues.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended August 10 was Spectre.ai Utility Token, which gained 108.67 percent.

- A new survey done by technology giant IBM shows that 16 percent of health care executives are planning to incorporate blockchain technology into their facilities within the next year, reports ETF Trends. Having more efficient operations can help reduce the bottom line, the article explains, noting three specific ways the emerging technology can change health care operations: 1) medical records and data distribution, 2) payment system, and 3) clinical trial logging.

- California-based business and financial software company Intuit has been awarded a patent by the U.S. Patent and Trademark Office (USPTO) this week, for a system that processes bitcoin payments via text message, reports Coindesk.com. The company has long been looking into improving access to bitcoin payment processors, originally filing this patent back in 2014, which was shortly after the launch of its QuickBooks Bitcoin Payments service. This newly awarded patent details how “a system of virtual accounts could enable two users to transfer funds using mobile phones,” the article reads.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended August 10 was Niobium Coin, which lost 50.58 percent.

- According to a study by researchers at the University of Pennsylvania, the unregulated and murky nature of the initial coin offering (ICO) market could be a legitimate reason for concern, writes MarketWatch. One of the biggest findings of the study was that ICO code and disclosure often do not match. “Of the biggest ICOs in 2017, which raised a combined $2.6 billion of the $3.7 billion in total ICOs last year, only 20 percent had code that matched their promise 100 percent of the time,” the article reads.

- The price of bitcoin fell earlier in the week to under $6,500, reports Seeking Alpha. The move accelerated after the Securities and Exchange Commission pushed back on an eagerly-awaited VanEck exchange-traded fund backed by bitcoin. According to the article, a verdict is now expected by the end of September.

Opportunities

- Starbucks is the latest company to jump on the cryptocurrency bandwagon, reports CNBC. The coffee giant is teaming up with Microsoft, Intercontinental Exchange and a handful of others to create a new digital platform called Bakkt. A spokesperson for the coffee chain said that this platform aims to convert digital assets like bitcoin into U.S. dollars, which can be used at Starbucks.

- According to Bloomberg News, Goldman Sachs Group could “offer a boost for the burgeoning universe of funds betting on cryptocurrencies.” People with knowledge of the matter say the firm is considering a plan to offer custody for crypto funds. This means that Goldman would hold these securities on behalf of the funds, which would reduce the risk for clients wanting to guard against any threats of losing their investments to rogue attacks, the article continues.

- As Coindesk.com reports, 20 Thailand cryptocurrency exchanges have applied for new digital asset licenses just weeks after the nation’s new requirement was announced. The rules went into effect July 16 after a royal decree was made public in May, stating that all projects that intend to offer crypto exchange services must also gain approval from the SEC before trading starts. This is a positive sign as it appears many ICOs have expressed interest in becoming registered to conduct compliant token sales in the country, the article reads.

Threats

- Total transaction volume in bitcoin related with illegal uses has surged since 2013, according to Lilita Infante at the U.S. Drug Enforcement Administration. When Infante started seeing bitcoin pop up across her cases five years ago, her analysis showed criminal activity was behind about 90 percent of transactions, reports Bloomberg. However, there has been a positive shift in this trend, will illegal activity shrinking to about 10 percent and speculation becoming the dominant driver behind cryptos, the article continues.

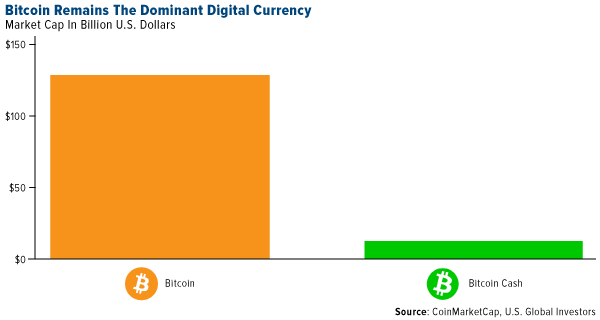

- Roger Ver, who used to be known as “Bitcoin Jesus” is now a supporter of bitcoin cash, saying that bitcoin is “no longer bitcoin.” The alternative, which claims to be faster and cheaper at transaction processing, is closer to Nakamoto’s (the name used by the unknown person who developed bitcoin) original vision, Ver said. As seen in the chart below, however, bitcoin cash still has a much lower market cap than bitcoin, despite endorsements by Ver. As Bloomberg reports this week, there seems to be a culture war brewing between bitcoin’s old and new money, and Ver’s opinion is just one example. Many going by pseudonyms, such as Cobra, are posting unpopular, anonymous rhetoric as a slump prolongs in the space.

