This Self-Made Billionaire Reminds Americans that Only Capitalism Creates Wealth

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits“Capitalism works” is how Ken Langone, billionaire co-founder of Home Depot, opens his new book, I Love Capitalism!: An American Story.

“Let me say it again: It works! And—I’m living proof—it can work for anybody and everybody…. Show me where the silver spoon was in my mouth. I’ve got to argue profoundly and passionately: I’m the American Dream.”

This week, I had the privilege to attend the Cornerstone Macro Conference in New York. Langone’s presentation, moderated by Omega Advisers CEO Lee Cooperman, stood out as one of the highlights.

Growing up poor in Roslyn Heights, Long Island, the son of a plumber and a school cafeteria worker, Langone didn’t initially seem destined for greatness.

|

But like other self-made billionaires, Langone didn’t let his humble background stand in the way of his ambitions. Married with a toddler and another baby on the way, he quit a good-paying insurance position to try and make it on Wall Street—a “closed, Waspy world back in those bad old days,” as he describes it in I Love Capitalism!

He managed to get his first Wall Street job, in institutional sales at broker-dealer R.W. Pressprich, after offering to get paid a secretary’s salary. The rest, as they say, is history.

Since co-founding Home Depot—which employees upwards of 400,000 people and hit $100 billion in sales for the first time last year—Langone has become a prominent philanthropist.

Remember hearing recently that New York University (NYU) would now be tuition-free for all incoming med students? That was made possible not because of socialism, but because of donations from capitalists like Langone. He and his wife gave the school $100 million after learning that the U.S. could face a serious doctor shortage in the coming years.

As he explained at the conference, only capitalism creates wealth, which is then freely redistributed. Socialism creates little to no wealth and redistributes poverty. People in Venezuela, sadly, are learning this lesson firsthand, as inflation, there is forecast to hit an unbelievable 1 million percent by the end of the year.

I believe this is a lesson many Americans need to be reminded of, especially now as faith in capitalism is waning and interest in socialism is getting stronger, according to a Gallup poll in August. Capitalism “is not perfect,” Langone said on FOX Business last month, “but it’s the best out there.”

Global Risks May Bring the Polish to Gold

Keep your eyes on the price of gold because the Fear Trade is about to heat up. And I’m not just saying that because the U.S. trade war with China is about to intensify even further, with tariffs on $267 billion worth of Chinese goods announced today.

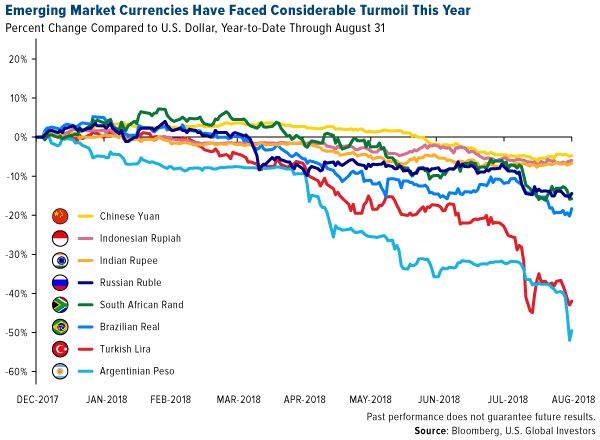

It’s been 10 years now since the start of the global financial crisis, and emerging markets are signaling trouble that some investors fear could have a spillover effect into developed markets. This week, the MSCI EM Index, which consists of 24 countries, entered bear market territory after falling more than 20 percent from its January high.

EM currencies have been under considerable pressure so far this year, with some of them falling to record or near-record lows against the U.S. dollar. Other factors include global trade tensions and higher oil prices—both of which contribute to faster inflation. Rising U.S. interest rates are also making it harder for governments to pay off dollar-denominated debt.

The fear is that the EM slowdown could spell contagion, as we saw in the late 1990s with the Asian financial crisis. Although I don’t believe the current situation to be as bad as the one in 1997, it might prove prudent to ensure that your portfolio has the recommended 10 percent weighting in gold bullion and high-quality gold funds with a proven track record. In its latest report, research firm Metals Focus warns that global growth could take a hit should these markets continue to stumble, “with the resultant stock market impact encouraging investors to gradually rotate in favor of gold.”

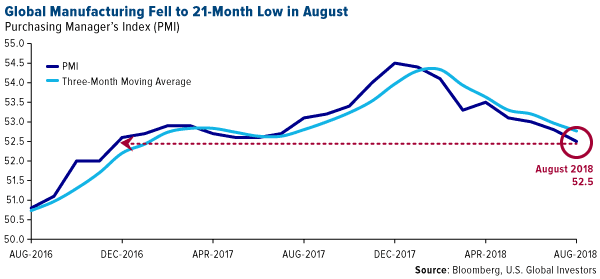

We’re already seeing some slowdown in the global manufacturing expansion rate. The purchasing manager’s index (PMI) has been dropping steadily since its recent high in December 2017, and in August it fell slightly to 52.5 from a July reading of 52.8, with “confidence regarding the outlook for one year’s time [dipping] to a near two-year low,” according to IHS Markit, which compiles the monthly PMI data.

This week gold was trading in the $1,200 an ounce range. But there’s even greater upside potential, I believe, as investors, especially those in emerging markets, seek a safe haven from their country’s weakening currencies against the dollar. Now could be a good opportunity to add to your exposure at an attractive valuation.

Another Emerging Market Crisis?

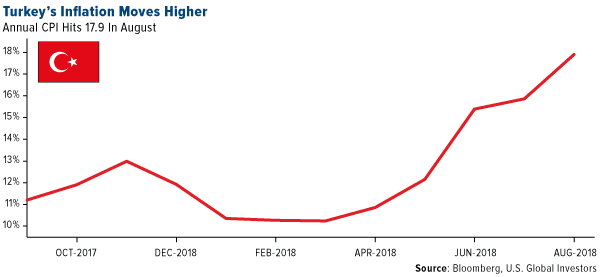

Turkey was among the fastest growing economies last year, expanding 7.4 percent, but it could be facing stagflation on higher inflation—consumer prices rose close to 18 percent in August—U.S.-imposed sanctions and a private sector debt crisis. The lira has lost more than 40 percent this year, and as I shared with you last month, President Recep Erdogan has urged his fellow Turks to convert gold and hard currencies into lira in an attempt to shore up the country’s troubled currency.

The worst performing currency in emerging markets so far this year is the Argentinian peso, off 50 percent as South America’s second-largest economy edges closer to recession. Investors were rattled this week when President Mauricio Macri’s administration unexpectedly enacted new export taxes and austerity measures, including ministry cuts, in an effort to balance the budget ahead of a $50 billion emergency loan from the International Monetary Fund (IMF). With interest rates at an eye-watering 60 percent, the highest in the world, economists surveyed by the country’s central bank forecast an economic contraction of nearly 2 percent in 2018.

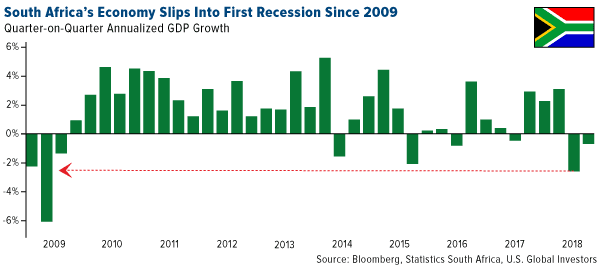

And then there’s South Africa. Its economy has slipped into recession for the first time since 2009, having contracted for two straight quarters, according to the national statistical service.

Among the weakest sectors in South Africa during the second quarter was agriculture, which plunged almost 30 percent on lower production. The best performing sector was mining, which rose nearly 5 percent on increased production of platinum metals, copper and nickel.

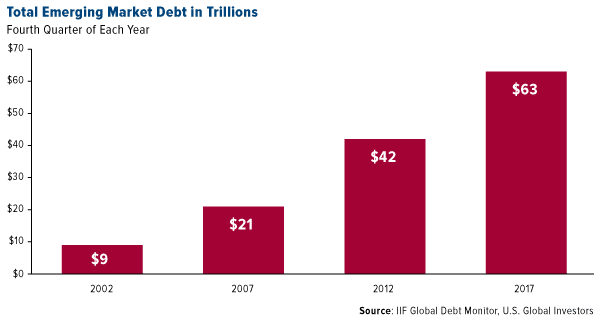

Exacerbating all of this is historically high levels of debt. Debt in emerging markets stood at $63 trillion in 2017, up sevenfold from 2002 levels, according to the Institute of International Finance (IIF). And as I said earlier, higher U.S. interest rates make servicing this debt more expensive.

American Workers Get a Raise

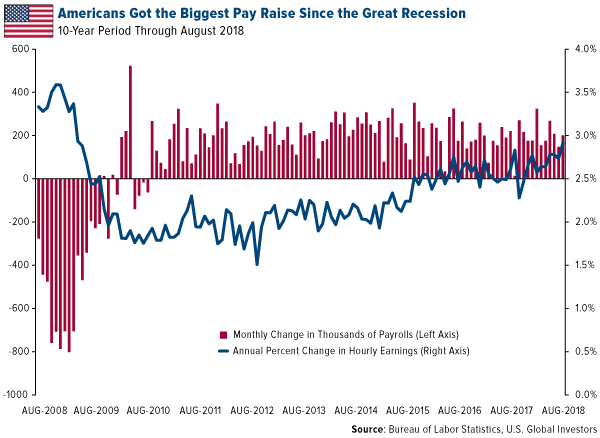

Speaking of interest rates, I believe it’s a near-guarantee that they’ll be hiked again this month after today’s positive jobs report. The U.S. added 201,000 in August, beating economists’ expectations of 190,000. This is the 95th straight month that U.S. employers hired more people than fired—a record streak.

What’s more, wages for American workers in August accelerated 2.9 percent year-on-year—right in line with official annual inflation and marking the fastest pace of wage growth since the financial crisis.

This is good news indeed for retailers such as Home Depot. It’s also constructive for the U.S. economy as a whole. Second-quarter gross domestic product (GDP) growth is expected to be revised up to 4.4 percent from the earlier 4.2 percent, based on higher-than-anticipated consumer spending. And the Federal Reserve Bank of Atlanta now predicts GDP in the third quarter to expand at the same rate, 4.4 percent, spurred by strong consumer confidence, lower corporate taxes and deregulation.

Explore exciting investment opportunities in the domestic market!

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.19 percent. The S&P 500 Stock Index fell 1.03 percent, while the Nasdaq Composite fell 2.55 percent. The Russell 2000 small capitalization index lost 1.58 percent this week.

- The Hang Seng Composite lost 3.45 percent this week; while Taiwan was down 1.96 percent and the KOSPI fell 1.78 percent.

- The 10-year Treasury bond yield rose 7.9 basis points to 2.94 percent.

Domestic Equity Market

Strengths

-

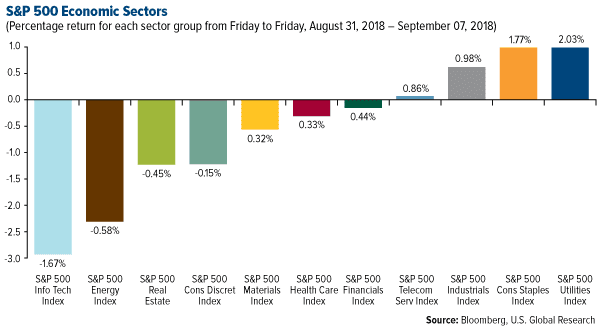

- Utilities was the best performing sector of the week, increasing by 0.99 percent versus an overall decrease of 1.04 percent for the S&P 500.

- Ulta Beauty was the best performing stock for the week, increasing 9.92 percent.

Weaknesses

- Information technology was the worst performing sector for the week, decreasing by 2.93 percent versus an overall decrease of 1.04 percent for the S&P 500.

- Micron Technology was the worst performing stock for the week, falling 14.58 percent.

- Shares of Tesla fell as much as 10 percent during trading on Friday as the company disclosed that its chief accounting officer resigned less than a month after he assumed the job. It has also been reported that its chief human resources officer, Gaby Toledano, is not returning to the company after taking a leave.

Opportunities

- Broadcom's revenue surged this week. The chipmaker reported revenue rose 13.6 percent year-over-year in the second quarter to $5.06 billion, topping the $4.46 billion that analysts were expecting.

- Okta, the company that helps employees log into their corporate apps, soared 16 percent on a major earnings and revenue beat. The company's quarterly losses decreased, and it projected continued growth in the upcoming third quarter.

- Google announced it will unveil its next Pixel smartphone on October 9. Invitations to the launch were sent out Thursday, and the event will be held in New York City for the first time.

Threats

- Semiconductor stocks plunged after warnings on demand from Wall Street and a key industry player. Morgan Stanley said the memory chip market's fundamentals are getting worse, citing rising pricing pressure and inventories. KLA-Tencor shares fell after its chief financial officer, Bren Higgins, gave more negative appraisal of the memory market at a technology conference Thursday.

- A so-called “blue tsunami” during the election could be devastating for stocks. Such a scenario, in which the Democrats win both the House and the Senate, could produce extreme gridlock, slower regulatory relief, a freeze on Supreme Court nominations and impeachment proceedings, Mike Ryan, the chief investment officer at UBS, said in a note on Tuesday.

- America's small businesses warned of widespread layoffs and shutdowns if Trump doesn't back down from a trade war with China. Small businesses that testified before a panel of U.S. trade officials at a public hearing in Washington last month said that they would have to immediately lay off employees to absorb the cost of tariffs on imports if Trump enacted new measures against China.

The Economy and Bond Market

Strengths

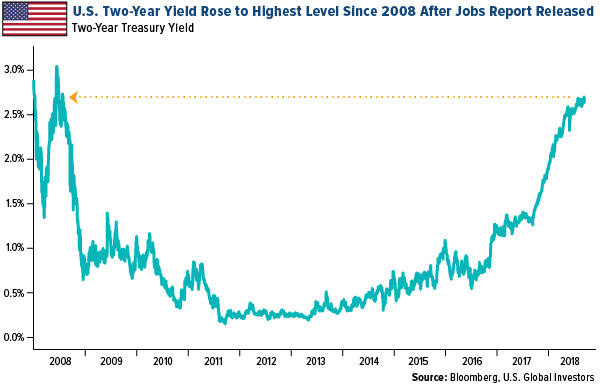

- The yield on two-year Treasuries rose to 2.69 percent on Friday, the highest level since July 2008, after the U.S. jobs report for August showed an unexpected uptick in average hourly earnings growth. The better-than-anticipated data are helping to cement expectations for a Federal Reserve rate hike later this month, while the odds of an additional increase by year end have also received a boost.

- Total nonfarm payroll employment increased by 201,000 in August, and the unemployment rate was unchanged at 3.9 percent, the U.S. Bureau of Labor Statistics reported on Friday. Job gains occurred in professional and business services, health care, wholesale trade, transportation and warehousing and mining. Economists forecasted an increase of 191,000.

- Long-awaited wage growth posted its biggest increase of the economic recovery in August, with average hourly earnings rising 2.9 percent for the month on an annualized basis versus expectations of 2.7 percent. This is the largest increase since April 2009.

Weaknesses

- New orders for U.S. manufactured goods pulled back by more than expected in the month of July, according to a report released by the Commerce Department on Thursday. Factory orders fell by 0.8 percent in July. Economists had expected factory orders to drop by 0.6 percent.

- U.S. service sector business activity saw a weaker rise in August. The seasonally adjusted final IHS Markit U.S. Services Business Activity Index came in at 54.8, a drop from 56 in July. The overall rate of growth slowed to the weakest since April.

- U.S. construction spending remained mostly unchanged in July, as increases in homebuilding and investment in public projects were overshadowed by a sharp drop in private nonresidential outlays. The Commerce Department said that construction spending inched up 0.1 percent.

