Last week, the Federal Reserve increased interest rates, and promised much more of the same in the months ahead. The consensus among the Federal Open Market Committee (FOMC) sees overnight interest rates peaking at close to 3% before settling back down.

Tightening of this scale may be necessary to bring inflation to heel. But it may also raise the risk of recession. The Fed would certainly like to avoid this outcome, but may view the long-term economic costs of high inflation to be larger than the cost of a short downturn.

|

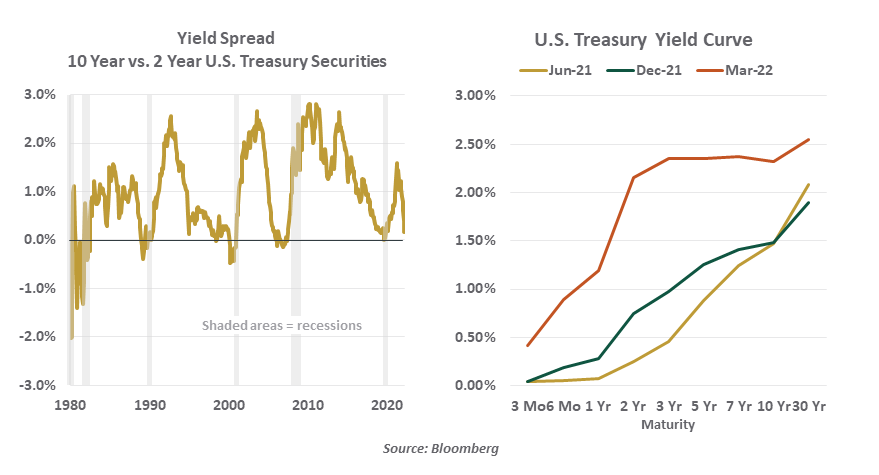

Yield curves have a muddy relationship with recessions.

|

As each step in the tightening process is considered, these risks will be reassessed. One gauge that will certainly be consulted is the yield curve, which is thought by many observers to be a primary recession indicator. The yield on two-year Treasury securities has exceeded the yield on ten-year Treasury securities prior to each of the last four U.S. downturns.

The intuition behind this juxtaposition is that central banks will have to retreat at some point in the future, which typically occurs when growth is faltering. To be clear, though, there is no cause-and-effect.

A closer look at the history raises some questions about the signal given off by the yield curve. There have been inversions which corrected without being associated with a downturn. The lead time between an inversion and a recession is highly variable; it has been as short as three months and as long as 20 months.

Further, the triggers for several recent recessions have been sudden. The invasion of Kuwait was a proximate cause of the 1991 recession; the dot-com crash was a catalyst for the 2001 recession; and the pandemic was solely responsible for the short recession we had in 2020. None of those events was within the yield curve’s estimations prior to their occurrence, suggesting that inversion and recession could be coincidental.

There are a lot of factors that drive the pricing of long-term securities. Prospective central bank strategy is just one of them; fiscal policy and the supply of debt play an important role, as well. The ten-year Treasury note is a global safe haven asset, receiving inflows when risk is being reduced and losing them when investors become more aggressive. Portfolios seeking to hedge interest rate risk will often use the ten-year tenor as a target point. Given this myriad of influences, it is hard to infer clearly that inversions in the bond markets are recession forecasts.

Looked at broadly, today’s U.S. yield curve is anything but inverted. With three-month yields of less than 50 basis points and 10-year yields converging on 2.5%, the overall slope is decidedly upward. But most of the steepness comes within the first two years of maturities, consistent with the message that the Fed has been sending about its plans for monetary policy. Thereafter, yields remain fairly steady, consistent with a soft landing.

On a technical note, interest in the 10-year Treasury from pension managers has been especially robust recently. The general rise in interest rates has helped lift the ratio comparing future benefit payments to the assets set aside to cover them. When this “funded ratio” approaches 100%, managers will seek to reduce risk and match benefit and bond cash flows.

Keeping all of this in mind, it is still useful to watch the shape of the yield curve, among other signals, for early warnings of recession. But would a yield curve inversion cause the Fed to back off? I am not at all sure. Inflation is substantially higher than desired, and long-term price stability is a primary objective of monetary policy. The longer that inflation remains elevated, the more likely that it will become deeply embedded in the economy. Unearthing it at that point becomes very challenging.

Given the murky relationship between the yield curve and the business cycle, and the Fed’s intent to preserve its reputation, we expect them to keep interest rates moving up even if the yield curve turns upside down.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust