“It is difficult to make predictions, especially about the future.” - Danish Proverb

Since we are necessarily in the predictions business, this letter offers our expectations for equity market returns. We admit our crystal ball is typically cloudy when it comes to what markets will do in the near term. While nothing is ever for certain, we can better view the potential for longer-term stock market returns from a couple of perspectives. We attempt to form an idea about future long-term returns first by using cyclically adjusted earnings and then by using a framework articulated by Warren Buffett years ago.

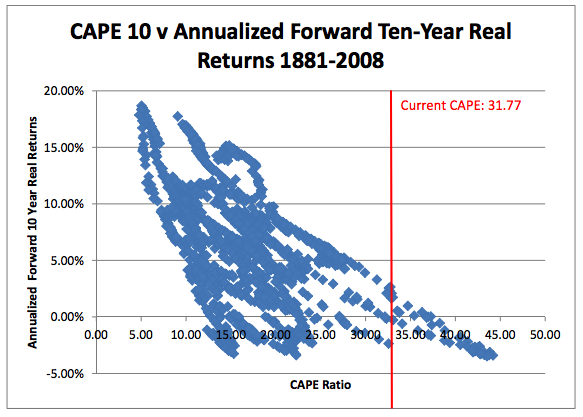

The cyclically adjusted price-to-earnings ratio (CAPE ratio) is the best predictor we know of when it comes to long-term equity returns1 . Forget for a moment how it is calculated and just know that it is basically a measure of market expensiveness. This measure is often misunderstood and misused. It does not identify market tops or bottoms or tell us what will happen tomorrow or next year – it has no bearing on these topics. The CAPE ratio has really just one useful application: giving a sense of the next ten years’ stock market returns. This is accomplished by going back in time, seeing what the CAPE ratio was at that time, and seeing also what the stock market actually returned for the next ten years (including dividends and adjusting for inflation). When these two measurements (the historical CAPE and subsequent ten-year returns) are plotted on a scatter plot, the relationship becomes obvious: the higher the CAPE the lower the returns2.

When the CAPE ratio has been similar to today’s 31.8 (as it was in 1929, 1997 and 20013 ), the S&P 500 Index delivered ten-year annualized returns, after inflation, ranging from +3.3% at best to -2.4% at worst, with an average of 0.8%. Yikes. Add 2% to 3% inflation to the “real returns” quoted above to get before-inflation “nominal returns” and you are supposed to have a good idea what the stock market may deliver annually over the coming decade. There is no prediction involved here; this is simply what has happened in the past when the market was similarly expensive according to the standard CAPE measure. And yet, we think there are some reasons that using this measure might not be ideal, and the future might not be so bleak.

So what is the CAPE measurement? It’s simply the ratio between the price of the market today, and the average earnings of the market for the past ten years4. This is the same as the standard P/E ratio (price divided by earnings) except that the CAPE uses ten years of earnings for the denominator while the standard P/E only uses one year’s worth. Why do we care about earnings generated five or ten years ago? Directly, we don’t. What we do care about is future earnings, but the idea here is that the past can tell us something about the future. If we are looking at the past to tell us about the future, the creators of the CAPE5 recognized that looking at shorter periods (say the last one or three years) can be misleading because corporate earnings fluctuate quite a bit. In a given year, earnings might be higher or lower than “normal”. The idea is to look back at enough years of history which should contain different parts of the earnings cycle to “smooth” earnings and help us gain a representative idea of what the future should be like, not just for a year or two, but all through the business cycle. This way, high CAPE ratios should arise from high stock prices, and not from temporarily low earnings.

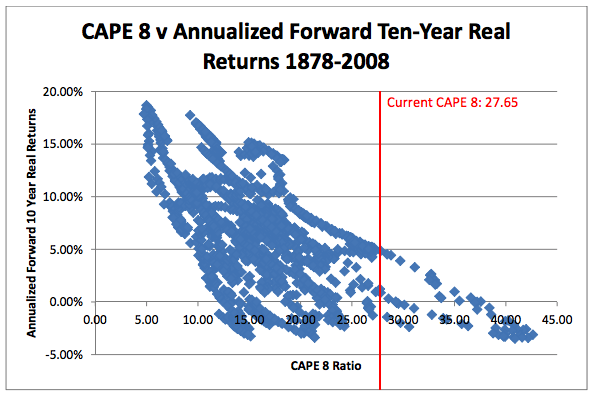

But what if the past isn’t representative of the future? Doesn’t that defeat the purpose of the CAPE? This has been a common criticism of the CAPE since the Great Recession. Since then, every ten-year lookback has contained a few far-from-ordinary earnings-starved years. The argument goes, and we agree, that this isn’t a good representation of the future because those years were exceptionally lean. Not only are we not likely to have another recession as bad as the “Great” one any time soon, but because of certain quirks of accounting (write downs and impairments), the “accounting earnings” during that time significantly understate the actual cash performance of businesses6. What if we excluded the worst of the recessionary years? Would that meaningfully change the forward outlook? We could create a CAPE 7 which would only look back seven years to 2011, or even a CAPE 6 to only look back to 20127. However, it feels intellectually dishonest to only use the past six or seven years’ earnings, completely excluding the recessionary years. The original CAPE was intended to include the impact of all parts of the business cycle, including recessions, and here we’re explicitly cutting one out (albeit because it was rather extreme). Using an eight year look-back (i.e. a CAPE 8) in order to include some of the depressed earnings years of 2010 and 2011, but not the most distortive outlier year of 2009 seems like a more reasonable compromise, one more likely to be representative of the typical business cycle going forward. Indeed, the CAPE 8 is 27.7, significantly lower than the standard CAPE (10) at 31.8. Markets with valuations near the current CAPE 8 have historically witnessed subsequent annualized real returns ranging from 5.24% to -1.43%, with an average of 3.01%.

Returning to the idea that we’re looking at the past to tell us about the future, are there other ways in which the past is misleading? What if we knew there was some factor that would make all earnings going forward higher than they were in the past? Wouldn’t then looking at the previous earnings history give us an understated view of the future? It’s no good extrapolating the past if we know the future will be meaningfully different. We are talking here about the recent corporate tax rate cut from 35% to 21%. Assuming the current corporate tax rates remain in effect8, we know earnings will be higher than they otherwise would have been. Should we not adjust for this? Let’s look back at eight years of earnings in order to include a more representative business cycle and adjust them to look like they had been taxed at the new corporate rate to get a better representation of the likely earnings future.

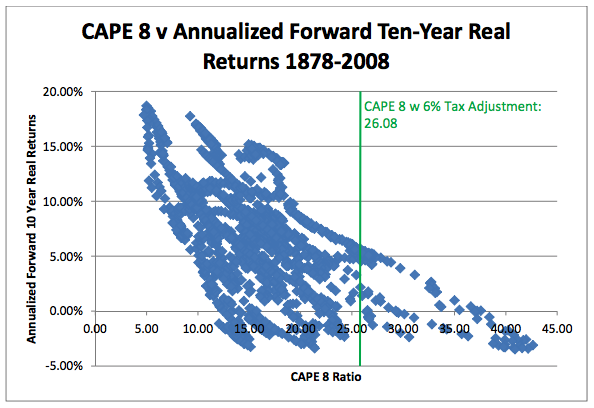

With the corporate tax rate going from 35% to 21%, for one dollar of pretax earnings, one might expect post-tax earnings to increase from $0.65 to $0.79, a 22% increase. However, the tax reality is not so simple, or advantageous. The new lower corporate tax rate has actually been observed to be increasing profits by only 10% to 12%. With a 12% bump to previous profits, the CAPE 8 falls from 27.7 to 24.7, a much more reasonable and promising reading. However, as we have written in previous letters, the tax cut windfall won’t in fact necessarily fall to the bottom line and stay there. Faced with initially fatter profit margins, companies will both have increased capital with which to compete with one another, and an increased incentive to do so. Many companies will compete by lowering prices, bringing margins partially back down and passing some of the gift of the tax cut along to consumers. How much of the tax windfall will corporations give back? We don’t know, but assuming about half seems reasonable. Thus, in our best effort to update the backwards looking CAPE 8 with a bit of foresight about future earnings, we will augment the previous eight years of earnings by 6%. This brings our final CAPE 8, half tax cut adjusted, back up to 26.1, with annualized forward ten-year returns at this level, after inflation, ranging from 6.07% to -1.26%, with an average of 4.23%9. It should be noted that although the lowest annualized ten-year real return among these observations was -1.26%, the true “worst case scenario” is probably something closer to the -3.3% *gulp* which has been experienced at both higher and lower CAPE values, as can be seen from the scatter plot on the next page.

So while the market does indeed look quite expensive on the standard CAPE 10 measure, which is usually a good measure, the situation is less alarming when two adjustments are made to account for the impact of the tax bill going forward and to exclude the worst of the Great Recession years. This suggests prospective real annual returns of about 4%, meaning the coming decade will likely see stock market annual returns lower than the long-term average of about 7%, but perhaps not so low as might initially be imagined.

