The idea that the United States can win a trade war is pure foolishness. Tariffs are a form of taxation that ultimately is paid not by the exporter, but by the U.S. consumer. If you want to see who the real victims of tariffs are, go look in the mirror.

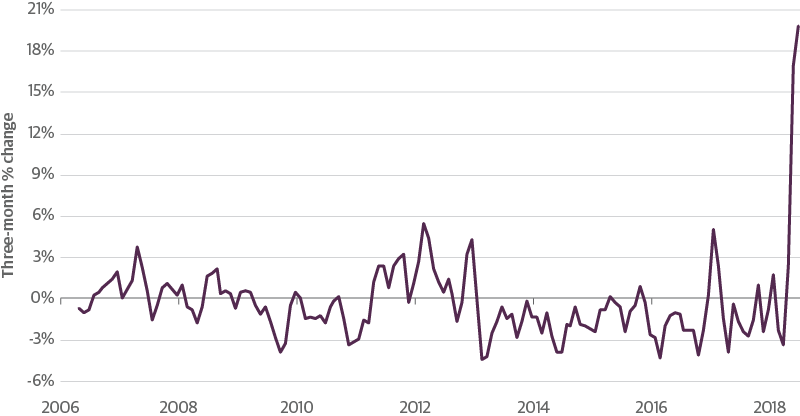

Most analysis of the trade situation does not reflect this hard truth. When the United States imposes tariffs on a specific product from a foreign nation, those tariffs affect pricing on the same products regardless of origin of manufacture, including the United States. When the United States imposed a tariff on imported washing machines earlier this year, domestic washing machine producers saw the opportunity to increase their profit margins and so they raised prices. As a result, according to the Bureau of Labor Statistics, washing machine prices across the board increased by 20 percent in the past three months, the biggest such move since data have been kept.

Tariffs on Imports Caused All Washing Machine Prices to Spike

Source: Bureau of Labor Statistics, Haver Analytics, Guggenheim Investments. Data as of 6.30.2018.

If tariffs are imposed on Chinese electronics or European automobiles, which represent a much larger sector of the economy than washing machines, that won’t just drive up the prices of computers and cars that are being imported into the country, it will drive up prices for those products across the board just as it did with washing machines. If Chinese machinery coming into the United States is slapped with a 25 percent tariff, then all machinery prices will rise.

Increasing the prices of goods and services through tariffs reduces the purchasing power of the disposable income of people who are spending part of their wallet on washing machines, or cars, and steel- and aluminum-based products. Additionally, there is a pass-through effect to other goods and services. For instance, an Uber driver who pays more for a car will either charge more or see a hit to his or her income. The economy-wide increase in the price of goods and services in the United States, called inflation, will only be driven higher by tariffs, which detracts from economic growth, lowering the standard of living for all U.S. citizens.

This imported inflation is coming at a time when tight domestic capacity constraints are already pushing prices higher across the board. The addition of tariffs creates a dilemma for Federal Reserve policymakers, who must lean against this inflationary impulse while recognizing the job-killing aspects of tariffs.

If the goal of tariffs is to help grow the domestic manufacturing base, this is a shaky proposition at best. Placing tariffs on industrial inputs like steel or electrical components only serves to raise costs for domestic manufacturers, partly offsetting any benefit gained from the tariffs on the finished products produced in the United States. One example is that associated with specialty steel, which has left domestic energy producers scrambling to adjust investment plans, as some steel pipelines necessary for projects are simply not made in the United States.

Markets have started to focus more on trade and tariffs because of the concern over their potential negative impact on asset values and the negative impact on the economy.

Our view has been that the yield on the 10-year Treasury note will probably rise to somewhere between 3–3.25 percent in this tightening cycle, with the possibility of briefly reaching as high as 3.5 percent. The latest move above 3 percent, however, has clearly stalled out as talk of trade war picks up. Stocks have shown similar trepidation.

Whether recent events are going to lead to a full-scale global trade war or just become an obscure footnote of history is anybody’s guess, but markets are clearly spooked. With neither the Chinese nor U.S. leader about to blink, this tariff skirmish could ultimately turn into something much bigger and worse than currently imagined. There are voices of moderation in the White House, people like Steve Mnuchin and Larry Kudlow, who are opposed to the idea of engaging in a trade war, but others like Peter Navarro and Wilbur Ross certainly have the president’s ear at the moment. For the time being, I don’t see how we are going to back ourselves off of the trade cliff.

This is unfortunate, because while the focus on China and automobiles is no accident in the administration’s drive to reduce the trade deficit, the chart below shows there are other products and countries trade hawks could target.

Trade Hawks Could Target More than Cars and China

U.S. Goods Trade Defecit by Sector and Country

Source: Department of Commerce, Goldman Sachs, Guggenheim Investments. Data as of 12.31.2017. Size of bubbles reflect size of deficit. No bubble = no trade deficit.

Using tariffs as a policy tool is a game that no one can win. Tariffs on imports from China are not a tax on Chinese citizens, they are a tax on Americans. (So are tariffs on imports from Canada, Mexico, and Europe.) Yes, China will export less so it will hurt them too, but the cost of it is being born by citizens in the United States and the cost is a lot larger than the tariffs being threatened on $250 billion of imports from China.

As China and Europe get dragged into a tit-for-tat battle, more and more consumer goods are likely to be targeted, making the effects of tariffs felt much more in the pocketbooks of Americans. We may soon find that the impact of tariffs on our economy will take away many of the benefits of the fiscal stimulus that was passed in last year’s tax bill. One thing is certain—wars are not fought without cost, and Americans will bear their share of the cost in fighting this war.

Important Notices and Disclosures

Investing involves risk, including the possible loss of principal.

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author or speaker, but not necessarily those of Guggenheim Partners, LLC or its subsidiaries. The opinions contained herein are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information. No part of this material may be reproduced or referred to in any form, without express written permission of Guggenheim Partners, LLC.

Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Real Estate, LLC, GS GAMMA Advisors, LLC, Guggenheim Partners Europe Limited and Guggenheim Partners India Management.

©2018, Guggenheim Partners, LLC. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC.