Trade Turmoil Doesn’t Derail Our Outlook for India

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Indian markets haven’t been immune from the struggles affecting emerging markets generally in 2018.

Domestic headwinds include the re-introduction of long-term capital gain taxes (which affect foreign investors), difficulties collecting the goods and services (GST) tax, interest-rate hike concerns and a weakening rupee. Political uncertainty has also affected market sentiment; recent state elections suggest the ruling party may not be as popular as it had been in the past.

Currency Pressures

While the Indian rupee has been under significant pressure this year, we don’t think there are reasons to be overly concerned right now. A global backdrop of monetary policy tightening, elevated oil prices and rising trade tensions triggered capital outflows from emerging markets and supported US dollar strength. Contagion concerns from the recent Turkey crisis have hurt most emerging-market currencies, not just the rupee. We would also point out that the fall in the rupee has been relatively small compared with the currencies of economies with weaker fundamentals such as Argentina or South Africa.

The Reserve Bank of India has intervened aggressively to support the rupee. In our view, there’s room for further intervention even after the recent reduction in foreign exchange reserves.

While a weak rupee makes imports more expensive, Indian companies have been passing on higher input costs to consumers, which has lifted profits, a sign of solid demand. On the other hand, a weak rupee is positive for export-oriented industries and companies. For example, information technology (IT) companies would likely benefit from a weaker rupee since most of their revenues come from foreign countries. With India’s current account deficit widening, a weaker rupee could help the country’s trade competitiveness as India looks to boost exports.

Positive Macro Factors Amid Headwinds

Despite volatility in India, our assessment of the macro picture and of corporate fundamentals supports our positive long-term conviction for India’s market. We see several factors we think should support a multi-year growth cycle, including growth in consumption and public investment.

Private investment has also shown signs of picking up, along with exports, which look likely to continue to improve.

India is a domestically oriented economy with limited export dependence. With a robust macro situation and strong domestic liquidity in local equities, we expect the Indian market to be more resilient to external factors.

Despite some headwinds, India benefits from a variety of cyclical and structural growth catalysts that preserve our positive outlook. Economic growth has accelerated and the bottom-up corporate earnings trend has improved.

India’s current account deficit has widened versus last year and concerns around fiscal slippage have emerged but the twin deficits remain at levels the government should be able to manage, in our view. Importantly, the widening of the current account deficit can be partly explained by the acceleration of domestic demand (hence import demand) relative to slower growth or even stagnation in global demand. In our view, if the current account deficit increases due to higher domestic growth, market confidence in the currency is unlikely to deteriorate because the market should understand the widening is driven by growth opportunities. Foreign investments could also pick up under the circumstances, supporting the balance of payments.

In addition, the government’s “Make in India” program, which is intended to turn India into a global manufacturing hub, is gradually gaining ground and should likely benefit a variety of sectors, in particular in the electronics manufacturing sector. For example, Samsung opened the world’s largest phone factory near New Delhi earlier this year, in order to manufacture phones at a lower cost compared to China and improve competitiveness in India’s huge smartphone market. In the long term, we could see a substantial rise in the share of locally manufactured products, which would also bode well for the current account balance.

The overall Indian macro story appears stable to us, with consistent positives such as steady gross domestic product (GDP) growth, rising per-capita income, increased private consumption and public investment, and improvement in high-frequency growth indicators such as stronger auto sales and cement production.

