Economic Outlook

The domestic economy is functioning as well as any period since 2007, however we expect economic growth to slow next year. Measured by GDP, we expect the economy grew by a solid 4.0% in the second quarter and is growing at a rate of 2.7% with most sectors performing well. There are significant issues that are helping to spur continued economic growth including the follow through effects of recent tax cuts on consumption, the impact of repatriated cash on business investment, and the improved labor market.

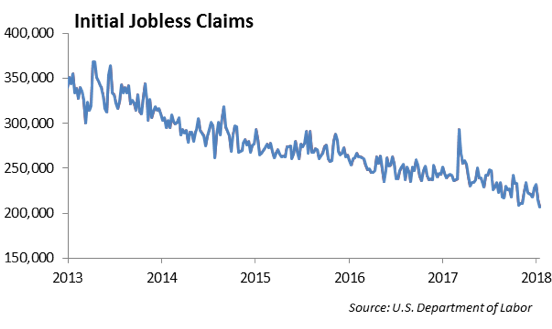

One of the pillars to sustained economic growth is a strong labor market, and we are in the midst of a very healthy jobs market with the U.S. economy producing over 200 thousand jobs per month. Jobless claims measured by the Labor Department are at their lowest level since 1969 and we have seen a slight improvement in the labor force participation rate as more workers come back to the labor force. However, we have not seen a meaningful increase in productivity. Increases in productivity lead wage inflation which is one of the reasons we have yet to experience a meaningful increase in wage rates.

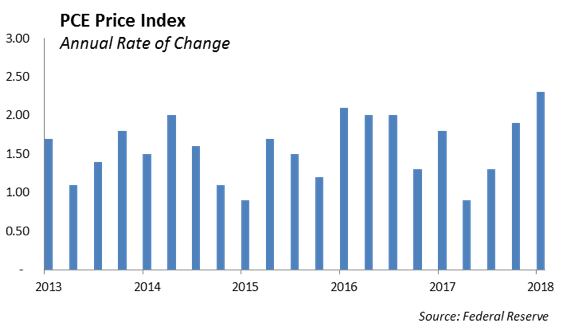

The rate of inflation is trending closer to the Fed’s 2% target. The price index for the personal consumption expenditures increased at a 2.7% pace in the first quarter. We expect to see some noise in the inflation data over the next quarter as trade tariffs impact prices.

The current economic expansion, which began in 2009, is now the second longest expansion on record. It appears we are in the sweet spot for the U.S. economy; however, cross winds are beginning to mitigate future growth prospects. The coordinated global economic recovery is weakening as Europe, Japan and China economic growth slows. Trade tariffs, acting much like taxes, will dampen domestic growth, disrupt supply chains and pressure prices of goods higher. As a result, we expect companies will make capital decisions that support the stability of their supply chains. Recently, Tesla announced that they will build a factory in China rather than deal with U.S. tariffs on exports. Similarly, Harley Davidson announced it will move production to Europe rather than deal with tariffs.

The Consumer sector

Consumer confidence remains high, which should bode well for continued near term economic growth. Consumer spending, measured by the Commerce Department, accelerated in the second quarter as retail sales increased 1.3% and 0.5% in May and June respectively. At the same time, the personal savings rate declined modestly from 3.8% to 3.2% in May and consumer credit spiked to $24.6 billion. Domestic consumption is increasing as consumer debt increases and the balance sheet deteriorates. Further increases in consumer debt will be a drag on future economic growth. In addition, consumer confidence slipped in June after rising in May. Rising gas prices, increasing inflation and confusion over the impact on tariffs may be hurting consumer’s expectations for near term economic growth.

The Corporate Sector

We expect corporate earnings will be strong this quarter; however, rising commodity prices, increased labor costs and tariffs will begin to erode profit margins. Uncertainty caused by the political environment and tariffs will have a negative impact on business investment. It appears that companies are buying back their own stock rather than make capital investments in their business for the long term. In the long run, this will hurt the competitive positions for many companies.

While some of the acceleration in economic growth can be attributed to the recent cut in corporate tax rates, there is an increased risk that the next economic downturn is more severe as a result of less tax revenue to support fiscal spending requirements.

Monetary Policy

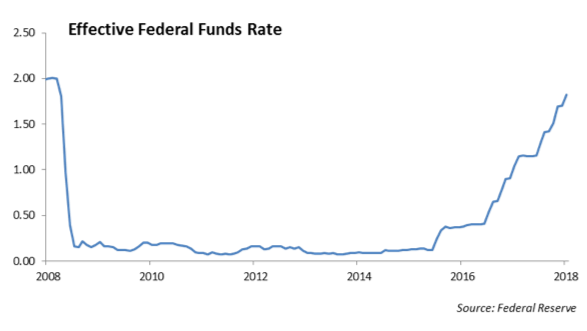

Since the Financial Crisis, the domestic economy has benefitted from historic low interest rates and aggressively stimulative monetary policies. We have moved to a period now where the Federal Reserve is becoming less accommodative and beginning to unwind its bond portfolio. It is important to remember this is a huge experiment in monetary policy and the impact on the global economy is at best unknown. The Fed believes the economy is now healthy enough to allow it to increase the Fed Funds rate as quickly as possible so that it can adjust rates lower during the next economic downturn in the hope of stimulating growth.

Over the past year, the Federal Reserve has pushed short term interest rates higher by 75 bps with the current Fed Funds target now at 2.0%. Given the strength in the domestic economy and the employment market, we expect the Fed will continue to push rates higher even if it means inverting the yield curve.

We believe that an inverted yield curve is the single best predictor of slowing economic activity within the next two years. The U.S. bond market is foreshadowing a high probability of an economic slowdown in 2019.

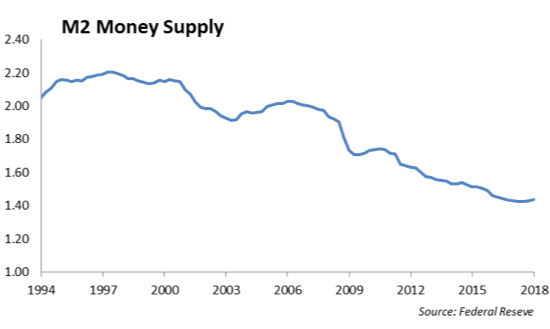

At the same time, year over year growth rates of money supply (measured by M2) have also been slowing. This is consistent with the Federal Reserve’s initiative to tighten monetary conditions. The velocity of money has been in a long term decline.

Since the Financial Crisis, an acceleration in the level of debt is fueling global economic growth. However, the efficiency of debt to produce increasing rates of growth has dwindled. The higher levels of debt are producing smaller increases in GDP. This is consistent with the decline in the velocity of money.

Global growth should produce revenue in excess of the recent tax reductions. However, when economic growth ultimately declines, the tax revenue will also decline. This leads to higher budget deficits and further increases in the level of debt. The resulting increased interest expense from the higher level of debt will be a burden on the economy as risks to inflation decline.

“The Great Unwind” of the Federal Reserve’s stimulus program will continue for the second half of the year. However, when the economy starts to show signs of deceleration or we experience a sharp market dislocation, we expect the Fed will slow down the unwinding of its bond portfolio. Adjusting the Fed Funds rate is the primary tool that the Fed uses to calibrate monetary policy; however, its quantitative easing program is the more powerful tool given its impact on interest rates across the yield curve. While it will likely prove unpopular, we would not be surprised to see the Fed increasing the size of its bond portfolio again if the next economic slowdown is too severe.

Europe

Economic growth in Europe is slowing as it faces significant challenges which will impact its economy over the near term. These challenges include: a growing populist movement, Brexit, slowing economic growth, a pullback in monetary stimulus and increasing trade barriers.

After accelerating in 2017, economic growth in the Eurozone has slowed this year and is estimated to be growing at 1.6%. The European Central Bank (ECB) announced their plan to begin to wind down its massive €2.4 trillion bond buying program this year which was designed to stimulate economic growth after its Financial Crisis. The ECB is currently purchasing €30 billion a month of government and corporate bonds, which is down from €60 billion per month in prior years.

The European Union (EU) is quickly nearing the deadline for Brexit talks with the U.K. in order to administer a smooth exit. However, Brexit talks appear to be in gridlock. The EU as a governing body has always shown difficulty making decisions for the collective good of its members. As a result, we expect they will push the decision out to the future and “kick the can down the road.” Brexit has the potential to be a major source of volatility in the capital markets heading into the fourth quarter.

Investment Strategy

Equities

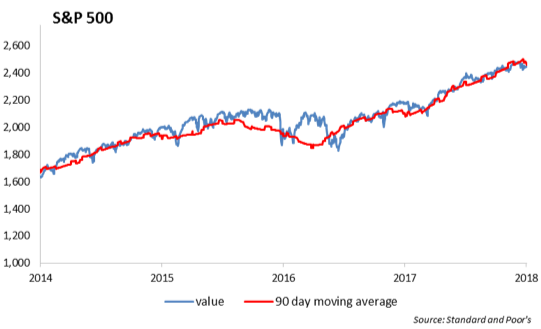

We expect earnings on S&P 500 to increase substantially this year with profits of $158 per share. At its peak, the S&P500 traded near 19 times 2018 estimated earnings. Today, price to expected earnings is closer to 16.9 times which is still above the long term average of 15.

While we believe that the large cap equity market is fairly valued, small cap and mid cap offers excellent risk/reward. As bank lending accelerates, we expect small cap in particular to benefit from access to credit. In addition, we believe company shares in the technology, energy and consumer discretionary offer opportunities for investors in this market. Share repurchases have been occurring this year at record levels. Our analysis of companies in the S&P 500 that have repurchased shares over the past year shows that only 20% had prices higher than their average share repurchase price. In other words, 80% of companies in the S&P 500 are trading at prices below their average share repurchase price.

While share repurchases have been a tailwind for earnings in a rising stock market, it is not the best use of corporate cash when the company’s stock declines.

Fixed Income

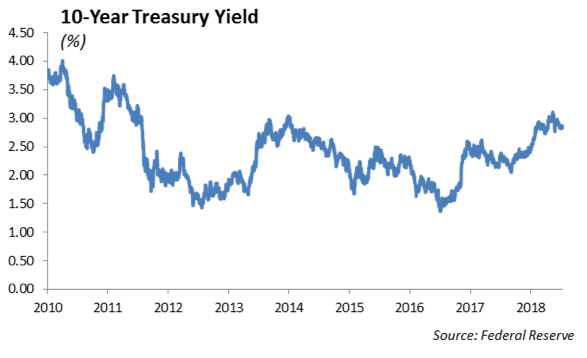

A cocktail of issues including geo-political concerns, uncertainty around trade tariffs, and the potential for slower economic growth have helped to keep interest rates low. The yield on the ten year U.S. Treasury has traded in a tight range between 3.0% and 2.75% for most of this year. While there is potential for interest rates to move higher if economic growth accelerates and inflation picks up, we do not expect a significant increase in long term rates. As a result, the Fed’s push to increase short term interest rates higher will ultimately invert the yield curve in the early part of next year.

Credit spreads on investment grade corporate bonds have widened throughout 2018 despite a decrease in supply. However, spreads on high yield bonds continue to tighten with default rates remaining low.

We particularly like the bank sector given their strong balance sheets and capital position. In addition, bonds in the pipeline sector offer excellent relative value given their cleaner capital structures, general reductions in leverage and the rising price in oil.

Real Estate

As interest rates adjusted higher through the second quarter, we did not see a correlated increase in cap rates in the real estate market. There appear to be growing risks in real estate as competition increases from insurance companies, government sponsored entities including Fannie Mae and Freddie Mac, and other non-bank financial institutions. Lending to commercial real estate by the larger banks has declined as the banks pull back on the risk. It appears that the banks are pulling back on their office, shopping malls, retail, and senior living loans.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2018 Winthrop Capital Management

Read more commentaries by Winthrop Capital Management