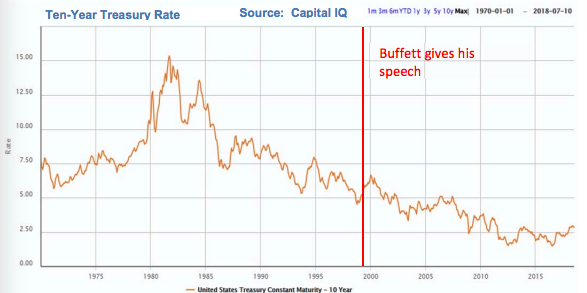

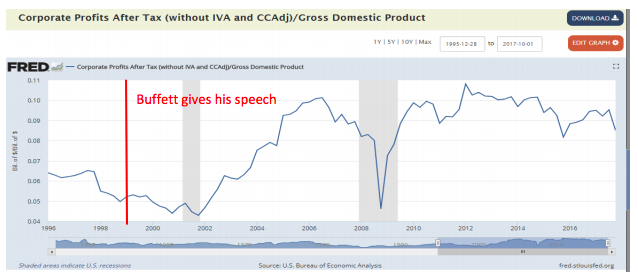

There are of course other ways to estimate forward returns. While the CAPE approach relies only on recorded past experience, a much more forecast-heavy approach was once laid out by Warren Buffett. His approach used three variables: GDP growth, interest rates and corporate profits as a percent of GDP. His forecast was offered in a 1999 speech, on the eve of the dot com bust, as a warning not to expect big gains in the stock market. Quite prescient, right? After all, the market proceeded to get chopped in half, declining for the next three years in a row, which hadn’t happened since the 1930s. Buffett, however, was discussing his forecasts for the next 17 years. Since it has now been about 17 years since his speech, perhaps it is a good time to evaluate his projections. Buffett’s main message in 1999 was that the annualized stock market returns of 13% seen over the prior 17 years, and widely expected to continue, weren’t likely to be realized. To see such heady results, two unlikely things would have to happen, he said. First, the long decline in interest rates since the early 1980s would have to continue for another 17 years in order to keep the good times rolling. A nearly 40-year decline in interest rates made this requirement seemingly improbable. Buffett explicitly said if interest rates fell from the 6% level of the time to 3%, the stock market should double accordingly. But as we now know, that’s exactly what happened!

Second, in Buffet’s improbable requirements for heady returns, corporate profits as a percentage of GDP, which were near the top of their observed range, would need to keep expanding even further. Here Buffett was more explicit about the likelihood of this transpiring, labeling profit margins the “most mean-reverting series in capitalism” and saying, “In my opinion, you have to be wildly optimistic to believe that corporate profits as a percentage of GDP can, for any sustained period, hold much above 6%.” Now for the amazing part: this happened as well! It has turned out that profits have run near 10% of GDP for the better part of the past decade, helped by S&P 500 Index containing a much greater proportion of foreign profits which don’t relate to U.S. GDP as well as having more high-margin tech companies10.

Buffett, not expecting these trends, projected a 6% nominal (4% real) annualized rate of return. He must have been way off, right? The actual annual return of the past 17 years was 5.2% nominal (2.9% real). Despite both improbable positive trends of declining interest rates and higher profits/GDP occurring, the stock market delivered pretty close to Buffett’s prediction and actually less. What went wrong? Why did the stock market deliver “only” 2.9% annualized real returns over the past 17 years? For one thing, nominal annual GDP averaged 4%, not 5% as Buffett predicted. Equity valuation also collapsed. Buffett gave his speech near the height of the tech bubble, probably because he knew valuations were stretched and he wanted to temper expectations. This is a good reminder that profits can be strong and interest rates favorable, but the price one pays still bears on forward returns.

We also bring Buffett’s projections up to point out that there is much imprecision in investing. The Sage of Omaha, while a genius, still got two of his main points wrong. Thus, we cannot dismiss the possibility that for the next 17 years interest rates continue down while corporate profits as a percentage of GDP continue to increase. Perhaps the forces that drove the past 17 years are still active. Perhaps we will continue to experience excellent returns despite a GDP growth rate that has slowed meaningfully.

However, it is certainly easier and perhaps more prudent to imagine these tailwinds reversing and turning into headwinds. If we actually do get secularly-rising interest rates and see a higher share of GDP going to workers, which certainly is possible given the multi-decade lows in unemployment, it would represent a significant drag on stock returns regardless of what the economy is doing11. We can make some hypothetical calculations using the observable historical relationship between valuations, earnings and interest rates. For example, assume:

• Nominal GDP of 3.5%

• Inflation of 2%

• Real GDP growth of 1.5%

• Corporate profits as a percentage of GDP at 7% (down from today’s 9.6% but still above what Buffett thought was sustainable)

• Interest rates 2% higher across the yield curve (i.e. ten-year Treasury goes from 3 to 5%)

If the above statistics were in place during the next 17 years, without factoring in any change in valuation from sentiment (which would likely move lower given the unfavorable developments), we calculate the total return of the stock market over this full period would be barely below breakeven. For 17 years. If you added to this mix some serious inflation, you would end up with a seriously negative result.

The above isn’t what we think will happen, but we have to admit it is one of many possible scenarios and we have some concern the trends are beginning to shift a little bit in that direction. We always have to be open to all possible future economic conditions including the possibility that just like Buffett 17 years ago, we could be wrong on our assumptions... GDP could run higher than assumed and corporate profits could become an even more extreme proportion of the economy. This is precisely why we like the historically-based CAPE valuation method when thinking about the future market environment as it involves less explicit forecasting.

What’s the point of walking through all these projections? Consider the valuation/return diagrams you saw earlier in this letter. While they don’t tell us exactly what rate of return to expect from the market, it does appear fairly straightforward that there is an upper limit to them. Fabulous returns are only produced when starting valuation is low, which is not the case today. But since the diagrams generally still suggest a positive rate of return, is this information even that useful? Yes, we can use it to make sure stocks are the best game in town (versus cash, gold, bonds, etc.), but most of the time they are... and this indeed appears true today. Even at elevated levels, our various CAPE-based projections suggest stocks are a better buy than bonds for those with a five to ten year horizon. Our work tells us we will see 4% to 5% annual rates of stock market appreciation (2% to 3% percent after inflation) for the next five to ten years, which is better than the 3% yield (1% after inflation and negative after tax) currently offered by ten-year Treasury bonds, the 3% to 4% (1% to 2% after inflation) for most corporate bonds, and interest rates of 1% to 2% (-1% to 0% after inflation) paid today on cash.

Ultimately we expect that our projections for more middling market returns are actually more useful to you, our clients, than they are to us. While we cannot just decide to have the market deliver higher returns, you can just decide to spend in a manner consistent with investment values growing at a more modest rate. Of course, we endeavor to provide you better returns than those of the overall stock market, but we can only buy stocks that are in the market. Put another way, we can get some blood from the stone but not infinite quantities. Hopefully this letter will help you in making your financial plans, with how much to save, how much to spend and how long to work. We can help you with these plans as well. Our rule of thumb is that spending only 4% of your nest egg each year should see you through retirement, and spending 2% to 3% should see your assets stable or growing and keep your purchasing power intact relative to inflation.

Thank you for indulging a wonky (but we think important) letter. If you would like to see the work behind our projections or better understand our different CAPE calculations, please come see us.

Sincerely,

John G. Prichard

Miles E. Yourman

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

1 We are indebted to Nobel Laureate and Yale University professor Robert Shiller for this approach, and especially for sharing all of his data online which we have used in the forthcoming analysis.

2 Another unfortunate pattern is also recognizable: negative long term results can be achieved at all but the lowest starting valuations.

3 Our dataset actually contains monthly observations, 11 of which have a CAPE ratio within 0.5 of the present reading of 31.77. However, from a practical perspective July, August, and September of 1997 shouldn’t really be considered independent observations.

4 Here when we write “the market” we really mean the S&P 500. In actuality the S&P 500 makes up only about 80% of the total U.S. stock market value, so it’s only an approximation, albeit a pretty good one.

5 Though popularized by Professor Shiller, the idea behind the CAPE was originally advocated by the father of value investing, Benjamin Graham.

6 Accounting is asymmetric in this way: many classes of assets are written down in bad times but not written back up in good times.

7 We actually did look at these. The CAPE 6 is 27.0 and the CAPE 7 is 27.2.

8 This is a bit of an assumption, especially given that government deficits are increasing, and not least because of this tax cut. If you think corporate tax rates are going right back up soon, you can skip this section. Our best guess is that corporate rates will stay low and it is personal rates that will go up (along with entitlement benefits going down).

9 For those interested, a similar CAPE 8 reading was observed in 1901, 1929, 1996, 2001, 2002, 2003, 2004, 2005, 2006, 2007, with the number of observations heavily weighted towards these later years.

10 Offshoring to cut costs and save on taxes didn’t hurt either.

© Knightsbridge Asset Management, LLC

Read more commentaries by Knightsbridge Asset Management