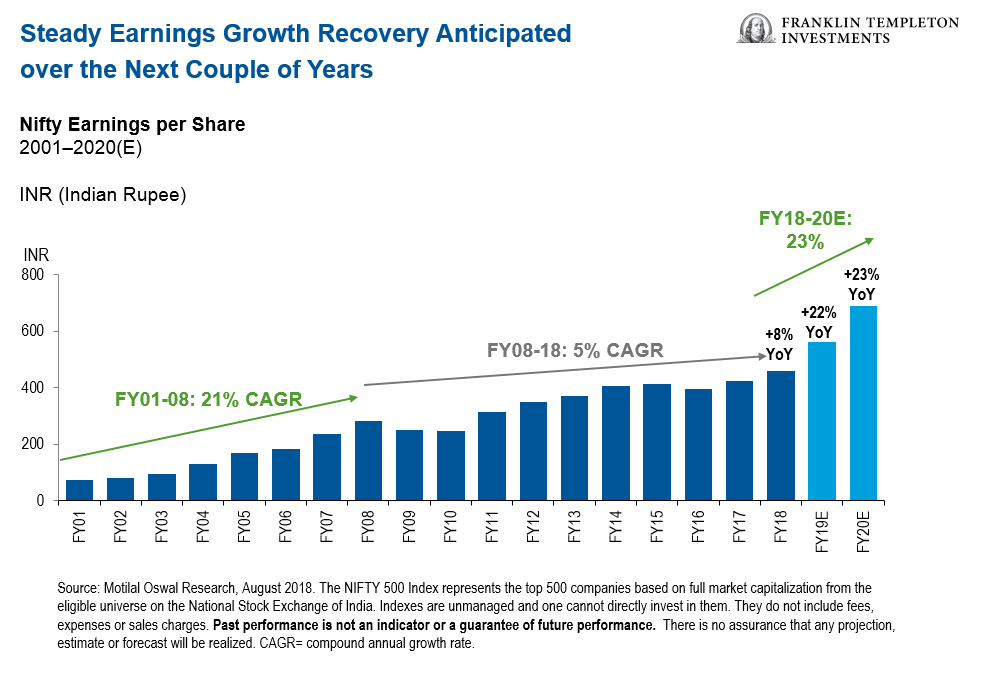

Economic growth appears to remain on a recovery path, and the bottom-up corporate earnings trend has improved in the last few quarters. We think the Indian central bank’s inflation targeting should also help keep inflation in check.

Will India Survive a Potential Trade War?

In relation to trade-war concerns, India exports more to the United States than it imports, so the trade surplus has made India a target of the United States, along with several other countries. In June, India pledged retaliatory tariffs on some US goods, but implementation was delayed to allow time to consider ways to resolve the trade dispute.

While further escalation and resulting uncertainty may further dent sentiment, we believe the fundamentals of the Indian economy remain intact and should be able to weather these issues. We would note that China reduced or eliminated tariffs for goods from India as well as for other countries in Asia, which should help counteract negative impacts of the US actions.

Importantly, India’s growing middle-class population could fuel a boom in consumption, which already makes up over 60% of India’s GDP.1 India’s domestically oriented economy could mean less vulnerability to external factors relative to other more export-driven markets, especially if the trade dispute drags on. The chart below shows that 76% of revenues of companies in the Nifty 500 Index were generated in India.

A Look at Market Sectors

We favor Indian companies with secular growth drivers and remain selective in our picks in domestic cyclicals. Our current focus is on high-quality private sector banks with a strong capital and liability franchise, companies poised to benefit from rising domestic consumption and within sectors that cater to the government’s investment priorities (highways, railways or power transmission). We look for firms with strong internal drivers and long-term fundamentals that could perform irrespective of the economic cycle and may exhibit less vulnerability to macro factors. At the micro level, we feel encouraged by positive feedback from companies generally seeing strong demand on the ground.

Financials: The Indian banking system has been one of the fastest-growing banking systems in the world. However, the average Indian household holds more than 90% of its wealth in real estate, physical goods and gold and only 5% in financial assets such as deposit and savings accounts, publicly traded shares, mutual funds, life insurance and retirement accounts.2 So we think there is significant growth potential for financial services, particularly banks.

Financials: The Indian banking system has been one of the fastest-growing banking systems in the world. However, the average Indian household holds more than 90% of its wealth in real estate, physical goods and gold and only 5% in financial assets such as deposit and savings accounts, publicly traded shares, mutual funds, life insurance and retirement accounts.2 So we think there is significant growth potential for financial services, particularly banks.

State-owned banks dominate market share but are less competitive and lag private-sector banks in areas like automation, technology, customer service and management quality. Thus, we expect private-sector banks to grow faster and gain market share. Recent concerns about high levels of bad loans at state banks could also benefit private lenders. In addition, with non-performing loans (NPLs) almost fully recognized by banks, we should likely see some continued improvement in credit growth and acceleration in loan growth.

Energy: While India’s economy can probably absorb oil prices at current levels or temporary spikes in oil prices, we recognize sustained high oil prices may be detrimental, as it is an energy-dependent economy and an oil net importer. High oil prices could have some detrimental effect as the government is committed to staying on the path to fiscal consolidation and managing government finances prudently. In addition, due to heavy regulations governing the energy sector in India, oil exploration and production companies can’t benefit significantly from rising oil prices. So, currently we don’t see opportunities in the sector to play an increase in oil prices. Therefore, the sector is not one we are particularly keen on at this time.

Energy: While India’s economy can probably absorb oil prices at current levels or temporary spikes in oil prices, we recognize sustained high oil prices may be detrimental, as it is an energy-dependent economy and an oil net importer. High oil prices could have some detrimental effect as the government is committed to staying on the path to fiscal consolidation and managing government finances prudently. In addition, due to heavy regulations governing the energy sector in India, oil exploration and production companies can’t benefit significantly from rising oil prices. So, currently we don’t see opportunities in the sector to play an increase in oil prices. Therefore, the sector is not one we are particularly keen on at this time.

Industrials: Despite some challenges, we remain positive on select companies in the sector that look to potentially benefit from consumer demand. For example, we expect strong structural growth in demand for air conditioning given the very low penetration. Auto parts are another example where demand seems likely to grow along with India’s middle class. In his 2018 budget speech, India’s Finance Minister Arun Jaitley described infrastructure as a growth driver and said the country will need massive investments in roads, airports and railways and inland waterways while hinting that the money could be raised through the equity market. 3

Telecommunication Services: The industry went through a period of consolidation as a new entrant disrupted the market with extremely low pricing in late 2016. However, we believe such a pricing strategy is not likely sustainable in the long run. We see value in select stocks in the sector and think there is further room to run now that the industry has entered the final phase of consolidation.

Information Technology (IT): As India is known for its IT outsourcing capabilities, we see increased spending from global companies. India’s IT sector may also benefit from any rupee weakening. We are focused on IT names where we believe the combination of increasing growth and currency depreciation may support earnings growth for the next couple of years. We see increases in spending from global companies, especially in new development projects, which indicates a sign of revival. In our experience, such projects are multi-year in duration which indicates a multi-year upcycle. IT is a key area of spending for many companies, and we now see potential opportunity in this sector.

Information Technology (IT): As India is known for its IT outsourcing capabilities, we see increased spending from global companies. India’s IT sector may also benefit from any rupee weakening. We are focused on IT names where we believe the combination of increasing growth and currency depreciation may support earnings growth for the next couple of years. We see increases in spending from global companies, especially in new development projects, which indicates a sign of revival. In our experience, such projects are multi-year in duration which indicates a multi-year upcycle. IT is a key area of spending for many companies, and we now see potential opportunity in this sector.

Valuations

We believe Indian market equity valuations remain reasonable in the context of a low earnings base and expected earnings growth recovery. Indian price-earnings (P/E) valuations also remain reasonable within a standard deviation to the long-term average, while a total market capitalization to GDP ratio of ~89% (as of July 31, 2018) indicates to us that Indian equities remain reasonably priced, in our view.4

Moreover, valuations have come down given the market’s recent correction, and we think this can provide a good potential buying opportunity. While we had been of the view that mid-cap valuations had risen to unsustainable premiums to large caps for some time, mid-cap valuations have come off from recent highs and to a greater magnitude than their large-cap counterparts. That said, we feel Indian mid-cap stocks remain expensive compared to larger companies, which warrants cautious selectiveness in this segment.

Importantly, we continue to find numerous companies offering attractive valuations in our research universe so we don’t feel concerned about current benchmark multiples.

Market Outlook

Looking ahead, we believe India’s economic growth remains on a recovery path. We see signs of a GDP growth recovery after the recent softening trend tied to the disruptive effect of one-off events, such as demonetization and the implementation of the GST. Recent high-frequency indicators have confirmed a pickup in growth momentum, led by an acceleration in consumption growth, and with a notable improvement in industrial production.

Moreover, India benefits from several secular growth drivers including favorable demographics, infrastructure investment, urban consumption growth and increasing income levels, as well as the impressive reform agenda being pursued by the government. Many of the changes currently taking place in the country will serve as a positive catalyst, spurring potential future growth, in our view.

While the election calendar may distract investors, we believe investors should be cautious not to read too much into state elections poll results. These polls may not be indicative of what the results in the national elections will be, as there have been reports of people voting against the ruling party in the state election but still intending to vote for Prime Minister Modi in the next national elections. Regardless of which party ultimately wins the 2019 general election, we do not believe the election result will change the course of the economy or cause any significant policy disruptions. The pillars of economic growth are moving in the right direction.

In addition, although concerns have emerged around macro stability due to oil price trends and their potential impact on the current account deficit, inflation and fiscal situation, we believe the government is committed to staying on the path to fiscal consolidation and managing government finances prudently.

All in all, we think the case for investing in India remains.

The comments, opinions and analyses presented herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

What Are the Risks?

All investments involve risks, including the possible loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

________________________________________

1. Sources: FactSet and India’s Ministry of Statistics & Programme Implementation, March 2018. See www.franklintempletondatasources.com for additional data provider terms and conditions.

2. Source: Reserve Bank of India, “Report of the Household Financial Committee,” Indian Household Finance, July 2017.

3. Source: Budget 2018-2019 Speech of Arun Jaitley, February 1, 2018.

4. Source: CEIC, Morgan Stanley Research, July 31, 2018. The price-earnings (P/E) ratio is a valuation multiple defined as market price per share divided by annual earnings per share (EPS). Standard deviation is a measure of the degree to which an asset’s return varies from the average of its previous returns. The larger the standard deviation, the greater the likelihood (and risk) that performance will fluctuate from the average return.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All