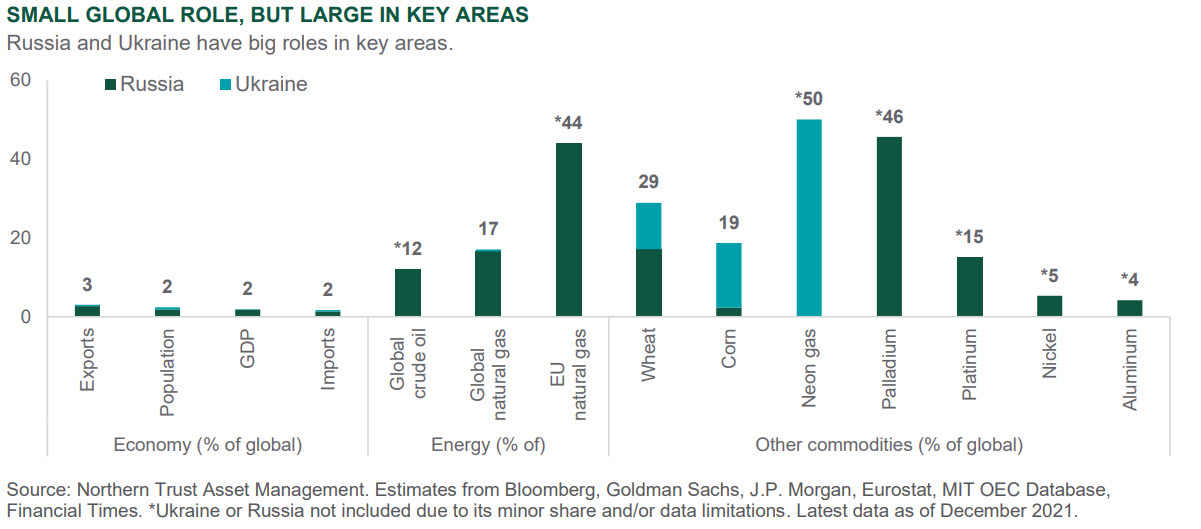

In just a few weeks’ time, the threat of a Russian invasion of Ukraine has become the reality. The resulting humanitarian toll has led to millions of Ukrainians leaving the country, with a similar number displaced and too many killed or injured. Forecasting the eventual outcome remains highly uncertain, but Russia’s relentless attacks show no signs of abating and the “off-ramp” for President Putin remains elusive. European growth will be most notably affected due to the region’s close economic ties and reliance on Russian gas and oil. There will also be second-order effects as surging commodities prices affect inflation and growth globally. So far this year, oil prices are up 45%, European natural gas prices are up 74%, and global metals prices have risen 33%. As shown in the exhibit below, Russia and Ukraine represent a small percentage of the global economy, but they have an outsized role in European energy and global agriculture. Beyond the risk of war-related supply disruptions, there is the potential for “weaponizing” the supply of key commodities. Russia and Ukraine are major producers of palladium, used in many industrial applications, and neon gas which is used in semiconductor production.

The impact of surging commodity prices will be felt most directly in those economies that are large net importers – such as major European countries and some emerging market economies like China. The U.S. is better positioned as a major producer of energy and agriculture, but it won’t be immune to the indirect effects. We have downgraded our growth outlook for Europe as a result, and risks around U.S. growth have risen. We have also increased our inflation expectations globally, as inflation was reaccelerating even prior to the Ukraine invasion.

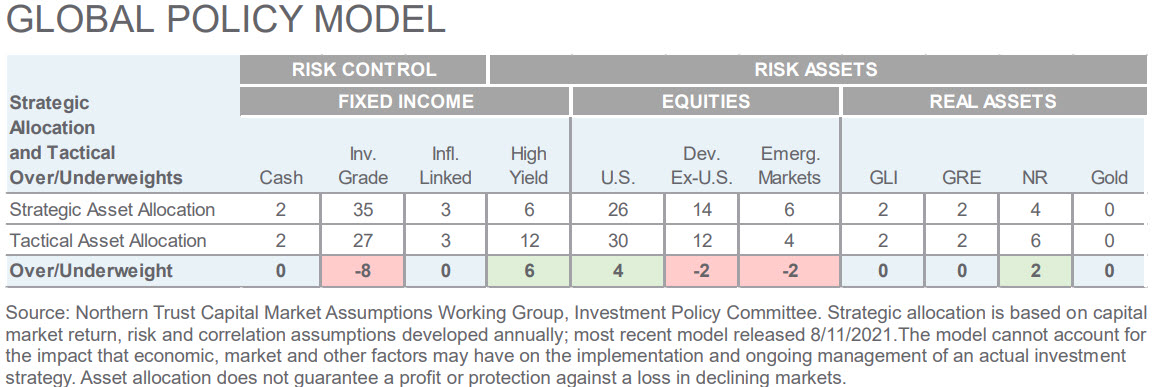

In our global policy model, we have reduced our recommended exposure to developed ex-U.S. and emerging market equities, and increased our exposure to inflation-linked bonds, high yield bonds, U.S. equities and cash. Our base case outlook now envisions slower growth due to the fallout from the invasion, and more persistent inflation as countries have to find new commodity supplies. Our risk cases focus on the potential for military escalation by Russia, through unconventional war tactics or the invasion of the Baltics and other NATO countries. Our final risk case addresses the potential of a greater economic shortfall as the economic restructuring necessary to address the “newest world order” is greater than market expectations.

INTEREST RATES

- Inflationary pressures have pushed nominal yields higher in recent weeks.

- Falling real yields (in the face of geopolitical risks) have provided some offset to higher interest rates.

- We currently prefer ILB (for inflation protection) and cash (for dry powder) over investment grade bonds.

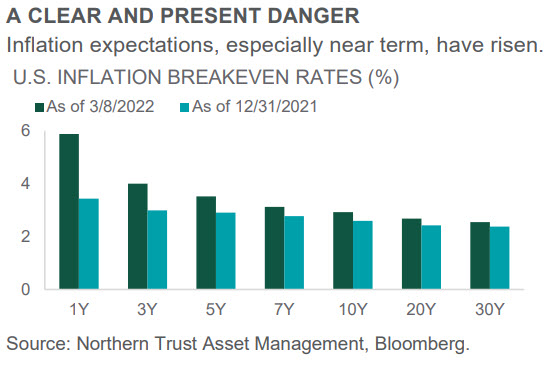

At the end of 2021, near-term inflation expectations were higher than longer term expectations. This relationship is even more pronounced now (see chart). While all inflation expectations have shifted higher, near-term inflation expectations have notably risen, while the increase in longer term expectations has been less substantial. This suggests that investors believe that elevated inflation levels will normalize over a medium-to-longer time horizon.

Consumer Price Index (CPI) components hit hard by the pandemic such as used cars and trucks, airfares, and housing have kept inflation elevated. Additionally, due to the Russia-Ukraine conflict, food and energy prices have quickly moved higher and are likely to have a strong impact on upcoming inflation readings. Price stability is currently the main focus for the Federal Reserve and if prices remain near current levels they will likely move rates swiftly and forcefully. As long as real yields remain low, inflation-linked bonds (ILB) should outperform nominal Treasuries over the near term, but we anticipate a lot will ride on the outcome of the Ukrainian conflict. We believe inflation will remain elevated in the near term but expect it to move lower over the longer run as supply chains heal and tighter monetary policy cools demand.

CREDIT MARKETS

- High yield’s energy sector weight can support the asset class during ongoing geopolitical risks.

- High yield, in general, is a downside protection risk asset, making it preferable over equities at present.

- We prefer credit risk over interest rate risk and retain our meaningful overweight to high yield fixed income.

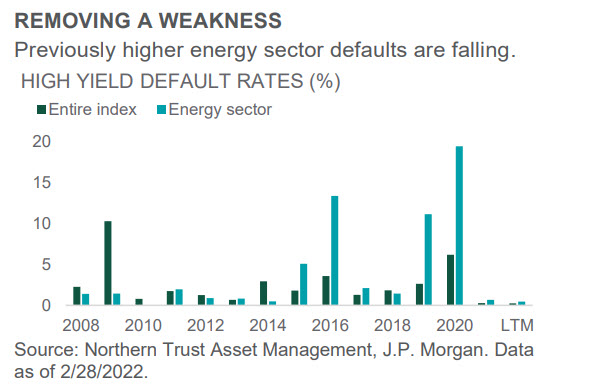

With the Russian invasion of Ukraine, already-elevated oil prices rapidly rose to the highest levels seen in 13 years, driving further inflation pressures. High energy prices can put strains on margins for the overall economy, but the high yield market is better positioned with greater exposure to energy versus other asset classes. Energy makes up roughly 13% of high yield, while only 8% for investment grade and 4% of the S&P 500. The energy default rate has exceeded the overall high yield market in 6 of the past 7 years (see chart). Historically, energy default rates have been a headwind for the high yield market with half of defaults since 2010 coming from the energy sector.

However, with rapidly rising energy prices, it’s likely the energy default rate will continue to trend lower, further supporting the overall high yield market with default rates at all-time lows. A higher energy sector weighting in high yield should also allow for a better hedge against rising energy prices and volatility in other asset classes. This dynamic has provided support for high yield valuations and continued interest in the asset class. High yield remains the largest overweight in our global policy model.

EQUITIES

- Global equities have been hit by the escalating situation in Ukraine – notably European equities.

- Wars are unpredictable with binary outcomes; “dry powder” is ready to deploy should the outlook improve.

- We are neutral traditional equities; overweights to U.S. equities offset underweights in the rest of the world.

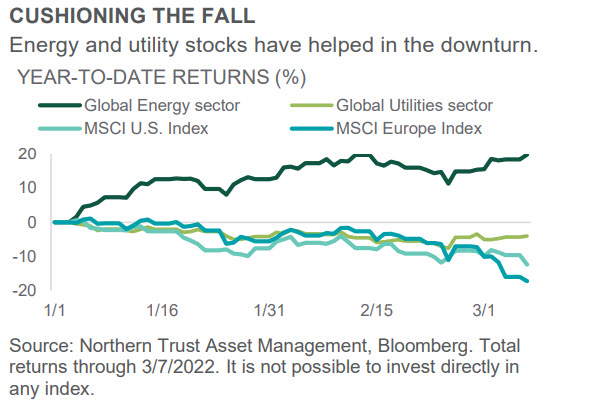

Global equities were heavily impacted by the Russian invasion of Ukraine over the past 30 days, losing 7.7% for the month. On the year, they are now down 12.5%. Given the negative impact of the crisis in Ukraine on the outlook for economic growth and inflation, notably in Europe, the market reaction is understandable – especially since we currently don’t have a clear line of sight on the resolution of the conflict. We are in a very uncertain situation, facing multiple possible scenarios with potentially big implications for financial markets. This was reflected in the equity markets through the underperformance of Europe (down over 15%) and the outperformance of Energy and Utility stocks (and by extension Value vs. Growth).

In reaction to the developments in Ukraine, we have made several changes to our global policy model. Because Europe and emerging market equities are more directly exposed to the negative impacts, we lowered our allocations in both regions to an underweight position. We reallocated that money to U.S. assets, both equity and high yield bonds, as well as inflation-linked bonds and cash. This lowers our risk position and provides dry powder should some sort of resolution allow for a turnaround in equity markets.

REAL ASSETS

- Russia’s Ukrainian invasion has had a large impact on a variety of commodities – from oil to wheat.

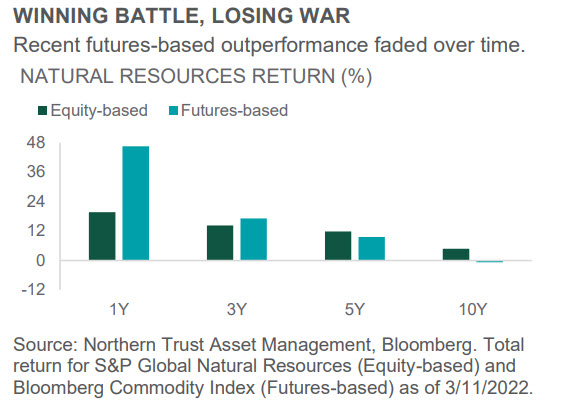

- While a futures-based approach has shown near-term strength, we believe an equity-based strategy is better long-term.

- We retain our natural resources overweight, which is currently providing a ballast to the risk asset portfolio.

Russia’s Ukrainian invasion has pushed up commodity prices in general but the agriculture and energy sectors have been hit hardest. Within agriculture, wheat prices have shot up 41% this year. The world faces the acute risk of falling production in both Russia (due to sanctions) and Ukraine (because of planting disruptions) but also faces a more general risk (for wheat prices globally, but also many other crops) given soaring fertilizer prices (pushed higher by rising energy costs to produce). Those rising energy prices are the result of curtailed production from Russia and Ukraine (for the same reasons as above), pushing natural gas and oil prices up 129% and 50%, respectively.*

Overall, broad commodity spot prices are up 27% year-to-date while the futures-based commodity index (investible and incorporating roll and collateral yield) is up 28%. This compares to the equity-based index return of 11%. While the futures-based strategy outperforms in the environment we find ourselves in (not held back by the increased equity risk premium priced into equities), a longer-term outlook favors an equity-based approach – just as it has historically (see chart). We retain our overweight to equity-based natural resources as a geopolitical and inflation hedge.

*Using U.S.-based natural gas and oil pricing as of March 2022.

- Jim McDonald, Chief Investment Strategist

IN EMEA AND APAC, THIS PUBLICATION IS NOT INTENDED FOR RETAIL CLIENTS

© 2022 Northern Trust Corporation.

The information contained herein is intended for use with current or prospective clients of Northern Trust Investments, Inc. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. This information is obtained from sources believed to be reliable, and its accuracy and completeness are not guaranteed. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor. Forward-looking statements and assumptions are Northern Trust's current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information. Investments can go down as well as up.

Northern Trust Asset Management is composed of Northern Trust Investments, Inc., Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K., NT Global Advisors, Inc., 50 South Capital Advisors, LLC, Belvedere Advisors LLC and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

Issued in the United Kingdom by Northern Trust Global Investments Limited.

© Northern Trust

Read more commentaries by Northern Trust