As we have noted in this space in the past, there is a lot of the world that cannot be captured by the most elegant and detailed of spreadsheets.

John Vail, Chief Global Strategist at Nikko Asset Management, discusses Nikko AM’s Global Investment Committee views on current global market drivers as well as expectations for the markets moving forward.

…war is an old habit of thought, an old frame of mind, an old political technique.

The first quarter of 2022 brought violence that rocked communities – and markets – internationally. We look at what aftershocks may still be yet to come.

Last month, the Federal Reserve kicked off a campaign to increase interest rates to bring down the highest inflation the U.S. has experienced since the 1980s. Critics contend the Fed still isn’t doing enough, and the central bank seems to agree. Several high-ranking Fed officials, including Chair Jerome Powell, have said in recent days that interest rates may need to rise faster, and possibly higher, than initially planned.

On the latest edition of Market Week in Review, Director of Investment Strategies, Shailesh Kshatriya, and Director of Institutional Investment Solutions, Greg Coffey, discussed market reaction to the latest developments in the Russia-Ukraine war.

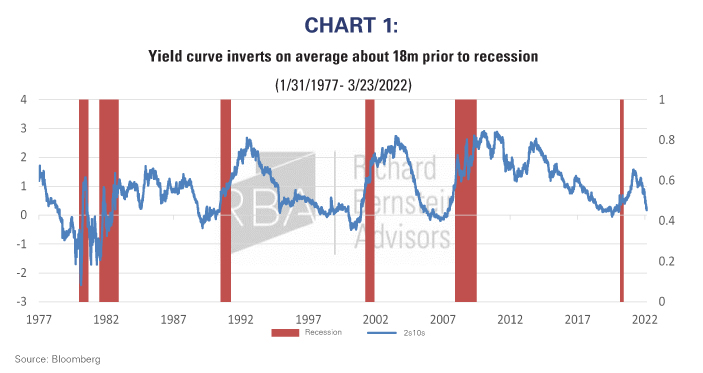

Yield curve inversion conversations are dominating the media to the point it almost sounds like the start of a bad joke.

As quarters go, this was one for the record books. Taking three months, or a calendar year, to have any particular significance makes no sense, but it’s difficult to quell it. So, here is an attempt to summarize what’s changed in the last three months from the point of view of markets.

Federal Reserve Chair Jerome Powell and his colleagues are on the march to return ultra-loose monetary policy and accommodative financial conditions to more normal levels. The trouble is, their destination is uncertain and the terrain may be shifting as they forge forward with higher interest rates.

Reflecting on the history of our family office, our investing philosophy mirrors how previous generations built their wealth through farming. They patiently waited to harvest the crops they planted; we buy securities and patiently wait for them to appreciate.

The yield curve is really just a symptom. I like to compare it to a fever—not serious in itself, but a sign you have an infection or some other ailment. An inverted yield curve means something is wrong in our economic body. So today we’ll consider what it means.

The surge in bond yields suggests that we are nearing the ideal entry point to buy longer-duration bonds for capital appreciation and portfolio protection.

The Federal Reserve’s first rate hike in years has sparked bond volatility, pushing investors to search for yield elsewhere.

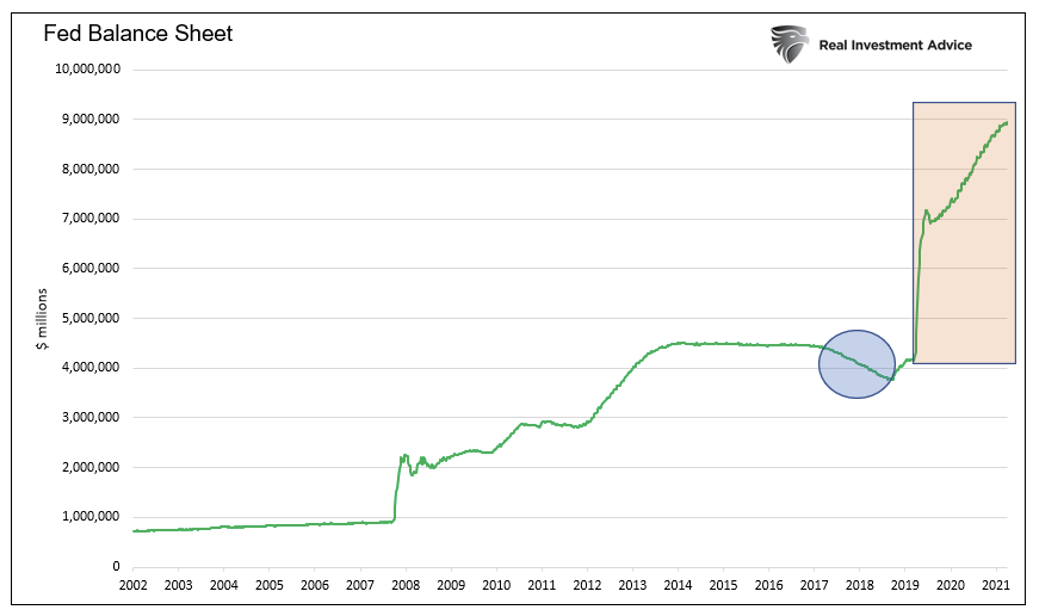

With QE finished and QT on the horizon, I answer a few questions to help you better appreciate what QT is, how it will operate, and discuss how draining liquidity will affect markets.

The US Federal Reserve is turning increasingly hawkish—hiking rates fast enough to slow inflation while maintaining economic growth will be a monumental task.

In June of 2021, KCR’s Equity Research Team wrote a brief but pointed review of the legendary treatise on value investing, A Margin of Safety by Seth A. Klarman.

Much of the commentary about the Ukraine war’s implications for the investment-management industry has tended to be both immediate and narrow, particularly in discussions about the spillovers for different segments. By zooming out, however, some longer-term ramifications become more apparent for both public and private markets.

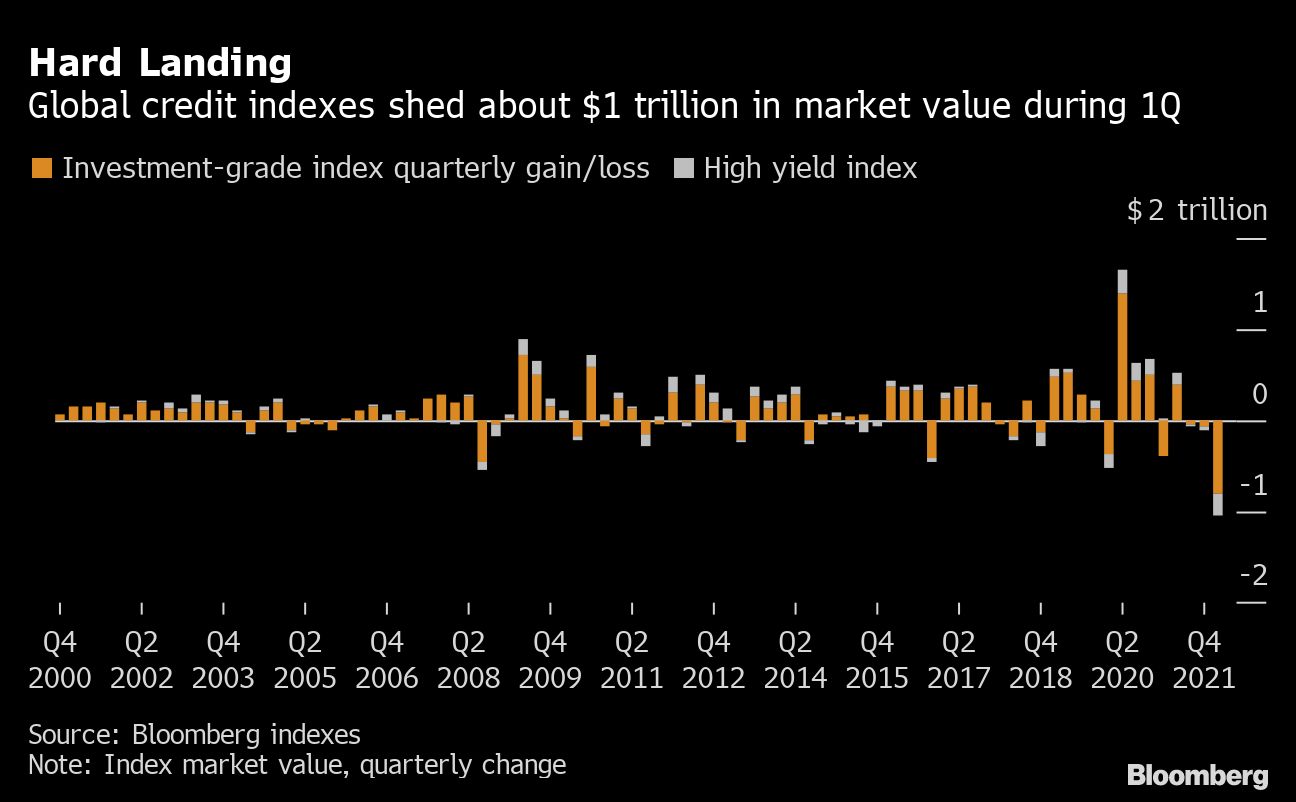

Investors in corporate bonds are bracing for more trouble after getting hammered by rampant inflation and rising yields in the first quarter.

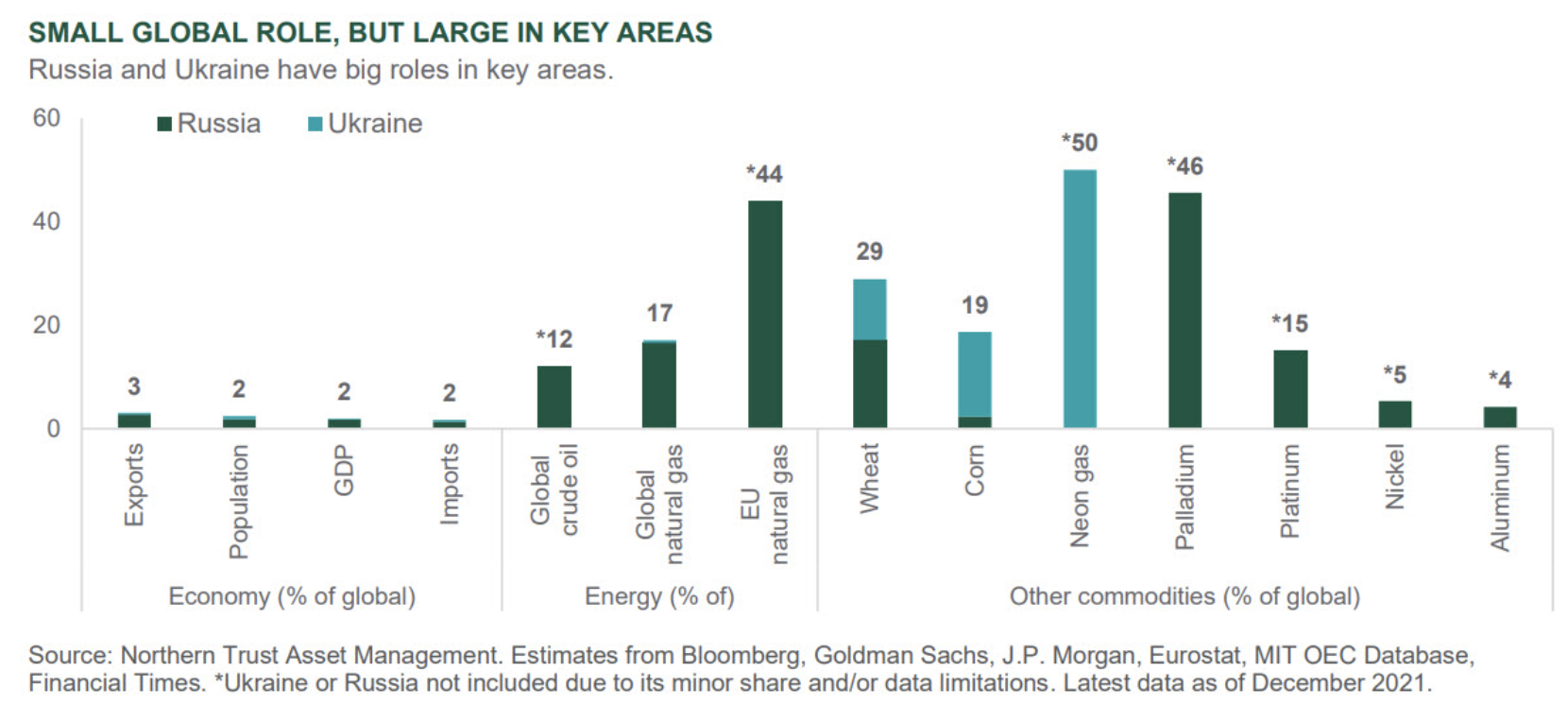

The Russian invasion of Ukraine is a shock to the existing world order. From an economic perspective, the initial impact of the war is rising inflation given the importance of Russia and Ukraine in the supply of commodities to the world.

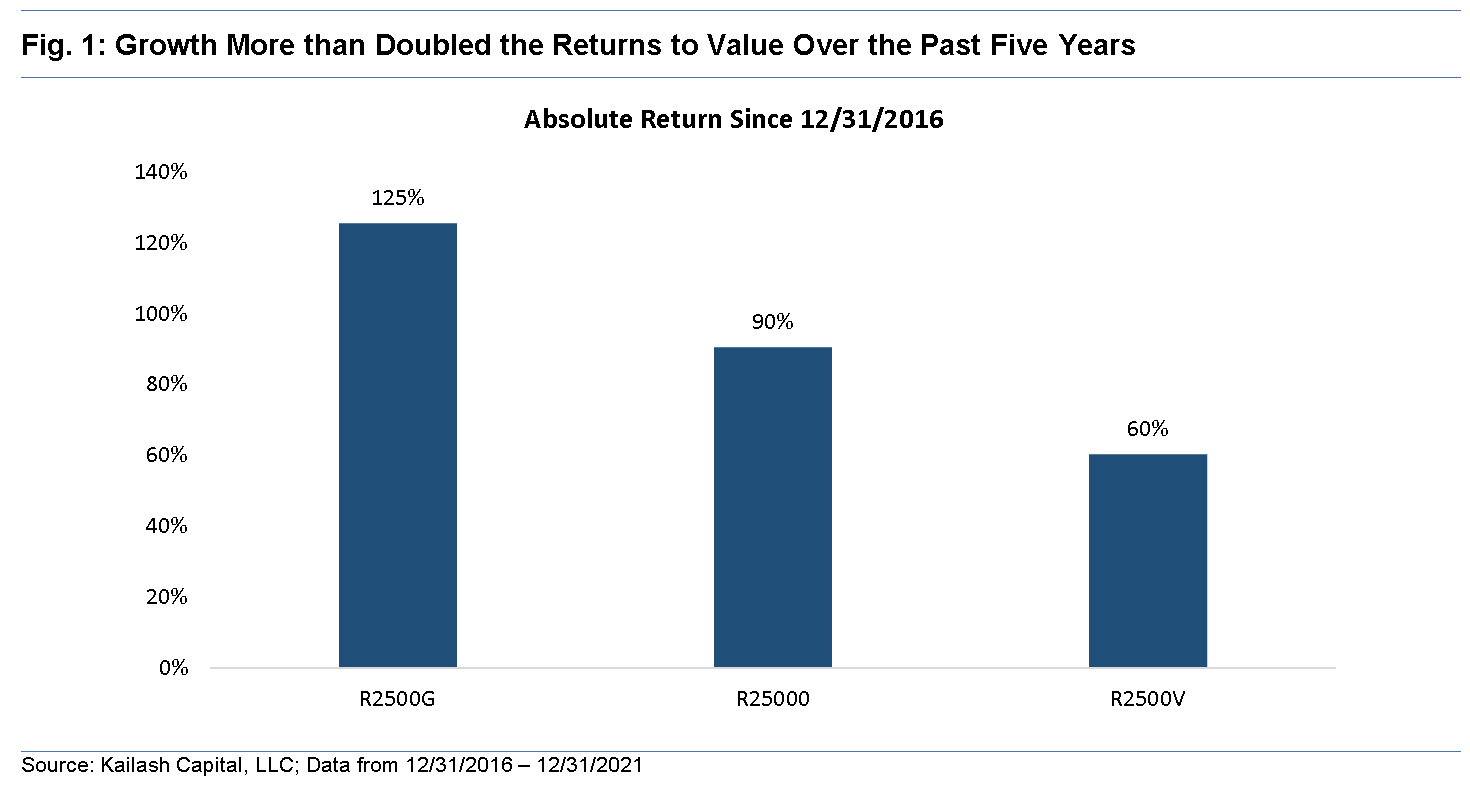

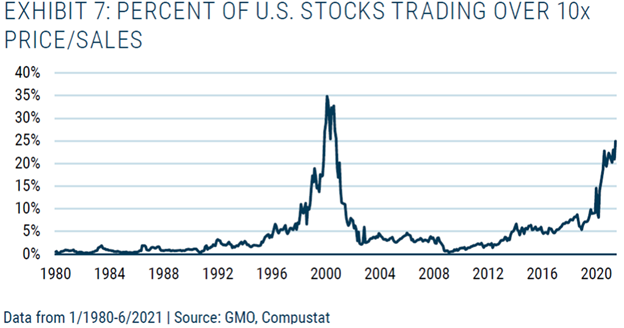

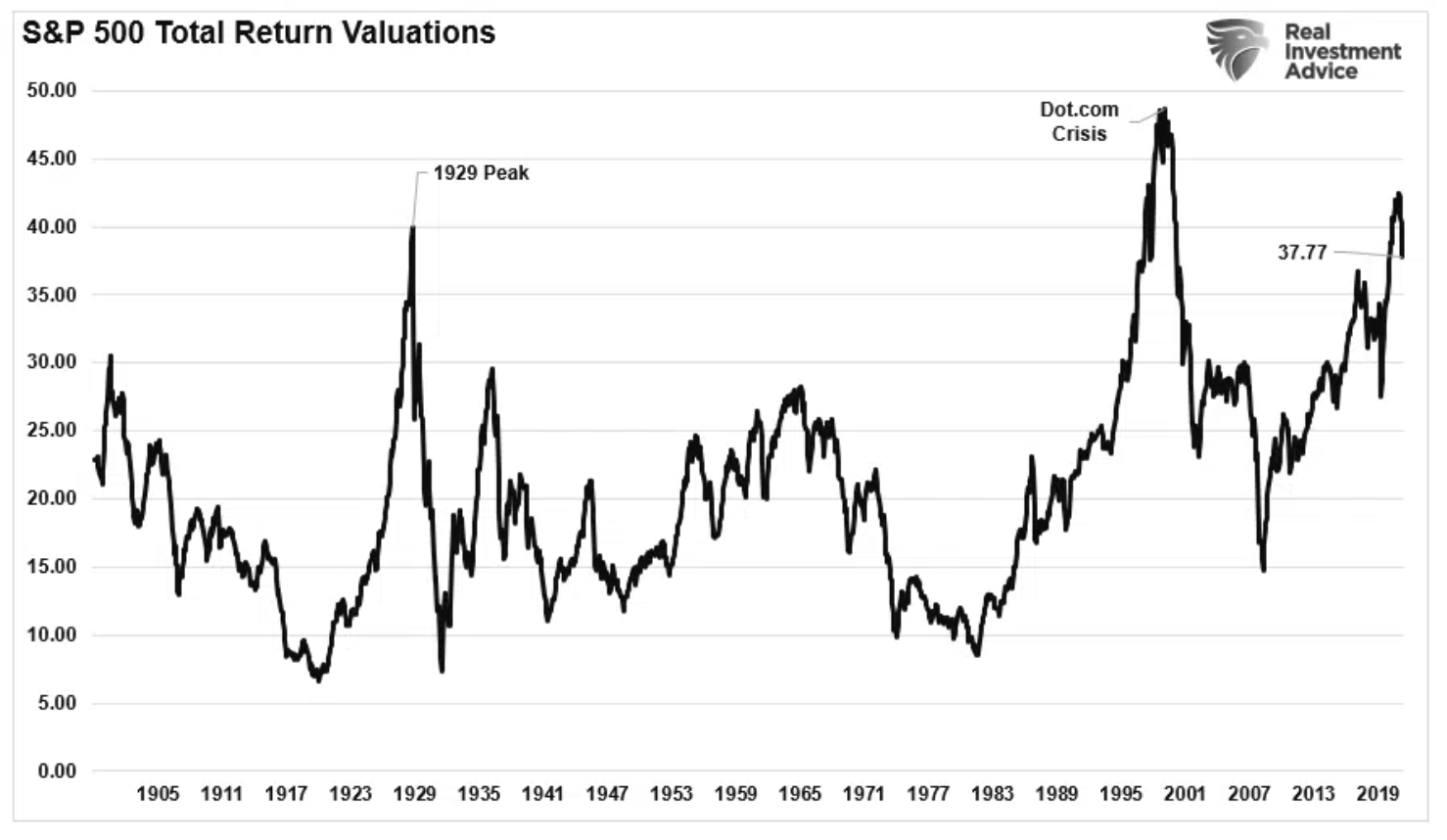

Totally Addressable Markets (TAM) are at the heart of what Charlie Munger calls the biggest euphoria episode he has ever seen in his career. We believe that the coming stock market failure emanating from the over-pricing of the U.S. stock market is closely tied to TAM.

The yield curve's movements are unlikely to change the Fed's course.

Home price fundamentals suggest appreciation will slow but remain resilient.

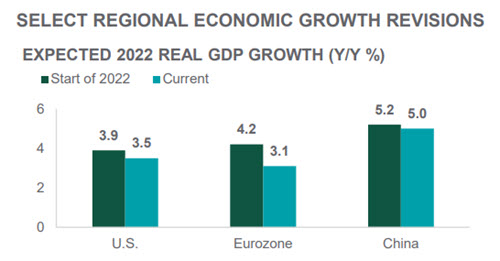

Russia's invasion of Ukraine has sparked higher inflation, unleashed additional market volatility and will likely lead to a slowdown in global growth rates. However, we believe above-trend growth is still possible this year, provided hostilities ease and energy prices stabilize.

Buyout activity is picking up pace in Europe, but a number of banks are taking a cautious approach to new risk, looking for higher pricing, more flex protection and in some instances fuller fees on junk-rated debt underwrites against a backdrop of heightened volatility, inflation and rising rates.

The expected return from a roulette spin is negative: -5.26%.

Bailouts are the root cause of the dysfunction of capitalism and the demise of free markets.

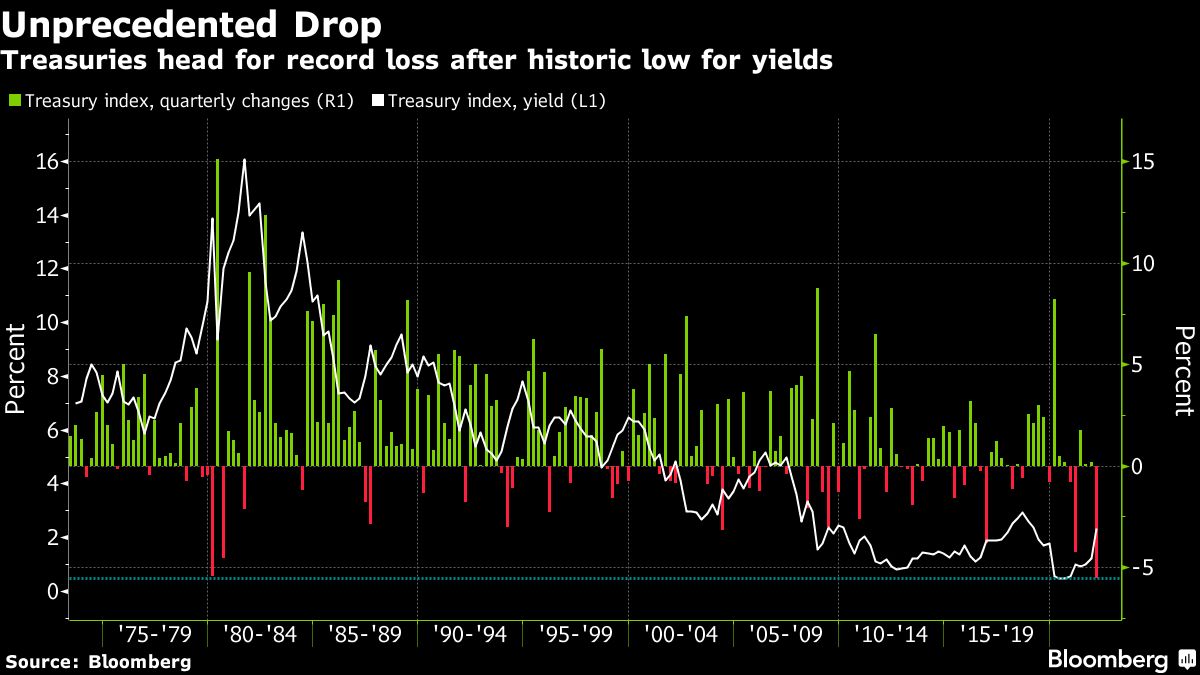

The Bloomberg Global Aggregate Index, a benchmark for the bond market worldwide, has tumbled 11% from its peak in January 2021, equating to a drop of $2.6 trillion in the index’s market value.

Economic theory says that “green” stocks – those of companies with a low carbon footprint – should underperform “brown” ones. But in recent years that has not been the case, and new research explains how cash flows to sustainable strategies have driven short-term outperformance.

Some countries have climates and athletes that are better suited for the Winter Olympic Games, and others for the Summer Olympic Games. Every country on earth had to deal with Covid, though, whether they’re hot or cold, rich or poor.

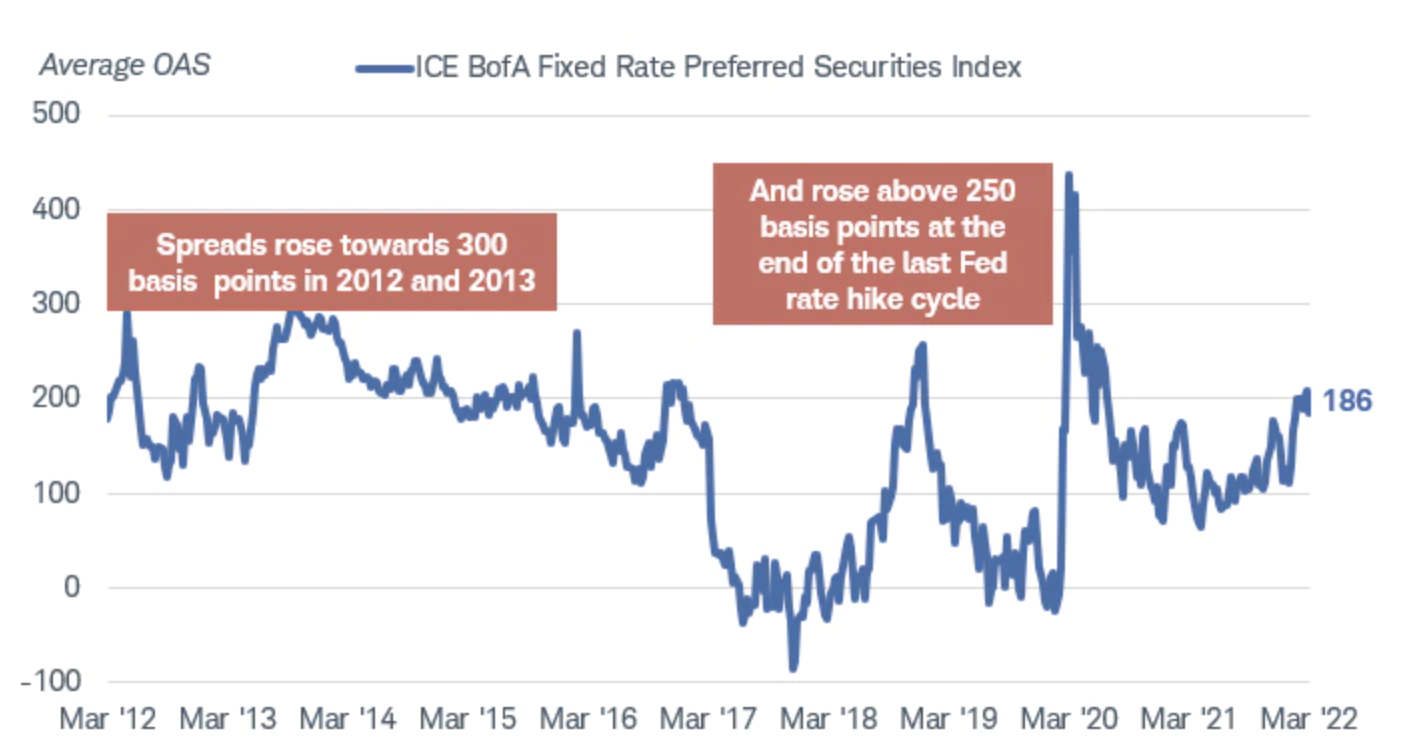

Preferred securities prices have fallen sharply, presenting an attractive entry point for income-oriented investors who can ride out the volatility.

The 2s10s curve is once again knocking on the door of becoming inverted (while some curves like the 3s10s and 5s10s already are), causing quite a stir among market watchers that recession is imminent. In his latest report, Michael Contopoulos examines the 2s10s yield curve movement leading up to the past 6 times the US economy slipped into a recession and discusses what could be different this time.

Filling out your March Madness bracket provides insight into how investors select assets, structure portfolios, and react during volatile market periods.

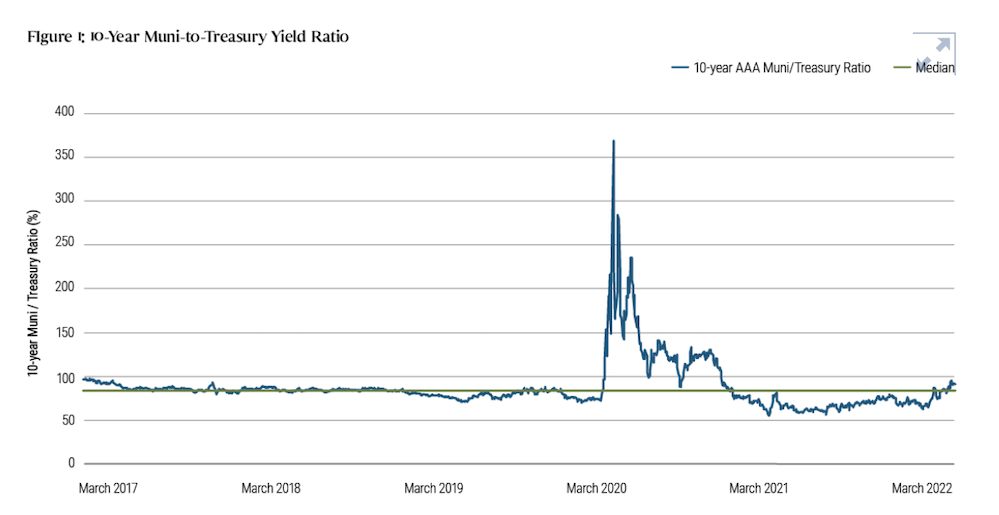

Their track record in periods of rising interest rates suggests municipal bonds could be well-positioned for this year’s market environment.

Yesterday, I laid out why I am not concerned, in general, about what a yield curve inversion means for the economy, while still being very aware of the increasing risks.

Unfunded pensions for state and local governments were once expected by some to sink the whole market.

The Fed struck a hawkish tone at its latest meeting, but Franklin Templeton Fixed Income Chief Investment Officer Sonal Desai believes it still underestimates how far rates will likely need to rise—and so do the markets.

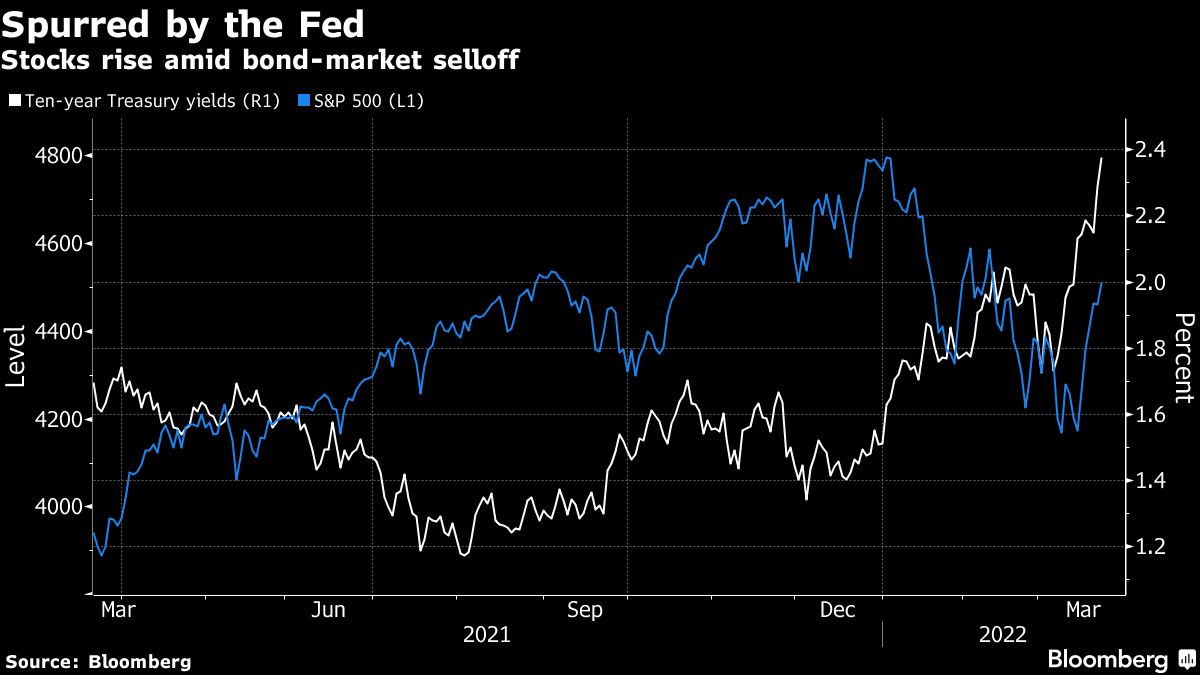

Call them brazen, call them naïve, but stock investors are giving no sign of being daunted by the hottest inflation in decades or the accompanying surge in bond yields. Their boldness has sent analysts in search of ways to explain how the S&P 500 Index has managed to rally in five of the last six sessions, even as the Federal Reserve promises higher rates while war rages in Europe and Treasury rates see the biggest two-day jump in two years.

Federal Reserve Chair Jerome Powell had his foghorn out on Tuesday blaring that there is nothing, repeat nothing, to stop policymakers from yanking interest rates up in half-point steps. His hawkishness prompted the yield curve to flatten to levels not seen since 2016, setting off alarm bells about a potential inversion - where shorter-dated levels rise above longer-term rates - signaling recession.

The U.S. bond market reeled further on Tuesday, extending Monday’s declines after Federal Reserve Chair Jerome Powell’s aggressive rate hike comments drove yields on short-dated Treasuries to one of their biggest daily jumps of the past decade.

Judging from price movements on Monday, the Federal Reserve risks slipping further into a no-win interaction with markets that is more familiar to developing countries that lack policy credibility than to a systemically important central bank — let alone the world’s most powerful one.

The Fed last week signaled a large and rapid increase in its policy rate over the next two years and struck a surprisingly hawkish tone, indicating it’s ready to go beyond normalizing to try to tame inflation.

Actively managed global allocation funds claim that skilled investment managers can produce a superior rate of return compared to traditional index funds. But the reality does not match the hype.

Elon Musk recommends that investors own “physical things” instead of cash in the face of historically high inflation. So why is he holding on to his Bitcoin and Ethereum?

Dividend Contenders are mostly fast-growing dividend growth stocks that increase their dividends for 10 to 25 consecutive years.

Mutual Series’ analysts see value opportunities in the financials sector as the interest-rate environment turns more favorable in the United States and European banks see greater clarity about the impact of the Russia-Ukraine war.

Senior Sovereign Analyst Gregory Hadjian and Alpha Strategies Portfolio Managers Andrea DiCenso and Peter Yanulis consider the potential opportunity offered in local EM debt markets.

The Fed’s QE is officially over.

With no end to Russia’s attack on Ukraine in sight, energy and agriculture are feeling the strain.

The Federal Reserve announced a 25-basis-point increase in the target range for the federal funds rate, to a range of 0.25% to 0.50%, its first rate hike since December 2018.

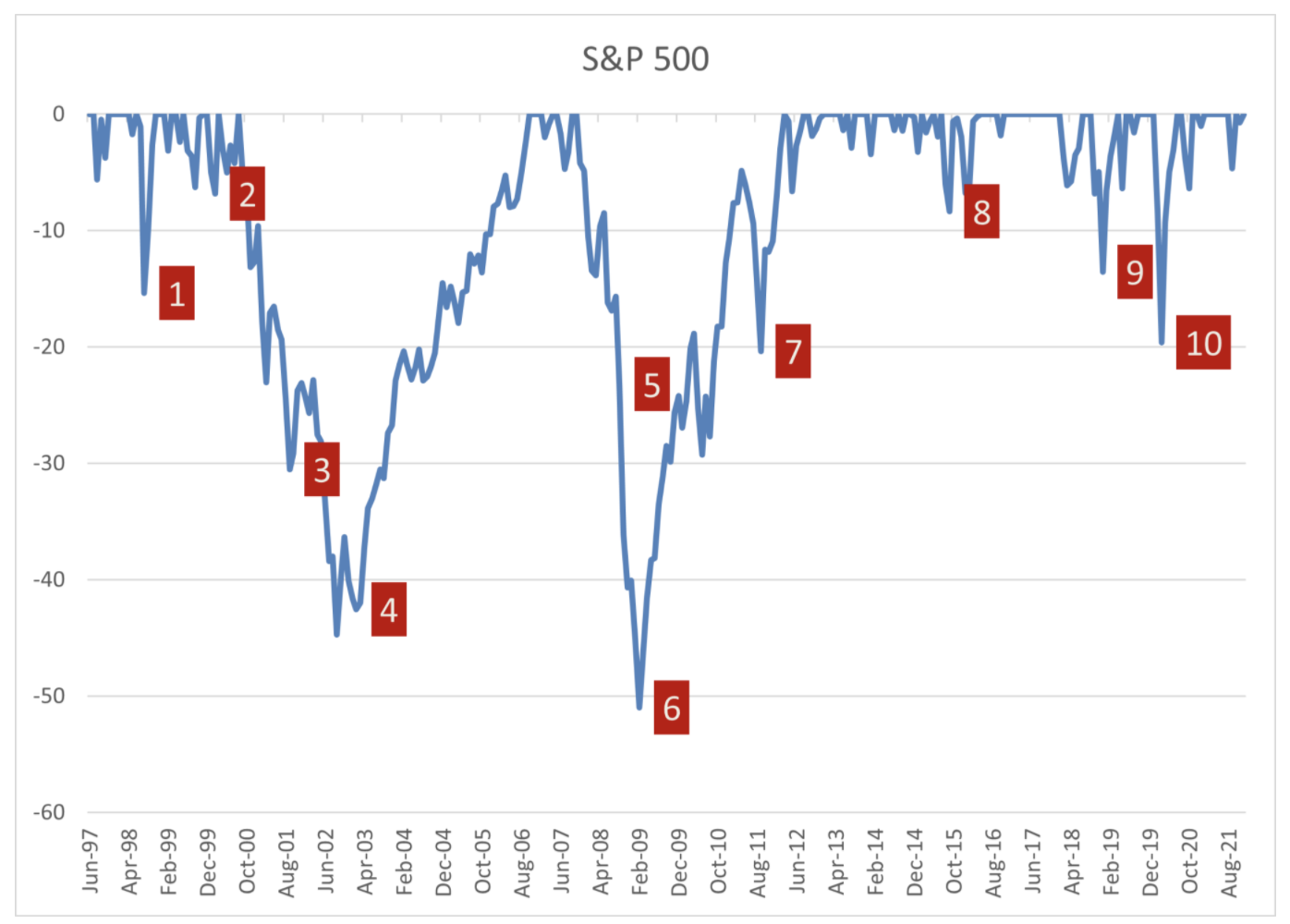

Quick – where were you 25 years ago?