- According to Bloomberg, cryptocurrency technical signals are flashing more pain ahead. Analysts are warning against pouncing on the dip, the article reads, and with bitcoin falling again on Thursday, it seems that traders are listening. The largest cryptocurrency is attracting bearish calls as it falls below its 50-day moving average.

Energy and Natural Resources Market

Strengths

- Natural gas was the best performing major commodity this week rising 3.12 percent. The commodity rallied after U.S. inventories grew less than expected, and warmer weather in Europe is set to continue for the next few weeks.

- The best performing sector this week was the S&P 1500 Fertilizers and Agricultural Chemicals Index. The index rose 60 basis points after trade war headlines suggest rising grain prices may support farmer economics and increase demand for fertilizer products.

- The best performing stock for the week was Daqo New Energy Corp. The producer of solar energy equipment rose 9.3 percent after reporting a second quarter beat and guiding for better-than-expected third quarter demand.

Weaknesses

- Lumber was the worst performing commodity this week. The commodity dropped 3.48 percent after China introduced retaliatory tariffs on certain paper and forest products, suggesting lower export volumes out of North America may pressure domestic margins.

- The worst performing sector this week was the Bloomberg Americas Auto Parts Index. The index dropped 4.41 percent after major index constituents downgraded their expectations for the second half of the year on tariff-related cost headwinds.

- The worst performing stock for the week Novolipetsk Steel PJSC. The Russian steel producer dropped 13.77 percent after Russia announced it is studying a proposal to levy higher taxes on mining companies to make up for lost revenue on lower export duties.

Opportunities

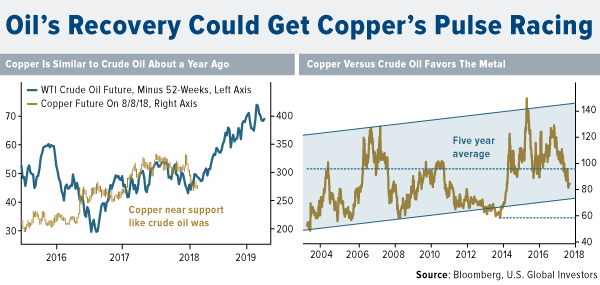

- Copper shows signs it may rebound just like crude oil did last year. About 20 percent below its peak, copper’s fate appears similar to last year’s nadir in crude oil, says Bloomberg. After being declared to be in a bear market last summer, crude oil rallied about 80 percent. In addition, copper is entering the lower end of its price range relative to oil, suggesting the metal may be in a better position to rally.

- Gold is showing resistance near 1,200 an ounce, suggesting prices have found a floor. While the strong dollar is hurting bullion’s appeal, geopolitical concerns have investors seeking safe havens. Investors have added more than $16 billion to money market funds and U.S. Treasury funds in the past month, and with yields not rising, investors may find an alternative in gold.

- Emerging market currencies look set for a rebound, according to Fibonacci analysis. A drop in the MSCI Emerging Markets Currency Index has found a level between the 50-61.8 percent retracement range that tends to signal a trend-correction is running out of steam. A rebound in emerging market currencies should be net positive for commodity demand and natural resource stocks.

Threats

- Worker walkouts are the most imminent threat to mining companies, beating trade-war-related concerns. In Australia, roughly 1,500 workers at alumina refineries are striking over pay and working conditions. That follows labor unrest in South Africa and South America. Miners, having warned against cost inflation, must now grapple with labor renegotiations that may result in slimmer margins and cash flow.

- The world’s supply of oil expanded in July on the back of surging Russian crude production, according to recent data by the International Energy Agency (IEA). Russian production climbed 150,000 barrels a day last month, a sharper-than-expected acceleration in output that may pressure global crude prices lower.

- Hurricane season may be more gentle than expected, lowering the chances for supply disruptions. The most recent Hurricane Season Outlook based on the NOAA’s Climate Prediction Center has increased the likelihood of a below-normal season to 60 percent. Products transiting through the Gulf of Mexico, mainly crude oil, may be less supported by traders as a result.

China Region

Strengths

- Hong Kong was the best performing country in the region this week, gaining 2.49 percent.

- All currencies in the region were down this week. Perceived safe-haven currencies, such as the U.S. dollar, were higher this week as emerging markets continued their slide amid ongoing turmoil in Turkey. There is no direct contagion risk from Turkey to Asia, however, the sentiment effect and a stronger dollar are weighing on Asian currencies. Relative to the other currencies in the region, the Taiwan dollar was the best performing currency this week down only 1 basis point.

- Information Technology was the best performing sector this week up 5.43 percent.

Weaknesses

- Thailand was the worst performing country in the region this week, losing 36 basis points.

- The South Korean won was the worst performing currency in the region this week down 55 basis points. China and U.S. trade frictions could adversely affect Taiwan’s economy as it drags on, encouraging investors to avoid risk assets.

- All HSCI sectors were up this week. Utilities was the lowest performing sector relative to the other sectors this week, up only 54 basis points.

Opportunities

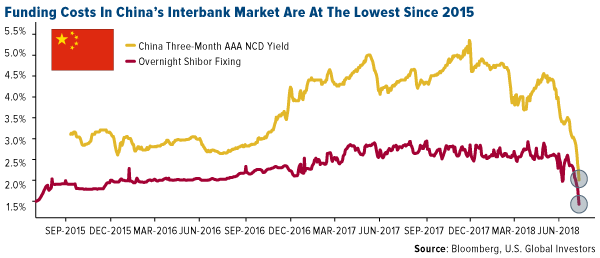

- Faced with a slowing economy and the risk of trade war fallout, the People’s Bank of China has turned on the liquidity taps. To borrow yuan overnight in the onshore market, the annualized charge is 1.40 percent, the lowest since 2015. For smaller banks needing to sell negotiable certificates of deposit, yields are at record lows. Currency forwards, interbank borrowing costs, government bonds and interest-rate swaps paint a similar picture. There are signs that local traders are seizing on the funding, with the volume of overnight repurchase agreements rising to a record in July. This could be a great window for foreign investors to take hedged positions in Chinese bonds, says JPMorgan Asset Management.

- According to EvercoreISI research, Hong Kong consumer fundamentals are positive, employment is at a record high and the unemployment rate at 2.8 percent is very low. Consumer confidence has increased, but remains in the middle of historical range. Consumer spending surged back in 2017 and is likely to increase about 6 percent year-over-year in the fourth quarter of this year and 4 percent in in the fourth quarter of 2019. Spending by visitors to Hong Kong is providing particularly strong support to retail sales and spending by local residents remains buoyant as well.

- Jeremy Schwartz, Wisdom Tree’s director of research, expects to see strong growth in China’s consumer tech sector in the next five to ten years as the country pivots to a more consumer-focused economy. China is pouring resources into its tech sector. The government wants 5G network speeds deployed on a large commercial scale by 2020 and all the major carriers have promised to meet that goal. Now may be the best time to invest in strong technology companies whose stock prices have been driven down by an escalating trade war that shows no sign of slowing.

Threats

- The United States Trade Representative announced late Tuesday afternoon that 25 percent tariffs on an additional $16 billion in Chinese imports will be finalized and go into effect on August 23. China is expected to retaliate with additional tariffs. These tariffs are part two of the initial 25 percent levy on $50 billion worth of goods announced in June. The first set of tariffs on $34 billion in goods went into effect in early July.

- China’s exports grew faster than expected last month, while imports surged, showing both domestic and international demand continue to shrug off the uncertainty of the trade conflict with the U.S. Exports rose 12.2 percent in July in dollar terms from a year earlier, faster than the forecasted 10 percent, said the customs administration on Wednesday. Imports climbed 27.3 percent, leaving a trade surplus of $28 billion. As the world’s largest exporter, China is still benefiting from robust global demand, but increasing tensions and rising trade barriers with the U.S. are weighing on the outlook. Although most of the threatened tariffs still haven’t gone into effect, China and the U.S. remain locked in an escalating tit-for-tat exchange of threats, signaling worse is to come.

- Hong Kong property prices are at new all-time high. The prices of lived-in homes in Hong Kong – the world’s most expensive property market – gained for a 25th straight month in April. IMF analysis suggests that property prices were overvalued at 25 to 35 percent as of the third quarter last year. Government authorities are working to restrain prices, but so far without much success, posing a risk of a housing bubble.

Emerging Europe

Strengths

- Romania was the best performing country this week, gaining 88 basis points. Romania’s central bank surprised economists this week by leaving borrowing costs unchanged and lowering its inflation outlook for this year and next.

- All emerging market currencies were down this week amid uncertainty over U.S. sanctions on Russia and Turkey. The Czech koruna was down the least relative to the other currencies in the region, down 1.52 percent against the dollar.

- Information Technology was the best performing sector among eastern European markets this week.

Weaknesses

- The Czech Republic was the worst performing country this week, losing 1.72 percent.

- The Turkish lira was the worst performing currency this week, losing 19.5 percent against the dollar. The lira was down as much as 11 percent on Friday amid tensions with the U.S. The turmoil threatens to scare away the foreign capital that Turkey depends on to finance its large external deficit and hampers companies’ ability to repay foreign currency loans.

- Industrials was the worst performing sector among eastern European markets this week.

Opportunities

- Hungary's preliminary unadjusted industrial output grew by an annual 4.2 percent in June, somewhat overshooting a 3.95 percent forecast. The updated release comes after a 0.4 percent expansion in May, according to the Central Statistics Office (KSH).

- Eurozone confidence among investors rose to 14.7 in August from 12.1 in July. The agreement by the U.S. and the European Union to pull back from the brink of a trade war has allayed some concerns, as the gauge of euro-area investor confidence published on Monday rose for second month, with researchers noting “signs of relief.”

- Russia’s shield against sanctions has drawn praise from Moody’s. Measures to cut down holdings of Treasuries and reduce exposure to the dollar have made Russia’s economy less vulnerable to the threat of deeper penalties, Moody’s analyst Kristin Lindow explains. According to Lindow, the country could even weather the unlikely scenario of sanctions on sovereign debt recently proposed by U.S. lawmakers.

Threats

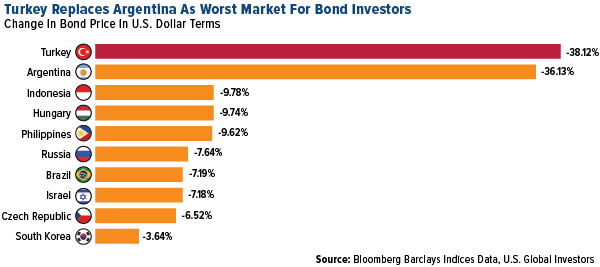

- Turkey-U.S. tensions ratcheted higher after President Erdogan froze the assets of two American officials. The move was in retaliation for U.S. sanctions over the continued imprisonment of Pastor Andrew Brunson. President Donald Trump doubled tariffs on Turkish steel and aluminum imports, escalating a diplomatic row that tipped the nation’s economy deeper into crisis. Following the lira’s plunge to a record, Bloomberg reports that Turkey is now the year’s worst performer in local-currency bonds and the carry trade, replacing Argentina. “Losses for both nations far exceed the 4.7 percent average decline in emerging market local-currency debt in 2018,” the article continues. In dollar terms, investors holding lira-denominated bonds have lost 38 percent. Argentina’s losses stabilized at 36 percent, according to Bloomberg Barclay’s indices.

- For the fourth month in a row, international investors have been reducing infusions in Russian assets, siphoning off about $2 billion from Russian shares. By early August, the money outflow considerably weakened. However, U.S. senators’ initiatives to impose new anti-Russian sanctions could slow down the return of foreign investors to the Russian market. The ruble hit a two-year low after the U.S. announced new sanctions on Russia over a nerve-agent attack in the U.K.

- German manufacturers took a hit in June as a slide in overseas demand knocked factory orders amid escalating trade tensions. The Economy Ministry’s report shows overseas orders fell 4.7 percent in June, with demand from non-eurozone nations slumping 5.9 percent. The Economy Ministry acknowledged that “uncertainty from trade policy played a role” as demand from non-eurozone countries led the slide.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All