The Death of a Wholesaler

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

The traditional wholesaler is dying. The future of wholesaling will combine analytics and portfolio construction.

Here’s how a typical wholesaler, Robin, will drive business a decade from now.

It’s 2020 and Robin logs into the CRM and views 15 new leads from last night. The company just launched its latest digital portal that helps HNW clients and advisors to visualize the risk in their current products. Robin looks at the portfolios and logs into the firm’s AI big data solution to make sure they are automatically uploaded. Check. Robin reviews the models and uses a digital report that the AI system has created that offers conclusions about the portfolio.

Robin sees that the prospect’s overall risk is quite high in a rising interest rates scenario. Down 32% - yikes. The client is 55-years old. Robin can surmise this client is nearing retirement. A loss like that would definitely crush the prospect’s retirement timeline. Does he/she know that?

Robin wants to share this information with the prospect. The wholesaler clicks on “proposal generation” and flips through a branded digital report with eight slides that showcase the strengths/weaknesses of the current allocation. Robin adds notes with digital stickies on each page for the prospect. He grabs the email and shoots it out the door. While the prospect can chew on their current trouble spots, Robin starts to look at the firm’s current lineup of investments and thinks a couple of alt strategies could benefit this prospect. Robin quickly adds those funds into the model and takes out some funds giving unneeded risk.

Hours later, the prospect emails back – “Interesting information. Can we setup a web call to review?” Robin responds “Perfect.” Robin books the meeting. This meeting is a perfect chance to showcase this new alt strategy and consult.

This is the new breed of wholesaler – a portfolio consultant.

In Arthur Miller’s Death of a Salesman, he notes, “the only thing you’ve got in this world is what you can sell.”

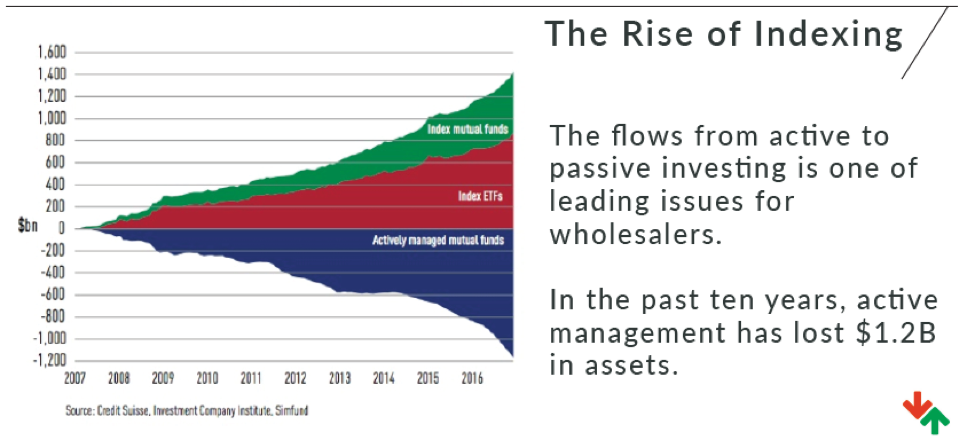

For today’s asset managers that statement illustrates the problem. The rise of technology, transparency and compressing fees has led to outflows for some fund companies. Further, the rise of indexing and ETFs, set against a background of rapid access to information, has created a tough landscape for active management.

The challenges to asset managers have been widely discussed, so this article will focus on the sales process of asset management. For years, the norm has been to use wholesaling divisions to interface with institutions, advisors and other entities to get distribution of funds. That process has involved trade shows, free tickets, perks and rounds of golf. The shifting landscape has challenged this norm.

The death of the traditional wholesaler is inevitable. How it’s reborn is what we’re interested in discussing.

Wholesalers will be reborn as a tech-enabled financial product experts who create efficiency by leveraging omnichannel technology solutions. It’s putting down the golf clubs and picking up a tablet. It’s throwing away business cards for digital portals that collect information in unique and interesting ways. It’s combining tech skills with people skills to be able to enhance wholesaler performance.

We’ll begin with current issues and answers to problems. We’ll construct the future wholesaler as a portfolio consultant, and we’ll conclude with positing about what lies beyond the next few years.

Key trends and topics we will discuss in this paper:

- Three trends plaguing traditional asset management

- Are the current answers working or are they stopgaps?

- The future of wholesaling and distribution: Portfolio consulting

Three trends plaguing traditional asset management

Compression of fees and transparency

What led to the compression of fees in asset management? It’s a bit of a chicken and egg. The rise of fee transparency led to the popularity of lower cost investments and ETFs. Yet, lower cost index funds and ETFs helped bring about a rise in transparency. Further, ease with which advisors can compare products led to a compression of fees. If the fees of a strategy don’t give significant benefit to end clients – why use them?

Technology, lower fees and a solid decade of mostly bull markets has led to a fundamental change in what many institutions, advisors and clients believe investments should cost.

Will this change? A bear market might provide a short-term reprieve to this notion, as it will cause some alternative and actively managed strategies to shine, but the compression of fees will continue.

To paint a similar picture, we turn to our friendly travel agent (wait, you don’t know a friendly travel agent?).

The travel agent: The rise of indexing and technology

It’s the 1990s; you want to take a trip to Europe with the family for the summer. You are thinking Eifel Tower in June with a stroll through Montmartre and lunch by the Champs Elysees. Magical sounding? It certainly is.

Who can help you book such a trip? How about your friendly travel agent who put together that wonderful Canadian fishing trip last year.

The travel agent provided an invaluable service. Today, however, the Internet and technology have rendered the travel agent obsolete. Except, the travel agent still does exist. What for? Exotic vacations, wealthy families and those who are taking large group trips that require significant coordination. For the average family trip, though, the Internet suffices.

This is exactly what is occurring in wealth and asset management, especially to wholesalers. Advisors who interface with clients have technology at their fingertips that can help them review funds/ETFs and make decisions on behalf of clients. For end clients, reading about strategies, researching investments, and using pre-packaged strategies from robo-platforms and index ETFs parallels the ease at which one can compare 15 flights from Atlanta to New York City online in seconds. Comparison makes it easy for investors to investigate both active and passive investment strategies with a couple of mouse clicks.

Financial analysis and planning is wildly more complex than booking a hotel. Thus, the role of the asset manager and the advisor has remained intact. The complexity of finance and financial planning will always allow humans to maintain their dominance over technology, but tech continues to improve. So, it begs the question – are humans improving as well? Are we adopting technology and utilizing it to make us better than we were last year?

Despite the growing number of investors, many mid-level asset managers continue to experience outflows. A few asset managers, though, have continued to grow. They all have something in common … they weren’t afraid to change or adopt new strategies. The reality of the asset management space will be – adapt or die.

Are current answers working or are they stopgaps?

Fees are going down. Transparency is increasing. Passive investment products are becoming ubiquitous and technology is rendering some roles obsolete.

What can asset management firms do? Some of these answers start to get at changing how asset managers sell, but more change is still needed.

Asset manager = technology manager?

In late 2017, Barron’s put out an article called “Blackrock Flexing Its Advisor Technology Muscle.” The article began by noting that Blackrock wants to “control the advisor desktop.” They launched financial planning tools. They built a risk analysis platform that analyzes portfolios. They want the advisor to use Blackrock in every facet. Why? Because if they do, they can control the assets. What better way to get distribution and diversify business than being at the forefront of the technology advisors + end-clients interact with.

This should scare asset managers. Yet, so far there has been some interest in trying to keep up with Blackrock, but it’s muted at best. Maybe keeping pace is impossible, but if we assume that tech is the future, and then Blackrock is insulating itself very well from obsolescence.

Here is the question every asset manager executive should be asking: How are we adopting technology and how we can use it to create a competitive advantage? If you aren’t using technology, how do you plan to catch up to those that already are?

Fund-to-fund comparisons

One stopgap in the asset management industry is doing fund-to-fund comparisons – using cool charts and stats to show why your fixed income fund is better than theirs. This is one of those stopgap strategies that won’t work in the long run. Why?

It doesn’t battle against fee compression. In fact, it often draws more attention to fees. It doesn’t combat the rise of indexing or leverage unique technology. It just changes one actively managed strategy for another active managed strategy.

Instead, we need to turn comparative analysis on its head and introduce it in a meaningful way to advisors or end clients. Another antidote for the changing landscape – holistic approaches to investment analysis that help advisors build for lifestyles, risk aptitudes, and consult rather than sell.

Side-to-side comparison is the quintessential product-push strategy; whereas a holistic approach to portfolio analysis that investigates more than just single products can deliver exceptional benefits to advisors and their clients.

We’ve laid out some issues for asset managers. We’ve laid out what some firms are doing and what are some current answers.

Change is on the horizon, and if we want our sales divisions to be successful, major changes must occur.

The future of wholesaling and distribution

Retail is a blueprint for asset management. Retailers that wanted to survive the onslaught of technology have all adopted an omnichannel approach. It was the brick-n-mortar store to the digital store and a network between the two where you could order online and pick up in a store. Or, if you are in the store, they can get your size online and deliver to your house. It did, however, require new investments from retailers – larger warehouses, websites, digital marketing, developers, and tech help.

Wholesalers won’t actually die. Rather, they will be reborn. The wholesaler of today is a dying breed, and the wholesaler of tomorrow is better than today’s wholesaler and tech alone. Just like Mr. Gadget showed us years ago, a skinny 180-pound geek can fight super villains when he utilized technology, rendering Gadget … a hero.

Today, the wholesaler will be reborn as a “cyborg” who has to be adept at utilizing technology with a technology-enabled mind along with having the ability to interface with clientele.

We call it, “The Geek with People Skills.” If you had in your operation salespeople who all could be armed with extremely beneficial technology, could talk about asset allocation and portfolio construction backwards and forwards and grab a beer/catch a game with target clients … would that not be the ideal “store front.”

The cyborg wholesaler

No, we aren’t envisioning a world of robotic sales people; however, only about 25% of wholesalers utilize technology at their trade show booths. Why?

Asset managers are not prioritizing tech skills in hiring as well as in training. They are slowly adopting some aspects of technology. There is fear from wholesalers that technology can render them obsolete. That’s the wrong attitude. The best wholesalers are the ones who can impress their audience with technology and cut down on inefficiency.

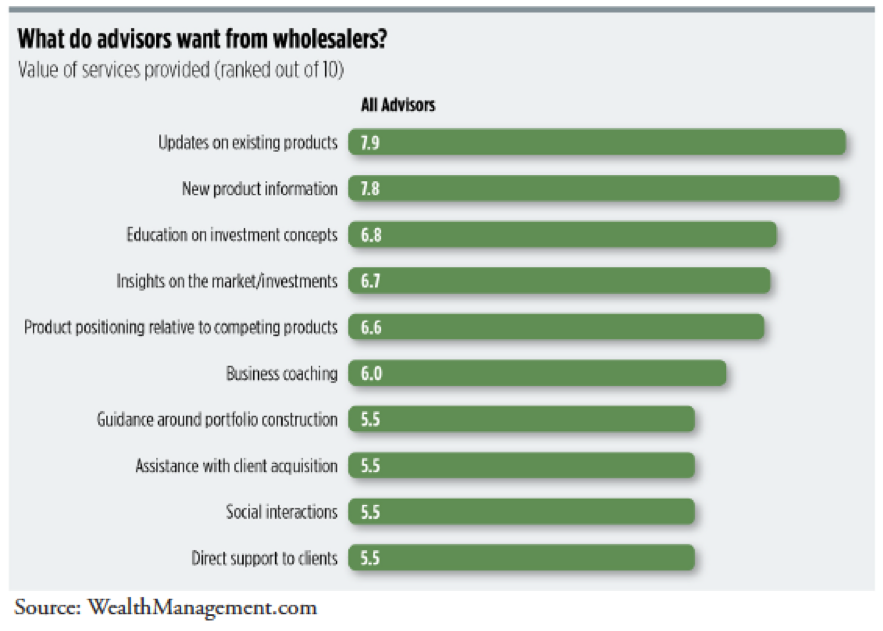

The main takeaways that we see for the future wholesaler are:

- Gains trust by offering something of value

- Consults rather than sells

- Offers product suggestions only when it makes material difference

- Uses an omnichannel approach to selling

We started with a day in the life of Robin – our future wholesaler. What does the life of this wholesaler look like beyond a couple hours in the morning:

At the trade show – Shows up in their best blue suit, shoes shined. Whips out a couple of beautiful touch-screen computers and iPads for the team. Sets up shop. As advisors and institutions begin to filter in, instead of throwing golf balls and Nerf footballs, he asks the advisor … “Can we quickly stress test your portfolio?” That’s something the advisor hasn’t heard before. The salesperson enters in a few tickers on their new portal and in moments is showing the advisor weaknesses/strengths in their current allocation. Well, the correlation risk looks pretty high and your Sharpe Ratio is below the benchmark. Could I follow up with a report for you that stress tests this against 100 economic outcomes? The wholesaler (now portfolio consultant) becomes an asset to the advisor not an annoyance. They are providing something of value immediately.

At the office – Having collected 25 allocations from advisors at the trade show, the wholesaler quickly prints branded reports that show the advisor statistics on their current portfolio. The wholesaler highlights five areas of concern and potential improvement for the advisor. All the while, at no point has the new breed of wholesaler pitched any product. Why? The wholesaler is gaining trust. The portfolio consultant uses time at the office to utilize tech to diagnose and add value to conversations.

Online – The wholesaler logs into a website portal he/she set up that has a short video introducing him/herself to visitors. The message is clear. Enter in your portfolio, and I will provide a 15-page report stress testing your holdings (or investigating asset allocation or checking your ESG score). A bouncing arrow next to an entry screen shows in real-time how the advisor or HNW client or institution looks as they enter holdings. When they submit, the information loads up to the CRM as a lead from the digital store.

Meetings and portfolio consulting –The wholesaler has a lead from Omaha, NE. He could hop on a plane and meet face-to-face, but being in San Francisco the flights to Omaha seem high. And the advisory firm is busy themselves. It’s a first meeting, so the wholesaler turns to the digital interfacing portal that the company has built that allows each party to see each other, and in real-time show the advisor information. Finally, the advisor is primed for a pitch. The wholesaler compares the firm’s current model to a new model that the wholesaler constructed using a portfolio optimization feature in its analytical tool. The wholesaler continues to become an asset for the advisor providing transparency and trust through useful information.

18 holes just became a two-hour webcast where the two discuss the value the asset management firm’s smart-beta ETFs can provide as a way to cut down on costs, but still offer active management. Additionally, the advisors’ HNW clients want access to options strategies, so the wholesaler’s new options SMA is perfect.

The cyborg wholesaler optimizes talent and plays off the changing landscape

As the role of the advisor changes, as tech continues to increase transparency and as the investment landscape becomes flatter with information, asset managers must respond by championing this landscape and not by playing catch up.

The good news for asset management firms is that technology to help leverage this future wholesaler is available today. Multiple vendors have developed turnkey solutions that are ready to be adapted for your firm. These solutions have been already adopted by some asset managers.,.

The rebirth of the wholesaler will happen. Will you shape it?

David Ristau is the director of business development for HiddenLevers. Before joining HiddenLevers, he launched fintech startups in the wealth management and options analysis space. Jeffrey Baker assists the HiddenLevers team in business development, he has held previous positions as an analyst at Raymond James and UBS.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All