Opportunities

- Retail sales data released next Friday are estimated to show a healthy growth rate in August. The forecast is for 0.4 percent month-over-month growth, moderating slightly from the prior 0.5 percent.

- Industrial production data set for release next Friday is forecast to show a third straight month of gains in August, rising by 0.3 percent month-over-month.

- The Consumer Price Index (CPI) report comes out next Thursday. Annual inflation as measured by the CPI is expected to decrease slightly from 2.9 percent to 2.8 percent. The core rate is forecast to stay unchanged at 2.4 percent. While the Fed doesn’t pay too much attention to CPI inflation, it is still considered a good indicator of inflationary pressures in the U.S. economy.

Threats

- President Donald Trump elevated trade war rhetoric with China on Friday, threatening tariffs on an additional $267 billion worth of Chinese goods.

- With investors showing more signs of concern about some of the market's biggest sources of return, including tech stocks and emerging markets, they have been moving big into the riskiest corner of the debt market this quarter: high-yield bonds.

- Germany's factory activity slowed unexpectedly in July, offering more evidence that President Donald Trump's aggressive trade rhetoric is affecting confidence globally.

Gold Market

This week spot gold closed at $1,196.57 down $4.83 per ounce, or 0.40 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 3.81 percent. The S&P/TSX Venture Index fell 1.75 percent. The U.S. Trade-Weighted Dollar Index ended the week up 0.25 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Sep-2 | CH Caixin China PMI Mfg | 50.7 | 50.6 | 50.8 |

| Sep-4 | US ISM Manufacturing | 57.6 | 61.3 | 58.1 |

| Sep-6 | US ADP Employment Change | 200k | 163k | 219k |

| Sep-6 | US Initial Jobless Claims | 213k | 203k | 213k |

| Sep-6 | US Durable Goods Orders | -1.70% | -1.70% | -1.70% |

| Sep-7 | US Change in Nonfarm Payrolls | 190k | 201k | 157k |

| Sep-11 | GE ZEW Survey Curent Situation | 72 | -- | 72.6 |

| Sep-11 | GE ZEW Survey Expectations | -14 | -- | -13.7 |

| Sep-12 | US PPI Final Demand YoY | 3.20% | -- | 3.30% |

| Sep-13 | GE CPI YoY | 2.00% | -- | 2.90% |

| Sep-13 | EC ECB Main Refinancing Rate | 0.00% | -- | 0.00% |

| Sep-13 | US CPI YoY | 2.80% | -- | 2.90% |

| Sep-13 | US Initial Jobless Claims | 210k | -- | 203k |

| Sep-13 | CH Retail Sales YoY | 8.80% | -- | 8.80% |

Strengths

- The best performing metal this week was palladium, down 0.31 percent. Gold traders and analysts are bullish on the yellow metal for a third week in a row, according to a weekly Bloomberg survey. Although silver has fallen 16 percent so far this year, its continued losses have spurred physical demand. The U.S. Mint reported its strongest silver sales so far this year with 1.53 million one ounce American Eagle Silver coins sold, a 72 percent increase from July. Annually, silver sales were up almost 50 percent from August 2017, reports Kitco News. The Perth Mint also reported strong numbers with sales of gold coins and minted bars surging 30 percent to 38.904 ounces in August. Silver sales rose nearly 7 percent from July and about 33 percent from a year earlier.

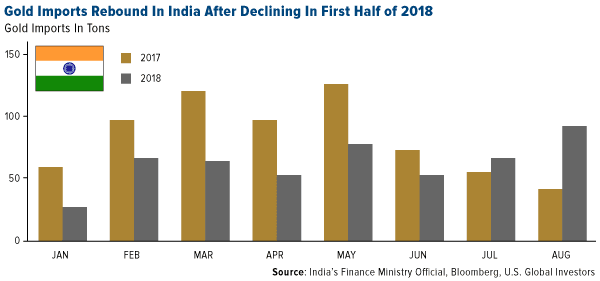

- Gold imports to India, the world’s second largest consumer of the yellow metal, more than doubled in August to their highest level in 15 months. Demand has been weak in India so far this year with imports falling 12.9 percent from a year earlier to 532.1 tonnes in the first eight months, according to data compiled by GFMS. The World Gold Council said that demand is expected to improve throughout the rest of the year as the government takes steps to boost farmers’ incomes, which would boost rural buying power.

- The Bank of Mongolia reported on Thursday that is has purchased 12.2 tons of gold in the first 8 months of this year, with a target of buying a total of 22 tons of gold by the end of 2018. Most of the gold purchased is locally mined, with gold miners submitting just over 20 tons to the central bank last year and total Mongolian production remaining below 21 tons. Central banks purchasing gold demonstrates continued support for gold as a strong reserve currency.

Weaknesses

- The worst performing metal this week was silver, down 2.54 percent. Although the U.S. Mint reported positive news for silver sales, they also announced subdued gold sales. Physical demand for gold coins fell to a four-month low in August. 21,500 ounces of gold in various denominations was sold, which is a 38 percent decline from July. According to the World Gold Council, holdings in gold-backed ETFs fell by 40 tonnes in August, or down 3 percent relative to July, for the third consecutive month of declining assets under management. Global outflows were led by North American funds, which lost $1.65 billion.

- On Monday, the highest court in Guatemala confirmed the suspension of Tahoe Resources’ mining licenses at its San Rafael unit, reports Kitco News. “The Constitutional Court upheld the suspension of licenses at Tahoe’s Escobal mine, one of the world’s biggest silver mines, and at the company’s smaller Juan Bosco mine,” the article reads. The initial suspension was in July 2017 when an anti-mining group alleged that the energy and mining ministry did not consult with the Xinca indigenous people prior to awarding the license to Tahoe, Kitco continues.

- According to the World Platinum Investment Council’s latest quarterly report, global platinum demand contracted by 8 percent from a year earlier in the second quarter of this year. Automotive demand fell 5 percent, while jewelry demand was unchanged. However, with demand weaker and supply little changed at 1 percent growth, the platinum market had a surplus of 340 koz. Overall forecasts for the year estimate both supply and demand for the precious metal will fall by 2 percent each.

Opportunities

- The Reserve Bank of India (RBI) has made its first gold purchase in nine years, reports Bloomberg. The bank purchased 8.46 tonnes of gold in financial year 2017-2018. According to its latest annual report, RBI held 566.23 tonnes of gold as of June 30, 2018, compared with 557.77 tonnes as of June 30, 2017, the article continues. A primary reason for this purchase was the depreciation of the rupee against the dollar, the report notes.

- A survey of 174 private banks, family offices, wealth management advisers and other market experts in Asia reveal the latest recommendation by advisers to Asia’s super rich clients. “Most advisers in the survey – 62 percent – said their clients should or maybe should increase their weighting in gold, versus 38 percent who said they should not,” reports The South China Morning Post. According to the survey, the advisers think their clients should be taking advantage of price declines to buy gold amid volatile global markets and U.S.-China trade tensions.

- Coeur Mining has declared commercial production at its silver-zinc-lead mine in British Colombia, which it gained after purchasing Silvertip in October. The company has updated company-wide output guidance as a result and projects 36.1 to 39.5 million silver-equivalent ounces, reports Kitco News. Randgold Resources has resumed operations at the Tongon gold mine after management lifted a lockout due to a protracted legal strike. Negotiations resulted in an agreement in which workers are being re-employed in phases as various sections of the mine start back up. Goldcorp said this week that it has achieved “significant progress” on key permitting and project milestones that are a part of the company’s five year plan to increase gold production and reserves by 20 percent. President and CEO David Garofalo said that Goldcorp has moving projects forward “on time and on budget through the permitting and development process.”

Threats

- A stronger U.S. dollar, paired with rising U.S. interest rates, has curbed the appeal of “non-interest bearing assets such as precious metals,” reports Bloomberg. In addition, worries over industrial demand because of trade disputes and emerging market turmoil have added to pressure on silver, the article continues. Silver has experienced a 16 percent decline this year, with the ratio of gold to silver price hitting its highest level since October 2008.

- The Argentinian government has enacted a temporary export tax that could likely negatively impact precious metals. BMO writes that while details are still emerging, it is known that precious metals bars will be subject to a 4 peso tax on every U.S. dollar of revenue. This tax has been implemented in an effort to balance the budget in the face the Argentina peso falling more than 50 percent so far this year. Mining companies are still assessing the potential impact on profits. BMO estimates that earnings-per-share will decline on average 7 percent for seven of the precious metals miners in the country.

- The Bureau of Labor Statistics released August numbers showing that the U.S. economy added 201,000 jobs and average hourly wages increased by 0.4 percent. The data was better than expected and a growing economy continues to support a stronger U.S. dollar. George Gero, managing director with RBC Wealth Management commented on the jobs numbers calling them “strong economic numbers that support the dollar and weaken gold temporarily”. Gold historically performs well during the month of September, however it might continue to struggle this month. In its monthly commodity outlook, ITNL FCStone writes that they believe “September likely will be another messy month for gold as in addition to the unresolved trade issues that threaten to push the dollar higher, the market will have to contend with yet another Fed rate increase.”

Blockchain and Digital Currencies

Strengths

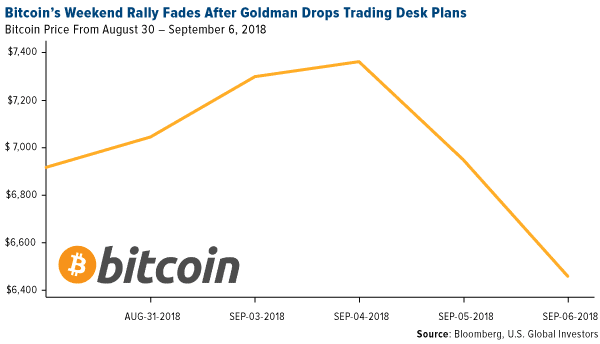

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended September 7 was Webcoin, which gained 308.60 percent. The price of bitcoin moved “sharply higher” over the weekend, up as much as 5 percent and crossing both its 50- and 100-day moving averages, reports MarketWatch, which are two closely watched momentum indicators. Unfortunately these gains didn’t last long as the week progressed.

- Riot Blockchain (RIOT) was up nearly 2 percent on Tuesday, following gains made by bitcoin in early morning trading at the start of the week, reports Seeking Alpha. RIOT announced a licensing pact with Coinsquare, to “provide a RiotX branded version of the Coinsquare platform that prepares Riot for launching a U.S.-focused cryptocurrency exchange,” the article continues.

- IBM’s blockchain division is expanding its work on technology designed to give individuals greater control over their personal data, writes Coindesk.com. IBM will be working with Hu-manity.co on an app that relates to the field of “self-sovereign identity,” and is a strong indication that the company sees great potential in the long-term business value in this use case for distributed ledgers. General Manager of IBM Blockchain Marie Wieck told Coindesk, “Getting people’s permissioned rights on a blockchain will create a marketplace and entirely new economic business models as a result.”

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended September 7 was AVINOC, which lost 51.82 percent.

- Despite bitcoin rising higher over the weekend and into the start of the holiday-shortened week, the popular digital currency fell as much as 6 percent in early trading on Wednesday and fell even further on Thursday, reports Bloomberg. Bitcoin, along with the market’s biggest digital coins, dropped sharply after a report came out stating that Goldman Sachs Group Inc. is “pulling back on near-term plans to set up a cryptocurrency trading desk,” the article continues.

- Total market capitalization of all cryptocurrencies fell nearly $20 billion in a single hour on Wednesday, from $240 billion to $222 billion. Crypto leader bitcoin dipped below $7,000, while Ethereum extended its plunge below $300.

Opportunities

- Korea Post, a $112 billion money manager run by the same South Korean government that warned of the corruption of digital currencies, is trying to learn more about cryptocurrency and blockchain world from Goldman Sachs, reports Bloomberg. In fact, Korea Post’s President Kang Seong-ju recently met with incoming chief executive of Goldman, David Solomon, in New York. At the end of this month, Korea Post’s staff will meet with the crypto research team from Goldman as well in Hong Kong. The two groups will discuss digital assets, blockchain and related areas such as artificial intelligence, the article reads.

- One year after banning sales in initial coin offerings (ICOs), Beijing has continued to clamp down on domestic cryptocurrency activity over the last few weeks, reports CNBC. Chinese authorities in the month of August warned specifically about risks associated with illegal fundraising activities under the guise of “cryptocurrencies.” Despite the efforts to limit speculation on digital currencies, the Chinese government does support blockchain technology, investing around $3.57 billion since 2016, the article continues.

- Twitter is looking toward blockchain technology as a solution for its platform, reports Coindesk.com. Twitter CEO Jack Dorsey told a Congressional committee on Wednesday the following: “We need to start with the problems that we’re trying to solve and the problems we’re solving for our customers and look at all available technology in order to understand if it could help us accelerate or make those outcomes much better. Blockchain is one that I think has a lot of untapped potential, specifically around distributed trust and distributed enforcement potentially.”

Threats

- A long-time cryptocurrency advocate, ShapeShift CEO Erik Voorhees, is backpedaling on his initial vision for one of the best known platforms offering peer-to-peer trading, reports Bloomberg. In a blog post on Tuesday, Voorhees said that the cryptocurrency exchange is launching a membership program, which will require basic personal information to be collected, and will be mandatory soon. As the Bloomberg article points out, this move seems to be an “about-face” for the platform which Voorhees previously touted as the “exchange without accounts.”

- Wall Street Horizon, the leading provider of corporate event data, released its annual Corporate Event Research Survey on Wednesday. The key findings of this survey, which helps keep a pulse on the investment community, show that 55 percent of those polled believe that tracking corporate event data is crucial for monitoring stocks on their watch list. However, 50 percent of respondents said they are “not likely” to purchase data services to support cryptocurrency trading, despite the hype around this industry.

- Belgium’s top financial regulator, the Financial Services and Market Authority (FSMA), issued new warnings about cryptocurrency fraud, reports Coindesk.com. In an announcement published at the beginning of the week, FSMA declared that “cryptocurrencies are the hype of the year” and that “fraudsters are well aware of that, and try to attract customers online through fake cryptocurrencies and huge profits.”

Energy and Natural Resources Market

Strengths

- Coal was the best performing major commodity this week rising 2.7 percent. The commodity rallied after China Securities International analyst Snowy Yao said coal prices will likely enter a slow uptrend on import restrictions, tighter domestic supply and increasing demand from northern cities stockpiling for winter.

- The best performing sector this week was the Alerian MLP Index. The index dropped .05 percent, the least of any major resource sector attributable to its higher yield nature and lower beta exposure to drops in commodity prices.

- The best performing stock for the week was OCI N.V. The Dutch fertilizer company rose 3.8 percent after Berenberg analyst Rikin Patel raised its target price, “owing to increased assumptions for nitrogen fertilizer pricing in 2018 and beyond, along with a slight increase in our volume estimates.”

Weaknesses

- Gasoline was the worst performing commodity this week. The commodity dropped 7.80 percent after U.S. gasoline inventories built 1.85 million barrels against analysts’ expectations for a substantial drop in weekly inventories.

- The worst performing sector this week was the S&P/TSX Oil & Gas Exploration and Production Index. The index dropped 4.50 percent after crude oil prices dropped following a two-week advance.

- The worst performing stock for the week was Golden Agri-Resources Ltd. The Singaporean palm oil producer dropped 10.9 percent to a 52-week low after market data suggests soybean oil prices may drop, increasing competition for palm oil products.

Opportunities

- Just as looming sanctions on Iranian oil threaten to disrupt supplies from the Middle East, mega refineries in China are showing signs of a growing hunger for crude. Rongsheng Petrochemical Co. was said to be an active buyer of spot cargoes this month, the first such purchase by the company. The petrochemical producer is preparing for the start of its $24 billion, 400,000 barrel per day refinery in Zhejiang province this year.

- Commodities trading is finally bringing some relief for major investment banks. The combined income at 12 top banks including Goldman and JPMorgan jumped 38 percent to $2.1 billion in the first half of 2018, according to analytics firm Coalition. The year-on-year rebound is partly due to one-off gains in energy and industrial metals.

- The physical metals market continues to display strong demand dynamics. Shanghai copper stockpiles extended its drawdown, hitting the lowest level since November 2017, according to Bourse Data. Copper inventories dropped another 1.5 percent last week, with aluminum and nickel inventories dropping 1 and 10 percent respectively.

Threats

- Commodity ETFs suffer seventh week of outflows. Outflows from U.S.-listed commodity ETFs totaled $461 million in the week ended September 6, compared with withdrawals of $484 million in the previous period, according to data compiled by Bloomberg. Over the past seven weeks, outflows totaled $2.99 billion.

- Oil is poised for the biggest weekly decline since mid-July as a rout in emerging markets raises contagion fears. Developing-nation equities

slipped into a bear market, increasing concerns that the tumult could sap energy demand. - Gold futures erased gains and headed toward an eighth weekly loss in nine after hiring and wages in the U.S. accelerated last month, further eroding demand for the metal as a haven asset. Average hourly earnings increased 2.9 percent from a year earlier while the jobless rate was unchanged at 3.9 percent, still near the lowest since the 1960s. The figures add to the headwinds facing gold, which has posted five straight monthly losses as improving global economies and signs of inflation spur bets on tighter U.S. monetary policy.

China Region

Strengths

- Singapore’s official purchasing manager’s index (PMI) reading came in better than expected, climbing to 52.6 for the August measurement period from July’s 52.3 reading, better than expectations of 52.2.

- The Nikkei Indonesia Manufacturing PMI climbed to 51.9 in August from July’s reading of 50.5.

- The Nikkei Philippines Manufacturing PMI climbed to 51.9 for August, rising from last month’s reading of only 50.9.

Weaknesses

- The Caixin China Manufacturing PMI came in at 50.6, slightly behind expectations for a 50.7 reading and down from last month’s reading of 50.8. The Services reading missed by a larger margin, however, coming in at only 51.5, well shy of an anticipated 52.6 print and also down from July’s reading of 52.8.

- It was a fairly rough week if you were not the telecommunications sector in the Hang Seng Composite Index. Consumer services was the worst performer, declining 6.55 percent this week, with information technology and properties and construction down 5.67 and 4.23 percent respectively.

- The Nikkei Vietnam Manufacturing PMI declined to 53.7 in the August reading from July’s 54.9 print.

Opportunities

- U.S. integrated oil giant ExxonMobil this week announced an agreement to go ahead with a proposal for a multibillion-dollar petrochemical project and gas terminal in southern China, Bloomberg News reports. The article quotes Jefferies analyst Laban Yu as saying: “Through the Exxon deal, China wants to send a message to U.S. companies that the country is still open for business, regardless of what President Trump may do.”

- The leaders of North Korea and South Korea will attend an upcoming summit September 18-20, South Korea’s Yonhap News reports. Kim Jong-Un has also reportedly been invited by Russian President Vladimir Putin to a regional summit in Russia next week.

- China’s foreign reserves number, clocking in at around $3.11 trillion, remained relatively steady in the midst of broad fluctuations in global currencies and trade war escalation.

Threats

- Trade war concerns remain firmly positioned near front and center of risks and perceived risks to China region investors. President Trump announced Friday that he is ready to place tariffs on $267 billion in goods in addition to the $200 billion currently under consideration and on top of the tariffs already in place. The U.S. imported $505 billion in goods from China in 2017.

- Inflation in the Philippines continues, with the August consumer price index (CPI) reading—expected to come in at 5.9 percent—jumping up to 6.4 percent. While the peso did recover itself to some degree on Friday, the island-nation’s currency rose above 54 to new 52-week and multiyear highs (lows) earlier this week. Governor Nestor Espenilla promised “strong immediate action.”

- Investor concern over any broad slowdowns or emerging market foreign exchange risks could have outsized effects upon countries deemed to be at risk.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 59 basis points. Equities trading on the Istanbul exchange gained despite weaker economic data. The manufacturing PMI declined in August to 46.4 from 49.0 in July. Inflation jumped higher to 17.9 percent from 15.85 percent in July.

- The Turkish lira was the best relative performing currency this week, gaining 2.1 percent against the dollar. The lira appreciated on speculations that the central bank will hike rates next week.

- Industrial was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 5.7 percent. After the formal exit from the bailout program last month, Greece promised to stick with its reforms and keep a 3.5 percent primary budget surplus. There is, however, increased talk of populist policies ahead of elections next year.

- The Russian ruble was the worst performing currency this week, losing 3.5 percent against the dollar. The ruble sharply declined on Thursday as much as 1.6 percent against the dollar after Prime Minister Medvedev made a comment supporting dovish policy. Moreover, investors may be expecting additional sanctions after two Russian individuals were identified who attempted to murder Sergei and Yulia Skripal in the UK in March.

- Information technology was the worst performing sector among eastern European markets this week.

Opportunities

- The equity indexes of Hungary, Poland and the Czech Republic have outperformed the MSCI Emerging Market benchmark recently. Open economies in these central emerging Europe countries (CEE) and strong monetary policies are the main reasons of their resilience to the selloff in emerging markets globally. Moreover, these CEE countries have close trade ties with Western Europe, low unemployment and stable growth.

- The Wood & Company research team maintains a positive outlook on the Romanian stock market. The MSCI Romania offers attractive dividend yields of 8-9 percent local equities are attractively priced. The index trades at 19 percent below its five-year average on the 12-month forward price-to-earnings ratio. According to Wood & Company, Romania is on the verge of meeting the criteria to make the MSCI emerging market watch list. Another index provider, FTSE, has had Romania on the emerging market watch list since September 2016.

- Next week Russia and Turkey will announce their interest rate decisions. Turkey is expected to hike its one-week repo rate from 17.75 percent to 21 percent, while Russia is expected to leave its key rate unchanged at 7.25 percent. The European Central Bank meets next week and economists expect the rates to remain unchanged.

Threats

- The sharp depreciation of the lira is boosting prices in Turkey unexpectedly. The CPI in August was reported at 17.9 percent, versus 15.85 percent in July, with economists forecasting it slightly lower at 17.6 percent. The government is trying to support the lira without raising rates. New legislation forces exporters to repatriate their hard currency export earnings within six months and convert 80 percent of it into lira. There may be further weakness in the lira, especially if the central bank does not hike rates at their meeting next week.

- Renaissance Capital softened their growth forecast for Russia for next year to 1.4 percent, assuming sanctions remain unchanged and the price of oil is at $60 per barrel. The lower GDP forecast is mainly due to VAT increases and tighter credit conditions. Renaissance kept their 2018 GDP forecast relatively unchanged at 1.9 percent, versus their original forecast of 2 percent. They do expect growth to accelerate to 2.4 percent in 2020. Russian economic policy strongly prioritizes stability over growth, pushing for low inflation, fiscal discipline and reserves accumulation.

- German Chancellor Angela Merkel’s CSU Bavarian allies said on Wednesday that the European Central Bank should quickly terminate its asset purchase program and put an end to its low interest rate policy. Many view the end to the QE program and rate hikes as a threat to Europe’s growth prospects.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 2.94 | +0.08 | +2.76% |

| DJIA | 25,916.54 | -48.28 | -0.19% |

| Gold Futures | 1,201.80 | -4.90 | -0.41% |

| Hang Seng Composite Index | 3,653.96 | -130.58 | -3.45% |

| Korean KOSPI Index | 2,281.58 | -41.30 | -1.78% |

| Nasdaq | 7,902.54 | -207.00 | -2.55% |

| Natural Gas Futures | 2.78 | -0.14 | -4.80% |

| Oil Futures | 67.83 | -1.97 | -2.82% |

| Russell 2000 | 1,713.18 | -27.57 | -1.58% |

| S&P 500 | 2,871.68 | -29.84 | -1.03% |

| S&P Basic Materials | 369.51 | -2.09 | -0.56% |

| S&P Energy | 534.93 | -12.65 | -2.31% |

| S&P/TSX Global Gold Index | 152.72 | -4.60 | -2.92% |

| S&P/TSX VENTURE COMP IDX | 712.06 | -12.65 | -1.75% |

| XAU | 63.04 | -3.20 | -4.83% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 2.94 | -0.02 | -0.71% |

| DJIA | 25,916.54 | +332.79 | +1.30% |

| Gold Futures | 1,201.80 | -19.20 | -1.57% |

| Hang Seng Composite Index | 3,653.96 | -207.54 | -5.37% |

| Korean KOSPI Index | 2,281.58 | -19.87 | -0.86% |

| Nasdaq | 7,902.54 | +14.22 | +0.18% |

| Natural Gas Futures | 2.78 | -0.17 | -5.87% |

| Oil Futures | 67.83 | +0.89 | +1.33% |

| Russell 2000 | 1,713.18 | +26.30 | +1.56% |

| S&P 500 | 2,871.68 | +97.66 | +3.52% |

| S&P Basic Materials | 369.51 | -1.94 | -0.52% |

| S&P Energy | 534.93 | -22.72 | -4.07% |

| S&P/TSX Global Gold Index | 152.72 | -23.73 | -13.45% |

| S&P/TSX VENTURE COMP IDX | 712.06 | +13.24 | +1.89% |

| XAU | 63.04 | -11.35 | -15.26% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 2.94 | +0.02 | +0.65% |

| DJIA | 25,916.54 | +675.13 | +2.67% |

| Gold Futures | 1,201.80 | -113.30 | -8.62% |

| Hang Seng Composite Index | 3,653.96 | -703.52 | -16.15% |

| Korean KOSPI Index | 2,281.58 | -189.00 | -7.65% |

| Nasdaq | 7,902.54 | +267.47 | +3.50% |

| Natural Gas Futures | 2.78 | -0.15 | -5.26% |

| Oil Futures | 67.83 | +1.88 | +2.85% |

| Russell 2000 | 1,713.18 | +45.41 | +2.72% |

| S&P 500 | 2,871.68 | +101.31 | +3.66% |

| S&P Basic Materials | 369.51 | -9.14 | -2.41% |

| S&P Energy | 534.93 | -31.33 | -5.53% |

| S&P/TSX Global Gold Index | 152.72 | -36.83 | -19.43% |

| S&P/TSX VENTURE COMP IDX | 712.06 | -63.51 | -8.19% |

| XAU | 63.04 | -19.95 | -24.04% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2018):

Coeur Mining

Goldcorp Inc

Broadcom Inc

The Home Depot Inc.

Exxon Mobil Corp

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the i

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All