click to enlarge

It was the best of times, it was the worst of times. A tale of two world leaders, U.S. president Donald Trump and China president Xi Jinping—both of whose countries have among the world’s best economies right now. But whereas Xi is playing Santa Claus to the rest of the world, doling out loans to finance-starved countries, Trump is playing Scrooge, waging an economic war with Canada, the European Union, China and others.

Respected economist Art Laffer, whom I’ve written about before, has always supported leaders who ignite global trade rather than close off its borders. A full-blown trade war, Laffer said recently, would be a “curse” on the U.S. economy.

Post-World War II, it was the U.S. that led global trade and infrastructure build-out—the Marshall Plan in Europe, the Interstate Highway System domestically. Both projects required massive amounts of commodities and raw materials, and employed hundreds of thousands of people.

Today, of the two leaders mentioned above, it’s Xi who has a clear foreign policy when it comes to trade and infrastructure.

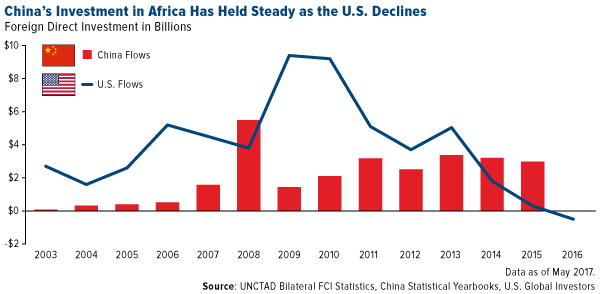

U.S. Fund Flows Into Africa Are Slowing

Case in point: This coming Monday and Tuesday, Beijing will host the Forum on China-Africa Cooperation (FOCAC). The summit, which takes place once every three years and is attended by representatives from 52 African countries, touches on areas as diverse as technology, trade, infrastructure, diplomacy, culture and agriculture.

During the last forum, in 2015, China pledged as much as $60 billion toward Africa’s development in interest-free loans. The Asian country, in fact, has increased its investments in the continent around 520 percent over the last 15 years, according to Global Trade Magazine.

As just one example, Kenya agreed to let China finance and build a standard gauge railway (SGR) connecting two major cities at a cost of $3.8 billion. Contracted by China Road and Bridge, the Mombasa-Nairobi SGR is Kenya’s largest infrastructure project since it declared independence from the U.K. in 1963.

Meanwhile, U.S. fund flows to Africa have been receding, and they’re expected to slow even more during Trump’s administration.

click to enlarge

Xi isn’t doing this out of the goodness of his heart, of course. China, having been Africa’s largest trading partner for nine consecutive years now, likely expects its investments to pay diplomatic and economic dividends for many decades to come.

Even Trump’s own commerce secretary, Wilbur Ross, acknowledges that the U.S. must do more in Africa. “By pouring money into Africa,” Ross wrote on CNBC earlier this month, “China has seen an opportunity to both gain political influence and to reap future rewards in a continent whose economies are predicted to boom in the coming decades,” due mainly to young demographics.

The Belt and Road Initiative Will Affect 60 Percent of the World’s Population

The most well-known among China’s projects is the Belt and Road Initiative (BRI), one of the most ambitious undertakings in human history. The biblical-size trade and infrastructure endeavor—a sort of 21st century Silk Road—could cost 12 times as much as what the U.S. spent on the Marshall Plan to rebuild Europe following World War II. The BRI has the participation of 76 countries from Asia, Africa and Europe, and is poised not only to reshape globe trade but also raise the living standards for more than half of the world’s population.

According to the International Monetary Fund (IMF), the “BRI has great potential for China and participating countries. It could fill large and long-standing infrastructure gaps in partner countries, boosting their growth prospects, strengthening supply chains and trade and increasing employment.”

The BRI, announced in 2013, will have a strong presence in Eastern Europe, also a prime destination for China FDI, as the countries there offer a wealth of metals, minerals and agricultural products.

According to Stratfor, Chinese companies have invested as much as $300 billion in Eastern Europe over the past decade. Last May, China and Ukraine agreed to cooperate on joint projects valued at nearly $7 billion, and in November, it was announced that China Railway International and China Pacific Construction would build a $2 billion subway line in the Ukrainian capital, Kiev. More recently, Chinese engineers with China Harbor Engineering completed a $40 million dredging operation in Ukraine’s Yuzhny Sea Port, allowing it to receive larger ships.

Like the Marshall Plan before it, the BRI will require tremendous amounts of commodities, metals and fuel.

In 2011, members of our investment team and I had the opportunity to see one of China’s high speed trains firsthand. The train averaged 185 miles per hour during our 923-mile trip from Shanghai to Beijing. As I wrote then, “I’ve traveled to all corners of the world and have seen many things during my travels, but viewing China’s explosive growth as it flies by you is something I will never forget.”

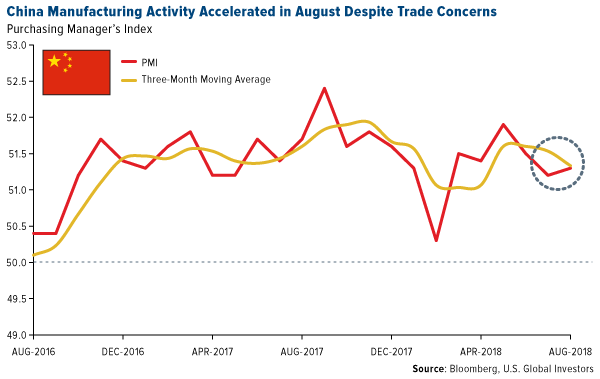

U.S. Investors Hiked Exposure to China

In light of all this, there’s no lack of negative news on China right now. I see headline after headline on the country’s “slowing economy” and “weakening consumption,” but like most things are in the media, these proclamations are overblown.

Look at China’s purchasing manager’s index (PMI). Fresh data out today showed that manufacturing expansion in August accelerated slightly faster than in the previous month. The PMI hit 51.3, up from 51.2 in July and beating analysts’ expectations of 51.0. This was the 25th straight month of economic expansion, despite what I earlier described as the Trump-Kudlow trade war with China.

click to enlarge

Also, as the Peterson Institute for International Economics (PIIE) wrote this week, “there is no empirical evidence that consumption in China is weakening,” contrary to what “official” retail sales data show.

The PIIE’s Nicholas Lardy cited Alibaba’s recent announcement that sales rose 60 percent in the most recent quarter compared to a year ago—“a sign that Chinese retail sales data likely do not fully capture China’s burgeoning digital retail.”

“In any case,” Lardy continued, “retail sales are an increasingly less useful measure of consumption, as China’s large and still growing middle class is spending a growing share of their rising income on education, health care, travel and other services that are not captured in official data on retail sales.”

click to enlarge

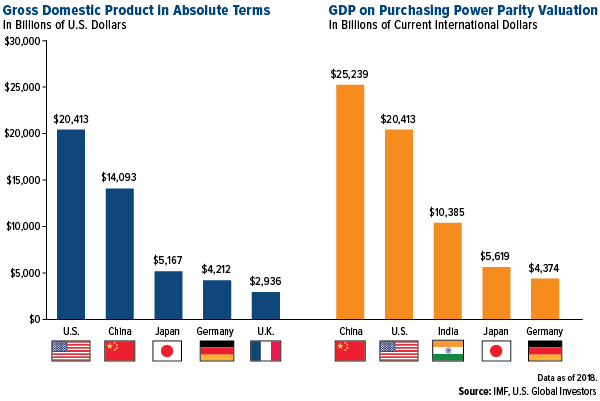

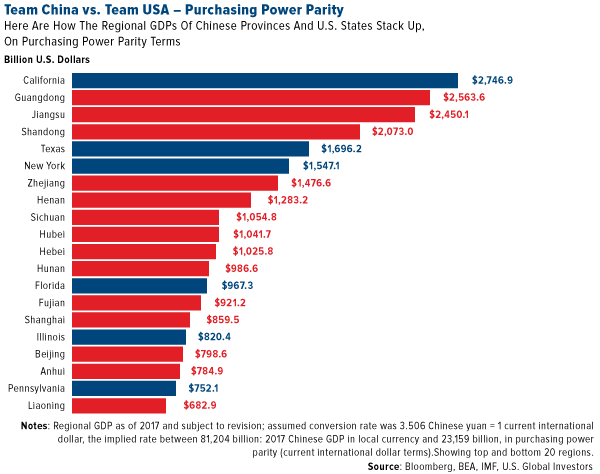

Savvy investors, I believe, get it and can see the opportunity in the world’s number one economy, as ranked by purchasing power parity (PPP). Reuters reports that, in the week ended August 22, U.S. investors poured $572 million into funds that invest in Chinese equities. That was the most for such funds since January.

Although some expect Trump to impose tariffs on $200 billion additional Chinese imports next week, “investors are expecting Beijing to continue counteracting the effects of the [trade] dispute with increasingly relaxed monetary and fiscal policies,” Reuters says.

Curious to learn more? Watch this short video on investment opportunities in China!

Gold Market

This week spot gold closed at $1,201.08 down $4.82 per ounce, or 0.40 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 1.98 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index rose 1.88 percent. The U.S. Trade-Weighted Dollar Index ended the week off 0.06 percent.

| Date |

Event |

Survey |

Actual |

Prior |

| Aug-27 |

Hong Kong Exports YoY |

6.0% |

10.0% |

3.3% |

| Aug-28 |

Conf. Board Consumer Confidence |

126.5 |

133.4 |

127.9 |

| Aug-29 |

GDP Annualized QoQ |

4.0% |

4.2% |

4.1% |

| Aug-30 |

Germany CPI YoY |

2.0% |

2.0% |

2.0% |

| Aug-30 |

Initial Jobless Claims |

212k |

213k |

210k |

| Aug-31 |

Eurozone CPI Core YoY |

1.1% |

1.0% |

1.1% |

| Sep-2 |

Caixin China PMI Mfg |

50.7 |

-- |

50.8 |

| Sep-4 |

ISM Manufacturing |

57.7 |

-- |

58.1 |

| Sep-6 |

ADP Employment Change |

190k |

-- |

219k |

| Sep-6 |

Initial Jobless Claims |

213k |

-- |

210k |

| Sep-6 |

Durable Goods Orders |

-- |

-- |

-1.7% |

| Sep-7 |

Change in Nonfarm Payrolls |

187k |

-- |

157k |

Strengths

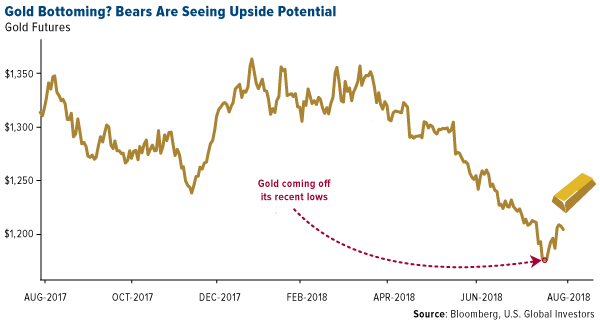

- The best performing metal this week was palladium, up 5.04 percent as hedge funds flip to net bullish on the metal this past week. Despite gold facing a fifth month of losses and bullion-backed ETF holdings reaching a 10-month low, analysts and traders are bullish on the yellow metal, according to a weekly Bloomberg survey. During the Jackson Hole Economic Symposium, Federal Reserve Chair Jerome Powell indicated that investors can expect continued gradual interest rate increases. Gold prices surged following Powell’s comments and held the majority of those gains.

click to enlarge

- In a great example of gold’s Love Trade, a strong U.S. economy empowered consumers to spend their discretionary income on gifts for their loved ones – in particular, gold jewelry. Signet Jewelers, the parent company for Kay Jewelers, experienced a startling 20 percent increase in premarket trading after an unexpected bump in sales. Last quarter, the company reported only a 1.7 percent rise. Tiffany & Co. posted a strong second quarter as well, increasing its global sales by 12 percent. The jeweler announced plans to expand its brick-and-mortar presence in China. This move is well-timed as nationwide gold consumption in China is up 0.3 percent. Gold bar sales in China are down 16 percent, which is completely offset by the gain in jewelry.

- The International Monetary Fund (IMF) approved adding the yuan, China’s currency, into the IMF’s foreign exchange basket. This is the first time the IMF has ever added a new currency to its foreign exchange basket. The IMF’s acceptance opens the door for potentially putting the yuan on par with the U.S. dollar, according to Reuters. Meanwhile, Shandong Gold, a state owned Chinese gold mining company, is preparing to raise $1 billion via a Hong Kong listing.

Weaknesses

- The worst performing metal this week was silver, down 1.92 percent as hedge funds boost their net bearish view to a 20-week high. Gold has fallen for the fifth straight month, making this the longest decline in five years. The yellow metal has been weakened by a variety of sources. U.S. equities are at record highs, the U.S. dollar has been strengthening and President Donald Trump announced his intention to add another $200 billion in tariffs on Chinese imports. In light of these external influences, gold’s road to recovery is unlikely to be a straight one.

- Heavy flooding in Kerala, India, resulted in over $3 billion in damages, draining away funds that would have otherwise been used during the upcoming wedding season. Kerala is India’s biggest gold-buying state. Under ordinary circumstances, families in Kerala spend 200 grams to 1 kilogram of gold for the average wedding. This is expected to drop 50 percent according to the All Kerala Gold & Silver Merchants Association president.

- The Commodity Futures Trading Commission (CFTC) ordered UBS Group AG, a Swiss multinational investment bank and financial services company, to pay a $15 million penalty for manipulating and spoofing precious metals futures markets from January 2008 to December 2013.

Opportunities

- The NYSE Arca Gold BUGS Index rebounded from oversold levels while the relative strength index reached a low on August 16 that hasn’t been seen since July 2015. The last time sentiment toward gold was this bearish was at the end of 2015, before the market swung aggressively the other way, according to BMO analyst Colin Hamilton. “You probably won’t see the short squeeze until about $1,225,” says George Gero, a managing director for RBC Wealth Management.

- Northern Star Resources, the Australia’s third-largest gold producer, announced its acquisition of Sumitomo Metal Mining Co.’s Pogo Mine in Alaskan for $260 million, marking its first overseas operation. This mine is expected to add as much as 260,000 ounces to the Australian producer’s yearly output. Pogo has a resource of 4.1 million ounces at 14 grams per tonne. We continue to see limited merger and acquisition activities playout within the gold sector, despite valuations in the junior space being very depressed.

- Cardinal Resources Limited announced positive drill results earlier this week, identifying significant gold intersections at shallow depths. The company reported 27.0 grams per tonne of gold at 2 meters, 12.6 grams per tonne at 6 meters and 2.2 grams per tonne at 7 meters. Allegiant Gold Ltd. similarly reported successfully expanding the drilling area for its Eastside gold project outside of Tonopah, Nevada. One of its drill holes returned 42.7 meters of 2.49 grams per ton of gold, including 9.1 meters of 9.03 grams per tonne.

Threats

- For those declaring that an inverted yield curve is no longer a recession predictor, the Federal Reserve Bank of San Francisco may have some bad news, reports Bloomberg. “Adjusting for the compensation investors demand to hold longer-dated bonds doesn’t invalidate the curve’s prognosis powers,” notes a new research post published on Monday. Markets have their eye on the narrowing gap between short- and longer-term rates. And as Canada’s yield curve approaches inversion for the first time in more than a decade, the nation’s central bank believes there is little cause for alarm. BlackRock Inc., however, isn’t so sure.

- Some of the biggest buyers of short-dated corporate debt are now turning into sellers, reports Bloomberg. Companies like Apple, Microsoft and Oracle at one time bought $25 billion of debt per quarter, but are now selling in $50 billion clips. According to data tracked by Bank of America Corp., this is leaving a $300 billion-a-year hole in the market and could drive up borrowing costs.

- During the month of June, home prices in 20 U.S. cities rose at the slowest monthly pace in nearly two years, writes Bloomberg. Data released Tuesday point to demand cooling due to affordability constraints. Other notable market news this week includes the fact that short positions against FAANG stocks have surged by more than 40 percent in the past year, to $37 billion. According to Bloomberg, this comes as investors are betting against some of the biggest drivers of the global bull market. Lastly, U.S. President Donald Trump seems to have made no real progress on one of his core promises as he heads into a midterm referendum on his presidency, reports Bloomberg – to raise the wages of America’s “forgotten man and woman.” After factoring in the impact of inflation, the typical hourly earnings of Americans are lower than they were a year ago.

Emerging Europe

Strengths

- Russia was the best performing country this week, gaining 2.9 percent. A lack of new harsh sanctions, the rising price of crude oil and a weaker ruble benefitted Russian equites this week. Gazprom and Lukoil, two of the largest oil and gas companies, posted strong second quarter results, mostly due to higher commodity prices and lower spending.

- The euro was the best relative performing currency this week, losing 12 basis points against the U.S. dollar. Euro-area inflation unexpectedly slowed in August. Consumer price growth came in at 2 percent for August, slightly below the 2.1 percent reading in July.

- Energy was the best performing sector among eastern European markets this week.

Weaknesses

- Czech Republic was the worst performing country this week, as the Prague stock exchange closed flat. The Czech Statistical Office said this week that the economy slowed in the second quarter to a 2.4 growth rate, down from 4.2 percent in the first quarter.

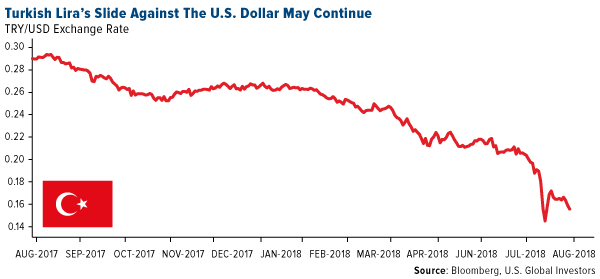

- The Turkish lira was the worst performing currency this week, losing 8.3 percent against the U.S. dollar. Fear of additional sanctions, a growing current account deficit, a high level of foreign debt and rising inflation are all putting pressure on the country’s currency.

- Industrials was the worst performing sector among eastern European markets this week.

Opportunities

- The Polish government announced the introduction of Employee Capital plans, a savings plan that resembles 401k plans in the United States. It had been discussed since 2016 and still needs to be voted on by parliament and signed by the President. These savings plans are set to launch in the second half of 2019 and will cover 11 million people. Tomasz Nowicki from Trigon Analizy believes that it will have a positive impact on the Polish stock exchange. Inflows to the Polish stock exchange should oscillate to around 7-13 billion zloty annually, depending on the amount of contributions. The largest beneficiaries should be the companies comprising the WIG20 Index.

- The Russian government recommended again that state companies should be paying at least 50 percent of net profits in dividends. A higher dividend policy should not lead to a reduction in investment programs, in fact, higher and stable long-term dividends should make Russian assets more attractive to investors.

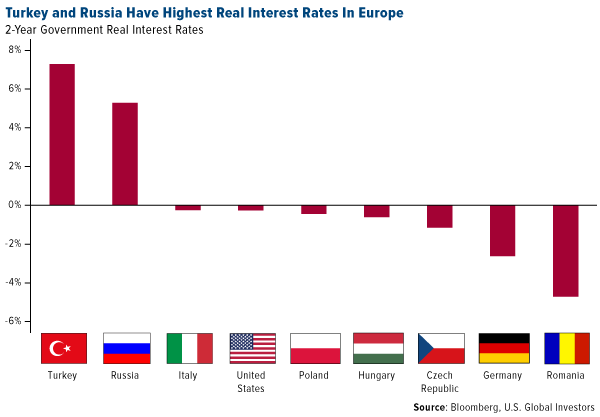

- Turkey and Russia have the highest real interest rates in Europe, while Germany, Europe’s largest economy, and the United States have negative real rates. These emerging markets should be attractive to carry traders. However, the lingering possibility of additional sanctions on Russia and geopolitical uncertainty in Turkey might be keeping them away from these high real rates.

click to enlarge

Threats

- According to Vladimir Tikhomirov, chief economist at BCS Financial Group, the ruble could fall to 76 per dollar by end of 2018 if the U.S. imposes hash sanctions on Russian state banks, energy companies or new sovereign dent. Additionally, GDP would contract by 0.3 percent next year. The Central Bank of Russia may hike rates by 100-150 basis points if the ruble falls sharply against the dollar.

- Ratings agency Moody downgraded 20 Turkish financial institutions, citing there were signs of substantial increase in risk of a downside scenario. Moody’s said Turkey’s operating environment had deteriorated beyond previous expectations. The United States may impose new sanctions over the continued detention of an American pastor, which should put further pressure on the weakening economy and the lira.

click to enlarge

- Eurozone economic sentiment data released on Thursday confirms further weakness in the region. The reading fell for the eighth consecutive month in August to 111.6, versus consensus at 112, and a prior reading of 112.1. Trade tensions between the United States and Eurozone plus the threat of auto tariffs were the main reasons cited for weaker sentiment.

© US Global Investors

www.usfunds.com

© U.S. Global Investors

Read more commentaries by U.S. Global Investors