Investing for the Long Term: A Conversation with Marc Lichtenfeld

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Before sharing with you my interview with Marc Lichtenfeld, chief income strategist at the Oxford Club, I think a mea cupla is in order. When President Donald Trump began imposing tariffs on China and other U.S. trading partners, I believed it would have a negligible impact on metal prices. The main reason why I thought this was because I assumed the tariffs would be very short-lived and that negotiations would be swift. Clearly I underestimated the effects of Trump and his economic advisor Larry Kudlow’s China bashing. As you can see above, the tariffs and rhetoric have been a strong headwind for copper, which has long been seen as a barometer of the global economy. This could mean further weakening for a handful of other metals and commodities. Zinc, for instance, has been badly hammered.

Trump’s selection of Kudlow as economic advisor, I believe, has only helped aggravate the rhetoric between the U.S. and the world’s second largest economy. In March, when Kudlow was appointed, I described what I’ve viewed for many years as his bias toward gold and China. Remember, it’s not the political party as it is the politics that investors should care about.

The trade war has also turned up in the U.S. Global Sentiment Indicator, which recently dropped to the 20 percent level, indicating that markets are oversold. Investors appear to be concerned.

It’s not just investors, though. The University of Michigan announced today that its consumer sentiment index dropped to an 11-month low in August.

Ramifications of the trade war are showing up across the board. It’s important to remain diversified in short-term government and municipal bonds, and to think long-term, while we wait for a potential short-term rally.

My good friend Marc Lichtenfeld from the Oxford Club has always been savvy in following such strategies. I invite you to learn from his investment journey in this special Q&A.

What inspired you to get into the financial world?

|

When I was in college, I had no interest in the stock market or finance. I wanted to be a sportscaster. It wasn’t until after I graduated that I started to invest for myself, and I became kind of obsessed with it. This was before the internet, so I would spend Saturday afternoons in the library researching companies and learning everything I could.

I eventually decided to make my hobby my profession, but nobody was interested in hiring a 20-something kid with no relevant experience.

I decided to visit a trading firm right down the street from my house that I knew was looking for a trading assistant. When I walked in and handed them my resume, I got the impression that I wouldn’t be getting a call back. I could see, though, that they desperately needed help entering orders and balancing their books, so I made the guy an offer he couldn’t refuse. I told him I’d work for free for a week, and if he wasn’t happy with what he saw, he could tell me no thanks. But by the end of the week, he told me to come back on Monday and that he’d start paying me.

That was my entry into the world of finance. From there, I had a couple of other positions, including as a sell-side analyst at Avalon Research Group, and then in 2007 I joined the Oxford Club, where I’ve been ever since.

Tell us about your start with Oxford Club and how the group has contributed to your professional development.

|

One of the things I admire most about the Oxford Club is its emphasis on individual investors. It really tries to teach investors how to grow their wealth the right way by managing risk and investing in quality companies.

I began there by writing about biotech, which even now I believe is an industry of the future. A few years later, I spoke with Julia Guth, our CEO and publisher, about taking over the dividend newsletter, and in 2013 I launched my own dividend newsletter, the Oxford Income Letter.

My main focus since then has been on dividend growth companies. Around the same time that we launched the Oxford Income Letter, I wrote a book called Get Rich with Dividends. The strategy I describe is one that’s worked for many years. When you invest in companies that are raising their dividends 5 percent, 8 percent, 10 percent a year, you vastly improve your odds of generating some impressive returns and beating the market year after year. If you’re still in the wealth-building phase, it’s also important to reinvest the dividends because then the compounding machine just goes into overdrive.

This can really make a significant difference in the size of your portfolio and change your life down the road. It’s one of the many reasons why I started my kids investing in dividend growth companies. If they started as children, they could be in a very good position 30 years from now when they’re looking to buy a house or send their own kids to college.

Sticking with that strategy sometimes requires a lot of discipline.

I was actually having a conversation with my brother recently because he’s looking to put some money to work and wanted to get my thoughts. He’s a bit of a worrier, though, so I reminded him that if he’s going to invest, he really needs to be disciplined and not freak out if the market takes a downturn in, say, three years. What’s far more important is where the market will be 10 years from now. Historically, the market is up 10 years down the road—it’s very rare that it’s not—but you need to have the discipline to stay with it.

The important takeaway here is to know your tolerance for risk and adjust your investments accordingly. My brother’s very cautious, so he probably shouldn’t put every dollar in the market if he’s going to lose sleep over a correction and sell at the wrong time.

It’s easier for those who’ve seen the data and know that the market has historically been up in 10 years, even if we’re at the top of the business cycle. In Get Rich with Dividends, I talk about the only times when markets have been down over a 10-year period, and those are in the middle of the Great Depression and in 2008-2009 during the Great Recession. You would literally need to cash out in the middle of a historic downturn not to make money over 10 years, and that’s if you sold right at the bottom. If you had waited another year or two, you might have come out at least breaking even, if not better.

Who were your mentors early on?

My biggest mentor was David Hines. David was my research director at Avalon, which had the reputation of being the most contrarian research firm on Wall Street. We initiated ratings on stocks only if that rating was going to be contrarian. If we were bullish on energy and so was the rest of the Street, there was no reason for us to publish our research. Why would anyone listen to us versus Goldman Sachs or Morgan Stanley?

In any case, I thought I was contrarian—until I met David. Any time I came to him with my research, he would just poke so many holes in it. It made me double and triple-check that all my i’s were dotted and t’s were crossed before presenting an argument to him.

What book do you think every investor should read?

I would say The Richest Man in Babylon, by George Clason. It’s 70 or 80 pages, so you could read it in an afternoon. The book, which is about 100 years old now, is filled with great life lessons on money management and saving and investing. I would recommend it especially to someone who has a teenager or young adult in their life, and they want to impart some important lessons.

On the more technical side, I would recommend David Dreman’s Contrarian Investment Strategies. He’s considered to be the father of contrarian investing. The book is pretty data-rich, but if you like that kind of thing, it really makes a strong argument for contrarian investing.

In one of your recent presentations, which I attended, you explained that cash flow is more important than earnings. Can you elaborate on that?

There’s no doubt earnings are important. Stock prices tend to follow earnings over the longer term, but earnings can easily be doctored and manipulated. Let’s say a company records a sale of $1 million on December 30. Even if it hasn’t been paid yet, it can still include that sale as part of its revenue for the fiscal year, depending on the industry. The $1 million means nothing, then, in terms of its ability to pay bills and dividends and meet payroll.

Cash flow can tell a truer story because it excludes all the non-cash items and adjusts for accounts receivable. It represents only the cash that has come into a business during the year, and it gives you a better idea of a company’s ability to pay the bills. In the above example, cash flow would show you that the $1 million hasn’t come in yet. Also, if there’s fraud going on, oftentimes cash flow is where you’ll be able to detect it. If earnings are constantly going straight up and cash flow is not following it, this might raise some red flags.

Now, I want to caution, this doesn’t always mean fraud is taking place if earnings rise for a year or two and cash flow doesn’t follow. But if you see a trend of rising earnings but deteriorating cash flow, then you might want to start asking some questions.

So what’s your outlook for the rest of 2018?

We don’t try to time the market at the Oxford Club. Rather, we focus on trying to find great opportunities—stocks that are undervalued or that we expect to go up because of momentum or fundamentals—and manage risk.

Having said that, I don’t see any reason to expect a market correction at this point. The market has so far shrugged everything off—trade wars, outrageous presidential tweets, higher interest rates and more. It seems the market wants to keep going higher, so we’re going to continue to try to ride it higher, too.

Interested in reading more interviews with the world’s top market experts? Subscribe to my award winning CEO blog, Frank Talk, by clicking here!

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 1.41 percent. The S&P 500 Stock Index rose 0.59 percent, while the Nasdaq Composite fell 0.29 percent. The Russell 2000 small capitalization index gained 0.36 percent this week.

- The Hang Seng Composite fell 5.19 percent this week; while Taiwan was down 2.67 percent and the KOSPI fell 1.57 percent.

- The 10-year Treasury bond yield remained essentially flat at 2.87 percent.

Domestic Equity Market

Strengths

- Telecommunications was the best performing sector of the week, increasing by 3.65 percent compared to an overall increase of 0.62 percent for the S&P 500 Index.

- Nielsen Holdings was the best performing stock for the week, increasing 19.03 percent.

- Nordstrom’s second-quarter earnings and sales beat analysts' estimates, and the retailer raised its fiscal-year guidance. The stock jumped more than 9 percent on Friday.

Weaknesses

- Energy was the worst performing sector for the week, decreasing 3.59 percent.

- Baker Hughes was the worst performing stock for the week, falling 10.76 percent.

- J.C. Penney tumbled to an all-time low. Shares fell more than 27 percent on Thursday to a record low of $1.75 apiece after the retailer missed Wall Street estimates for the second quarter and slashed its guidance.

Opportunities

- Apple could launch smart glasses in 2020 and an Apple Car in 2023, according to an analyst with a strong track record on the company. Respected TF Securities analyst Ming-Chi Kuo suggested the new services could take Apple's valuation to $2 trillion.

- Goldman Sachs is advising Elon Musk on his plans to take Tesla private. The bank confirmed on Wednesday that it is suspending research coverage of Tesla because it is "acting as a financial advisor" to the car company.

- Warren Buffett's Berkshire Hathaway now has a $3 billion stake in Goldman Sachs. The Buffett-led conglomerate raised its stake in the Wall Street bank by 21 percent to 13.2 million shares during the second quarter, according to a 13F filing out Tuesday.

Threats

- Jeremy Grantham, the cofounder and chief investment strategist at the $71 billion Grantham Mayo Van Otterloo & Co., told Business Insider’s Joe Ciolli that earlier this year he was convinced a severe stock-market bubble burst was coming—until President Donald Trump's trade war injected skepticism into the market. Nonetheless, he thinks considerable pain for investors is still in store.

- Nvidia cut its guidance. The chipmaker said Thursday that it booked third-quarter revenue of about $3.25 billion, down from its previous estimate of $3.34 billion, sending shares lower by about 6 percent in after-hours trading.

- MoviePass has less than three months left before it runs out of cash. The company burned through more than $219 million in the first six months of the year, and said it now has $26 million in cash on hand and another $25.4 million on deposit at its merchant bank.

The Economy and Bond Market

Strengths

- The U.S. economy grew stronger this summer and is likely to expand steadily in the months ahead, according to an index that measures the nation’s economic health. The Conference Board report on Friday showed that the leading economic index rose 0.6 percent in July after a 0.5 percent gain in June. Measures of economic health that look ahead, such as business orders, were particularly strong in the month of July.

- U.S. retail sales rose by more than forecasted in July, extending solid consumer-spending gains to the start of the third quarter. The value of overall sales advanced 0.5 percent in July, Commerce Department figures showed on Wednesday. The median forecast of economists surveyed by Bloomberg called for a 0.1 percent gain. The data suggests that consumer spending is continuing to drive the economy early in the quarter.

- The Empire State manufacturing index rose to 25.6 in August, the highest level in 10 months, the New York Fed said this week. Economists expected a reading of 20, according to a survey by Econoday.

Weaknesses

- The University of Michigan reported its consumer sentiment index in August fell to 95.3, the lowest level in 11 months. Economists polled by MarketWatch expected a higher reading of 98.5. Buying conditions for large household durables, which include items such as furniture, cars and appliances, sank to the lowest level in nearly four years, the University of Michigan said.

- Home construction across the U.S. was weaker than Wall Street had expected, with many analysts taking a bleak view of the housing market. Housing starts grew 0.9 percent in July from the prior month, significantly weaker than the 8.3 percent bounce back economists surveyed by The Wall Street Journal had expected. This follows a sharp 12.9 percent drop in housing construction in June, the largest monthly decline since the end of 2016.

- U.S. industry output rose slowly in July, held down by weakness in the mining and utilities sectors. Industrial production inched up a seasonally adjusted 0.1 percent in July from the prior month, the Federal Reserve said Wednesday. Economists surveyed by The Wall Street Journal had expected the index to rise 0.3 percent. Output in the volatile mining sector declined 0.3 percent in July. Utility output also dropped from the prior month.

Opportunities

- Sliding commodity prices – copper and zinc are in bear markets and crude oil is in a correction – are likely to weigh further on market expectations of inflation. The five-year U.S. break-even rate, a gauge of price prospects, fell to a six-month low on Wednesday. The market is pricing in a slowdown in economic activity and inflation, potentially due to hawkish Federal Reserve monetary policy, according to Bloomberg Intelligence chief U.S. interest rate strategist Ira Jersey. A material slowdown in inflation would likely ease pressure on bond yields, boosting bond prices.

- In terms of U.S. data releases, the most noteworthy next week is durable goods orders for July. These are expected to give an indication on business spending in the third quarter. Durable goods are anticipated to have grown by 0.8 percent on a monthly basis in July, the same pace of growth as in June.

- GDP models are giving divergent views on the U.S. economy’s performance in the third quarter. The Atlanta Fed’s GDPNow model continues to predict continued strong growth from the second quarter, forecasting growth of 4.3 percent on an annualized basis, while the New York Fed’s tracker suggests a 2.6 percent rate. Friday’s prints will better inform markets on the state of the economy during the third quarter.

Threats

- The Fed minutes from the July 31 to August 1 meeting, which will be released next Wednesday, will give an indication on whether global tariff tensions or the Turkish lira debacle are posing concerns to the Fed’s economic outlook.

- July’s existing and new home sales data, released next week Wednesday and Thursday, respectively, will shed a light on whether the slowdown in housing is cementing in place.

- Next week the risk event Jackson Hole Economy Policy Symposium is taking place. The summit’s overall theme is “Changing Market Structure and Implications for Monetary Policy” and will feature influential central bankers and finance ministers from some of the world’s largest economies. Market-sensitive remarks coming out of the conference should not be ruled out.

Gold Market

This week spot gold closed at $1,185.05 down $26.65 per ounce, or 2.20 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 9.46 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index came in off just 2.27 percent. The U.S. Trade-Weighted Dollar reversed course this week and fell 0.25 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Aug-13 | China Retail Sales YoY | 9.1% | 8.8% | 9.0% |

| Aug-14 | Germany CPI YoY | 2.0% | 2.0% | 2.0% |

| Aug-14 | Germany ZEW Survey Current Situation | 72.1 | 72.6 | 72.4 |

| Aug-14 | Germany ZEW Survey Expectations | -21.3 | -13.7 | -24.7 |

| Aug-16 | Initial Jobless Claims | 215k | 212k | 214k |

| Aug-16 | Housing Starts | 1264k | 1168k | 1158k |

| Aug-17 | Eurozone CPI Core YoY | 1.1% | 1.1% | 1.1% |

| Aug-23 | Initial Jobless Claims | 215k | -- | 212k |

| Aug-23 | New Home Sales | 650k | -- | 631k |

| Aug-24 | Durable Goods Orders | -0.8% | -- | 0.8% |

Strengths

- The best performing metal this week was palladium, up 0.52 percent after rallying hard after a six percent drop mid-week, largely on talk of trade tensions easing. Inflation is creeping into the market, which has historically been positive for the price of gold. U.S. consumer sentiment fell to the lowest level in almost a year, according to a University of Michigan report. Bloomberg writes that this could be a possible caution signal for spending following strong gains in the second quarter. The report also showed that buying conditions for large household durable goods fell to the lowest in four years, car-buying views were the lowest since 2013 and home-buying conditions are the least favorable in about a decade. Another sign of inflation is in Deere & Co.’s lower earnings due to higher freight and raw material costs. Steel prices are rising due to tariffs on imports and freight costs are up due to higher oil prices and a shortage of big-rig drivers. Bloomberg writes that “cost inflation is marring what is proving to be a strong uptick in demand for agricultural-machinery.”

- Hedge-fund manager Ray Dalio has kept his faith in the two biggest ETFs backed by gold, even as other investors have backed away, reports Bloomberg. As of the end of the second quarter, Dalio’s Bridgewater Associates had 3.9 million shares in SPDR Gold Shares and 11.3 million in the iShares Gold Trust, according to regulatory filings. Ten-year real yields are down 10 basis points since the start of the month which likely helps to stall the dollar. A stronger dollar has kept investors away from gold, which may no longer viewed as the traditional safe-haven asset. However, Rick Rule, chief executive officer of Sprott U.S. Holdings Inc. doesn’t think this trend will last. Rule said that U.S. investors “will begin to diversify their risk-off trade to include, among other things, gold” after they shift focus away from the U.S. dollar relative to other currencies.

- The first bullion-backed ETF guaranteed by a government has launched on the New York Stock Exchange. Australia’s Perth Mint Physical Gold ETF (AAAU) started trading on Wednesday and allows shareholders to exchange their shares for gold and have the physical metal delivered to their doorstep by Perth Mint. Richard Hayes, the Perth Mint’s chief executive officer, said that “we believe investors will have greater confidence with the knowledge that their wealth is physically stored in one of the most secure central bank grade vaults in the southern hemisphere.”

Weaknesses

- The worst performing metal this week was platinum, down 4.83 percent as speculators increased their bearish position. The yellow metal continues to decline as gold prices fell below $1,200 per ounce this week. Gold is heading for its fifth monthly loss as the dollar continues to climb, for the worst run since 2013, writes Bloomberg. Gold traders and analysts have a bearish outlook in this week’s Bloomberg survey as the gold price sank to its lowest in more than 19 months.

- Money managers are making their biggest bets that prices will decline even further as investors are exiting gold ETFs and open interest for futures is dropping. Gold mining stocks are also falling as an index of bullion-mining companies tracked by Bloomberg Intelligence fell to the lowest in more than two years for a seventh straight loss on Tuesday. This week was the fourth straight week of commodity ETF outflows. Outflows from U.S.-listed commodity ETFs totaled $694 this week compared to withdrawals of $538 the week prior, according to Bloomberg data. Precious metals funds saw outflows of $495, compared with $399 of outflows the previous week.

- South Africa’s gold mining industry continues to weaken as the nation’s production fell for a ninth consecutive month. Gold Fields Ltd, which owns the world’s second-biggest known body of gold-bearing ore, the South Deep mine in South Africa, continues to face trouble. The South Deep mine has the potential to produce for 70-years, however the project loses around $7 million per month due to high costs and low volumes of output. The company has said it might cut 1,560 employees and contractors at the operation, reports Bloomberg. South African gold producers are also facing labor strikes from workers who are demanding pay raises. In talks this week, the labor unions rejected pay increases from four producers.

Opportunities

- Several miners posted positive drill results this week at various projects. Barsele Minerals Corp. reported results of 4.12 grams per ton of gold at 27 meters at their Swedish project. Pure Gold Mining Inc. reported surface drilling results at their Madsen Gold Project in Ontario of 32.9 grams per ton over 1.7 meters, 14.5 grams per ton over 1.5 meters, 12.7 grams per ton over 1.7 and more. Lastly, Novo Resources Corp. has announced the continuity of an upper gold-bearing conglomerate from the Comet Well to Purdy’s Reward.

- Jaguar Mining fell by 25 percent on Wednesday after releasing news production guidance was being reduced for the year and that Rodney Lamond is leaving his position as chief executive officer and director. This will be the third CEO that the Board of Directors at Jaguar has chewed through in two years. As a CEO, Rodney probably spent more time in country at the mine site trying to orchestrate a turnaround than most CEOs in the mining industry. Rodney previously was instrumental in the turnaround of Crocodile Gold which became Newmarket Gold and was later taken out by Kirkland Lake Gold. According to Bloomberg, Rodney owned a little more than 2.1 million shares in Jaguar (0.65 percent of outstanding shares), almost 6 times more shares than the Chairman of the Board, Richard Douglas Falconer. As a shareholder of Jaguar, the problem in our opinion is not Rodney, but is the Board of Jaguar. According to Glass Lewis & Co., a proxy rating service, the Jaguar Board cannot even keep attendance records of who attended what corporate governance meeting in the last year. The Board of Jaguar mining will now need to be reminded of whom the owners of Jaguar mining really are and how we expect the company to be run. The Chairman, Richard Douglas Falconer will have to be replaced, among others and therein will be the opportunity.

- Shares of Canyon Resources Ltd. are up 100 percent in two weeks after the company was granted exploration permits for a bauxite project in Cameroon. This is a world class ore body where the previous owner defined a large high-grade and low impurity bauxite deposit of 550 million tonnes averaging 45.5 percent bauxite and only 2 percent silica. Canyon managing director Phillip Gallagher noted the deposit is adjacent to rail with suitable access to port infrastructure. Also, that only about 40 percent of the prospect has so far been tested within the permit area and he expects the resource can be expanded.

Threats

- UBS writes that gold will continue to be under pressure and sees $1,125 as a strong support level for the yellow metal, which is still well below the current price. Gold sank to its lowest level in more than 19 months this week, even as global equities came under pressure, writes Bloomberg. Richard Hayes, the chief executive officer of Australia’s Perth Mint, said that investors have grown immune to economic and geopolitical risks, such as trade wars and the Turkish lira, which would normally drive safe-haven demand for gold. Hayes said “The world, to some degree, has been quite used to bad news,” which has been the reason behind gold’s months-long slump.

- Goldman Sachs wrote this week that there is no serious risk of a recession due to the flattening of the yield curve. The bank said that three out of the last 10 times the yield slope inverted, there was no recession over the following two-year period. However, seven of those 10 times there was a recession. Seventy percent of the time we get a recession? Not too comforting, Goldman.

- Companies are expected to be bringing back to the U.S. $1.5 trillion in corporate cash due to the tax overhaul passed last year, with $400 billion already repatriated, according to Invesco estimates. Bloomberg writes that the new tax law sets a one-time repatriation rate for untaxed cash held abroad – a 15.5 percent charge on cash and liquid assets which can be paid for over eight years. Previously these funds were hit with a 35 percent corporate tax. This could lead to further strengthening of the U.S. dollar if those proceeds are not already held in U.S. dollars overseas. The knock on effect could be tough for some companies. Cisco Systems pulled $5 billion from Deutsche Bank’s asset management arm. This amounted 40 percent of their redemptions in the first half of the year.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended August 17 was TaTaTu, which gained 203.35 percent.

- According to Ethereum’s co-founder Joseph Lubin, this isn’t the first rodeo for cryptocurrencies and supporters of the industry, Seeking Alpha reports. In a recent interview, Lubin explains that there have been six price bubbles and subsequent collapses over the years, with each one more astonishing than the last. “Trader types are behind these big prices changes, but developers are keeping their heads down creating the infrastructure needed to make crypto truly useable and scalable,” he said. Lubin promises, “big things are coming.”

- Ethereum classic (ETC) became listed on the Coinbase exchange on Thursday evening. The coin jumped 15 percent ahead of the listing and rose earlier this month when it was introduced on Coinbase Pro, a platform for more experienced traders. The exchange wrote that “the spike in ETC looks sustainable as it is backed by a pick-up in trading volumes.”

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended August 17 was Wild Crypto, which lost 68.80 percent. This month’s sell-off in cryptocurrencies has showed few signs of letting up. The total market capitalization of virtual currencies has dropped to $193 billion, down from around $835 billion in January, reports Bloomberg.

- Ether fell over 10 percent on Monday to around $286, after topping $1,000 in February, reports Seeking Alpha. Blockchain Capital’s Spencer Bogart said “investors are increasingly disillusioned with tokens and ICOs, most which have been launched on top of Ethereum, and we’re seeing this play out in the market with continued downward price pressure.” The underperformance of altcoins, led by Ethereum, continued mid-week, reports MarketWatch.

- The meltdown in Turkey has propelled the nation’s currency downward since last week, reports Bloomberg. In fact, the Turkish lira is looking nearly as volatile as the price of Bitcoin at the moment, the article continues. Looking at the chart below makes one question which line represents a national currency?

Opportunities

- The Winklevoss twins aren’t letting the second rejection from the Securities Exchange Commission (SEC) for their Bitcoin-based ETF deter their efforts, reports Bloomberg. Even though many large Wall Street investors aren’t on board with crypto quite yet, the brothers claim that they will continue to grow their business, Gemini Trust Co., by focusing on adding cryptocurrencies to the retail side. The two also submitted a proposal in March to create the Virtual Commodity Association, which is a “self-regulatory organization that would police digital-currency markets and custodians,” the article continues.

- CBOE Global Markets Inc. is racing toward the moving finish line for the first bitcoin ETF, writes Bloomberg, despite the amount of work needed to win approval from the SEC. “As we chip away at their issues to make them less concerned, at some point they’ll be comfortable with an ETF,” said Chris Concannon, the exchange operator’s president and chief operating officer.

- The world’s biggest producer of cryptocurrency mining chips, Bitmain Technologies, is planning a Hong Kong initial public offering (IPO), reports Bloomberg. People with knowledge of the matter estimate the IPO to raise as much as $3 billion. Bitmain’s 32-year-old co-founder Jihan Wu plans to file a listing application as early as September. “A successful listing would be a landmark event for the crypto industry, which is increasingly trying to move from the fringes of finance into the mainstream,” the article continues.

Threats

- Many hedge funds that have invested billions into the cryptocurrency space aren’t sure if they are calculating their taxes correctly, reports Bloomberg. This could prove to be a real issue, the article continues, particularly since the Internal Revenue Service (IRS) announced in July that virtual currencies would be a focus of audits for its large business and international division. A key cause of concern stems from how regulators share conflicting views on how they should be defined – the IRS considers them to be property, while the Commodity Futures Trading Commission says they’re commodities.

- Nearly one-third of U.K. businesses said they have been hit by cryptocurrency mining malware within the previous month, writes Coindesk.com. According to a recent survey published by Citrix, “almost 60 percent of responding companies further indicated they had found mining malware on their systems at some time in the past, with the vast majority of those instances (around 80 percent) being in the last six months.”

- Coindesk reports that on Tuesday it was unveiled that the Foreshadow vulnerability impacts all Intel’s Software Guard Extensions (SGX) enclaves, which is a specialized secure chip used for storing sensitive data. The enclave was designed to be tamper-proof, however researchers found a way for an attacker to steal the stored information. This has negative effects on the cryptocurrency space as many crypto projects had planned to use this technology and will need to restructure before launching.

Energy and Natural Resources Market

Strengths

- Lumber was the best performing major commodity this week rising 13.9 percent. The commodity rallied after wildfires sweeping across British Columbia, the world’s biggest exporter of softwood lumber, have sparked concerns of supply restrictions.

- The best performing sector this week was the S&P 1500 Paper & Forest Index. The index rose 2.9 percent tracking a sharp recovery in lumber prices resulting from wildfires sweeping across British Columbia.

- The best performing stock for the week was Interfor Corp. The Canadian timber producer rose 9.4 percent, posting its second weekly advance after six weeks of losses as wildfires supported a rally in lumber prices and associated equities.

Weaknesses

- Zinc was the worst performing commodity this week. The commodity dropped 7.9 percent posting its worst weekly loss since 2016 amid investor concerns that a rising dollar and turmoil in emerging markets may scuttle demand, while an index of miners tracked by Bloomberg Intelligence is poised for the biggest weekly loss since February.

- The worst performing sector this week was the NYSE Arca Gold Miners Index. The index dropped 9.3 percent in what was the worst week for precious metals in more than a year. With the dollar appreciating amid Turkey’s financial crisis and trade tensions, bullion dropped below the psychological support level of $1,200 an ounce this week.

- The worst performing stock for the week was Antofagasta PLC. The Chilean base metals producer dropped 14.1 percent to a 52-week low after the company reported operating costs rose due to lower production and higher input prices.

Opportunities

- A Chinese delegation led by Vice Minister of Commerce Wang Shouwen will meet U.S. representatives in Washington next week. The trade-focused meeting among the world’s two largest economies may facilitate a solution that avoids the proposed date of August 23, 2018 as the day in which each economy is due to slap multi-billion dollar tariffs on one another.

- Gold will fight back the U.S. dollar for safe-haven status, according to Sprott Inc. A gold rebound may stop the ascent of the U.S. dollar, which could lead to a commodity rebound in the weeks and months ahead. Bullion has slumped to the lowest since January 2017 and is set for a fifth month of losses as investors flee to the dollar amid trade tensions. Sprott Inc., added that the greenback’s strength is relative, not absolute, and the overwhelming faith that the global saver has placed in the U.S. currency is “probably partly misplaced.”

- China nearly quadrupled the value of fixed-asset investment projects approved in July as Beijing looks to accelerate infrastructure spending to boost the cooling economy. China gave the greenlight to 17 fixed-asset investment projects in July, worth a combined 77.69 billion yuan ($11.24 billion) among other support measures for businesses to cushion the economy as it braces for the impact of escalating U.S. trade tariffs.

Threats

- The oil market is facing an unexpected demand slowdown. Emerging markets are expected to contribute 1 million barrels a day of additional oil demand this year, about three quarters of total global growth, according to the International Energy Agency. However, many of those countries are also the epicenters of recent economic tumult with currency crises across a number of critical emerging markets making crude imports and energy costs unsustainable for industries.

- Metal demand fears persist as the trade war agenda takes over. Base metals came under further pressure after a short-lived relief rally. Zinc paced declines as it headed for its worst weekly loss in seven years, amid investor concerns that a rising dollar and turmoil in emerging markets may hurt demand, adding to losses even after China and U.S. agreed to restart trade talks later this month. Steelmakers struggled, despite rebar futures hitting new highs, while aluminum prices continued to lose some shine.

- The canary in the coal mine is sending messages about global economic growth. South Korea, a key bellwether in global economic matters posted the weakest jobs growth in nearly nine years in July, adding to pressure on President Moon Jae-in to do more to boost economic growth and abandon policies focused on raising wages and improving income distribution.

China Region

Strengths

- Vietnam’s Ho Chi Minh Stock Index gained 8 basis points in total return amid a red week for the region, with Thailand’s SET Index and India’s NIFTY and SENSEX indices falling less than one percent.

- West China Cement Ltd. (2233 HK) was the top-performing stock in the Hang Seng Composite Index (HSCI) over the last five trading days, rising 12.12 percent in that time.

- Telecom was the strongest sector in the HSCI this week, hanging in there and rising 54 basis points in a red week for the index.

Weaknesses

- Malaysia’s year-over-year GDP print for the second quarter came in at only 4.5 percent, shy of expectations for a 5.2 percent print and down from the prior quarter’s 5.4 percent reading.

- China’s industrial production rose only 6.0 percent year-over-year for the July measurement period, shy of expectations for a 6.3 percent gain, while retail sales clocked in at only 8.8 percent over the same time frame versus analysts’ anticipated showing of a 9.1 percent pace.

- China’s Fixed Assets Investment (FAI) also missed expectations, coming in at only 5.5 percent, well short of the 6.0 percent economists anticipated and down from the prior reading of 6.0 percent in June.

Opportunities

- Bitmain Technologies Ltd., which is the world’s biggest producer of cryptocurrency mining chips, is reportedly planning a Hong Kong initial public offering, according to Bloomberg News, that could raise as much as $3 billion. The Beijing-based company could file a listing application as early as September and the effort, which could mark yet another major technology listing for Hong Kong, may also serve as something of a test of investor sentiment toward the digital-currency scene.

- New home prices rose at the fastest pace in 22 months as China’s property market remained steady of late. Home prices rose faster in smaller, so-called third-tier cities (up 1.2 percent month-over-month) and second-tier cities (up 1.4 percent month-over-month) than in the largest metropolises, which rose 0.3 percent. The pace of gain overall of 1.2 percent is up slightly from last month’s pace of 1.1 percent.

- Indonesia announced it will boost spending next year to help economy, which it expects to grow at a 5.3 percent pace in 2019, even as the budget deficit is expected to shrink down to 1.8 percent of GDP.

Threats

- Trade wars real, perceived, and/or both remain a concern for both global and China-region investors.

- It’s earnings season in Hong Kong, and investors are watching carefully as some major leaders of the last run up (think technology, for example, or juggernaut Tencent [700 HK] as a specific stock) have reported numbers that missed expectations.

- The Philippines’ central bank Governor Nestor Espenilla highlighted the “extraordinary volatile” nature of financial markets this year, and Bloomberg reported on the suggestion that the country’s Financial Stability Coordination Council sees increased swings as rates become more volatile. Governor Espenilla pointed out, though, that he believes the country has plenty of buffer against any broader emerging markets concerns brought on by fluctuation or fallout in the Turkish lira.

Emerging Europe

Strengths

- Hungary was the best performing country this week, gaining 73 basis points.

- The Turkish lira was the best performing currency this week, up 6.61 percent against the U.S. dollar. The currency recovered after the finance minister announced Turkey would not impose capital controls to support the battered lira.

- Real estate was the best performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst performing country this week, losing 6.54 percent. Turkey adjusted its policies to make it harder to short the lira. Additionally, Qatar signaled it would invest $15 billion in Turkey. However, Turkey’s finance minister did not offer any concrete proposals to address its fundamental problems: high inflation, heavy reliance on external borrowing, and lack of credible and independent economic policies. Nearly three-quarters of its current account deficit, for example, is energy and the cost has surged in lira terms. Without corrective policy, domestic demand will suffer, and inflation will rise.

- The Czech koruna was the worst performing currency this week relative to the other currencies in the region, gaining only 6 basis points against the dollar.

- Telecommunications was the worst performing sector among eastern European markets this week.

Opportunities

- The ZEW survey of investor expectations came in at negative 13.7, beating consensus for negative 21.3. A jump in investor confidence hints at less gloomy prospects for the second half of the year. German financial professionals were more optimistic than expected in August, but the key indicator remained in negative territory amid international trade tensions.

- The euro-area economy grew faster in the second quarter than initially reported, suggesting some of the worries about the outlook at the start of the year may have been overdone. The second-quarter GDP was revised up to 0.4 percent from 0.3 percent.

- U.K. retail sales bounced back strongly in July as warmer weather and extended discounts at stores encouraged shoppers to open their wallets. Sales gained 0.7 percent from June, compared with a median estimate of a 0.2 percent gain in a Bloomberg survey.

Threats

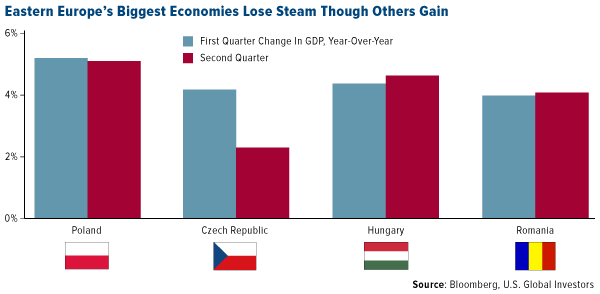

- Growth in Eastern Europe’s biggest economies probably slowed in the second quarter as the region began to feel the effect of trade tensions sparked by U.S. President Donald Trump. Second-quarter growth dipped from a peak at the start of the year in Poland and the Czech Republic, the region’s two biggest economies, data released Tuesday showed. Hungary, Romania and Slovakia managed slightly higher expansions. A slowdown in the euro area, the main export market, is partly to blame, along with higher borrowing costs.

- The recently proposed tax increases on Russian metals and mining companies have sent shockwaves across the market, although greater regulatory uncertainty could also widen the discount applied by the market. According to Rencap analyst Dan Salter, a targeted tax increase on profitable companies would risk undermining the work the government has done to date in keeping taxes stable, visible and predictable. It also risks incentivizing companies to show lower profitability (to avoid being targeted) and making them unwilling to invest given a less predictable tax environment. If that happens, it would confirm the view of many investors that Russia is a great fixed income story (fiscal discipline, floating currency, inflation targeting) but a less clear equity story.

- The EU’s trade surplus with the U.S. widened to almost 67 billion euros ($76 billion) in the first half of 2018, according to new figures from Eurostat. President Donald Trump, who says the EU has been “terrible” to the U.S on trade, slapped tariffs on European steel and aluminum this year, prompting retaliatory levies. While there is since been a truce, the growing surplus could harden U.S. attitudes in any negotiations toward a transatlantic accord.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All