The Fed last week signaled a large and rapid increase in its policy rate over the next two years and struck a surprisingly hawkish tone, indicating it’s ready to go beyond normalizing to try to tame inflation. It’s easy to talk tough, and we believe the Fed is unlikely to fully deliver on its projected rate path. The reason? It would come at too high a cost to growth and employment. We do now see a higher risk of the Fed slamming the brakes on the economy as it may have talked itself into a corner.

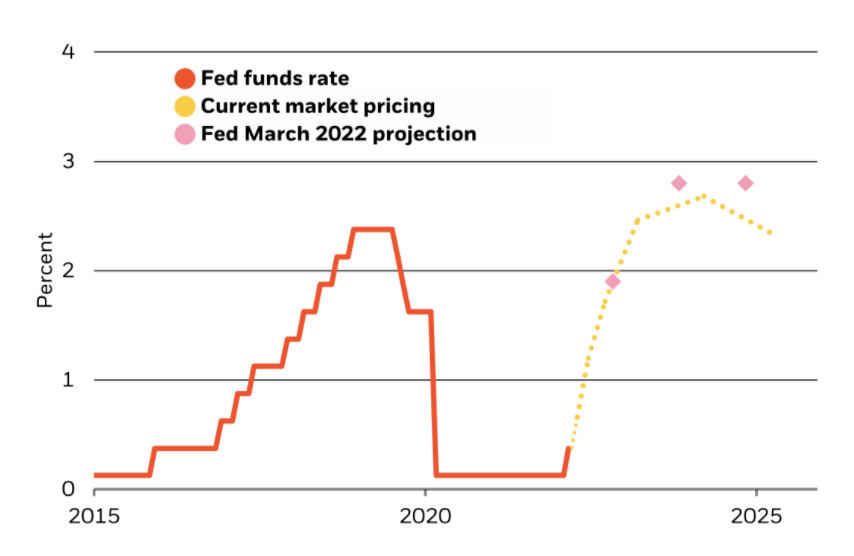

U.S. federal funds rate, market pricing and Fed projections, 2015-2025

Past performance is not a reliable indicator of current or future results. Indexes are unmanaged and not subject to fees. It is not possible to invest directly in an index. Sources: BlackRock Investment Institute, with data from Haver Analytics, March 2022. Notes: The chart shows the historical fed funds rate, current market pricing in forward overnight index swaps and the Fed’s March 2022 projection based on the median dot of policymaker projections.

The Federal Reserve has kicked off its hiking cycle with a quarter-point increase – the first since 2018. The decision was expected. What surprised was the Fed’s stated goal to get the fed funds rate to 2.8% by the end of 2023 (see the pink dots on the chart). This level is in the territory of destroying growth and employment, in our view. At the same time, the Fed’s latest economic projections pencil in persistently high inflation but low unemployment – even as it has called current labor conditions tight. We believe this means the Fed either doesn’t realize its rate path’s cost to employment or – more likely – that it shows its true intention: to live with inflation. We think this is necessary to keep unemployment low because inflation is primarily driven by supply constraints and high commodities prices.

BoE provides a glimpse ahead

The Bank of England (BoE), the first major developed market (DM) bank to kick off the current hiking cycle, increased its policy rate for the third time to 0.75%. Like the Fed, the BoE recognized additional inflation pressures from high energy and commodity prices. It also signaled that it may pause further rate increases, with rates back at pre-pandemic levels. We believe this means the BoE is willing to live with energy-driven inflation, recognizing that it’s very costly to bring it down.

The BoE provides a glimpse of what other DM central banks may do once they get back to pre-pandemic rate levels and the effect of rate rises on growth become apparent. The Fed’s tone may change as the consequences for growth become more apparent after aggressively hiking this year. The Fed last week perhaps wanted to appear tough by implying even more rate increases in future years to keep inflation expectations anchored, in our view, without expecting to deliver those hikes. To be sure: The Fed will normalize policy because the economy no longer needs pandemic-induced stimulus. It has also signaled it will start reducing its balance sheet, marking the start of quantitative tightening. Finally, we expect the Fed to raise the fed funds rate to around 2% this year – close to pre-pandemic neutral levels – and then pause to evaluate the effects.