Economic reality isn’t black and white. At any given time, both good things and bad things are happening. Ignoring one side because it doesn’t fit your preferred outlook is an excellent way to go badly wrong.

Hurricane Florence made landfall in North Carolina today, bringing with it destruction and calamity, the cost of which could top $170 billion, according to analytics firm CoreLogic. If so, that would make it the costliest storm ever to hit the U.S.

Two years ago, Islamic State, Kurds and various rebel groups controlled much of Syria. With Russian and Iranian assistance, Syrian President Assad has been steadily winning back territory.

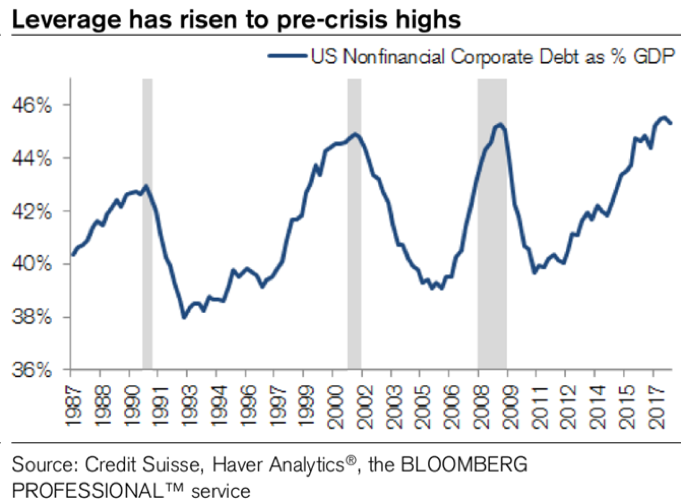

We believe that warning signs are starting to creep into the corporate lending market—and that the ramifications could be problematic for credit investors.

Stimulative measures drive growth, and the U.S. economy and stock market have benefited from quantitative easing, lower rates, less regulation and tax cuts. But Jeffrey Gundlach admonished investors that too much stimulus can backfire.

The recent action in the stock market seems to be governed by crowd psychology and reminds us of a theory we created in college called the “coat theory.” Back in the 1970s, the fraternities and sororities at my alma mater hosted several mixers so the students could get to know each other better.

Friday's jobs report finally included what appears to be evidence of the long-awaited acceleration in wage growth.

We assume prospects will carefully scrutinize every detail of our appearance, the ideas we present and the depth of our technical knowledge. That’s wrong. Believing the spotlight is on us will cost you prospects and assets.

The macro data from the past month continues to mostly point to positive growth. On balance, the evidence suggests the imminent onset of a recession is unlikely. The largest risk to the economy is the escalation in trade war rhetoric.

This week, I had the privilege to attend the Cornerstone Macro Conference in New York. Langone’s presentation, moderated by Omega Advisers CEO Lee Cooperman, stood out as one of the highlights.

In the span of human history, retirement is a fairly new idea. Only a few generations ago, most of our ancestors could expect to work until the end of their lives. We are happy to report this is no longer the case. Improving longevity brings the opportunity for retirement, but also the responsibility for preparing. Unfortunately, many Americans have not handled this responsibility very well at all.

As I get older I find that I value material things a lot less. I am still partial to gadgets, but soft things like conversations, walks – experiences – have started to matter to me a lot more than things. My writing was supposed to be about investing, how to make $2 out of $1, but existential topics have lately had a greater appeal for me than discussions about stocks or the economy.

Our advisors (seven of them) are perfectly content to work with existing clients and not worry about what’s coming next. I’m one of the younger partners in the firm and am motivated to put a true sales system in place. I need advisors who will sell within that system. How do I get them motivated and on board?

SPX, NDX, small caps as well as broad measures like the Russell 3000 - which equals 98% of total US market capitalization - made new all-time highs (ATHs) last week. The trend is clearly higher, and several new momentum studies suggest that equities are likely to gain more before year-end.

Northern Trust’s Economic Research team shares its monthly perspective on the growth prospects and challenges ahead for the U.S., U.K., Eurozone, China, and Japan.

Brad McMillan, Commonwealth’s CIO, recaps the market and economic news for August. It was another good month here in the U.S., with the stock market up across the board. The economy, consumer confidence, and hiring all continued to grow. This growth is translating into corporate profits as well, with 80 percent of companies beating expectations. Still, September is a historically volatile month, and the midterm elections may cause some turbulence. Will these strong fundamentals help carry us forward? Stay tuned to learn more. Follow Brad at blog.commonwealth.com/independent-market-observer.

Current stock market capitalization is largely an artifact of speculative psychology, not reasonably discounted cash flows. Unless investors rely on eternal sunshine of the spotless mind – the assumption that current levels of extreme cyclical optimism will be permanent – they should not expect the associated valuation extremes to be permanent either.

It won’t be easy and key risks remain, but we believe the players and strategies are now in place to transition markets beyond Libor.

It was neigh on ten years ago, the world was just about half way through the ‘Great Recession’ and I was sending out a newsletter wondering how much lower the Dollar could plunge. The Euro/USD pairing was touching 1.50 at one point. How the times have changed!

It was the best of times, it was the worst of times. A tale of two world leaders, U.S. president Donald Trump and China president Xi Jinping—both of whose countries have among the world’s best economies right now. But whereas Xi is playing Santa Claus to the rest of the world, doling out loans to finance-starved countries, Trump is playing Scrooge, waging an economic war with Canada, the European Union, China and others.

With the 10-year anniversary of the onset of the global financial crisis just weeks away, now is a good time to ask where the next global economic crisis might come from. To be clear: We’re not sounding any alarms here. We don’t think a crisis is imminent. But we do like to keep our eyes on the horizon.

In a future of lower expected price appreciation, investors should focus on the second leg of returns: income. ETFs make it incredibly easy to capture diversified sources of higher-yielding assets.

The traditional wholesaler is dying. The future of wholesaling will combine analytics and portfolio construction.

Change-management efforts can span months and should begin well before launch. During this period, firm stakeholders need to manage the expectations of those who’ll use and benefit from the technology. Here are four major themes to address.

When looking to build investment portfolios that target and solve for specific client objectives, we should be conscious of our competencies. We believe finding the appropriate expert to address or complement investor needs is just as important as acknowledging proficiencies.

We expect an acceleration of strategic investments into onshore China bonds as these securities join emerging market and global bond indexes.

Last week, we covered Turkey’s geopolitics and history. This week, we complete the series, starting with a discussion on Turkey’s economy with a focus on the changes brought by the Justice and Development Party (AKP), led by President Erdogan. We also examine how foreign debt affects Turkey’s economy and financial system, highlight the impact of the 2016 coup and analyze the causes of the current crisis in Turkey. From there, we discuss the debt problem and Turkey’s options for resolving the crisis. As always, we conclude with market ramifications.

Reduced global trade may have the unintended consequence of strengthening the US dollar, raising interest rates and pushing down stock prices. Together with tighter Federal Reserve policy, these developments may increase market turbulence.

Trade tensions have spooked investors in recent months, including those in India’s stock market. Franklin Templeton Emerging Markets Equity’s Sukumar Rajah weighs in on the positive economic fundamentals he and the team see, and why they think India’s equity market should be able to weather recent challenges.

Despite the US government’s recent upward revision to personal saving data, the overall national saving rate, which drives the current account, remains woefully deficient. And the major surplus countries – Germany, China, and Japan – have been only too happy to go along for the ride.

Let’s consider two seemingly conflicting ideas.

Can both of those be right? I think so.

Infrastructure investment promises are politically popular, but actual funding has been slow to follow. Italy’s bridge collapse illustrates the real risks of putting off infrastructure projects. The shortage of truck drivers in the U.S. is driving inflation, and this labor market gap looks likely to last.

China has rapidly become the second largest economy in the world – second only to the United States, and by some calculations the largest. As a result, China also has some of the fastest-growing publicly traded companies on the planet.

This memo covers three ways in which securities markets seem to be moving toward reducing the role of people: (a) index investing and other forms of passive investing, (b) quantitative and algorithmic investing, and © artificial intelligence and machine learning.

Read Harold Evensky's latest Newsletter.

The CFP Board wants its credentials to be a mandatory requirement for all advisers who hold themselves out as financial planners. If its lobbying efforts to this end are successful, the Board would then become the de facto regulator of the financial planning profession, which is the organization’s goal. But the Board’s disingenuous position on the fiduciary standard and its long history of putting its own interests ahead of those of consumers and its members make the Board decidedly unfit for this role.

We are living through a period of extremely crowded trades at the moment, as Jeff Gundlach notably quipped several days ago. The risk in crowded trades is of course that what would otherwise be relatively minor risk reversals can cause massive covering of positions resulting in large moves in the underlying.

Turkey has become a major topic of interest. A 2017 constitutional referendum gave the president sweeping powers, and President Erdogan won re-election in June 2018. Since then, an economic crisis has developed, with falling financial asset prices and a sharp currency decline.

Corporations are delegating more of their asset management responsibilities than ever. How does increased delegation affect fiduciary oversight?

US investment-grade corporate bonds look cheaper today than their lower-quality counterparts in the high-yield market. Is this the buying opportunity of a lifetime? Not exactly. A closer look reveals there’s actually method to the madness.

The master limited partnership (MLP) asset class has experienced considerable volatility since 2014, with many individual securities trading well off previous highs. However, the Invesco Real Estate team believes there has been a dislocation in MLP pricing, resulting in value and opportunity in the space.

US equities have returned to their January all-time highs. Several new momentum studies suggest that equities are likely to gain more into year-end. Despite the gains over the past 5 months, investor sentiment is not frothy. US equities now have a topping pattern in place: the momentum high in January has been followed a price high in August.

For the first time in at least 40 years, there’s a fundamental economic reason that a yield curve near-inversion might notherald a recession.

I see some major problems coming in the 2020s (and perhaps a bit sooner), but I also see a lot of good things happening right now. The economic recovery, while still weak by historic standards, is gaining some momentum that ought to carry it forward for another year or two, assuming (as I perhaps naïvely do) that we can put this trade war thing to rest. That’s good news because it buys us time to prepare for worse times, but it’s also just plain good news.

My good friend Marc Lichtenfeld from the Oxford Club has always been savvy in following such strategies. I invite you to learn from his investment journey in this special Q&A.

Dispute could be a setback for productivity, affecting consumers globally.

The crisis in Turkey is rapidly evolving, with new developments emerging every day. Turkish assets sold off significantly from August 8 to 13, before experiencing a short covering rally beginning on August 14. Perhaps the selloff was overdone, or perhaps not. Either way, the trajectory for Turkey has not changed.

Every summer for the past several decades, I have been organizing lunches for serious investors who spend at least part of their vacation time in eastern Long Island. Those attending include hedge fund wizards, real estate titans, corporate chiefs, thoughtful academics and a few others.

A review of last month’s market-moving events across countries and asset classes.